Recommended

PDF

자산관리관점에서 본 SME를 위한 FinTech

PDF

Fintech overview 페이게이트 박소영대표 20151006_v5

PDF

핀테크 포럼_이민화 교수_핀테크와금융민주화

PDF

PDF

핀테크(Fintech) 프리젠테이션

PPTX

PDF

PDF

PPTX

PDF

전자금융이 쌓아 온 금융아성, 핀테크가 뒤흔든다

PPT

PDF

규제 많은 미국이 핀테크를 선도하는 이유(Lgeri)

PDF

[한국핀테크포럼]150821 금융감독원 핀테크 해외진출 전략 세미나

PDF

금융과 It의 융합 핀테크(fin tech)의 사례와 원류

PDF

PDF

[와플세미나] 국내외 FinTech 동향20151104_김민호차장

PDF

PDF

PDF

PDF

PDF

국내 핀테크(Fintech) 산업의 현주소와 과제

PDF

PDF

PDF

PDF

국내 인터넷 결제 서비스 현황 및 개선방안(정보통신기술센터)

PDF

PDF

PDF

PDF

PDF

High frequency trading(우투증권)

More Related Content

PDF

자산관리관점에서 본 SME를 위한 FinTech

PDF

Fintech overview 페이게이트 박소영대표 20151006_v5

PDF

핀테크 포럼_이민화 교수_핀테크와금융민주화

PDF

PDF

핀테크(Fintech) 프리젠테이션

PPTX

PDF

PDF

What's hot

PPTX

PDF

전자금융이 쌓아 온 금융아성, 핀테크가 뒤흔든다

PPT

PDF

규제 많은 미국이 핀테크를 선도하는 이유(Lgeri)

PDF

[한국핀테크포럼]150821 금융감독원 핀테크 해외진출 전략 세미나

PDF

금융과 It의 융합 핀테크(fin tech)의 사례와 원류

PDF

PDF

[와플세미나] 국내외 FinTech 동향20151104_김민호차장

PDF

PDF

PDF

PDF

PDF

국내 핀테크(Fintech) 산업의 현주소와 과제

PDF

PDF

PDF

PDF

국내 인터넷 결제 서비스 현황 및 개선방안(정보통신기술센터)

PDF

PDF

Viewers also liked

PDF

PDF

PDF

High frequency trading(우투증권)

PDF

PDF

PDF

PDF

PDF

141022 핀테크(Fintech) 미니 컨퍼런스 임정욱 스타트업 얼라이언스 센ᄐ...

PDF

PDF

PDF

핀테크 기업조사- TransferWise, CurrencyCloud, TOSS

PDF

PDF

PDF

트랙킹 기술과 Information Privacy

PDF

PDF

구글 뉴스랩 펠로우십 2015/2016 미디어 파트너사 안내

PDF

PDF

국토․도시 및 개발 관련법령에서의 권한배분에 따른 현황고찰

PDF

구글 뉴스랩 펠로우십 2016/17 미디어 파트너사 안내

PDF

Similar to 핀테크(Fin tech): 거대한 디지털 격변의 현장

PPTX

PPTX

PDF

Fin tech and Fraud Detection System

PDF

20150317 세계일보 핀테크 - 금융과 IT 협업을 가로막는 법제도 장벽

PDF

PDF

PDF

핀테크를 통한 여신금융업계의 대응과 가치 창출 방안 여신금융 여름호 1508

PDF

Understanding FinTech & Case Study

PDF

핀테크 뉴스레터(무료)- 2015년 4월 27일자

PDF

산업간 융합 관점에서 본 핀테크 시사점(한국인터넷진흥원)

PDF

PDF

핀테크 뉴스레터(무료)- 2015년 4월 20일자

PDF

PDF

핀테크뉴스레터(무료)- 2015년 4월 13일자

PDF

PDF

PDF

PDF

PDF

180419 idean_entre_stripe

PDF

SD Lab* R&D* 핀테크 * 국내 전통 핀테크, 신생핀테크 서비스 현황 이해와 사용자 조사

핀테크(Fin tech): 거대한 디지털 격변의 현장 1. 2. 3. 우리는 (금융) 시스템을 새롭게 만들 기회를 가지고 있다. 금융

거래는 단지 숫자들에 불과하다, 금융 거래는 단지 정보다. 단

지 온라인 거래를 성사시키기 위해 10만 명의 사람과 뉴욕 맨

해튼의 값비싼 빌딩과 1970년식 (IBM) 메인프레임 (대형) 컴

퓨터로 가득찬 데이터 센터는 필요하지 않다.

“We have a chance to rebuild the system.

Financial transactions are just numbers; it’s just

information. You shouldn’t need 100,000 people

and prime Manhattan real estate and giant data

centers full of mainframe computers from the

1970s to give you the ability to do an online

payment."

