Downloaded 178 times

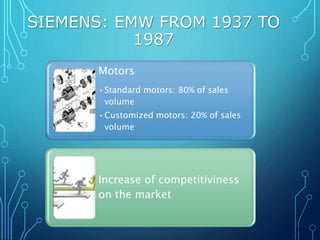

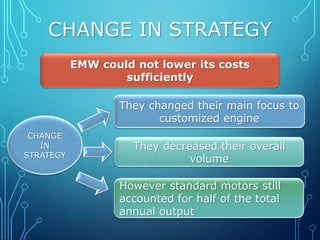

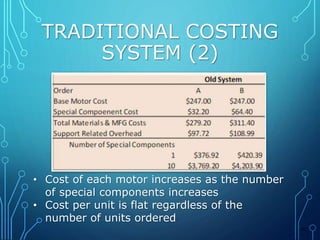

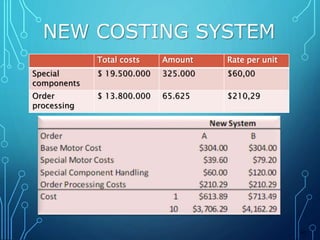

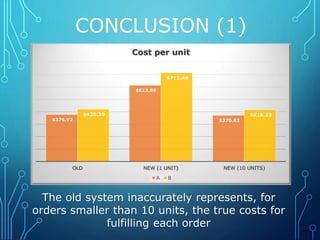

This document discusses Siemens Electric Motors' change to a new costing system. Previously, Siemens focused on standard motors but shifted strategy to customized motors. The traditional costing system did not properly allocate overhead costs. The new system separates overhead into special components costs and order processing costs pools. The director notes the new strategy would have failed without the improved costing system, which more accurately represents costs for small production runs.