Recommended

More Related Content

Similar to Callon Petroleum (CPE) - Burkenroad Reports - Fall 2018

Similar to Callon Petroleum (CPE) - Burkenroad Reports - Fall 2018 (20)

Recently uploaded

Recently uploaded (20)

Callon Petroleum (CPE) - Burkenroad Reports - Fall 2018

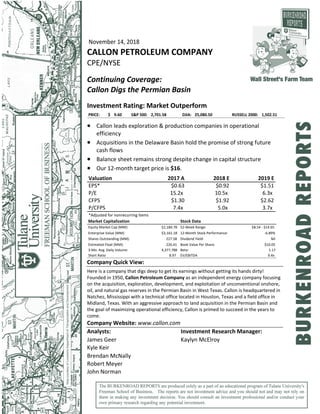

- 1. November 14, 2018 CALLON PETROLEUM COMPANY CPE/NYSE Continuing Coverage: Callon Digs the Permian Basin Investment Rating: Market Outperform PRICE: 9.60$ S&P 500: 2,701.58 DJIA: 25,080.50 RUSSELL 2000: 1,502.51 Callon leads exploration & production companies in operational efficiency Acquisitions in the Delaware Basin hold the promise of strong future cash flows Balance sheet remains strong despite change in capital structure Our 12‐month target price is $16. Valuation EPS* P/E CFPS P/CFPS *Adjusted for nonrecurring ite 2017 A 2018 E 2019 E $0.63 $0.92 $1.51 15.2x 10.5x 6.3x $1.30 $1.92 $2.62 7.4x 5.0x 3.7x ems Market Capitalization Stock Data Equity Market Cap (MM): $2,184.78 52‐Week Range: $8.54 ‐ $14.65 Enterprise Value (MM): $3,161.18 12‐Month Stock Performance: ‐6.89% Shares Outstanding (MM): 227.58 Dividend Yield: Nil Estimated Float (MM): 226.41 Book Value Per Share: $10.05 3‐Mo. Avg. Daily Volume: 4,377,788 Beta: 1.17 Short Ratio 8.97 EV/EBITDA 9.4x Company Quick View: Here is a company that digs deep to get its earnings without getting its hands dirty! Founded in 1950, Callon Petroleum Company as an independent energy company focusing on the acquisition, exploration, development, and exploitation of unconventional onshore, oil, and natural gas reserves in the Permian Basin in West Texas. Callon is headquartered in Natchez, Mississippi with a technical office located in Houston, Texas and a field office in Midland, Texas. With an aggressive approach to land acquisition in the Permian Basin and the goal of maximizing operational efficiency, Callon is primed to succeed in the years to come. Company Website: www.callon.com Analysts: Investment Research Manager: James Geer Kaylyn McElroy Kyle Keir Brendan McNally Robert Meyer John Norman

- 3. Callon Petroleum Company (CPE) November 14, 2018 3 Table 1: Historical Burkenroad Ratings and Prices Report Date Stock Price Rating 12 Month Target Price 11/14/2018 $9.60 Market Outperform $16.00 11/7/2017 $11.24 Market Perform $12.00 11/8/2016 $13.39 Market Outperform $16.50 11/6/2015 $8.83 Market Perform $10.00 11/9/2014 $6.64 Market Outperform $12.00 11/7/2013 $6.37 Market Outperform $14.00 11/13/2012 $4.40 Market Outperform $7.00 11/21/2011 $4.67 Market Outperform $6.00 11/17/2010 $5.27 Market Perform $6.06 12/4/2009 $1.60 Market Outperform $3.95 12/9/2008 $2.01 Market Outperform $4.58 12/4/2007 $14.47 Market Outperform $20.90 4/5/2007 $13.61 Market Outperform $23.00 3/24/2006 $20.22 Market Outperform $20.22 10/29/2004 $13.51 Market Outperform $13.51 3/19/2004 $11.12 Market Outperform $11.12 3/19/2003 $4.25 Buy $4.25 3/15/2002 $6.60 Buy $6.60 3/12/2001 $12.40 Market Perform $12.40 2/28/2000 $13.19 Buy $13.19 4/16/1999 $10.63 Buy $10.63 INVESTMENT THESIS Callon Petroleum continues to expand in the Permian Basin despite the land grab in the region effectively coming to an end. The Company is focused on operational efficiency and utilizes many tactics to increase its margins. Better margins, in turn, have led to more cash on hand for future investment. Callon has increased its production by 50% over the past two years, and with its recent acquisition of land in Ward County, it now boasts more net acres than most of its peers. This increased production, coupled with Callon’s effective debt and equity financing to limit risk exposure, leads to a positive outlook for the future of the firm. Callon leads exploration and production companies in operational efficiency Throughout 2018, Callon has continued to find more ways to increase its operational efficiency and reduce cash costs. Since the fourth quarter of 2016, Callon has shown a steady decline in cash costs per barrel, arriving at the current rate of less than 20% of revenues. Callon’s operating margin is the best of any publicly traded exploration & production company, and with Callon increasing the scale of its production, the cost efficiency will only continue to improve.

- 5. Callon Petroleum Company (CPE) November 14, 2018 5 VALUATION Our research team used the present value‐10 (PV‐10) method to calculate a 12‐month target price of $16.00 for Callon Petroleum. Further, we conducted a stress test to put upper and lower bounds on the expectations of Callon’s stock price during the 12‐month period. The stress test changed the forecasted price of oil up and down by one standard deviation and gave us a range of $11.92 to $19.28. Table 2 shows our findings based on the current oil and gas price forecast. The target price our team found is a 65.8% increase from the November 16, 2018 adjusted closing price of $9.65. PV‐10 Method The PV‐10 is a Securities and Exchange Commission approved valuation method widely used industry to accurately value companies within the Oil and Gas industry. The method values a company’s reserves based on production speed and forecasted price, less lease operating expense, discounted at a 10% rate. A key underlying assumption for the method is the forecasted price of oil and gas, which is why we conducted a stress test to cover the extremes of the price forecast. Other key assumptions are the production rates and how expensive it is to run that production, which can change over the course of a company’s life as well. The five‐ year net asset value (12‐month price estimate) is our target price of $16.00, and the seven‐year net asset value, equivalent to the 24‐month price estimate, is $24.10. Table 2: PV‐10 Method PV of Cash Flows 3 years $ 1,575,641 PV of Cash Flows 5 years $ 3,288,085 PV of Cash Flows 7 Years $ 5,080,833 Equity Valuation 3 years NAV: $ 7.47 Equity Valuation 5 years NAV: $ 15.60 Equity Valuation 7 years NAV: $ 24.10 INDUSTRY ANALYSIS Callon Petroleum is an exploration and production company (E&P), founded in 1950, which operates in the Permian Basin located in West Texas. It received its name because it has one of the greatest deposits of hydrocarbon from the Permian geologic period. The Permian Basin is comprised of several sub‐regions, including the Midland Basin, Delaware Basin, and the Marfa Basin. It spans an area of 250 miles wide and 300 miles long. The oil and gas industry is made up of three different sectors: upstream, midstream, and downstream. The upstream sector consists of finding the regions to drill, drilling exploratory wells, and controlling wells that bring gas to the surface. The midstream sector consists of transporting and storing crude oil.