3

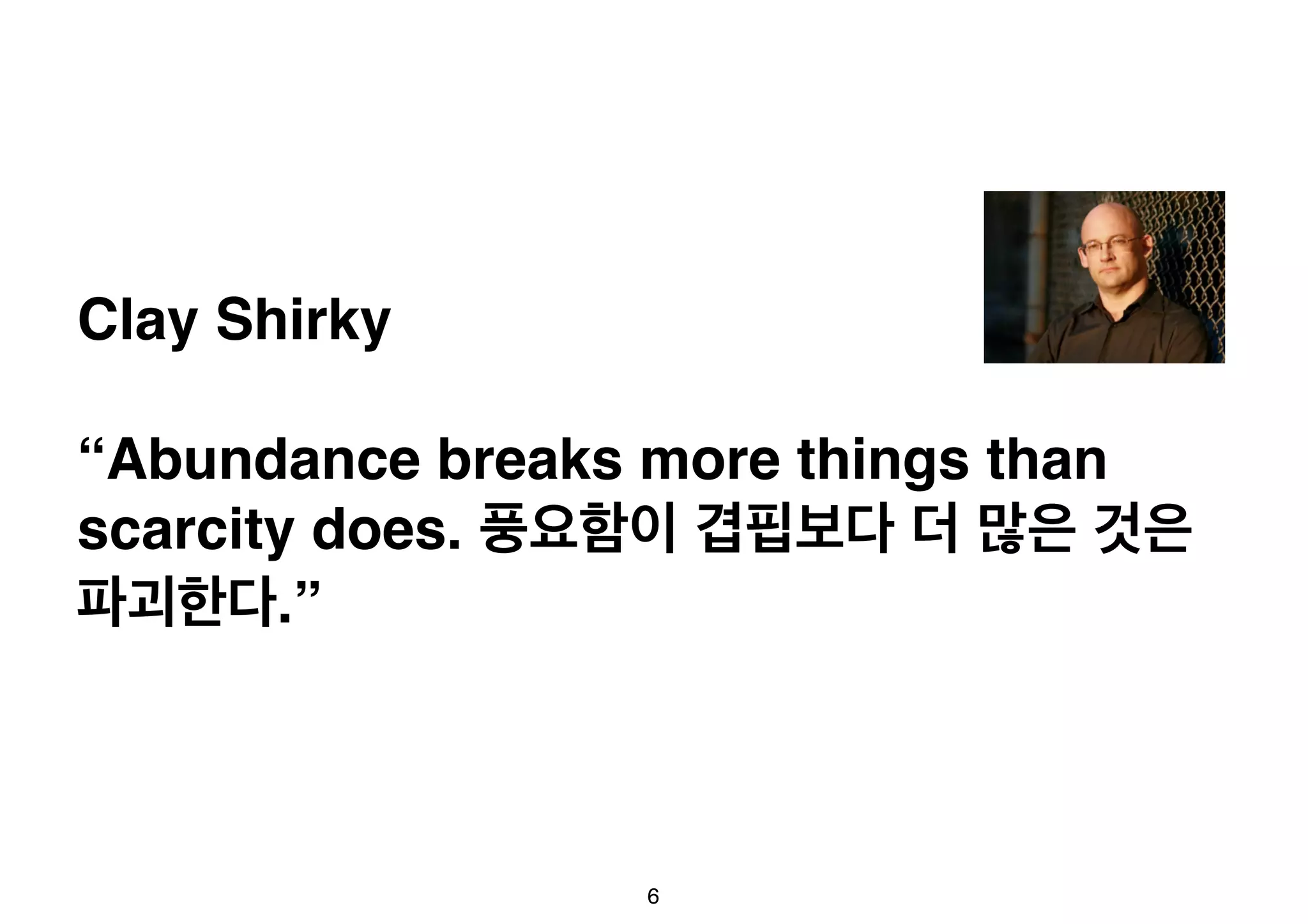

4. 5. Clay Shirky

“Institutions will try preserve the problem

to which they are the solution. 기관/조직/기

업은 자신(만)이 해답을 가지고 있는 문제가 해결되

지 않기를 추구한다.”

