1. Page 1 of 5

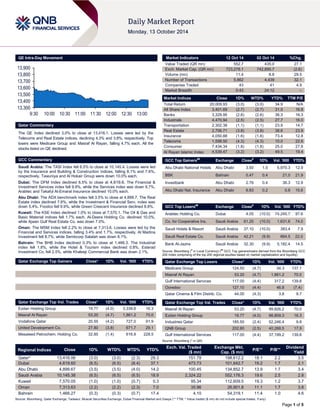

QE Intra-Day Movement

Qatar Commentary

The QE Index declined 3.0% to close at 13,416.1. Losses were led by the Telecoms and Real Estate indices, declining 4.3% and 3.8%, respectively. Top losers were Medicare Group and Masraf Al Rayan, falling 4.7% each. All the stocks listed on QE declined.

GCC Commentary

Saudi Arabia: The TASI Index fell 6.5% to close at 10,145.4. Losses were led by the Insurance and Building & Construction indices, falling 8.1% and 7.6%, respectively. Tawuniya and Al Hokair Group were down 10.0% each.

Dubai: The DFM Index declined 6.5% to close at 4,619.6. The Financial & Investment Services index fell 9.9%, while the Services index was down 9.7%. Arabtec and Takaful Al-Emarat Insurance declined 10.0% each.

Abu Dhabi: The ADX benchmark index fell 3.5% to close at 4,899.7. The Real Estate index declined 7.6%, while the Investment & Financial Serv. index was down 5.4%. Foodco fell 9.9%, while Green Crescent Insurance declined 8.8%.

Kuwait: The KSE Index declined 1.0% to close at 7,570.1. The Oil & Gas and Basic Material indices fell 1.7% each. Al-Deera Holding Co. declined 10.0%, while Ajwan Gulf Real Estate Co. was down 7.0%.

Oman: The MSM Index fell 2.2% to close at 7,313.6. Losses were led by the Financial and Services indices, falling 3.4% and 1.7%, respectively. Al Madina Investment fell 8.7%, while Sembcorp Salalah was down 8.1%.

Bahrain: The BHB Index declined 0.3% to close at 1,466.3. The Industrial index fell 1.8%, while the Hotel & Tourism index declined 0.8%. Esterad Investment Co. fell 2.5%, while Khaleeji Commercial Bank was down 2.1%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group

19.77

(4.0)

3,339.6

16.3 Masraf Al Rayan 53.20 (4.7) 1,861.2 70.0

Vodafone Qatar

20.55

(4.2)

727.0

91.9 United Development Co. 27.80 (3.8) 671.7 29.1

Mesaieed Petrochem. Holding Co.

32.85

(1.4)

616.9

228.5

Market Indicators 12 Oct 14 02 Oct 14 %Chg.

Value Traded (QR mn)

552.7

435.0

27.1 Exch. Market Cap. (QR mn) 723,278.1 742,895.7 (2.6)

Volume (mn)

11.4

8.8

29.5 Number of Transactions 5,862 4,439 32.1

Companies Traded

43

41

4.9 Market Breadth 0:43 24:12 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return

20,009.93

(3.0)

(3.0)

34.9

N/A All Share Index 3,401.69 (2.7) (2.7) 31.5 16.8

Banks

3,329.95

(2.6)

(2.6)

36.3

16.3 Industrials 4,470.94 (2.5) (2.5) 27.7 16.0

Transportation

2,302.38

(1.1)

(1.1)

23.9

14.7 Real Estate 2,706.71 (3.8) (3.8) 38.6 23.9

Insurance

4,050.88

(1.6)

(1.6)

73.4

12.8 Telecoms 1,598.50 (4.3) (4.3) 10.0 22.6

Consumer

7,434.34

(1.8)

(1.8)

25.0

27.8 Al Rayan Islamic Index 4,539.47 (3.2) (3.2) 49.5 19.4

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Abu Dhabi National Hotels

Abu Dhabi

3.50

1.5

5,970.3

12.9 BBK Bahrain 0.47 0.4 21.0 21.9

Investbank

Abu Dhabi

2.76

0.4

36.3

12.9 Abu Dhabi Nat. Insurance Abu Dhabi 6.83 0.2 0.8 15.6

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Arabtec Holding Co.

