Recommended

More Related Content

What's hot

What's hot (20)

Similar to Sunoco LP

Similar to Sunoco LP (20)

Sunoco LP

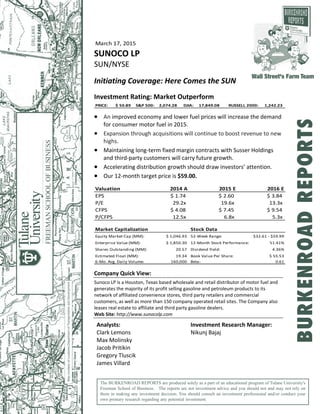

- 1. March 17, 2015 SUNOCO LP SUN/NYSE Initiating Coverage: Here Comes the SUN Investment Rating: Market Outperform PRICE: $ 50.89 S&P 500: 2,074.28 DJIA: 17,849.08 RUSSELL 2000: 1,242.23 An improved economy and lower fuel prices will increase the demand for consumer motor fuel in 2015. Expansion through acquisitions will continue to boost revenue to new highs. Maintaining long‐term fixed margin contracts with Susser Holdings and third‐party customers will carry future growth. Accelerating distribution growth should draw investors’ attention. Our 12‐month target price is $59.00. Valuation 2014 A 2015 E 2016 E EPS $ 1.74 $ 2.60 $ 3.84 P/E 29.2x 19.6x 13.3x CFPS $ 4.08 $ 7.45 $ 9.54 P/CFPS 12.5x 6.8x 5.3x Market Capitalization Stock Data Equity Market Cap (MM): $ 1,046.93 52‐Week Range: $32.61 ‐ $59.99 Enterprise Value (MM): $ 1,850.30 12‐Month Stock Performance: 51.41% Shares Outstanding (MM): 20.57 Dividend Yield: 4.36% Estimated Float (MM): 19.34 Book Value Per Share: $ 55.53 6‐Mo. Avg. Daily Volume: 160,000 Beta: 0.61 Company Quick View: Sunoco LP is a Houston, Texas based wholesale and retail distributor of motor fuel and generates the majority of its profit selling gasoline and petroleum products to its network of affiliated convenience stores, third party retailers and commercial customers, as well as more than 150 company operated retail sites. The Company also leases real estate to affiliate and third party gasoline dealers. Web Site: http://www.sunocolp.com Analysts: Investment Research Manager: Clark Lemons Nikunj Bajaj Max Molinsky Jacob Pritikin Gregory Tluscik James Villard The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment. Wall Street's Farm Team BURKENROADREPORTS

- 15. SUNOCO LP (SUN) BURKENROAD REPORTS (www.burkenroad.org) March 17, 2015 15 PEER ANALYSIS Sunoco LP operates within the gasoline and petroleum wholesale industry, as well as the motor fuel storage industry after the acquisition of Aloha Petroleum, Ltd. in 2014. The Company also transports motor fuel through a network of trucks, but does not operate in the pipeline transportation industry. Sunoco LP’s peer group includes similar companies involved in the downstream segment of the motor fuel value chain. The downstream segment includes the refining, distribution, and retail of gasoline and petroleum products. Sunoco LP’s peer group consists of: Delek US Holdings, Inc., Alon USA Energy, Inc., Global Partners LP, and CrossAmerica Partners LP. Although all these companies operate in the downstream segment of the value chain, some of these peers also operate within the refining and transportation segment of the motor fuel value chain. CrossAmerica Partners is Sunoco LP’s closest peer because its operations in the wholesale gasoline distribution and real estate holdings business resemble those of Sunoco LP. As Table 1 demonstrates, the Company’s peers all have market capitalizations within the range of $831 million and $2,282 million and all the companies have similar revenue with the exception of Global Partners LP. While Global Partners and CrossAmerica operate in different geographic locations, Sunoco LP intends to expand its operations to the east coast, thus justifying these companies’ inclusion in the peer group. Sunoco LP’s enterprise value to earnings before interest, taxes, and depreciation and amortization multiple (EV/EBITDA) and price to earnings ratio (P/E) are higher than most of its peers. While high EV/EBIDTA and P/E ratios can express overvaluation, they also demonstrate that investors feel the Company has potential for growth. The Company has a lower EV/EBITDA than its closest peer, CrossAmerica Partners, indicating that Sunoco LP is a more attractive choice to investors given the two companies’ operating models. Table 1: Peer Analysis Company Ticker (NYSE) Market Cap (MM) Revenue (MM) EV/ EBITDA Debt/ Equity ROE Div. Yield P/E Stock Price Sunoco LP SUN $2,282 $5,382 30.3 76.2% 9.3% 4.8% 27.6 $51.00 Delek US Holdings, Inc. DK $2,107 $8,324 4.5 58.9% 20.5% 1.7% 11.0 $36.28 Alon USA Partners LP ALDW $1,162 $3,221 5.1 139.4% 139.4% 15.1% 6.9 $18.54 Global Partners LP GLP $1,122 $18,532 7.8 189.4% 26.8% 7.3% 10.2 $34.85 Crossamerica Partners LP CAPL $831 $2,669 41.6 152.4% ‐4.5% 6.4% NEG $33.95 Average $1,501 $7,626 17.9 123.3% 38.3% 7.0% 13.9 Source: Thomson One March 12, 2015 (Last Twelve Months as of December 31, 2014)