- 10. Callon Petroleum Company (CPE) November 14, 2018 10 Fred Callon, the son of Sim Callon, became President and Chief Executive Officer (CEO) of Callon in 1984, and took the Company private in 1988. In 1994 Callon became public again following a merger with partners CCP and CN Resources. In 1998, Callon stock moved from the NASDAQ to the New York Stock Exchange. Callon ended 2000 with their highest revenues, net income, and oil and gas reserves in history. Revenues were up almost 50% to $58.1 million, while net income nearly quadrupled from the previous year to $12.5 million. The Company ended 2000 with estimated proven reserves of 334 billion cubic feet of natural gas equivalent (Bcfe), up 28% from 1999. In 2009, Callon shifted its production strategy, electing to pursue onshore exploration in the Permian Basin rather than drilling offshore in the Gulf of Mexico. Callon was able to buy 8,800 acres for $16 million, which is much cheaper than the land would be worth today. The Company currently focuses 100% of its operations in the Permian Basin of West Texas, with over 1,500 horizontal drilling locations in the region. Products In 2017, Callon Petroleum produced 6,557 thousand barrels of oil (MBbls) and 10,896 million cubic feet of natural gas (Mmcf). Callon includes natural gas liquids (NGLs) in their accounting for natural gas production, reflecting the premium paid for its natural gas. Through acquisitions and production increases, Callon has enjoyed a steady increase in production in the Permian and Delaware Basins since 2014. Callon produces the U.S. benchmark oil, West Texas Intermediate (WTI), in both the Permian and Delaware Basins. WTI is characterized as being a light, sweet crude oil. The American Petroleum Institute (API) weighs WTI at an API gravity of 39.6, with a sulfur content of 0.24%. Any API gravity above ten and sulfur content below 2% is considered a quality crude. These two characteristics make WTI easily produced and refined. Strategy Callon Petroleum continues to extend its operations in the Permian and Delaware Basins through acquisitions while driving down operating costs via larger drilling pads and investments in pre‐production infrastructure. Because of this, Callon is a fierce competitor in the West Texas area. Further, Callon is investing in water and chemical recycling programs to power its horizontal hydraulic rigs. The programs will both improve efficiency in the future and promote Callon as an environmentally conscious company. Lastly, Callon has strong liquidity and funds its new ventures with limited leverage; it operates almost entirely within its operational cash flow. Coupled with Callon’s strong hedging position, the firm’s strong strategy forecasts growth and production in the years to come.

- 12. Callon Petroleum Company (CPE) November 14, 2018 12 Table 3: Peer Analysis Data Company Callon Carrizo Energen Halcon Diamondb ack Apache EP Energy Corp WPX Energy Ticker Symbol CPE CRZO EGN HK FANG APA EPE WPX Market Cap ($MM) 2670 2250 7750 774 1182 17300 468 7510 P/E 18.23 12.66 32.48 ‐‐ 17.57 39.94 ‐‐ ‐‐ Net Sales ($MM) 129 239 349 55 501 1900 319 430 Total Debt 1080 1030 530 625 1300 8700 8010 2180 ROE 7.20 11.20 12.60 33.10 10.90 11.80 (40.3) (10.2) EPS (TTM) 0.64 1.94 2.35 (0.10) 6.82 1.13 (0.15) ‐‐ ROA 4.80 2.30 8.40 15.20 7.20 3.90 (3.7) (4.8) Operating Margin 37.1 32.5 14.9 185.3 50.5 23.5 12.4 3.2 Net Debt/ EBITDA 4.30 2.03 0.84 0.74 1.39 2.35 12.80 3.04 Sales 3yr Avg Growth 37.76 4.55 (0.66) (28.72) 45.19 (17.02) (28.3) 4.36 Estimated Comp. Sales Growth 52.43 43.84 82.25 (64.48) 98.19 14.84 ‐‐ 42.23 EV 3272.6 3999.8 8281.4 1294.9 14084.5 26042.8 4681.1 9826.4 EV/EBITDA 9.8 6.6 10.2 2.4 11.1 6.6 8.4 18.2 Proved Reserves (MMBoe) 137.0 261.7 444.0 51.1 335.4 1175.0 392.1 436.2 Production (MBOE/Day) 22.9k 53.8k 76.1k 27.4k 79.2k 457.3k 82.3k 109.8k Source: Bloomberg September 18, 2018 Callon has one of the highest enterprise value/earnings before interest, taxes, depreciation and amortization (EBITDA) ratios among its peers, signaling stronger operating performance than its competitors. However, Callon has significantly fewer net sales and production numbers than most of its peers. In terms of market cap, Callon’s direct competitor is Carrizo Oil & Gas. Both operate within the Permian Basin, yet Carrizo has additional operations in the Eagle Ford Shale in South Texas. In addition, Callon has a much higher price to earnings (P/E) ratio and return on assets (ROA), while Carrizo has a higher return on equity (ROE) and enterprise value (EV). Callon and the majority of its peers have low debt to EBITDA ratios, indicating liquidity within the companies. Callon’s estimated sales growth is superior compared to its peers, indicating favorable market growth for the Company. With commodities price on the rise, the future of Callon is promising.

- 15. Callon Petroleum Company (CPE) November 14, 2018 15 Table 4: Peer Group ROIC Company Callon Carrizo Energen Halcon Diamond back Apache EP Energy Corp WPX Energy Ticker Symbol CPE CRZO EGN HK FANG APA EPE WPX Market Cap ($MM) 2,670 2,250 7,750 774 1,182 1,730 468 7,510 2018 (Q2) 6.71 16.53 11.02 24.04 10.66 7.82 0.28 (1.22) 2017 5.78 13.15 7.69 52.16 9.62 9.99 0.64 1.89 2016 (3.69) (33.87) (3.43) (35.61) (2.63) (6.00) 7.91 (7.49) 2015 (33.02) (48.49) (14.63) (51.34) (16.30) (72.20) (49.00) (0.81) 2014 4.20 5.70 ‐‐ 1.65 6.67 (11.95) 11.61 4.92 Source: Bloomberg Joseph C. Gatto, Jr. President, Chief Executive Officer and Director, (47) Joseph C. Gatto, Jr. was promoted to CEO by the board of directors in May 2017, following the death of Fred Callon. He had previously served as President and Chief Financial Officer. Before joining Callon, Mr. Gatto was a managing director for Barclays and Merrill Lynch, where he was involved in all phases of mergers & acquisitions (M&A) and capital raising transactions. Mr. Gatto received his BS from Cornell University and his M.B.A. from the Wharton School of Pennsylvania. James P. Ulm, II Senior Vice President and Chief Financial Officer, (54) James Ulm, II joined Callon in December 2017 as the Senior Vice President and CFO. He has been involved with various energy companies for more than 30 years, responsible for finance, accounting, strategic planning, M&A, business development and risk management. Mr. Ulm received both his B.S. in Accounting and M.B.A. from the University of Texas. Gary A. Newberry Senior Vice President and Chief Operating Officer, (63) Gary Newberry has been with the Company since April 2010, serving all of his time as Senior Vice President and Chief Operating Officer. Before Callon, he held management positions for production and drilling operations in the Rockies, Alaska, and the Permian Basin. Mr. Newberry received his B.S. in Petroleum Engineering from Marietta College. Correne S. Loeffler Vice President, Finance and Treasurer, (41) Correne Loeffler is the Vice President, Finance and Treasurer for the Company. Prior to Callon, she served as an Executive Director with JPMorgan, where she spent ten years in the Corporate Client Banking group. While at JPMorgan, she was Callon’s relationship manager starting in 2013. Ms. Loeffler received her M.B.A. from the University of Texas and her B.A. from Indiana University.