5

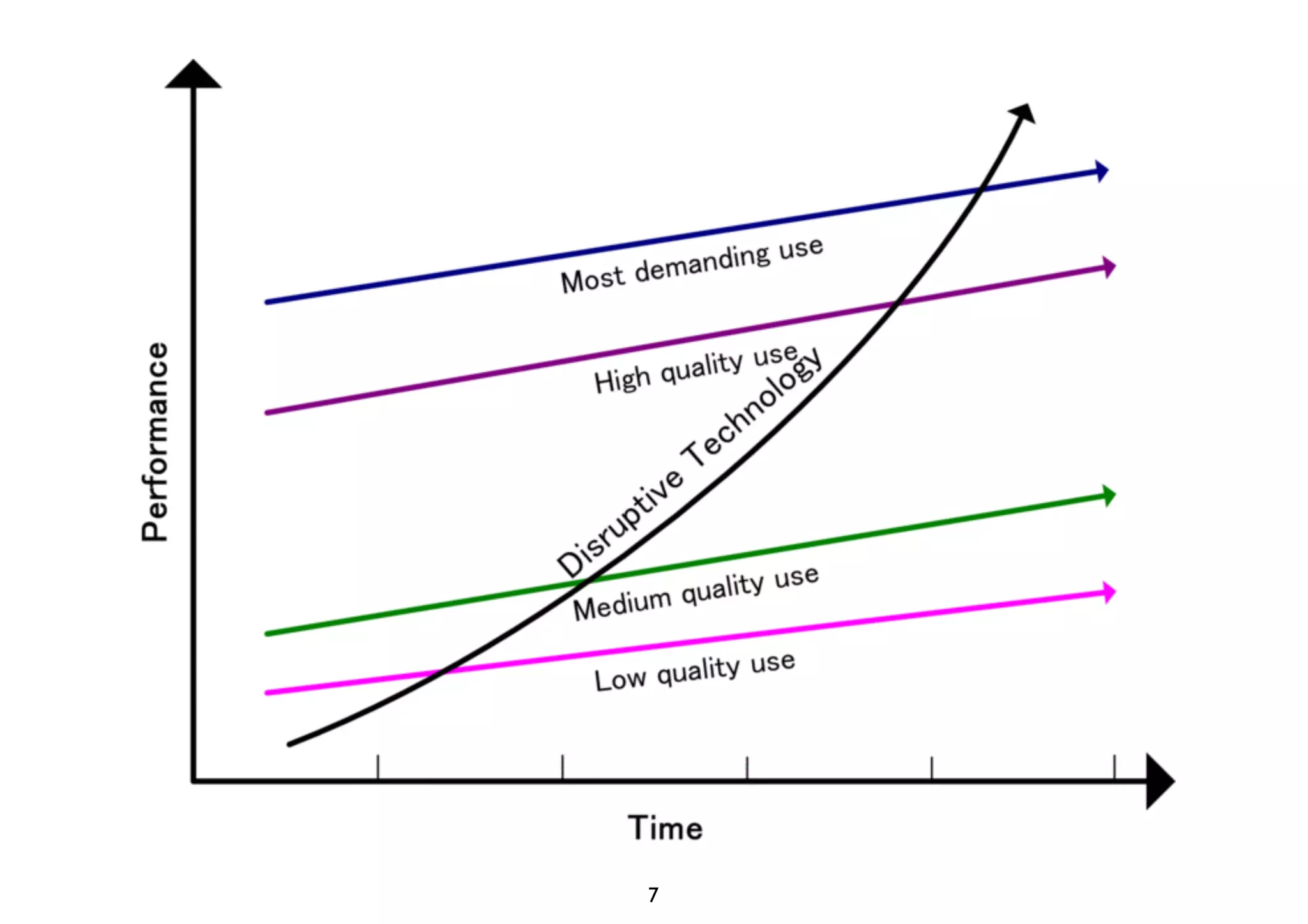

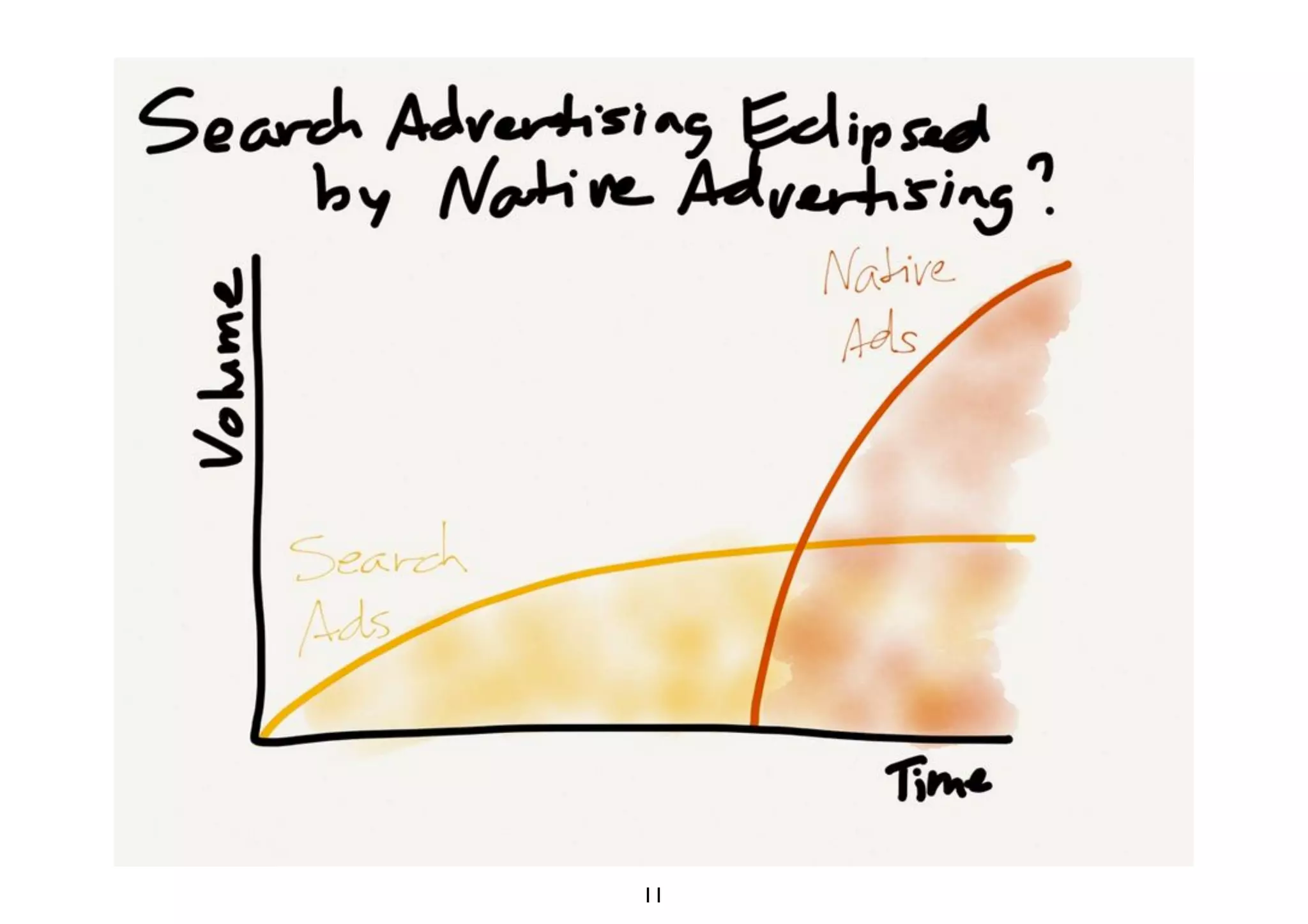

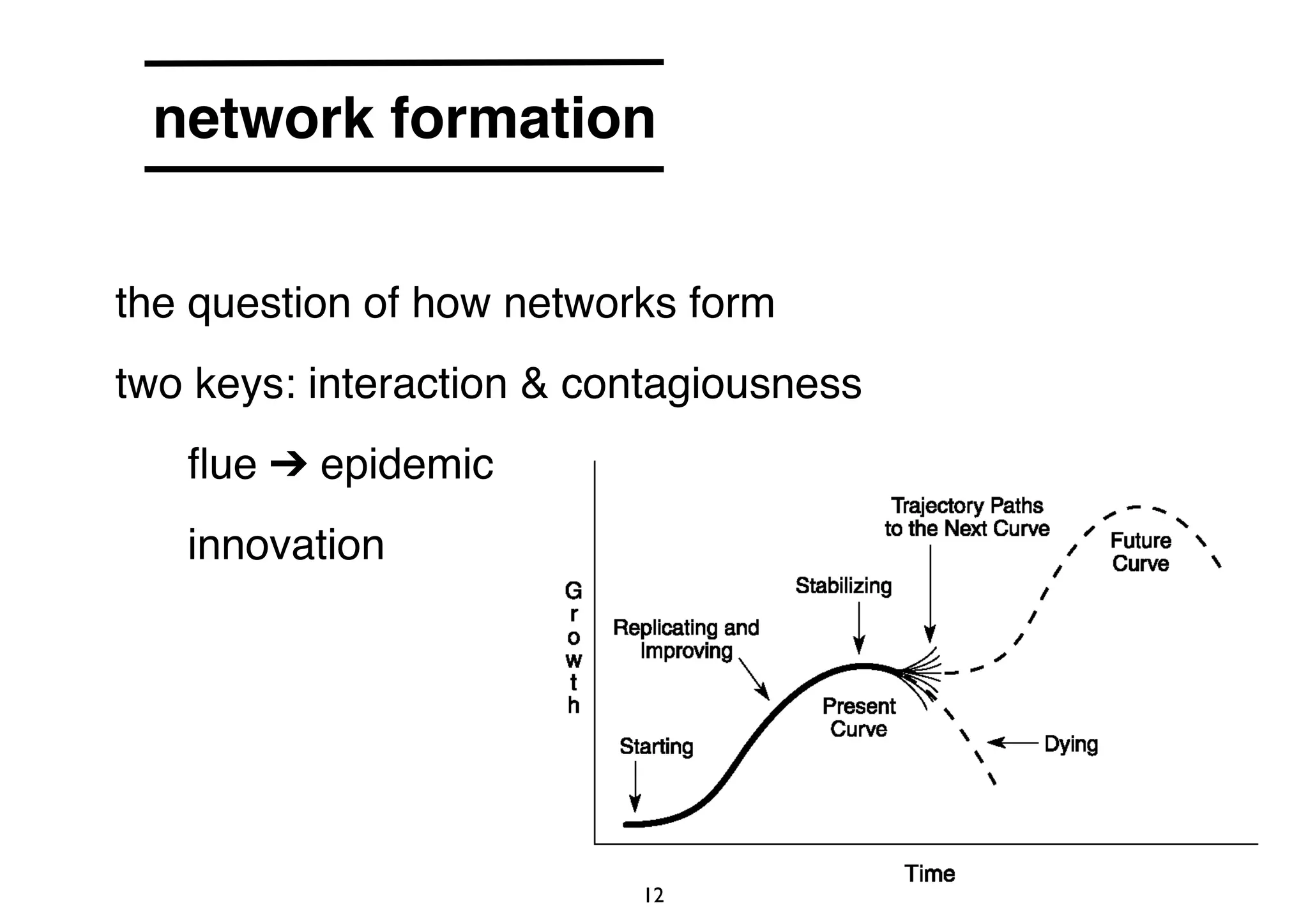

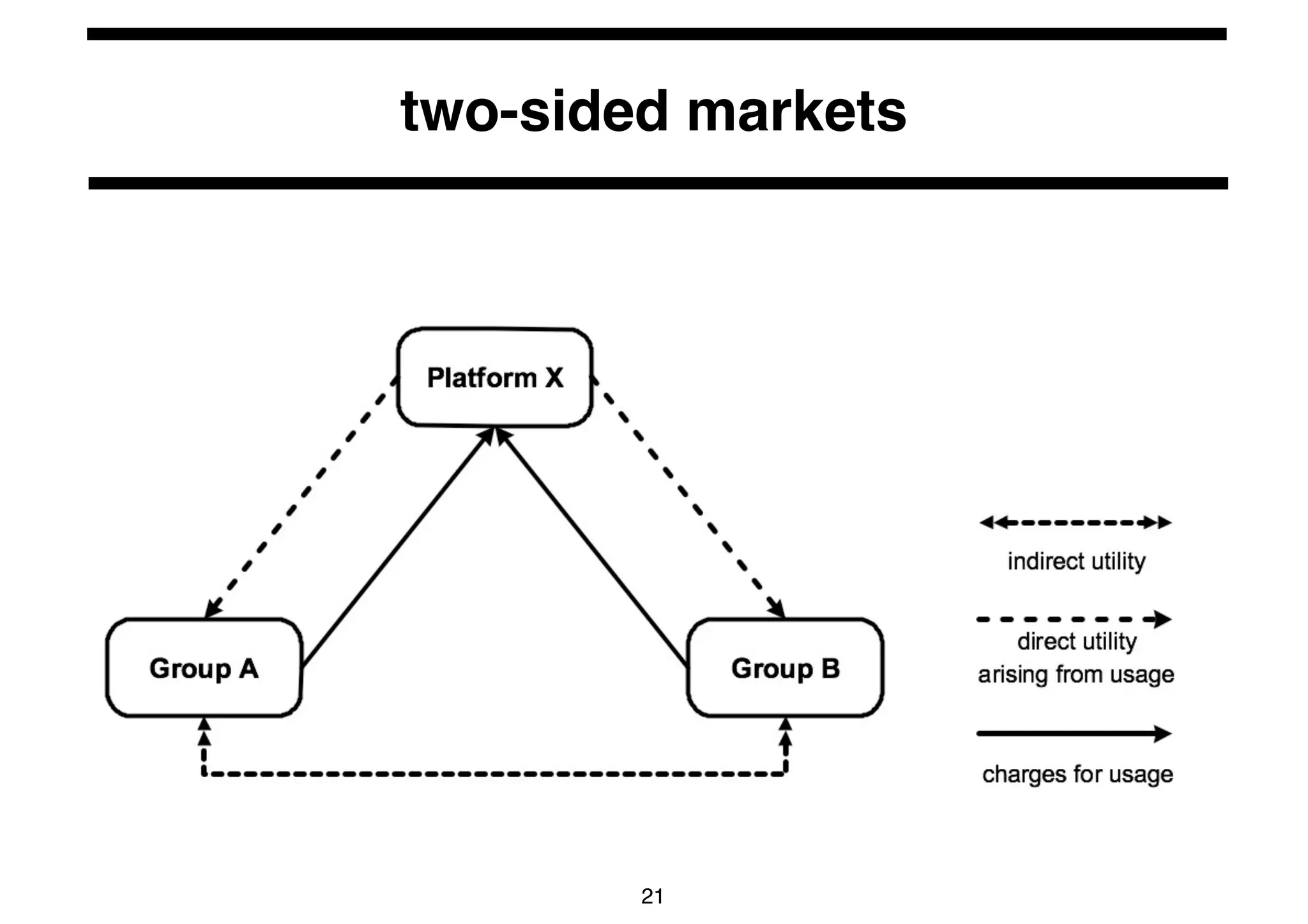

6. 7. 8. 9. 10. 11. 12. network formation