- 17. SUNOCO LP (SUN) BURKENROAD REPORTS (www.burkenroad.org) March 17, 2015 17 MANAGEMENT PERFORMANCE AND BACKGROUND Sunoco LP’s management consists of executives with over 80 years of combined experience in the motor fuel industry. Each executive also has experience working for Susser Holdings, Susser Petroleum Partners LP, or Sunoco, Inc., all of which are owned by Sunoco LP’s parent corporation Energy Transfer Partners (ETP). Table 2: Return on Invested Capital of Peers Sunoco LP Delek US Holdings, Inc. Alon USA Partners LP Global Partners LP CrossAmerica Partners LP Average ROIC 5.8% 13.5% 50.4% 10.9% 1.1% 16.3% Source: Thomson One March 12, 2015 As Table 2 displays, Sunoco LP’s return on invested capital (ROIC) is lower than most of its competitors at 5.8%. The Company’s current growth strategy is to acquire retail and wholesale businesses as well as assets from its parent company ETP. The Company also recently purchased Aloha Petroleum Ltd. and MACS for $240 million and $768 million respectively. Sunoco LP’s growth strategy is likely lowering its ROIC and, therefore, investors should not be dissuaded by its position next to its peers. Robert W. Owens President and Chief Executive Officer Robert Owens is the President and Chief Executive Officer of Sunoco LP and its affiliate Sunoco Inc. Previously he was Senior Vice President of Marketing of Sunoco, Inc., where he was responsible for all commercial supply and trading activities involving crude oil, refined products, and petrochemicals, as well as wholesale marketing and transportation operations. Mr. Owens holds a B.S. in Business Administration and Marketing from California Polytechnic State University and a M.B.A. from the Kellogg Graduate School of Management at Northwestern University. Cynthia A. Archer Executive Vice President and Chief Marketing Officer Cynthia Archer is the Executive Vice President and Chief Marketing Officer of Sunoco LP. She is responsible for marketing, merchandising, store design, product and environmental integrity, and engineering, design and construction across the network. She previously served as Vice President of Marketing and Development of Sunoco, Inc. She is also a Vice Chair of the Board of Trustees of Bryn Mawr College. Ms. Archer holds a B.A. degree in English literature from Bryn Mawr College and an M.B.A. from Harvard Business School.