- 17. Callon Petroleum Company (CPE) November 14, 2018 17 Table 5: Callon Investor Style Breakdown Investment Style # of Investors % Outstanding Shares Held Index 39 31.58% 71,876,104 Core Growth 95 25.23% 57,422,903 Core Value 69 23.88% 54,339,919 Hedge Fund 108 14.16% 32,233,178 GARP 68 12.71% 28,934,809 Growth 28 5.24% 11,918,828 Income Value 11 4.71% 10,729,569 Source: Thomson One September 21, 2018 Currently, Callon insider investors own 0.53% of Callon’s total shares outstanding. The last insider transaction was performed by Callon’s Vice President and Chief Accounting Officer, Mitzi P. Conn, who sold 15,000 shares on September 18, 2018. Despite the sold shares, Conn still directly holds 42,062 shares of Callon. Table 6 portrays holdings information about Callon’s top insider investors, including the individuals’ relationship to Callon, the number of shares held, and the most recent change in shares held. Table 6: Top Insider Holders Holder Name Relationship to Callon Direct Holdings Recent Change % Outstanding Fred L. Callon Former Chairman & CEO 467,455 29,735 0.21% Gary Newberry Senior VP & COO 260,852 (9,778) 0.11% Joseph C. Gatto Jr. President, Director & CEO 188,742 (15,760) 0.08% Larry D. McVay Independent Director 147,432 4,990 0.06% Anthony J. Nocchiero Independent Director 134,296 4,990 0.06% Source: Nasdaq.com ‐ Filings as of June 30, 2018 Table 7 exhibits Callon’s top‐ten institutional holders, who own 52.10% of Callon’s total market share. Additionally, Table 6 displays the investors’ number of shares held, the percentage of total shares outstanding, recent changes in shares held, and the investment style of each institutional investor. Currently, Callon’s largest investor is BlackRock Institutional Trust Company, which holds 9.96% of Callon’s total shares outstanding, and recently bought 2,930,350 additional shares. Of the top‐ten institutional holders, nine have recently increased their position in Callon. This faith in Callon indicates that the Company is positioned well for the future.

- 18. Callon Petroleum Company (CPE) November 14, 2018 18 Table 7: Top‐ten Institutional Holders Investor Name % Outstanding Shales Held Recent Change Recent Change (%) Investment Style BlackRock Institutional Trust Company, N.A. 9.96 22,661,930 2,930,350 14.85 Index The Vanguard Group, Inc. 8.69 19,780,445 2,376,599 13.66 Index Dimensional Fund Advisors, L.P. 7.59 17,261,443 2,256,780 15.04 Core Growth Wellington Management Company, LLP 6.38 14,512,608 (3,824,161) (20.86) Core Value State Street Global Advisors (US) 5.49 12,500,986 2,450,122 24.38 Index Goldman Sachs Asset Management (US) 3.45 7,862,036 1,170,589 17.49 Core Growth Luminus Management, LLC 2.91 6,620,618 2,618,965 65.45 Hedge Fund Silvercrest Asset Management Group LLC 2.68 6,106,366 214,636 3.64 Core Value Channing Capital Management, LLC 2.51 5,709,338 2,262,652 65.65 GARP Glenmede Investment Management LP 2.44 5,543,836 1,949,736 54.25 Hedge Fund Source: Thomson One September 21, 2018 RISK ANALYSIS AND INVESTMENT CAVEATS Companies that operate in the Oil and Gas industry face a multitude of risks, ranging from commodity prices to government regulation. Callon Petroleum is no different and has to account for all of these risks if it is to continue to be a sustainable competitor in its market. The following sections analyze three segments of Callon’s most relevant risks: operational, financial, and regulatory. Operational Risks Oil and Gas Price Risk Oil and gas prices are extremely volatile, exposing any player in the industry to incredible amounts of risk in their operations and forecasting future projects. Because exploration and production companies have no way to differentiate their products, revenues are entirely dependent on the current commodity prices. Luckily, prices have risen and stabilized at a highly profitable level for efficiently operated E&P companies, such as Callon.

- 20. Callon Petroleum Company (CPE) November 14, 2018 20 Table 8: Callon Oil and Natural Gas Reserves 2015 2016 2017 Proved Developed Oil (MBbls) 22,257 32,920 51,920 Natural gas (MMcf) 38,157 61,871 104,389 MBOE 28,617 43,232 69,318 Proved undeveloped Oil (MBbls) 21,091 38,225 55,152 Natural gas (MMcf) 27,380 60,740 75,021 MBOE 25,654 48,348 67,656 Total proved Oil (MBbls) 43,348 71,145 107,072 Natural gas (MMcf) 65,537 122,611 179,410 MBOE 54,271 91,580 136,974 Source: Callon Website As precise as the reserve estimation process may be, there is no real way to know how much volume is in the reserves without extracting the oil and gas. Callon assumes that the estimations are correct when forecasting future production, but actual production numbers will not be the same as the forecasted numbers. Callon may be slightly over or under its targeted production, or off by hundreds of thousands of barrels. Because of these discrepancies, Callon must be constantly aware of the possible effects inaccurate projections will have on its production and future revenues. Geographic Risk Callon strictly operates in the Permian Basin. Although this consolidates operations and promotes cost efficiency, Callon is entirely dependent on one basin’s reserves. As discussed above, if the Permian Basin’s reserves are not as vast as projected, Callon’s revenues will be severely impacted. The Permian Basin also experiences extreme weather from time to time, including tornadoes and tropical storms. Thus, operating in one basin proves very risky, and Callon may consider making plays into other nearby basins to hedge this risk. Environmental Risk Callon’s main environmental risk is weather. West Texas is exposed to dry lightning, which can adversely affect their drilling process. Additionally, tornados are prevalent in the Permian Basin. These tornados could uproot a well, so a company like Callon must take preventative measures to solidify their structures. Lastly, the area can easily flood due to intense thunderstorms, which can negatively affect their business.