• the question of how networks form

• two keys: interaction & contagiousness

• flue ➔ epidemic

• innovation

12

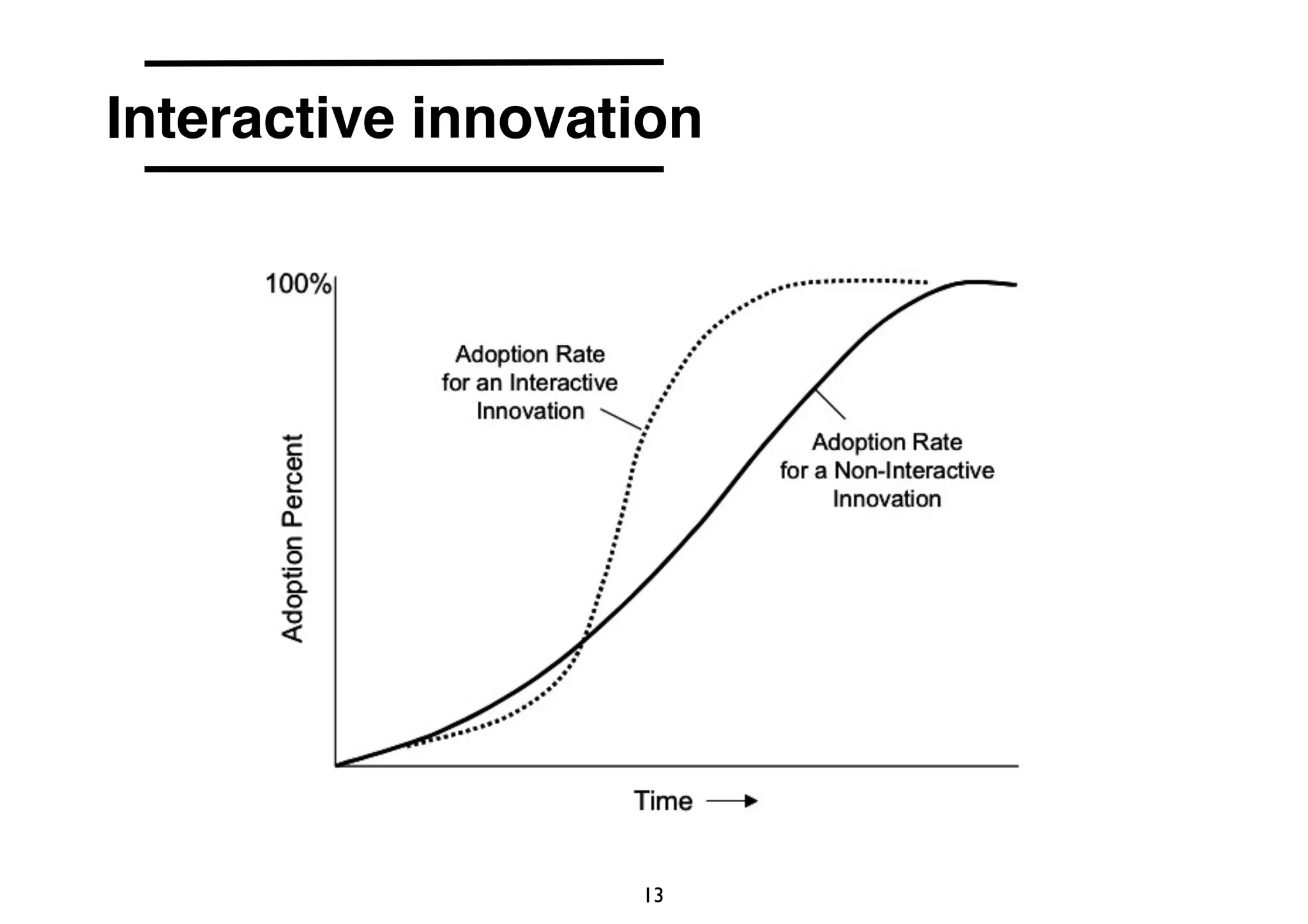

13. 14. 15. 16. 17. 17

경쟁은 선이고

독점은 악이다?