- 19. SUNOCO LP (SUN) BURKENROAD REPORTS (www.burkenroad.org) March 17, 2015 19 Board of Directors Sunoco LP’s Board of Directors consists of eight directors: Sam L. Susser, Robert W. Owens, Christopher Curia, Marshall S. McCrea, Matthew S. McCrea, Matthew S. Ramsey, Martin Salinas, Jr., Rick K. Turner, and William P. Williams. All of the Company’s directors have experience in the motor fuel industry and many have worked for the Company’s parent, ETP. Mr. Susser is the Company’s Chairman, and served as Susser Holding’s President and Chief Executive Officer until its merger with ETP. UNITHOLDER ANALYSIS Energy Transfer Partners is the general partner of Sunoco LP. As general partner, ETP is responsible for the operations of the Company. As Figure 7 previously displayed (see page 12), ETP also owns 44.2% of the Sunoco LP’s limited partner shares. The remaining shares trade publicly. Sunoco LP is a master limited partnership (MLP), meaning its limited partner ownership is sold publicly as units. Unitholders receive quarterly cash distributions directly from the Company’s cash on hand at the end of each quarter. As of February 11, 2015, Sunoco LP had a market capitalization of $1,783 million with 24.24 million shares outstanding. As Table 3 displays, investment managers own the majority of the Company’s outstanding shares, or 33.9% of the limited partner units. As Table 4 shows, OFI SteelPath, Inc. is the Company’s largest shareholder other than Susser Holdings, a subsidiary of ETP. OFI SteelPath is a hedge fund with a focus on energy infrastructure MLPs. The hedge fund is also heavily invested in Sunoco LP’s parent, ETP. Table 3: Sunoco LP’s Investor Type Investor Type Investors % O/S Position Value ($MM) Investment Managers 89 33.9% 8,217,196 $428.80 Corporations 19 16.8% 4,075,748 $187.60 Insiders 19 2.4% 590,225 $30.80 Brokerage Firms 15 2.3% 546,053 $29.99 Source: Thomson One February 11, 2015

- 20. SUNOCO LP (SUN) BURKENROAD REPORTS (www.burkenroad.org) March 17, 2015 20 Table 4: Sunoco LP’s Top Investors Investor Name % O/S Pos ETP and Subsidiaries 16.76 4,062,848 OFI SteelPath, Inc. 8.79 2,129,803 ClearBridge Investments, LLC 3.89 941,896 Geneva Advisors, LLC 3.01 729,559 Goldman Sachs Asset Management (US) 2.73 661,750 Advisory Research, Inc. 2.40 581,021 Morgan Stanley Investment Management Inc. (US) 2.20 533,736 Davenport Asset Management 2.11 510,585 Kornitzer Capital Management Inc. 1.43 345,500 Susser (Samuel L) 1.11 269,715 Source: Thomson One February 11, 2015 While large institutional investors can typically influence the management of a corporation, Sunoco LP’s structure as an MLP shields the Company from such influence. ETP owns the general partner of the Company, which is responsible for the management of the MLP. ETP is also a majority limited partner unitholder, though limited partners have no claim to the management of an MLP. Insider Unitholders Insiders own 2.4% of Sunoco LP’s total limited partner units. The largest individual investor is Sam L. Susser, who is the active Chairman of the Board. Mr. Susser became Chief Executive Officer of Susser Holding Company in 1992 and held the position until the Company merged with ETP in 2014. Mr. Susser graduated from the University of Texas with a BBA in finance. In addition to Sunoco LP, Mr. Susser sits on various boards and committees of Texas schools, hospitals, and foundations, and has won numerous awards for his impact on Texas businesses. RISK ANALYSIS AND INVESTMENT CAVEATS Sunoco LP faces many operational and regulatory risks due to the volatility of oil prices and demand, and the heavy governmental regulation of the gasoline and petroleum industry. The Company also faces financial risks associated with its quarterly distributions to unitholders, required by all master limited partnership (MLP). These risks affect Sunoco LP’s revenue and income, ultimately affecting the Company’s ability to pay quarterly cash distributions to its unitholders.

- 27. SUNOCO LP (SUN) BURKENROAD REPORTS (www.burkenroad.org) March 17, 2015 27 ANOTHER WAY TO LOOK AT IT ALTMAN Z‐SCORE Edward Altman created the Altman Z‐Score analysis in 1968 while teaching at New York University as a means of predicting a company’s risk of bankruptcy. The Z‐Score, which lenders use to judge a company’s financial security, is calculated using the financial ratios seen in Table 5. These ratios are then multiplied by a corresponding coefficient and then summed. The result of these calculations is the company’s Z‐Score. This model is believed to be roughly 72% accurate in predicting a company’s bankruptcy two years prior to the event. Altman Z‐scores fall in one of three ranges. A score above 3.0 means the company is generally safe from bankruptcy. A score under 1.8 translates to a very high risk of bankruptcy, while companies with scores in between 1.8 and 3.0 range from safe to mild risk of bankruptcy. Generally, investors of companies with scores under 3.0 should evaluate the company’s credit risk. As Table 6 displays, Sunoco LP has an Altman Z‐Score of 3.03 meaning the Company is safe from bankruptcy. In 2012 and 2013, Sunoco LP operated with very little debt, giving the Company no risk of default. In 2014, the Company took on debt to finance its acquisitions. Sunoco’s high Z‐Score of 3.03 is credited to its strong earnings and its limited use of debt. The Company’s earnings before interest and taxes (EBIT) increased by 64% in 2014. However, the Company also increased its liabilities by roughly $750 million due to debt. This increase in liabilities lowered the Company’s Z‐Score significantly, but the weight associated with the increase in EBIT keeps Sunoco LP safe from default. Table 5: Sunoco LP’s Altman Z‐Scores 2012 2013 2014 Altman Z‐Score 13.67 12.65 3.03 Source: Sunoco LP Annual Reports