- 28. Callon Petroleum Company (CPE) November 14, 2018 28 ANOTHER WAY TO LOOK AT IT ALTMAN Z‐SCORE The Altman Z‐Score is a measure of a public company’s default risk. Edward Altman built this indicator in 1968 as a means to determine whether manufacturing companies were viable. Since then, the Z‐Score has become popular as a means for evaluating loans. Tests on the Z‐ Score have shown to provide 72% reliability when predicting default up to two years in advance. Although popular and reliable, keep in mind that the Z‐Score only measures five factors and does not adjust over time. Also, consider that Altman intended this indicator for large‐cap manufacturing companies. The Z‐Score is a linear discriminant model, which compares working capital, retained earnings, earnings before interest and taxes, and sales to total total assets as well as the market value of equity to total liabilities. As a linear discriminant model, the three classifications are low, moderate, and high default risk represented by greater than 3.00, between 2.99 and 1.80, and less than 1.80, respectively. Callon Petroleum has a Z‐Score of 1.71 according to our forecasts, which is high compared to historical levels, although still in the distress zone of below 1.80. This low score can be attributed to the nature of the company. Callon is a mid‐cap exploration and production company, which relies heavily on oil prices, hedging, and debt financing to fund its operations. Callon uses its highly leveraged position to compete for growth through acquisitions. Historically, Callon’s Z‐Score has been low and even negative during some years, however, its stock price continues to grow gradually. The Company’s recent financing funded a land acquisition on a promising area of the Permian Basin. Once the Company fully capitalizes on the new land, it should be able repay its debts without having to refinance (oil prices permitting). Thus, Callon’s Z‐Score should increase as its default risk decreases. Table 9: Callon Z‐Scores 2010 2011 2012 2013 2014 2015 2016 2017 2018 -0.20 1.02 0.52 0.91 0.46 -0.57 2.24 1.87 1.71 Distress Zone Distress Zone Distress Zone Distress Zone Distress Zone Distress Zone Grey Zone Grey Zone Distress Zone

- 30. Callon Petroleum Company (CPE) November 14, 2018 30 WWBD? What Would Ben (Graham) Do? Ben Graham, known as “the father of value investing,” and a mentor to Warren Buffet, developed a method using eight hurdles to determine whether or not a stock is undervalued. According to Graham, a stock is attractive if a stock passes four of his eight hurdles, listed below. 1. Earnings to price yield that is twice the yield of a ten‐year U.S. Treasury bond. 2. Price to earnings ratio that is half of the stock’s highest P/E ratio in the last five years. 3. Dividend yield that is half the yield of a ten‐year U.S. Treasury bond. 4. Stock price that is less than 1.5 times the book value per share. 5. Total debt is less than book value. 6. Current ratio of two or more. 7. Earnings growth of 7% or more over the last five years. 8. Stable earnings growth. We found that Callon Petroleum passes three of the eight hurdles, detailed below. #4. Callon’s current $9.90 stock price is less than .5 times Company’s book value per share. #5. Callon’s total debt is less than the book value of the Company. #7. Callon’s compound annual growth rate is more than 7%. Callon failed five of the eight hurdles as follows. #1. Callon’s EPS yield of 6.08% is less than twice the yield on a ten‐year U.S. Treasury. #2. Callon’s current P/E ratio of 16.4 is above half of the stock’s highest P/E ratio in the last five years. #3. Callon does not issue dividends. #6. The Company’s current ratio is 0.6 #8. Callon has not demonstrated stable earnings growth in the past five years. As shown in Figure 11, the Company passes three of the eight hurdles, Graham would likely not consider the possibility of investing in Callon. Figure 11: Ben Graham Dial

- 31. Callon Petroleum Company (CPE) November 14, 2018 31 Earnings per share (ttm) 0.60$ Price: 9.90$ Earnings to Price Yield 36108 9.90$ 6.08% 10 Year Treasury (2X) 6.23% P/E ratio as of 2013 (653.0) P/E ratio as of 2014 8.4 P/E ratio as of 2015 (2.2) P/E ratio as of 2016 (19.7) P/E ratio as of 2017 21.7 Current P/E Ratio 16.4 Dividends per share (ttm) ‐$ Price: 9.90$ Dividend Yield 0.00% 1/2 Yield on 10 Year Treasury 1.56% Stock Price 9.90$ 9.90$ Book Value per share as of 6/30/18 10.82$ 150% of book Value per share as of 6/30/18 16.23$ Interest‐bearing debt as of 9/30/18 1,053,528$ Book value as of 9/30/18 2,288,308$ Current assets as of 9/30/18 188,975$ Current liabilities as of 9/30/18 333,132$ Current ratio as of 9/30/18 0.6 EPS for year ended 2017 0.56$ EPS for year ended 2016 (0.78)$ EPS for year ended 2015 (3.77)$ EPS for year ended 2014 0.65$ EPS for year ended 2013 (0.01)$ EPS for year ended 2017 0.56$ ‐172% EPS for year ended 2016 (0.78)$ ‐79% EPS for year ended 2015 (3.77)$ ‐680% EPS for year ended 2014 0.65$ ‐6600% EPS for year ended 2013 (0.01)$ Stock price data as of November 14th, 2018 NO CALLON PETROLEUM (CPE) Ben Graham Analysis Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury NO Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs YES Hurdle # 3: A Dividend Yield of at least 1/2 the Yield on 10 Year Treasury NO Hurdle # 4: A Stock Price less than 1.5 BV YES Hurdle # 5: Total Debt less than Book Value YES Hurdle # 6: Current Ratio of Two or More NO Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years NO Hurdle # 8: Stability in Growth of Earnings