“disruptive

monopoly”

새로운 시장

= 사업자 1

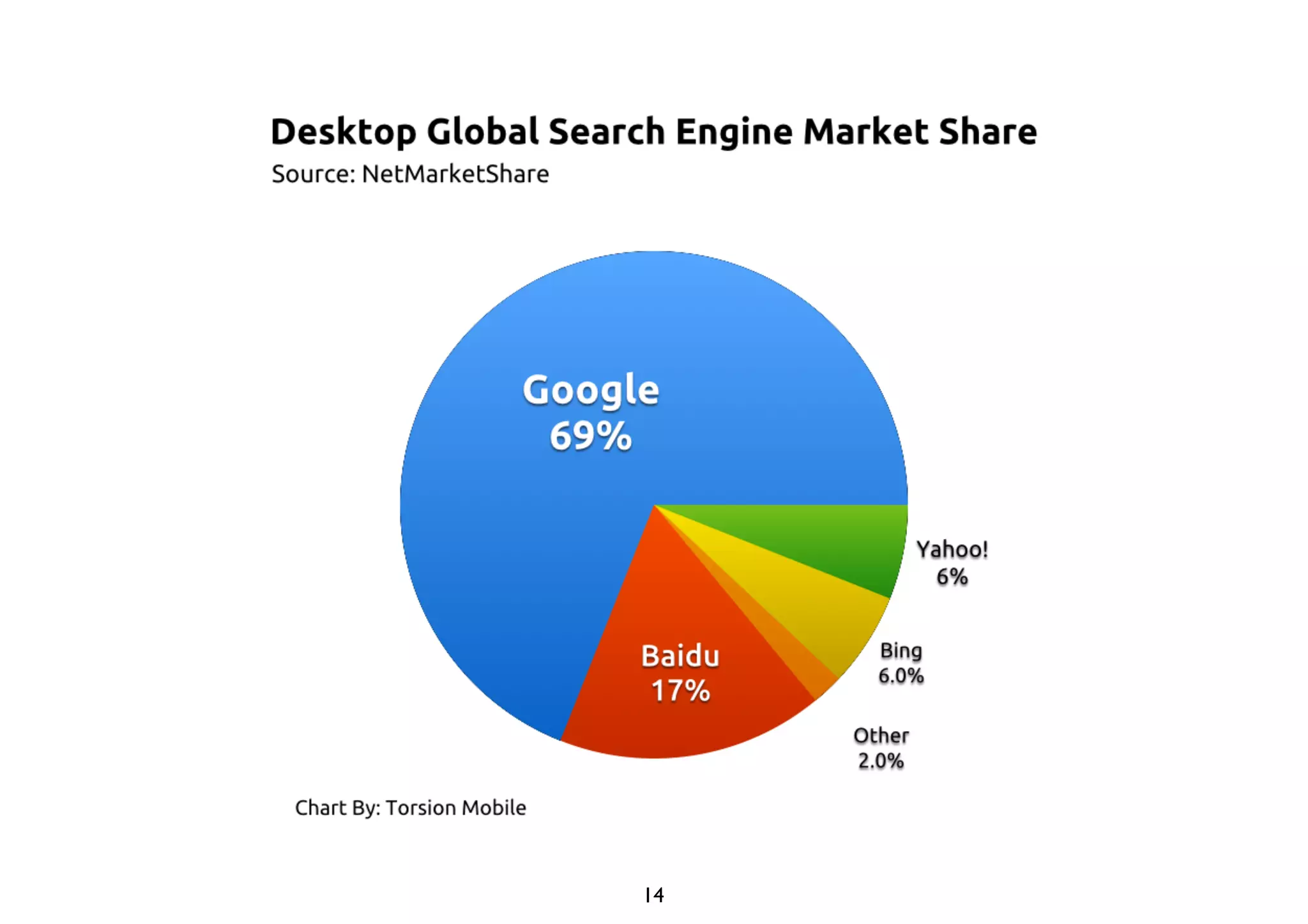

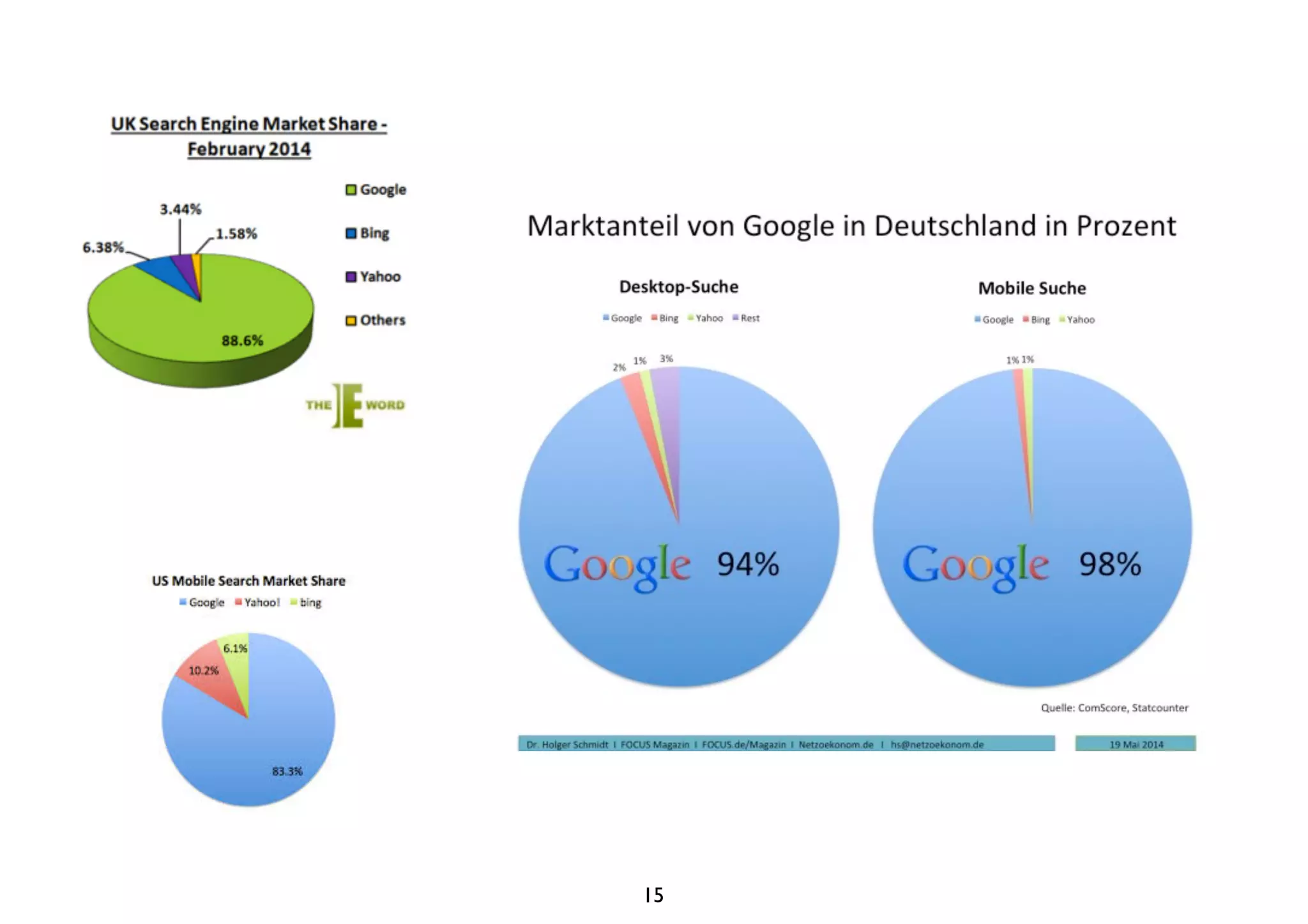

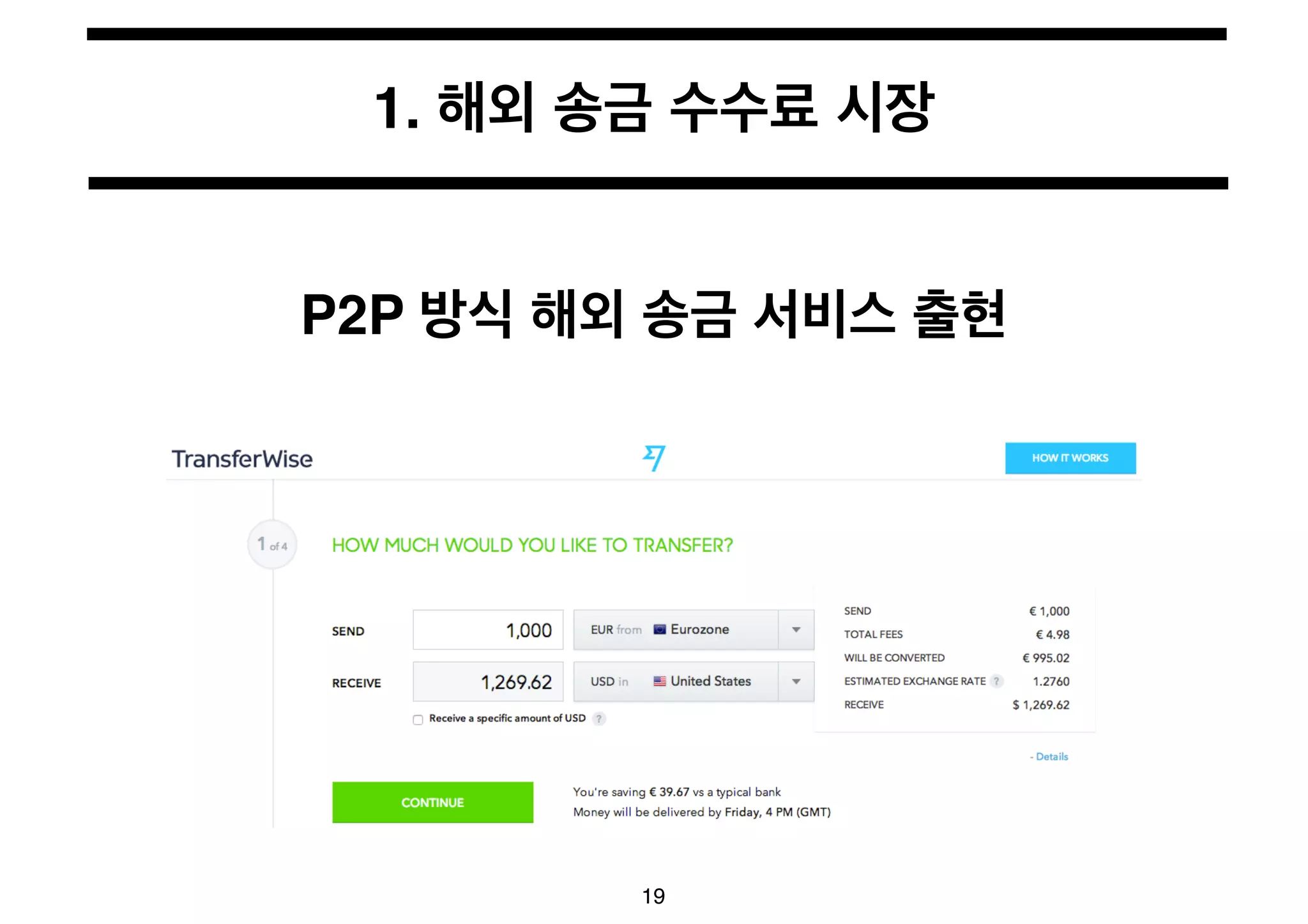

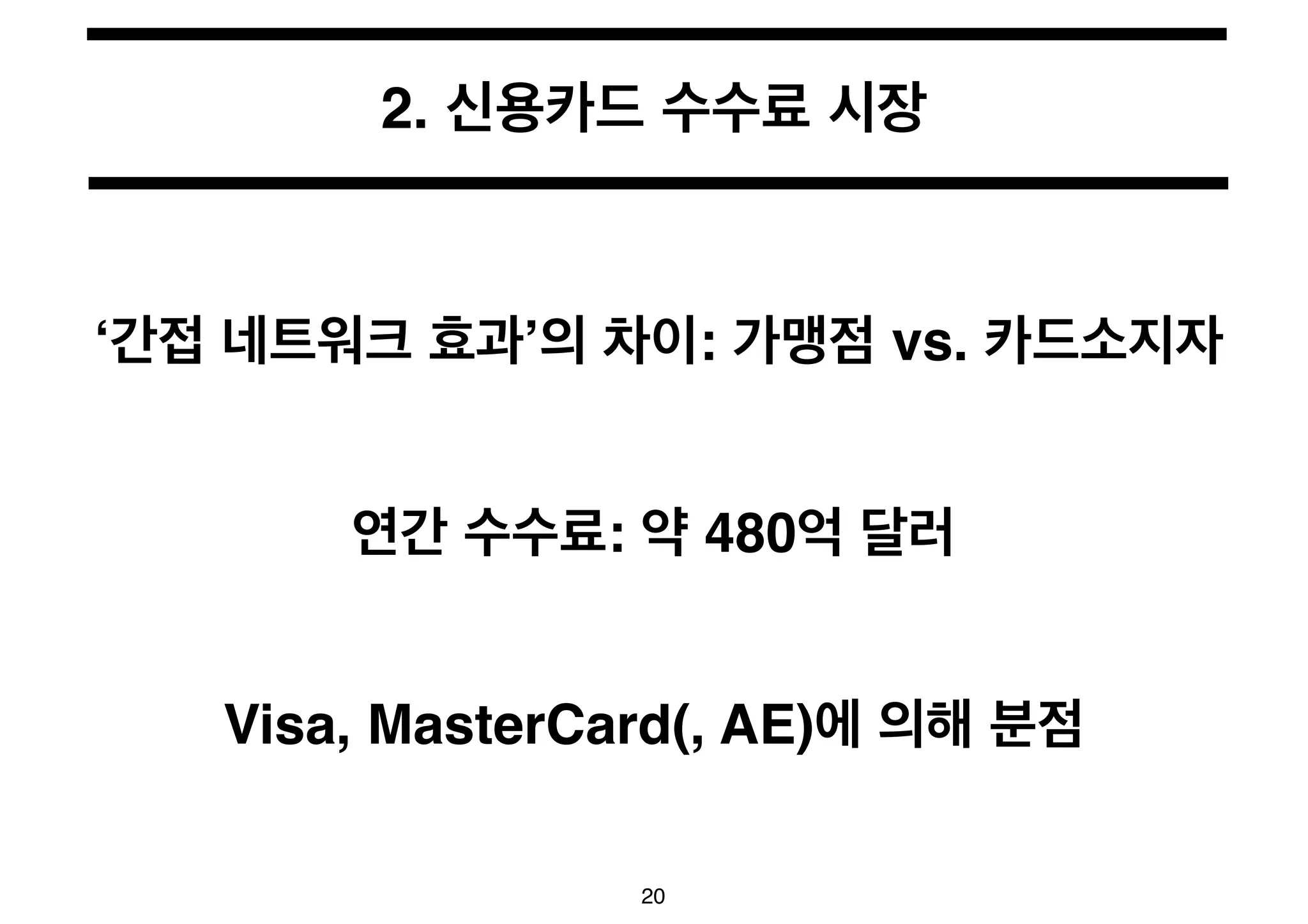

18. 19. 20. 2. 신용카드 수수료 시장

‘간접 네트워크 효과’의 차이: 가맹점 vs. 카드소지자

연간 수수료: 약 480억 달러

Visa, MasterCard(, AE)에 의해 분점

20

21. 22. 23. 3. Apple Pay vs. CurrentC

카드 소지자 vs. 가맹점

애플 vs. 월마트

Penguin Phase? Chicken & Egg Problem?