Dubai

4.05

(10.0)

74,245.7

97.6 Co. for Cooperative Ins. Saudi Arabia 61.25 (10.0) 1,631.6 74.0

Saudi Hotels & Resort

Saudi Arabia

37.10

(10.0)

383.4

7.9 Saudi Real Estate Co. Saudi Arabia 42.21 (9.9) 664.5 22.0

Bank Al-Jazira

Saudi Arabia

32.30

(9.9)

5,182.4

14.5

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Medicare Group

124.50

(4.7)

34.3

137.1 Masraf Al Rayan 53.20 (4.7) 1,861.2 70.0

Gulf International Services

117.00

(4.4)

317.2

139.8 Ooredoo 127.10 (4.4) 46.8 (7.4)

Qatar Cinema & Film Distrib. Co.

44.00

(4.3)

3.8

9.7

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan

53.20

(4.7)

99,826.2

70.0 Ezdan Holding Group 19.77 (4.0) 66,809.3 16.3

Industries Qatar

185.50

(2.4)

52,246.4

9.8 QNB Group 202.80 (2.5) 40,268.5 17.9

Gulf International Services

117.00

(4.4)

37,199.2

139.8

Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield

Qatar*

13,416.06

(3.0)

(3.0)

(2.3)

29.3

151.79

198,612.2

18.1

2.2

3.5 Dubai 4,619.60 (6.5) (6.5) (8.4) 37.1 473.73 101,642.7 19.2 1.7 2.1

Abu Dhabi

4,899.67

(3.5)

(3.5)

(4.0)

14.2

100.45

134,852.7

13.9

1.7

3.4 Saudi Arabia 10,145.38 (6.5) (6.5) (6.5) 18.9 2,324.22 552,176.3 19.6 2.5 2.8

Kuwait

7,570.05

(1.0)

(1.0)

(0.7)

0.3

95.34

112,609.5

19.3

1.2

3.7 Oman 7,313.63 (2.2) (2.2) (2.3) 7.0 35.96 26,901.8 11.1 1.7 3.8

Bahrain

1,466.27

(0.3)

(0.3)

(0.7)

17.4

4.10

54,319.1

11.4

1.0

4.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,30013,40013,50013,60013,70013,80013,9009:3010:0010:3011:0011:3012:0012:3013:00

2. Page 2 of 5

Qatar Market Commentary

The QE Index declined 3.0% to close at 13,416.1. The Telecoms and Real Estate indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari shareholders.

Medicare Group and Masraf Al Rayan were the top losers, falling 4.7% each. All the stocks listed on QE declined.

Volume of shares traded on Sunday rose by 29.5% to 11.4mn from 8.8mn on Thursday. However, as compared to the 30-day moving average of 14.8mn, volume for the day was 23.5% lower. Ezdan Holding Group and Masraf Al Rayan were the most active stocks, contributing 29.4% and 16.4% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings

Earnings Releases Company Market Currency Revenue (mn)3Q2014 % Change YoY Operating Profit (mn) 3Q2014 % Change YoY Net Profit (mn) 3Q2014 % Change YoY Advanced Petrochemical Co. (APC) Saudi Arabia SR – – 197.0 37.3% 229.0 62.5% Almarai Co. (Almarai) Saudi Arabia SR – – 625.3 13.0% 539.4 13.4%

Oman United Insurance Co. (OUIC)*

Oman

OMR

34.7

2.8%

–

–

4.4

10.6% Al Anwar Ceramic Tiles Co. (AACT)* Oman OMR 22.5 5.9% – – 6.8 8.1%

Al Omaniya Financial Services (AOFS)

Oman

OMR

14.0

0.4%

–

–

4.3

6.5%

Source: Company data, DFM, ADX, MSM (* 9M2014 results)

News

Qatar

QNB Group posts impressive 9M2014 results, net profit up 12.6% YoY – QNB Group (QNBK) posted a net profit of QR8.0bn, up by 12.6% compared to last year. This was driven by operating income, which increased to QR11.7bn, up by 6.8% compared to 9M2013. Net interest income increased by 6.4% to reach QR9.1bn, with net fee and commission income and net gain from foreign exchange reaching QR1.6bn and QR0.6bn, respectively. The Group’s prudent cost control policy and strong revenue generating capability allowed it to maintain an efficiency ratio (cost to income ratio) of 20.9%. Total assets increased by 8.8% YoY to reach QR475bn, the highest ever achieved by the Group. This was the result of a strong growth rate of 8.1% in loans and advances which reached QR329bn. The Group was able to maintain the ratio of non-performing loans to gross loans at 1.6% with the coverage ratio reaching 124% in 9M2014. At the same time QNB Group increased customer funding by 6.4% to QR352bn. This led to a 93% loan to deposit ratio. The Group’s CAR on a Basel III basis stood at 15.0%, higher than the QCB’s minimum requirements. (Press Release)