- 32. Callon Petroleum Company (CPE) November 14, 2018 32 CALLON PETROLEUM (CPE) Annual and Quarterly Earnings In thousands For the period ended Operating revenues Oil sales Gas sales 2015 A 125,166$ 12,346 2016 A 177,652$ 23,199 2017 A 31‐Mar A 30‐Jun A 30‐Sep A 31‐Dec E 2018 E 31‐Mar E 30‐Jun E 30‐Sep E 31‐Dec E 2019 E 322,374$ 115,286$ 122,613$ 142,601$ 122,441$ 502,941$ 128,393$ 140,059$ 176,508$ 187,938$ 632,898$ 44,100 12,154 14,462 18,613 12,153 57,382 13,794 13,932 15,918 19,266 62,910 2019 E2018 E Total operating revenues Costs and expenses: Lease operating expenses Production taxes Depreciation, depletion and amortization 137,512 27,036 9,793 69,249 200,851 38,353 11,870 71,369 366,474 127,440 137,075 161,214 134,595 560,324 142,187 153,991 192,426 207,205 695,808 49,907 13,039 13,141 18,525 15,151 59,856 16,232 17,968 19,787 21,086 75,073 22,396 8,463 7,539 10,263 8,734 34,999 9,477 10,380 11,550 12,346 43,754 115,714 35,417 38,733 48,257 40,482 162,889 43,775 47,933 53,115 56,666 201,488 General and administrative Settled share‐based awards Accretion expense Gain on sale of other property and equipment Rig Termination Fee Acquisition expense 28,347 660 3,075 27 26,317 958 3,673 27,067 8,769 8,289 9,721 9,435 36,214 10,074 11,017 12,257 13,044 46,392 6,351 677 218 206 202 4,479 5,105 859 841 815 800 3,315 2,916 548 1,767 1,435 3,750 Impairment of oil and gas properties Total operating expenses Income (loss) from operations Other (income) expenses: Interest expense 208,435 346,622 (209,110) 21,111 95,788 248,328 (47,477) 11,871 225,028 66,454 69,675 88,403 78,281 302,813 80,418 88,139 97,523 103,942 370,022 141,446 60,986 67,400 72,811 56,314 257,511 61,769 65,852 94,902 103,263 325,787 2,159 460 594 711 711 2,476 711 711 711 711 2,844 Unrealized gain on mark‐to‐market derivative instruments, net (Gain) loss on early extinguishment of debt Loss on derivative contracts (28,358) 12,883 20,233 18,901 4,481 16,554 34,339 1,496 56,870 (3,579) (3,679) 228 187 (6,843) Interest and other (198) (637) (1,311) (211) (703) (1,657) (2,571) Total other (income) expenses Income (loss) before income taxes Income tax expense (benefit) Net Income (loss) before Medusa Spar LLC (7,445) (201,665) 38,474 (240,139) 44,350 (91,827) (14) (91,813) 19,749 4,730 16,445 33,393 2,207 56,775 (2,868) (2,968) 939 898 (3,999) 121,697 56,256 50,955 39,418 54,107 200,736 64,638 68,821 93,963 102,365 329,786 1,273 495 481 1,487 524 2,987 569 623 693 741 2,625 120,424 55,761 50,474 37,931 53,583 197,749 64,069 68,198 93,270 101,624 327,160 Preferred stock dividends (7,895) (7,295) (7,295) (1,824) (1,824) (1,823) (1,823) (7,294) (1,824) (1,823) (1,823) (1,823) (7,293) Net income (loss) (248,034)$ (99,108)$ 113,129$ 53,937$ 48,650$ 36,108$ 51,760$ 190,455$ 62,245$ 66,374$ 91,446$ 99,801$ 319,867$ Net income (loss) per common share: Basic Adjustment for nonrecurring items Adjusted basic Diluted Adjustment for nonrecurring items Adjusted diluted Weighted average shares outstanding: Basic Diluted SELECTED COMMON‐SIZE AMOUNTS (% of oil and gas sales) Lease operating expenses Depreciation, depletion and amortization General and administrative Income (loss) from operations Net income (loss) YEAR‐TO‐YEAR CHANGE Operating revenues Lease operating expenses Depreciation, depletion and amortization General and administrative Interest expense Total operating expenses Income (loss) from operations Net income (loss) (3.77)$ 1.95$ (1.82)$ (3.77)$ (2.49)$ (1.28)$ 65,708 65,708 19.66% 50.36% 20.61% ‐152.07% ‐180.37% ‐9.45% 20.85% 22.08% 12.90% 116.04% 205.15% ‐646.41% ‐930.35% (0.78)$ 0.74$ (0.04)$ (0.78)$ (0.47)$ (0.78)$ 126,258 126,258 19.10% 35.53% 13.10% ‐23.64% ‐49.34% 46.06% 41.86% 3.06% ‐7.16% ‐43.77% ‐28.36% ‐77.30% ‐60.04% 0.56$ 0.27$ 0.23$ 0.17$ 0.25$ 0.92$ 0.30$ 0.31$ 0.43$ 0.47$ 1.51$ 0.08$ 0.02$ 0.06$ 0.12$ 0.63$ 0.29$ 0.29$ 0.29$ 0.25$ 0.92$ 0.30$ 0.31$ 0.43$ 0.47$ 1.51$ 0.56$ 0.27$ 0.23$ 0.17$ 0.24$ 0.90$ 0.29$ 0.31$ 0.43$ 0.47$ 1.51$ 0.08$ 0.02$ 0.06$ 0.12$ 0.64$ 0.29$ 0.29$ 0.29$ 0.24$ 0.90$ 0.29$ 0.31$ 0.43$ 0.47$ 1.51$ 201,526 201,921 210,698 210,698 210,836 210,836 210,976 211,112 211,250 211,380 211,380 202,102 202,588 211,465 211,465 211,536 211,536 211,676 211,812 211,950 212,080 212,080 13.62% 10.23% 9.59% 11.49% 11.26% 10.68% 11.42% 11.67% 10.28% 10.18% 10.79% 31.57% 27.79% 28.26% 29.93% 30.08% 29.07% 30.79% 31.13% 27.60% 27.35% 28.96% 7.39% 6.88% 6.05% 6.03% 7.01% 6.46% 7.09% 7.15% 6.37% 6.30% 6.67% 38.60% 47.85% 49.17% 45.16% 41.84% 45.96% 43.44% 42.76% 49.32% 49.84% 46.82% 30.87% 42.32% 35.49% 22.40% 38.46% 33.99% 43.78% 43.10% 47.52% 48.17% 45.97% 82.46% 56.63% 66.59% 90.53% 13.86% 52.90% 11.57% 12.34% 19.36% 53.95% 24.18% 30.13% 0.79% 8.20% 59.37% 14.77% 19.93% 24.49% 36.74% 6.81% 39.17% 25.42% 62.13% 44.96% 47.76% 69.17% 10.78% 40.77% 23.60% 23.75% 10.07% 39.98% 23.70% 2.85% 68.44% 28.91% 33.92% 15.45% 33.79% 14.88% 32.91% 26.08% 38.26% 28.11% ‐81.81% ‐30.83% 0.85% 60.14% 54.23% 14.68% 54.57% 19.70% 0.00% 0.00% 14.86% ‐9.38% 35.31% 19.02% 66.21% 21.96% 34.57% 21.01% 26.50% 10.32% 32.78% 22.19% ‐397.93% 89.11% 183.87% 131.69% 4.23% 82.06% 1.28% ‐2.30% 30.34% 83.37% 26.51% ‐214.15% 19.05% 54.12% 136.67% 146.47% 68.35% 15.40% 36.43% 153.26% 92.81% 67.95%

- 33. Callon Petroleum Company (CPE) November 14, 2018 33 CALLON PETROLEUM (CPE) Annual and Quarterly Earnings In thousands For the period ended OTHER 2015 A 2016 A 2017 A 31‐Mar A 30‐Jun A 30‐Sep A 31‐Dec E 2018 E 31‐Mar E 30‐Jun E 30‐Sep E 31‐Dec E 2019 E 2019 E2018 E Production ‐ gas (MMcf) Production ‐ oil (MBbls) Production ‐ equivalent units (MBoe) Production ‐ gas MMCFe(daily) Production ‐ oil MBbls (daily) Production ‐ Mboe (daily) Gas as % of total production YY change in production QQ change in production Depreciation, depletion and amortization per Mboe Prodcution Taxes per Mboe Lease operating expense per Mboe Average price of gas Average price of oil 4,312 2,789 3,508 11.81 7.64 9.61 20% 70.11% 259.76% 19.74$ 2.79$ 7.71$ 2.86$ 44.88$ 7,758 4,280 5,573 21.25 11.73 15.27 23% 58.88% 229.93% 12.81$ 2.13$ 6.88$ 2.99$ 41.51$ 10,896 3,240 3,839 4,144 4,024 15,247 4,274 4,654 5,159 5,473 19,559 6,557 1,851 1,995 2,521 2,104 8,471 2,251 2,465 2,745 2,924 10,385 8,373 2,391 2,635 3,212 2,775 11,012 2,963 3,240 3,605 3,836 13,645 29.85 36.00 42.19 45.04 43.73 41.74 47.49 51.14 56.07 59.49 53.55 17.96 20.57 21.92 27.40 22.87 23.19 25.01 27.09 29.84 31.79 28.43 22.94 26.57 28.95 34.91 30.16 30.15 32.92 35.61 39.18 41.70 37.35 22% 23% 24% 22% 24% 23% 24% 24% 24% 24% 24% 639.34% 30.11% 30.37% 54.83% 13.72% 799.46% 23.92% 22.98% 12.24% 38.26% 793.56% 50.24% ‐71.44% 10.20% 21.89% ‐13.60% 31.52% ‐73.09% 9.36% 11.25% 6.42% 23.90% 13.82$ 14.81$ 14.70$ 15.03$ 14.59$ 14.78$ 14.77$ 14.79$ 14.73$ 14.77$ 14.77$ 2.67$ 3.54$ 3.18$ 3.20$ 3.15$ 3.27$ 3.20$ 3.20$ 3.20$ 3.22$ 3.21$ 5.96$ 5.45$ 5.21$ 5.77$ 5.46$ 5.47$ 5.48$ 5.55$ 5.49$ 5.50$ 5.50$ 4.05$ 3.75$ 3.77$ 4.03$ 49.16$ 62.28$ 61.46$ 59.75$

