Downloaded 1,443 times

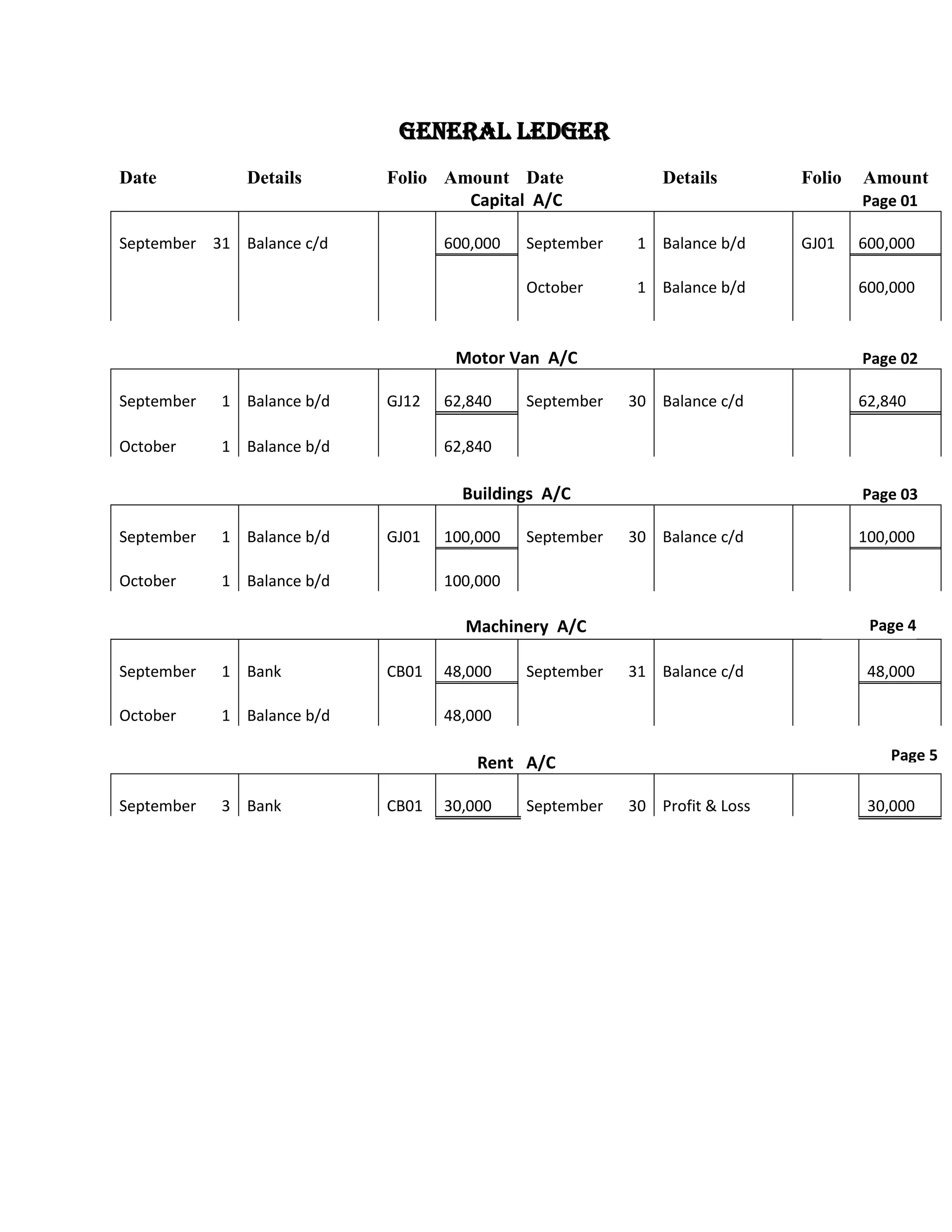

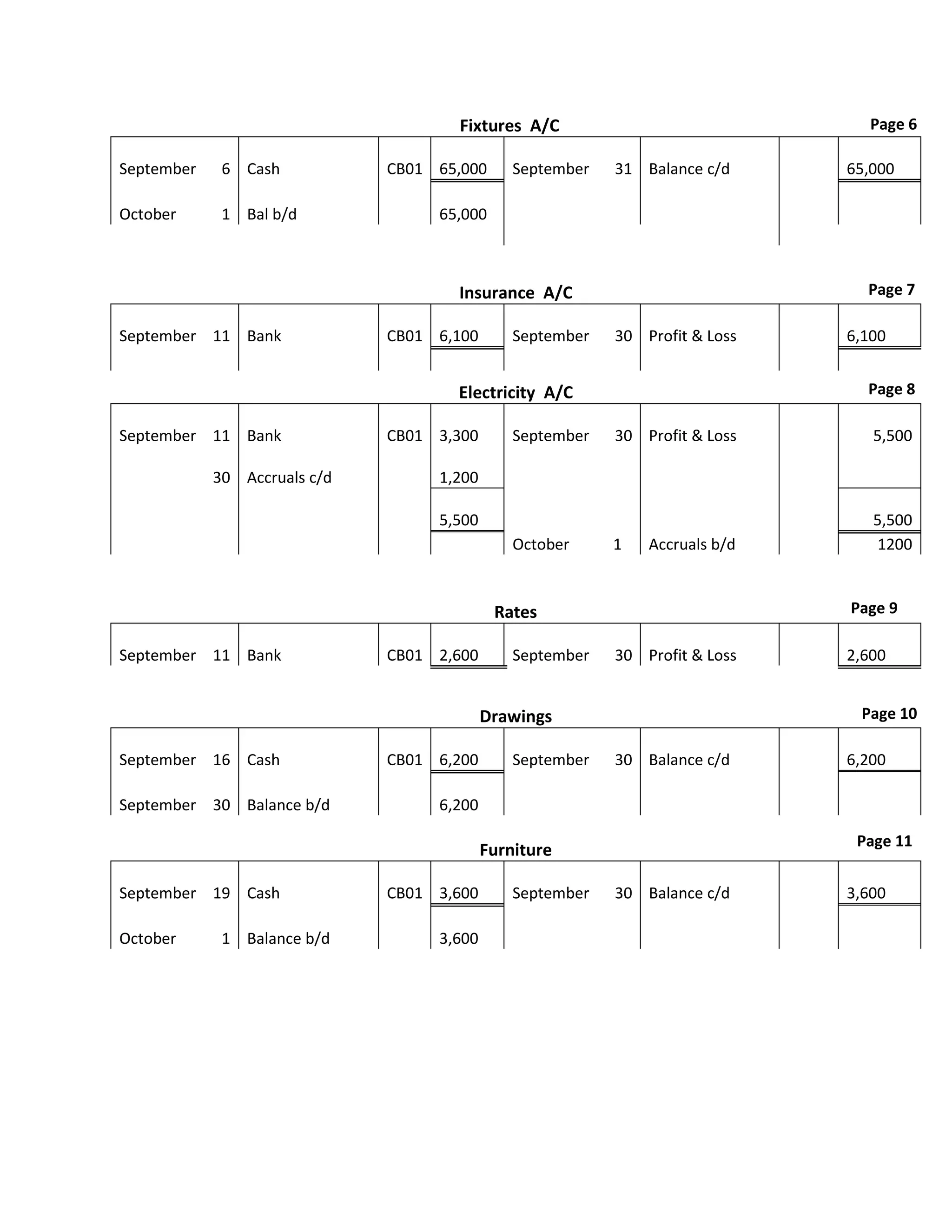

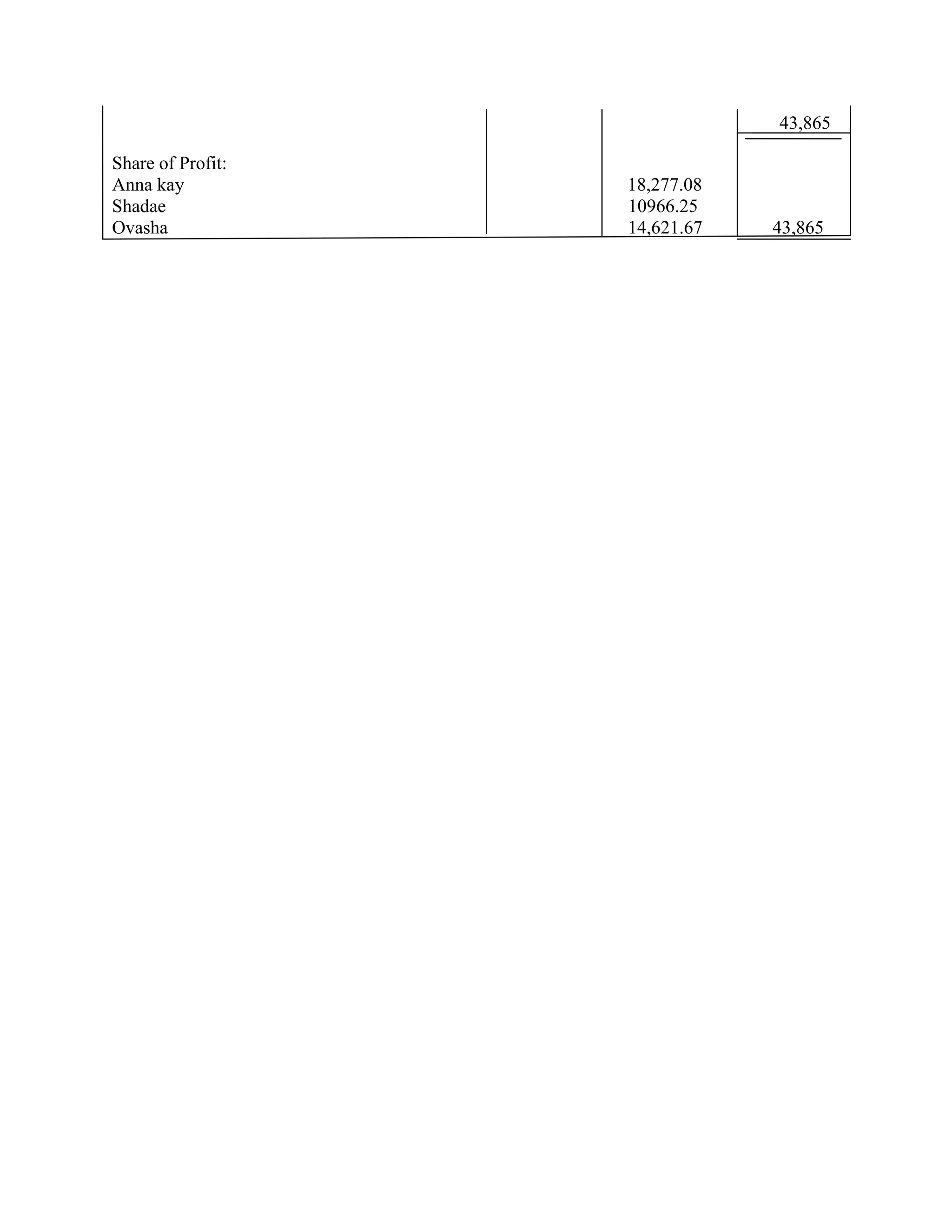

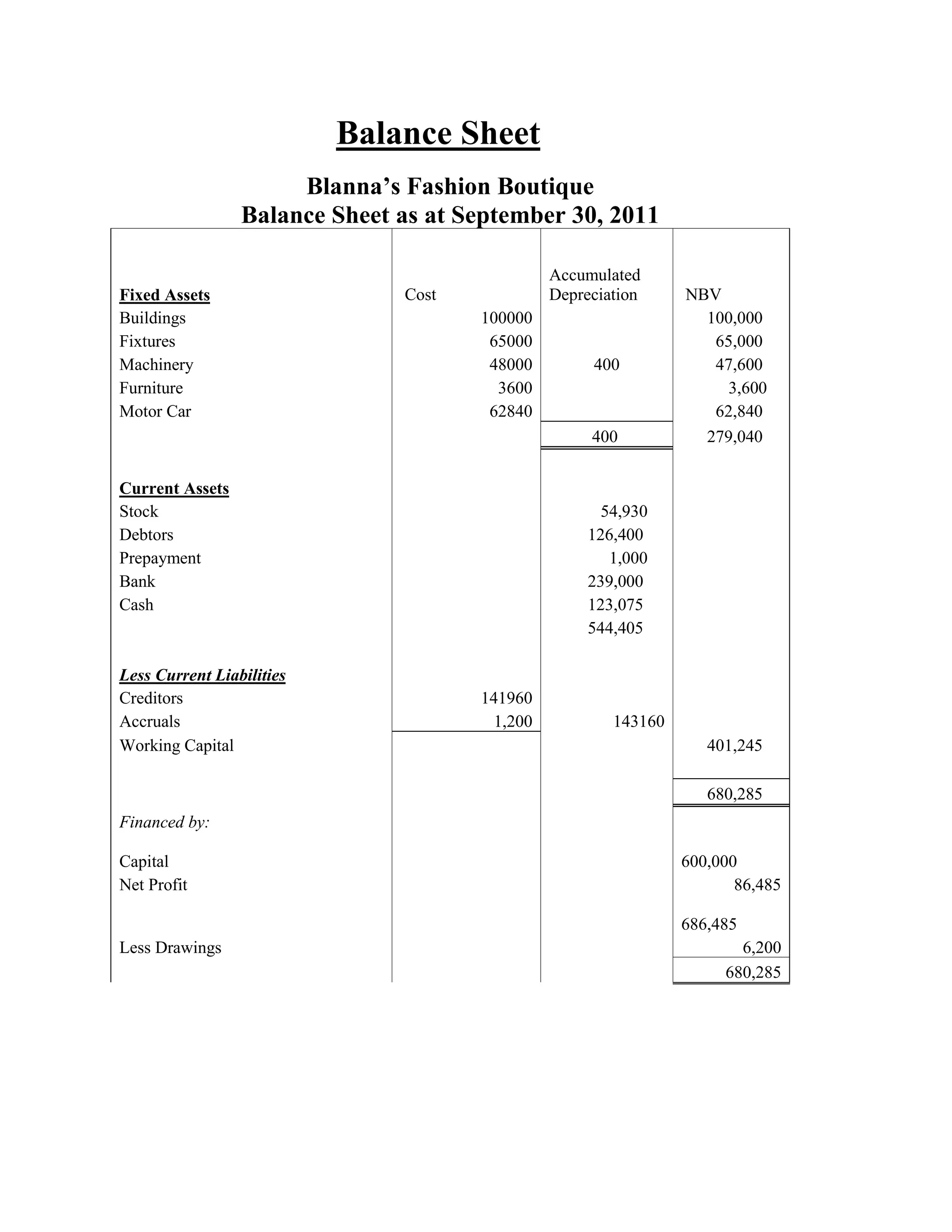

This document is an accounting project submitted by Anna Kay Blake for her Principles of Accounts certification. It contains the accounting records for Blanna's Fashion Boutique for the period ending September 30, 2011. The records include various journals, ledgers, trial balance, stock valuation and other financial statements that provide details of the business transactions and financial position of the boutique. The aim of the project is to demonstrate Anna's understanding of business accounting and to analyze the strengths and weaknesses of Blanna's Fashion Boutique.