QEWS posts QoQ and YoY growth in net profit – Qatar Electricity & Water Company (QEWS) reported a net profit of QR454.0mn for 3Q2014 (BBG consensus: QR408mn) resulting in an increase of 9.0% and 8.8% QoQ and YoY, respectively. Growth in net income was supported by other/miscellaneous income. Moreover, QEWS’ revenue touched QR812.1mn, 1.3% shy of our estimate (QR823.1mn). Revenue grew by 4.2% QoQ but was flattish YoY. (QE)

QNB Group: Qatar’s construction activity up 14.5% in 2Q2014 on infrastructure expansion – QNB Group (QNBK) said a 14.5% YoY expansion in local construction activity was seen in 2Q2014 on the back of major infrastructure projects in the country. QNBK said these include the new metro in Doha, major real estate projects such as Musheireb and Lusail, as well as new roads, highways and further expansion of the new

Hamad International Airport (HIA). In addition, transportation and communication increased by 11.8% YoY, predominantly owing to increased passenger flows through the new airport. Real GDP growth accelerated to 5.7% in 2Q2014, from a revised 5.4% in the previous quarter. Financials, real estate, and business services were the fastest growing sector (16.6% YoY in 2Q2014) as banking intermediation accelerated and real estate services were boosted by demand for housing for the growing population. In the future, the only gas project expected to add to growth is Barzan, which is only for domestic supply and should add incremental growth to hydrocarbon GDP annually during the 2015-23 period. (Gulf-Times.com)

IMF outlook acknowledges Qatar’s diversification story – According to the International Monetary Fund’s (IMF) October 2014 economic outlook, Qatar is expected to grow by 6.5% in 2014 and 7.7% in 2015, respectively. In the last forecast from the General Secretariat for Development Planning, Qatar had indicated that its economy is likely to grow 6.3% in 2014 and reach 7.8% in 2015. Brisk, double-digit expansion in the non-oil & gas economy is also expected in 2014 and 2015. Qatar’s economic growth picked up slightly to 5.7% on an annual basis in 2Q2014 as robust non-oil activity outweighed a decline in the hydrocarbon sector. The above economic trends indicate that the recent IMF outlook acknowledges the fact that Qatar’s non- hydrocarbon diversification is going to be the driver of its economic growth. As per the IMF outlook, Qatar is expected to have an annual inflation of 3.4% in 2014. Qatar’s inflation surged to 3.8% in August 2014 on rising rents and food prices. (Gulf-Times.com)

Final phase of HIA to be completed in three years – Qatar Airways (QA) Group CEO Akbar al-Baker said the final phase of the Hamad International Airport (HIA) will be completed over the next three years. He added that the final phase of work involves the extension of concourse D and E, which will have more boarding gates and extended facilities. According to HIA data, it Overall Activity Buy %* Sell %* Net (QR)

Qatari

72.60%

50.81%

120,493,224.81 Non-Qatari 27.39% 49.19% (120,493,224.81)

3. Page 3 of 5

serves more than 360,000 flights and 30mn passengers every year. (Gulf-Times.com)

New firm to launch taxis this week – Capital Taxis, the fourth franchisee of the Karwa, will hit the roads later this week providing a major boost to Qatar’s public transportation sector. Capital Taxis will be operated by Ibin Ajayan Group, a vehicle distributor firm in Qatar, handling a number of automotive brands including Ashok Leyland buses, Iveco buses and trucks, Skoda cars, Golden Dragon buses (China) and Clark forklifts among others. Ibin Ajayan consultant-CEO G Ravi Pillai said its taxi services would start with an initial batch of 50 cars, but would achieve the target of 500 vehicles set by regulators, Mowasalat, in about two months. (Gulf-Times.com)