- 34. Callon Petroleum Company (CPE) November 14, 2018 34 CALLON PETROLEUM (CPE) Annual and Quarterly Balance Sheets In thousands As of Current assets: Cash and cash equivalents Accounts receivable 31‐Dec‐15 A 1,224$ 39,624 31‐Dec‐16 A 652,993$ 69,783 31‐Dec‐17 A 31‐Mar A 30‐Jun A 30‐Sep A 31‐Dec E 31‐Dec‐18 E 31‐Mar E 30‐Jun E 30‐Sep E 31‐Dec E 31‐Dec‐19 E 27,995$ 18,473$ 509,146$ 12,129$ 54,869$ 54,869$ 71,820$ 38,124$ 11,076$ 17,750$ 17,750$ 114,320 122,411 111,964 168,753 124,051 124,051 133,961 143,488 177,351 190,973 190,973 2019 E2018 E Fair market value of derivatives Other current assets Total current assets Oil and gas properties, full‐cost accounting method: Evaluated properties Less accumulated depreciation, depletion and amortization 19,943 1,461 62,252 2,335,223 (1,756,018) 103 2,247 725,126 2,754,353 (1,947,673) 406 4,210 11,569 4,289 4,289 4,289 4,289 4,289 4,289 4,289 4,289 2,139 2,078 7,689 3,804 3,804 3,804 3,804 3,804 3,804 3,804 3,804 144,860 147,172 640,368 188,975 187,013 187,013 213,873 189,704 196,520 216,815 216,815 3,429,570 3,598,868 3,814,242 4,305,189 4,409,837 4,409,837 4,555,437 4,701,037 4,846,637 4,992,237 4,992,237 (2,084,095) (2,119,599) (2,158,225) (2,208,066) (2,248,548) (2,248,548) (2,292,324) (2,340,257) (2,393,371) (2,450,037) (2,450,037) Net evaluated properties Unevaluated properties excluded from amortization Total oil and gas properties 579,205 132,181 711,386 806,680 668,721 1,475,401 1,345,475 1,479,269 1,656,017 2,097,123 2,161,289 2,161,289 2,263,113 2,360,780 2,453,266 2,542,200 2,542,200 1,168,016 1,174,385 1,144,138 1,385,529 1,385,529 1,385,529 1,385,529 1,385,529 1,385,529 1,385,529 1,385,529 2,513,491 2,653,654 2,800,155 3,482,652 3,546,818 3,546,818 3,648,642 3,746,309 3,838,795 3,927,729 3,927,729 Other property and equipment, net Deferred tax asset 7,700 14,114 20,361 21,173 21,514 21,738 21,738 21,738 21,738 21,738 21,738 21,738 21,738 52 26 26 Restricted investments Deferred Financing Costs 3,309 3,642 3,332 3,092 3,372 3,382 3,393 3,413 3,413 3,413 3,413 3,413 3,413 3,413 3,413 4,863 4,588 5,749 6,406 5,698 5,698 3,241 784 (1,673) (4,130) (4,130) Fair value of derivatives Acquisition deposit 46,138 2,299 900 28,500 Other assets, net Total Assets Current liabilities: Accounts payable and accrued liabilities Asset retirement obligations ‐ current 305 788,594$ 70,970$ 790 384 2,267,587$ 95,577$ 2,729 5,397 5,524 5,322 5,552 5,552 5,552 5,552 5,552 5,552 5,552 5,552 2,693,296$ 2,835,519$ 3,507,326$ 3,708,736$ 3,770,232$ 3,770,232$ 3,896,460$ 3,967,501$ 4,064,345$ 4,171,118$ 4,171,118$ 162,878$ 187,267$ 193,981$ 251,754$ 195,613$ 195,613$ 265,625$ 266,784$ 268,488$ 271,628$ 271,628$ 1,295 2,784 2,284 4,464 3,503 3,503 3,668 3,827 3,976 4,121 4,121 Accrued Interest Cash‐settled restricted stock unit awards 5,989 10,128 6,057 8,919 9,235 18,491 11,351 27,325 16,253 16,253 22,070 22,166 22,308 22,569 22,569 4,621 4,081 1,781 2,422 2,422 2,422 2,422 2,422 2,422 2,422 2,422 Fair market value of derivatives 18,268 27,744 25,912 35,948 47,167 47,167 47,167 47,167 47,167 47,167 47,167 47,167 Total current liabilities 87,877 131,550 205,773 238,535 245,345 333,132 264,958 264,958 340,952 342,366 344,361 347,906 347,906 6.125% senior notes, due 2024 6.375% senior unsecured notes due 2026, net of unamortized deferred financing costs Senior secured revolving credit facility Second lien term loan facility 40,000 288,565 390,219 595,196 595,374 595,552 595,729 595,729 595,729 595,729 595,729 595,729 595,729 595,729 392,907 392,799 392,799 392,799 392,799 392,799 392,799 392,799 392,799 25,000 75,000 65,000 140,000 140,000 125,000 125,000 125,000 125,000 125,000 Asset retirement obligations ‐ long‐term 4,317 3,932 4,725 7,717 7,782 5,428 10,737 10,737 11,243 11,728 12,187 12,629 12,629 Cash‐settled restricted stock unit awards Fair value of derivatives Deferred tax liability Other long‐term liabilities Total liabilities Stockholders' equity: 4,877 200 425,836 8,071 28 90 295 534,185 3,490 2,392 1,900 2,818 2,818 2,818 2,818 2,818 2,818 2,818 2,818 1,284 2,942 11,136 15,440 15,440 15,440 15,440 15,440 15,440 15,440 15,440 1,457 1,950 2,431 3,917 91 91 1,100 2,395 3,818 5,330 5,330 405 465 665 6,165 6,165 6,165 6,165 6,165 6,165 6,165 6,165 837,330 924,375 1,257,718 1,420,428 1,428,737 1,428,737 1,491,246 1,494,440 1,498,318 1,503,816 1,503,816 Preferred stock, $.01 par value Common Stock, $.01 par value 16 801 15 2,010 15 15 15 15 15 15 15 15 15 15 15 2,018 2,019 2,275 2,276 2,276 2,276 2,276 2,276 2,276 2,276 2,276 Capital in excess of par value 702,970 2,171,514 2,181,359 2,182,599 2,472,155 2,474,748 2,476,175 2,476,175 2,477,648 2,479,121 2,480,641 2,482,114 2,482,114 Retained earnings (deficit) Total stockholders' equity Total liabilities and stockholders' equity (341,029) 362,758 788,594$ (440,137) 1,733,402 2,267,587$ (327,426) (273,489) (224,837) (188,731) (136,971) (136,971) (74,725) (8,351) 83,096 182,896 182,896 1,855,966 1,911,144 2,249,608 2,288,308 2,341,495 2,341,495 2,405,213 2,473,061 2,566,028 2,667,302 2,667,302 2,693,296$ 2,835,519$ 3,507,326$ 3,708,736$ 3,770,232$ 3,770,232$ 3,896,460$ 3,967,501$ 4,064,345$ 4,171,118$ 4,171,118$

