Costi Industriali e Costi Variabili: 4. I vantaggi dell’ approccio della Contribuzione dei Costi

•

0 likes•360 views

Variabile versus Industriale https://www.manager.it/default.asp?page=A_contabilita.html

Recommended

More Related Content

What's hot

What's hot (10)

Similar to Costi Industriali e Costi Variabili: 4. I vantaggi dell’ approccio della Contribuzione dei Costi

Similar to Costi Industriali e Costi Variabili: 4. I vantaggi dell’ approccio della Contribuzione dei Costi (20)

More from Manager.it

More from Manager.it (20)

Recently uploaded

Recently uploaded (20)

Costi Industriali e Costi Variabili: 4. I vantaggi dell’ approccio della Contribuzione dei Costi

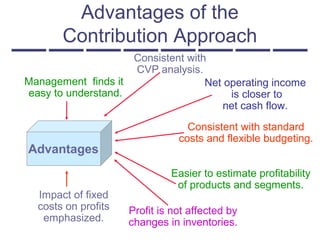

- 1. Advantages of the Contribution Approach Advantages Management finds it easy to understand. Consistent with CVP analysis. Net operating income is closer to net cash flow. Profit is not affected by changes in inventories. Consistent with standard costs and flexible budgeting. Impact of fixed costs on profits emphasized. Easier to estimate profitability of products and segments.

- 2. Fixed costs are not really the costs of any particular product. Variable Costing Variable versus Absorption Costing Absorption Costing All manufacturingAll manufacturing costs must be assignedcosts must be assigned to products to properlyto products to properly match revenues andmatch revenues and costs.costs.

- 3. Absorption Costing These are capacity costs and will be incurred even if nothing is produced. Variable versus Absorption Costing Variable Costing Depreciation, taxes, insurance and salaries are just as essential to products as variable costs.

- 4. Variable Costing Absorption costing product costs are misleading for decision making. They are the numbers that appear on our external reports. Absorption Costing Variable versus Absorption Costing

- 5. Note on the Effects of Volume Variable cost $10 Fixed manufacturing overhead $100,000 Units sold 10,000 Units Produced Total Variable Cost Fixed Manufacturing Overhead Total Manufacturing Cost Average Manufacturing Cost Cost of Goods Sold 10,000 $100,000 $100,000 $200,000 20.00$ 200,000$ 12,000 $120,000 $100,000 $220,000 18.33$ 183,333$ 14,000 $140,000 $100,000 $240,000 17.14$ 171,429$ 16,000 $160,000 $100,000 $260,000 16.25$ 162,500$ 18,000 $180,000 $100,000 $280,000 15.56$ 155,556$ 20,000 $200,000 $100,000 $300,000 15.00$ 150,000$ Absorption Costing Cost of goods sold decreases because production exceeds sales, leaving a portion of fixed manufacturing costs in inventory.

- 6. Note on the Effects of Volume COGS for 10,000 units $100,000 $150,000 $200,000 10,000 14,000 18,000 22,000 26,000 30,000 34,000Number of units produced COGS Absorption Costing Cost of goods sold decreases because production exceeds sales, leaving a portion of fixed manufacturing costs in inventory.

- 7. Impact of JIT Inventory Methods In a JIT inventory system . . . Production tends to equal sales . . . So, the difference between variable and absorption income tends to disappear.