International

European banks raise 35% more capital before ECB stress test – According to a report published by law firm Linklaters, banks in the Eurozone have raised 35% more capital ahead of the European Central Bank's (ECB) latest stress test than they had set aside before the 2011 ECB review. The Eurozone's 130 most important banks are set to find out on October 26 how they have fared in the ECB's landmark review, which is designed to remove lingering doubts about whether lenders have valued their assets properly and are strong enough to withstand another recession. Linklaters said the Eurozone banks have already raised €35bn ahead of the review, a figure that could rise to €50bn by the end of the year. The law firm's data also showed that just over one quarter of the 66 banks in the least capitalized jurisdictions had successfully raised capital in 2014. Meanwhile, ECB Governing Council Member Ewald Nowotny said the euro is likely to continue weakening against other major currencies. Nowotny said this was due to the difference in the ECB's monetary policy as compared to policies in the US and the UK. (Reuters)

Germany defensive as criticism of economic course mounts – German Finance Minister Wolfgang Schaeuble put on a brave face at the end of IMF meetings in Washington DC, dismissing suggestions that Berlin had come under pressure to shift its economic course. However, the reality is that Germany has not been so isolated over its policy prescriptions for Europe since the height of the Eurozone financial crisis. Schaeuble endured lectures from longtime critics such as Larry Summers, the former US Treasury Secretary, who accused Germany of leading Europe down a path of Japanese-style deflation with a misguided focus on budget consolidation. He also had to listen to advice from traditional allies such as Finland's Jyrki Katainen, a future vice president of the European Commission, who warned that Germany could not remain strong forever if it failed to invest more in its own infrastructure and education system. (Reuters)

Greece begins talks with IMF to end bailout – According to a Greek government official, Greece has begun talks for ending the International Monetary Fund (IMF) aid to the country, but will continue to have routine post-bailout reviews. The IMF is deeply unpopular in Greece for insisting on austerity cuts under the country’s €240bn EU/IMF bailout, and Prime Minister Antonis Samaras hopes that cutting ties with the IMF will help turn around his flagging political fortunes. The IMF's role in Greece after it leaves is expected to have political implications for the government, which is keen to portray the IMF departure as an end to supervision by the group, while the opposition says such a departure would only be in name. (Reuters)

Chinese exports rise to support economy amid property downturn – Exports from China rose more than estimated in September 2014, while its imports rebounded as global demand

helped underpin growth in the world’s second-largest economy. China’s customs administration said exports increased 15.3% YoY, compared with the 12% median estimate in a Bloomberg News survey. Imports rose 7%, against projections for a 2% decline, leaving a trade surplus of $31bn. China is benefiting from a steady recovery in the US, which bolsters an economy weighed down by a property slump and slowdown in industrial- output growth. Analysts forecast China’s expansion this year will moderate to 7.3% and to 7% in 2015, which are the slowest since 1990. (Bloomberg)

Regional

S&P: GCC Islamic finance industry to maintain rapid growth – According to Standard & Poor’s (S&P), the GCC Islamic finance industry is expected to maintain its rapid growth over the coming years despite mixed results across various sectors in 2014. The industry’s expansion is expected to be driven mainly by the GCC’s robust economic prospects, continued infrastructure needs and rising issuance from governments and government-related entities. Prospects for the Sukuk segment will be a key theme, which has already registered healthy volumes in 2014-YTD with $20.3bn worth of issuances in the GCC as of October 5, growing 27.3% YoY. S&P believes 2014 Sukuk issuance is on course for a 5% growth from last year. According to Stuart Anderson, Managing Director & Regional Head, Middle East, S&P, despite this growth, the industry remains a demand-driven market, with limited supply. The expansion of existing Islamic finance centers in the GCC region and a more transparent regulatory environment are critical to accelerate growth, he added. (GulfBase.com)

Vela vessel transferred to Bahri ownership – The National Shipping Company of Saudi Arabia (Bahri) announced that ‘Saiph Star’, a VLCC vessel in the Vela fleet, has been transferred to Bahri's ownership on October 8, 2014 for a cash consideration of SR344.55mn, and its name was changed to ‘Karan’. The remaining Vela vessels shall be transferred to Bahri on a staggered basis as per the vessel delivery schedule by the end of 2014. (Tadawul)

Almarai reports fire at Jeddah bakery plant – Almarai Company announced that on October 9, 2014 a fire incident occurred at one of its Western Bakeries plant in Jeddah. Western Bakeries is a wholly owned subsidiary of Almarai. There has been significant damage to that plant and the adjacent bakery plant on the same site was also affected. Meanwhile, Almarai’s BoD mandated the executive management to accelerate the company's plan to consolidate its Jeddah-based bakery facilities into a new site in King Abdullah Economic City in Rabigh as an alternative to the existing factories in Jeddah. (Tadawul)