- 35. Callon Petroleum Company (CPE) November 14, 2018 35 CALLON PETROLEUM (CPE) Annual and Quarterly Balance Sheets As of Current assets: 31‐Dec‐15 A 31‐Dec‐16 A 31‐Dec‐17 A 31‐Mar A 30‐Jun A 30‐Sep A 31‐Dec E 31‐Dec‐18 E 31‐Mar E 30‐Jun E 30‐Sep E 31‐Dec E 31‐Dec‐19 E 2019 E2018 E Accounts receivable 28.8% 34.7% 31.2% 96.1% 81.7% 104.7% 92.2% 22.1% 94.2% 93.2% 92.2% 92.2% 27.4% Evaluated properties Net evaluated properties Unevaluated properties excluded from amortization 1698.2% 421.2% 96.1% 1371.3% 401.6% 332.9% 935.8% 2824.0% 2782.6% 2670.5% 3276.4% 787.0% 3203.8% 3052.8% 2518.7% 2409.3% 717.5% 367.1% 1160.8% 1208.1% 1300.8% 1605.8% 385.7% 1591.6% 1533.1% 1274.9% 1226.9% 365.4% 318.7% 921.5% 834.7% 859.4% 1029.4% 247.3% 974.4% 899.7% 720.0% 668.7% 199.1% Accounts payable and accrued liabilities 51.6% 47.6% 44.4% 146.9% 141.5% 156.2% 145.3% 34.9% 186.8% 173.2% 139.5% 131.1% 39.0% Asset retirement obligations ‐ long‐term 3.1% 2.0% 1.3% 6.1% 5.7% 3.4% 8.0% 1.9% 7.9% 7.6% 6.3% 6.1% 1.8% SELECTED COMMON SIZE BALANCE SHEET AMOUNTS (% of total assets) Total current assets Evaluated properties Net evaluated properties Unevaluated properties excluded from amortization 7.9% 296.1% 73.4% 16.8% 32.0% 121.5% 35.6% 29.5% 5.4% 5.2% 18.3% 5.1% 5.0% 5.0% 5.5% 4.8% 4.8% 5.2% 5.2% 127.3% 126.9% 108.8% 116.1% 117.0% 117.0% 116.9% 118.5% 119.2% 119.7% 119.7% 50.0% 52.2% 47.2% 56.5% 57.3% 57.3% 58.1% 59.5% 60.4% 60.9% 60.9% 43.4% 41.4% 32.6% 37.4% 36.7% 36.7% 35.6% 34.9% 34.1% 33.2% 33.2% Total current liabilities 11.1% 5.8% 7.6% 8.4% 7.0% 9.0% 7.0% 7.0% 8.8% 8.6% 8.5% 8.3% 8.3% Senior secured revolving credit facility 5.1% 0.0% 0.9% 2.6% 0.0% 1.8% 3.7% 3.7% 3.2% 3.2% 3.1% 3.0% 3.0% Asset retirement obligations ‐ long‐term 0.5% 0.2% 0.2% 0.3% 0.2% 0.1% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% Total liabilities Total stockholders' equity 54.0% 46.0% 23.6% 76.4% 31.1% 32.6% 35.9% 38.3% 37.9% 37.9% 38.3% 37.7% 36.9% 36.1% 36.1% 68.9% 67.4% 64.1% 61.7% 62.1% 62.1% 61.7% 62.3% 63.1% 63.9% 63.9%

- 36. Callon Petroleum Company (CPE) November 14, 2018 36 CALLON PETROLEUM (CPE) Annual and Quarterly Statements of Cash Flows In thousands For the period ended Cash flows from operating activities: Net income (loss) Adjustments: Depreciation, depletion and amortization 2015 A (240,139)$ 69,891 2016 A (91,813)$ 73,072 2017 A 31‐Mar A 30‐Jun A 30‐Sep A 31‐Dec E 2018 E 31‐Mar E 30‐Jun E 30‐Sep E 31‐Dec E 2019 E 120,424$ 55,761$ 50,475$ 37,930$ 53,583$ 197,749$ 64,069$ 68,198$ 93,270$ 101,624$ 327,160$ 118,051 36,066 39,387 48,977 40,482 164,912 43,775 47,933 53,115 56,666 201,488 2019 E2018 E Writedown of oil and natural gas properties Accretion expense Gain (loss) on sale of properties 208,435 660 95,788 958 677 218 206 202 4,479 5,105 859 841 815 800 3,315 22 (102) (80) Amortization of non‐cash debt related items Amortization of deferred credit 3,123 3,115 2,150 453 588 708 708 2,457 2,457 2,457 2,457 2,457 9,828 Non‐cash loss on early extinguishment of debt 9,883 Deferred income tax expense (benefit) 38,474 (14) 1,273 495 481 1,487 (3,826) (1,363) 1,009 1,295 1,423 1,511 5,238 Unrealized gain on derivative contract 38,135 Net loss on derivatives, net of settlements Loss on sale of other property and equipment Noncash charge ‐ stock compensation plans Non‐Cash Expense related to equity share‐based awards Change in the fair value of liability share‐based awards Payments to settle asset retirement obligations 6,658 221 6,612 (3,258) 558 6,953 (1,471) 10,429 (3,978) 8,572 25,102 29,696 62 8,254 1,131 1,627 1,708 1,427 5,893 1,473 1,473 1,520 1,473 5,940 3,288 1,012 (463) 879 1,428 (2,047) (366) (207) (507) (131) (1,211) (188) (197) (206) (214) (805) Changes in current assets and liabilities: Accounts receivable (4,761) (30,055) (44,495) (8,067) 10,447 (56,764) 44,702 (9,682) (9,910) (9,527) (33,864) (13,621) (66,922) Other current assets (20) (786) 108 61 (5,611) 3,885 (1,665) Current liabilities 8,001 25,288 30,947 12,938 4,123 47,740 (67,213) (2,412) 75,829 1,255 1,845 3,401 82,331 Change in other long‐term liabilities Change in long‐term prepaid Payments to settle vested liability share‐based awards related to early retirements Payments to settle vested liability share‐based awards 80 (3,538) (3,925) 96 (10,300) 121 (4,650) (13,173) (3,089) (1,901) (4,990) Other long‐term liabilities Other assets, net Cash provided (used) by operating activities Cash flows from investing activities: Capital expenditures 338 86,852 (227,292) (840) 118,567 (190,032) 87 200 5,500 5,787 (1,528) (507) (182) (709) (1,398) 229,891 92,215 107,764 116,036 74,211 390,226 179,374 113,727 120,375 154,097 567,574 (419,839) (111,330) (187,040) (156,982) (104,648) (560,000) (145,600) (145,600) (145,600) (145,600) (582,400) Acquisition expenditures Acquisition deposit Proceeds from sale of mineral interests and equipment (32,245) 377 (654,679) (46,138) 24,562 (718,456) (38,923) (6,469) (550,592) (595,984) 45,238 900 (28,500) 27,600 20,525 3,077 5,249 8,326 Cash provided (used) by investing activities (259,160) (866,287) (1,072,532) (149,353) (218,932) (674,725) (104,648) (1,147,658) (145,600) (145,600) (145,600) (145,600) (582,400) Borrowings on credit facility Payments on credit facility Payments on senior secured credit facility, net 181,000 (176,000) 217,000 (257,000) (300,000) 25,000 80,000 85,000 105,000 75,000 345,000 (15,000) (15,000) (190,000) (40,000) (230,000) (30,000) 30,000 Payments and extinguishment of debt Payments of preferred stock dividends (7,895) (7,295) (7,295) (1,824) (1,823) (1,824) (1,823) (7,294) (1,824) (1,823) (1,823) (1,823) (7,293) Proceeds from issuance of debt, net 400,000 200,000 400,000 400,000 Debt issuance cost Issuance of common stock 175,459 1,357,577 8,250 288,357 7 288,364 Payment of deferred financing costs Tax withholdings related to restricted stock units Cash provided (used) by financing activities Net increase (decrease) in cash and cash equivalents Cash and cash equivalents at beginning of period 172,564 256 968 (10,793) 1,399,489 651,769 1,224 (7,194) (8,664) (1,296) (9,960) (1,118) (560) (1,029) (215) (1,804) 217,643 47,616 601,841 61,672 73,177 784,306 (16,824) (1,823) (1,823) (1,823) (22,293) (624,998) (9,522) 490,673 (497,017) 42,740 26,874 16,950 (33,696) (27,048) 6,674 (37,120) 652,993 27,995 18,473 509,146 12,129 27,995 54,869 71,820 38,124 11,076 54,869 Cash and cash equivalents at end of period 1,224 652,993 27,995 18,473 509,146 12,129 54,869 54,869 71,820 38,124 11,076 17,750 17,750