23

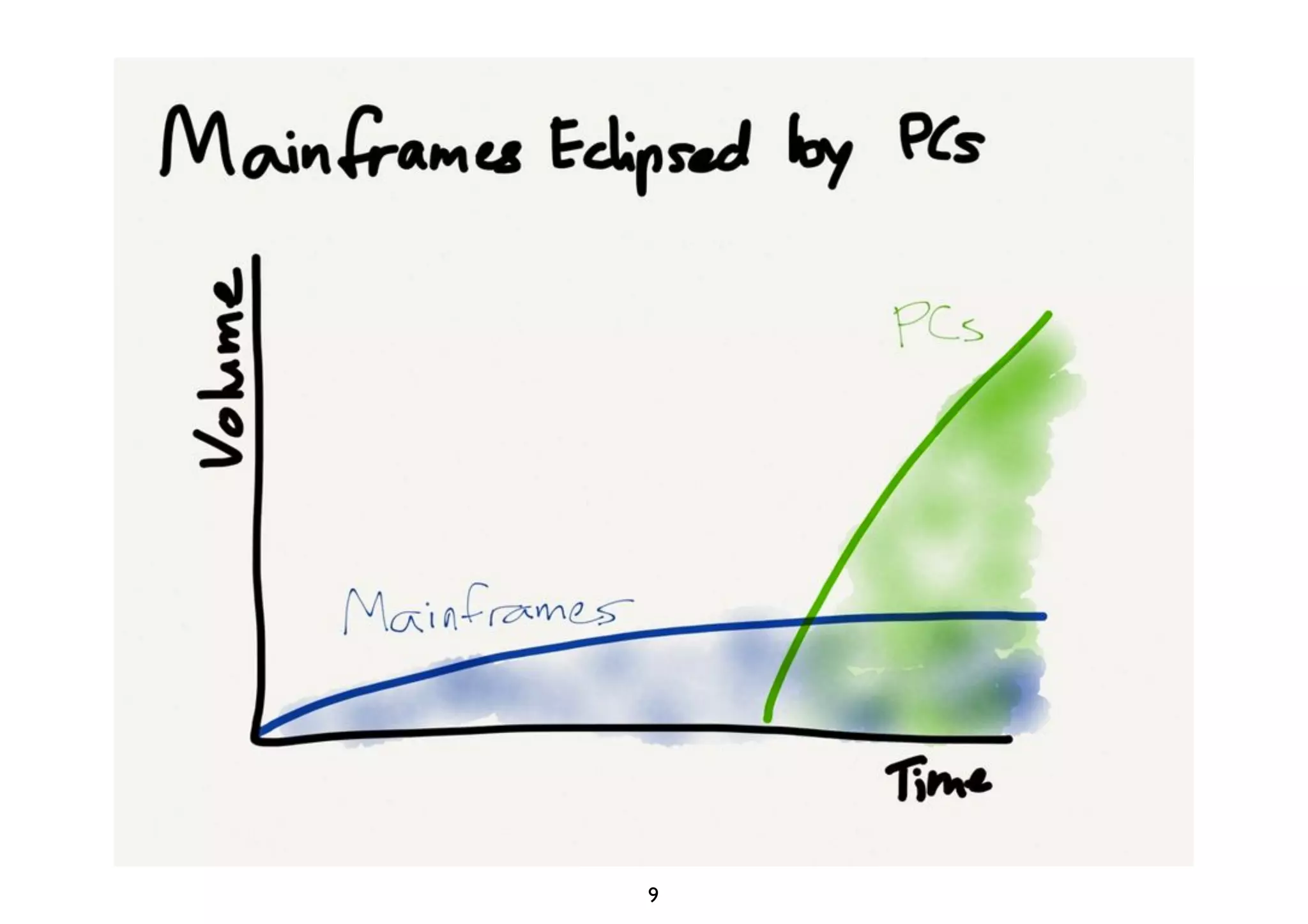

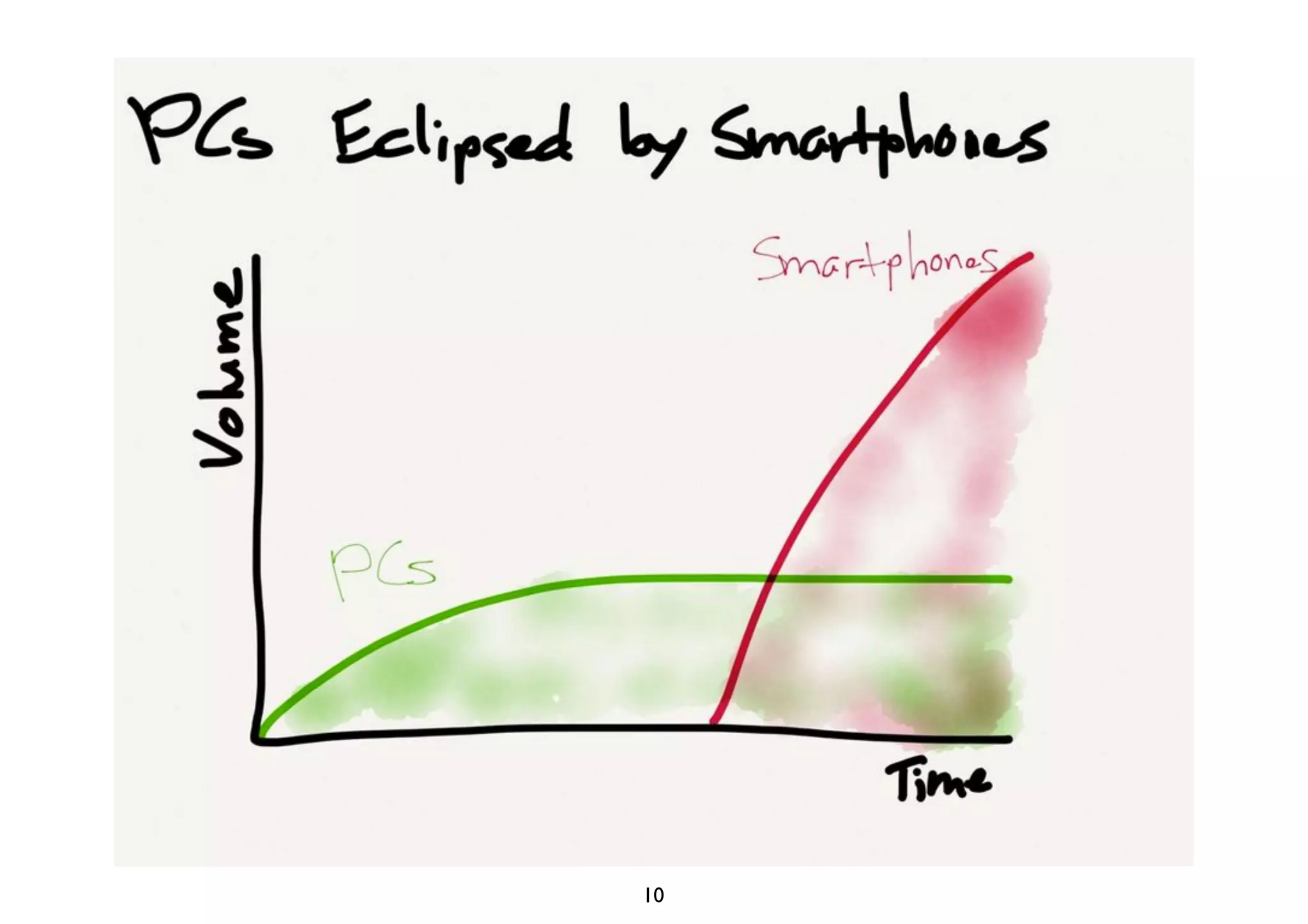

24. 4. Google as a Bank

구글, 2007년 영국에서 은행 사업권 획득

전통 은행 서비스와 다른 은행 서비스란?

Bank as s Platform?

24

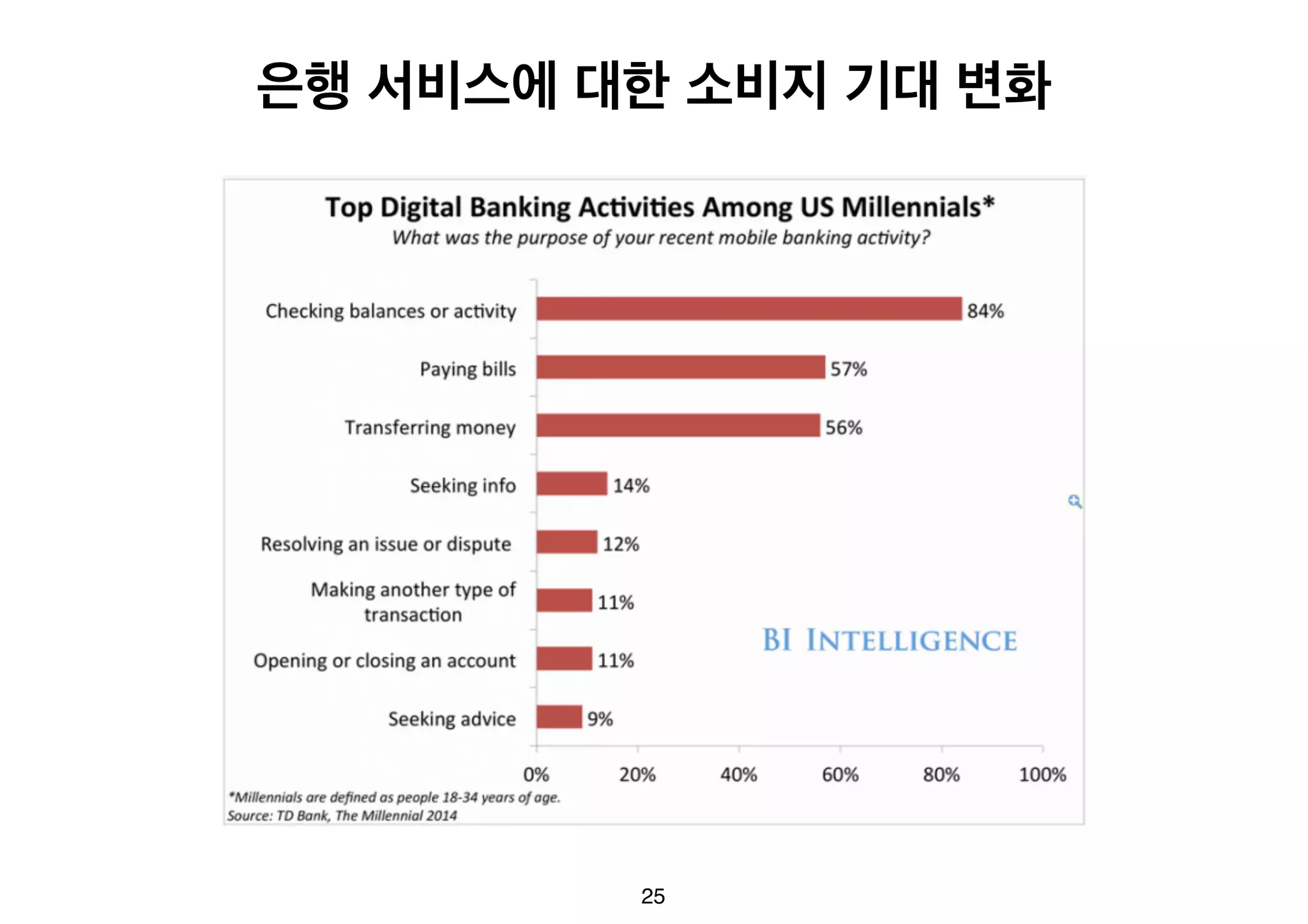

25. 26. 27. 28.

![[한국핀테크포럼]150821 금융감독원 핀테크 해외진출 전략 세미나](https://cdn.slidesharecdn.com/ss_thumbnails/sywork-2763271-v2-150828070951-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![[와플세미나] 국내외 FinTech 동향20151104_김민호차장](https://cdn.slidesharecdn.com/ss_thumbnails/20151104-fintech-151124094621-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![[한국핀테크포럼] 제6회 정기포럼](https://cdn.slidesharecdn.com/ss_thumbnails/random-150828080638-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![[1차]송금과 네이버페이(151003)](https://cdn.slidesharecdn.com/ss_thumbnails/1-151003-160216170955-thumbnail.jpg?width=640&height=640&fit=bounds)

![[도서 리뷰] 왜 지금 핀테크인가?](https://cdn.slidesharecdn.com/ss_thumbnails/whyfintech-181204100633-thumbnail.jpg?width=640&height=640&fit=bounds)