Emaar’s BoD approves AED9bn cash dividend – Emaar Properties’ board of directors has approved a special cash dividend of AED9bn to be distributed to the company’s shareholders, taking the total value of dividends distributed in 2014 to over AED17.12bn. The total dividend value is about 250% of the par value of Emaar’s shares. The company will conduct an ordinary general meeting to seek the approval of its shareholders in distributing the special dividend. (GulfBase.com)

Eshraq to raise share capital by AED600mn – Abu-Dhabi listed Eshraq said the company plans to raise its capital by AED600mn, and has invited its shareholders to subscribe to the additional 600mn shares at AED1 each. This will bring the company’s total share capital to AED2.325bn from the earlier AED1.725bn. (GulfBase.com)

4. Page 4 of 5

EDB: Bahraini economy grew by 5.6% in 2Q2014 – According to Bahrain Economic Quarterly report issued by the Economic Development Board (EDB), Bahrain experienced overall YoY GDP growth of 5.6% in 2Q2014. On a QoQ basis, GDP grew 3.2% in 2Q2014. The non-oil sector grew by 4.7% YoY during 2Q2014, while the oil sector registered 9.3% growth. On a QoQ basis, the non-oil sector registered a rise of 3.0% and the oil sector registered a rise of 4.1% in 2Q2014. The report revealed that the hotels & restaurants as well as the transport & communications sectors were among the key drivers of growth within the non-oil economy for 2Q2014, where growth exceeded 10% in each of these sectors. (GulfBase.com)

KCB signs BHD7mn financing deal for Bahrain hospital – Khaleeji Commercial Bank (KCB) announced the signing of a new BHD7mn corporate financing deal for the construction of Al Salam Specialist Hospital in Bahrain. The financing will be utilized to finance the construction and equipping of the new hospital located in Riffa. (Bloomberg)

5. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg, *$ adjusted returns.

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Sep-10 Sep-11 Sep-12 Sep-13 Sep-14

QE Index S&P Pan Arab S&P GCC

(6.5%)

(3.0%)

(1.0%)

(0.3%)

(2.2%)

(3.5%)

(6.5%)

(8.0%)

(6.4%)

(4.8%)

(3.2%)

(1.6%)

0.0%

Saudi Arabia

Qatar

Kuwait

Bahrain

Oman

Abu Dhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD%

Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,223.09 0.0 0.0 1.4 DJ Industrial 16,544.10 0.0 0.0 (0.2)

Silver/Ounce 17.39 0.0 0.0 (10.7) S&P 500 1,906.13 0.0 0.0 3.1

Crude Oil (Brent)/Barrel (FM

Future)

90.21 0.0 0.0 (18.6) NASDAQ 100 4,276.24 0.0 0.0 2.4

Natural Gas (Henry

Hub)/MMBtu

3.86 0.0 0.0 (11.2) STOXX 600 321.62 0.0 0.0 (10.2)

LPG Propane (Arab Gulf)/Ton 95.00 0.0 0.0 (24.8) DAX 8,788.81 0.0 0.0 (15.7)

LPG Butane (Arab Gulf)/Ton 113.75 0.0 0.0 (16.7) FTSE 100 6,339.97 0.0 0.0 (8.9)

Euro 1.26 0.0 0.0 (8.1) CAC 40 4,073.71 0.00 0.0 (13.1)

Yen 107.66 0.0 0.0 2.2 Nikkei 15,300.55 0.0 0.0 (8.5)

GBP 1.61 0.0 0.0 (2.9) MSCI EM 989.87 0.0 0.0 (1.3)

CHF 1.04 0.0 0.0 (6.7) SHANGHAI SE Composite 2,374.54 0.0 0.0 10.8

AUD 0.87 0.0 0.0 (2.6) HANG SENG 23,088.54 0.0 0.0 (1.0)

USD Index 85.91 0.0 0.0 7.3 BSE SENSEX 26,297.38 0.0 0.0 25.6

RUB 40.37 0.0 0.0 22.8 Bovespa 55,311.59 0.0 0.0 5.3

BRL 0.41 0.0 0.0 (2.2) RTS 1,064.29 0.0 0.0 (26.2)

192.8

157.4

141.8