- 37. Callon Petroleum Company (CPE) November 14, 2018 37 CALLON PETROLEUM (CPE) Ratios For the period ended Productivity Ratios Receivables turnover 2015 A 3.94 2016 A 3.67 2018 E 2019 E 2017 A 31‐Mar A 30‐Jun A 30‐Sep A 31‐Dec E 2018 E 31‐Mar E 30‐Jun E 30‐Sep E 31‐Dec E 2019 E 3.98 1.08 1.17 1.15 0.92 4.70 1.10 1.11 1.20 1.13 4.42 Oil and gas turnover 0.03 0.03 0.04 0.01 0.01 0.01 0.01 0.04 0.01 0.01 0.01 0.01 0.04 Working capital turnover 3.13 3.05 3.56 0.57 0.57 0.56 0.45 4.23 0.47 0.45 0.56 0.60 4.00 Net fixed asset turnover 0.19 0.18 0.18 0.05 0.05 0.05 0.04 0.18 0.04 0.04 0.05 0.05 0.19 Net fixed asset turnover (Production) 0.00 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 Total asset turnover 0.35 0.18 0.27 0.05 0.04 0.04 0.04 0.30 0.04 0.04 0.05 0.05 0.33 # of days sales in accounts receivable 105.17 126.81 113.86 86.45 74.33 96.30 84.79 80.81 84.79 84.79 84.79 84.79 100.18 # of year's costs in evaluated properties 33.72 38.59 29.64 25.06 24.55 22.49 27.46 27.07 25.66 24.45 23.00 22.21 24.78 # of days costs in operating payables 92.47 139.16 125.90 138.61 89.38 138.08 150.00 117.43 150.00 150.00 150.00 150.00 151.95 Liquidity Ratios Current ratio 0.71 5.51 0.70 0.62 2.61 0.57 0.71 0.71 0.63 0.55 0.57 0.62 0.62 Quick ratio 0.46 5.49 0.69 0.59 2.53 0.54 0.68 0.68 0.60 0.53 0.55 0.60 0.60 Cash ratio 0.46 5.49 0.69 0.59 2.53 0.54 0.68 0.68 0.60 0.53 0.55 0.60 0.60 Cash flow from operations ratio 0.99 0.90 1.12 0.39 0.44 0.35 0.28 1.47 0.53 0.33 0.35 0.44 1.63 Working capital ‐25,625 593,576 ‐60,913 ‐91,363 395,023 ‐144,157 ‐77,945 ‐77,945 ‐127,079 ‐152,662 ‐147,841 ‐131,091 ‐131,091 Financial Risk (Leverage) Ratios Total debt/equity ratio 1.17 0.31 0.45 0.48 0.56 0.62 0.61 0.61 0.62 0.60 0.58 0.56 0.56 Debt/equity ratio (excluding deferred taxes) 1.17 0.31 0.45 0.48 0.56 0.62 0.61 0.61 0.62 0.60 0.58 0.56 0.56 Total LT debt/equity ratio 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 LT debt/equity (excluding deferred taxes) 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 1.80 Interest coverage ratio (Earnings = EBIT) ‐8.91 ‐3.00 66.51 133.58 114.47 103.41 80.20 105.00 87.88 93.62 134.48 146.24 115.55 Interest coverage ratio (Earnings = EBI) ‐10.73 ‐3.00 65.92 132.50 113.66 101.32 79.47 103.80 87.08 92.74 133.50 145.19 114.63 Total debt ratio 0.54 0.24 0.31 0.33 0.36 0.38 0.38 0.38 0.38 0.38 0.37 0.36 0.36 Debt ratio (excuding deferred taxes) 0.54 0.24 0.31 0.33 0.36 0.38 0.38 0.38 0.38 0.38 0.37 0.36 0.36 Profitability/Valuation Measures Gross profit margin 29.98% 45.37% 54.81% 61.98% 62.16% 58.58% 58.67% 60.25% 57.80% 57.20% 62.11% 62.48% 60.25% Operating profit margin ‐152.07% ‐23.64% 38.60% 47.85% 49.17% 45.16% 41.84% 45.96% 43.44% 42.76% 49.32% 49.84% 46.82% Return on assets ‐68.32% ‐8.46% 11.04% 2.56% 2.17% 1.53% 2.16% 15.97% 2.59% 2.75% 3.76% 4.10% 26.36% Return on equity ‐126.87% ‐9.50% 11.68% 2.96% 2.43% 1.67% 2.31% 15.09% 2.70% 2.80% 3.70% 3.88% 21.10% Earnings before interest margin ‐164.69% ‐17.72% 38.84% 47.83% 49.25% 44.68% 41.98% 45.87% 43.54% 42.82% 49.33% 49.82% 46.85% EBITDA margin ‐85.89% 18.65% 71.40% 76.52% 78.34% 75.99% 72.45% 75.83% 74.73% 74.35% 77.29% 77.53% 76.19% EBITDA/Assets ‐29.95% 3.30% 19.43% 3.53% 3.39% 3.40% 2.61% 22.54% 2.77% 2.91% 3.70% 3.90% 25.42%