- 29. SUNOCO LP (SUN) BURKENROAD REPORTS (www.burkenroad.org) March 17, 2015 29 WWBD? What Would Ben (Graham) Do? Ben Graham is widely considered the father of value investing, influencing many of today’s most successful investors, including Warren Buffet. Graham set up ten hurdles to help investors make investment decisions on a company. Our abbreviated approach uses eight hurdles. The eight hurdles used to determine whether a company is expected to see strong, consistent growth in the future can be seen on the following page. According to Graham, a stock must pass at least three of the hurdles to be considered for purchase. As Figure 11 shows, Sunoco LP passed six out of the eight hurdles, making it an extremely attractive investment according to Ben Graham. Figure 11: Ben Graham Investment Dial Sunoco LP has only traded publicly for three years, and therefore, we could only look to thee years of the Company’s past performance instead of five. The Company fails to meet only two of the hurdles: a price to earnings (P/E) ratio of one half the highest in five years, and a current ratio of two or more. We believe Sunoco LP is still trading at a high P/E ratio (29.2) because of the recent acquisitions the Company made, as well as the announcement the Company made regarding future acquisitions. Investors clearly believe the earnings of the Company will begin to increase, as the Company’s P/E, while lower than its high of 53.5, is significantly higher than its low of 18.5. Sunoco LP’s acquisitions also affect its current ratio. The Company borrowed against its revolver to finance its acquisitions. The increase in short term debt is holding the current ratio down, while we believe that higher earnings in the future will increase the firm’s cash flow, thereby raising the current ratio to above 2.

- 30. SUNOCO LP (SUN) BURKENROAD REPORTS (www.burkenroad.org) March 17, 2015 30 Figure 12: Ben Graham Hurdles Earnings per share (ttm) 4.04$ Price: 50.89$ Earnings to Price Yield 7.93% 10 Year Treasury (2X) 4.20% P/E ratio as of 12/31/12 53.5 P/E ratio as of 12/31/13 18.5 P/E ratio as of 12/31/14 28.3 Current P/E Ratio 29.2 Dividends per share (ttm) 2.17$ Price: 50.89$ Dividend Yield 4.27% 1/2 Yield on 10 Year Treasury 1.05% Stock Price 50.89$ Book Value per share as of 12/31/14 55.53$ 150% of book Value per share as of 12/31/14 83.29$ Interest‐bearing debt as of 12/31/14 528,335$ Book value as of 12/31/14 1,142,376$ Current assets as of 12/31/14 225,141$ Current liabilities as of 12/31/14 154,682$ Current ratio as of 12/31/14 1.5 EPS for year ended 12/31/14 1.74$ EPS for year ended 12/31/13 1.69$ EPS for year ended 12/31/12 0.42$ EPS for year ended 12/31/14 1.69$ EPS for year ended 12/31/13 1.74$ EPS for year ended 12/31/12 0.42$ Stock price data as of M arch 17, 2015 Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years Yes Hurdle # 8: Stability in Growth of Earnings Yes Hurdle # 6: Current Ratio of Two or More No Hurdle # 3: A Dividend Yield of 1/2 the Yield on 10 Year Treasury Yes Yes Hurdle # 4: A Stock Price less than 1.5 BV Yes Hurdle # 5: Total Debt less than Book Value Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs No SUNOCO LP (NYSE: SUN) Ben Graham Analysis Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury Yes Stock Price as of March 17, 2015