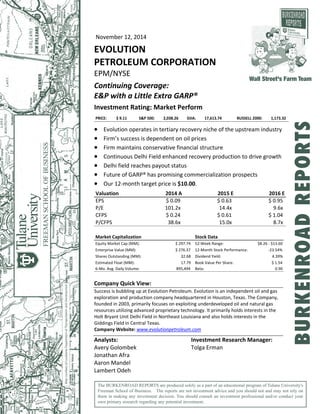

More Related Content Similar to Evolution Petroleum Burkenroad Report Similar to Evolution Petroleum Burkenroad Report (20) 1. November 12, 2014

EVOLUTION

PETROLEUM CORPORATION

EPM/NYSE

Continuing Coverage:

E&P with a Little Extra GARP®

Investment Rating: Market Perform

PRICE: $ 9.11 S&P 500: 2,038.26 DJIA: 17,613.74 RUSSELL 2000: 1,173.32

Evolution operates in tertiary recovery niche of the upstream industry

Firm’s success is dependent on oil prices

Firm maintains conservative financial structure

Continuous Delhi Field enhanced recovery production to drive growth

Delhi field reaches payout status

Future of GARP® has promising commercialization prospects

Our 12‐month target price is $10.00.

Valuation

EPS

P/E

CFPS

P/CFPS

2014 A

$ 0.09

101.2x

$ 0.24

38.6x

2015 E

$ 0.63

14.4x

$ 0.61

15.0x

2016 E

$ 0.95

9.6x

$ 1.04

8.7x

Market Capitalization Stock Data

Equity Market Cap (MM): $ 297.74 52‐Week Range: $8.26 ‐ $13.60

Enterprise Value (MM): $ 276.37 12‐Month Stock Performance: ‐23.54%

Shares Outstanding (MM): 32.68 Dividend Yield: 4.39%

Estimated Float (MM): 17.79 Book Value Per Share: $ 1.54

6‐Mo. Avg. Daily Volume: 895,494 Beta: 0.90

Company Quick View:

Success is bubbling up at Evolution Petroleum. Evolution is an independent oil and gas

exploration and production company headquartered in Houston, Texas. The Company,

founded in 2003, primarily focuses on exploiting underdeveloped oil and natural gas

resources utilizing advanced proprietary technology. It primarily holds interests in the

Holt Bryant Unit Delhi Field in Northeast Louisiana and also holds interests in the

Giddings Field in Central Texas.

Company Website: www.evolutionpetroleum.com

Analysts: Investment Research Manager:

Avery Golombek Tolga Erman

Jonathan Afra

Aaron Mandel

Lambert Odeh

The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's

Freeman School of Business. The reports are not investment advice and you should not and may not rely on

them in making any investment decision. You should consult an investment professional and/or conduct your

own primary research regarding any potential investment.

Wall Street's Farm Team

BURKENROADREPORTS

2. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

2

Figure 1: 5‐year Stock Price Performance

Source: Bloomberg November 16, 2014

INVESTMENT SUMMARY

We give Evolution Petroleum a rating of Market Perform with a 12‐month target price of

$10.00. To reach this target price we used the present value of estimated future oil and gas

returns, net of estimated direct expenses, discounted at an annual rate of 10%. Evolution is a

petroleum exploration and production (E&P) company that focuses on underdeveloped

onshore oil fields.

Evolution will continue to realize steady cash flows from the Delhi field, its sole significant

revenue producing asset. Delhi proved and probable reserve volumes have grown 8%, to 22.6

million barrels of oil and the field has a reserve life index of approximately 18 years. Future

strategy is to increase free cash flow from the Delhi Field, commercialize its Gas Assisted Rod

Pump (GARP®), and increase shareholder returns. The reversionary interest agreement with

Denbury Resources reached its payout during October, 2014.

Additionally, Evolution continues to focus business efforts on the commercialization of its

GARP® technology. After the Company’s divestment of most non‐GARP® operated properties,

Evolution underwent a substantial restructuring. Several management changes occurred,

including the appointment of top management to GARP® related positions and a reduction in

engineering staff. As such, Evolution’s unlevered financial structure, risk‐averse operations,

significant cash flow, and near‐maximum Delhi production make it an attractive option for

acquisition.

3. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

3

Table 1: Historical Burkenroad Ratings and Prices

Date Rating Price*

03/17/14 Market Perform $14.00

03/28/13 Market Outperform $13.00

04/05/12 Market Outperform $14.00

03/25/11 Market Outperform $14.00

04/14/10 Market Outperform $11.05

*Price at time of report date

INVESTMENT THESIS

We have established a 12‐month target price of $10.00 and a rating of Market Perform.

Evolution operates in tertiary recovery niche of the upstream industry

Evolution Petroleum operates within a specific niche of the oil exploration and production

(E&P) industry. The Company focuses on tertiary oil production and does not engage in the

exploration of reservoirs, which requires large capital expenditures and can be highly

speculative. Specifically, Evolution’s operations utilize a highly specialized proprietary

technology to enable tertiary recovery. The Company implements horizontal drilling and

artificial lifts to increase the useful life of wells and enhance petroleum recovery from

previously productive yet underdeveloped formations.

Firm’s success is dependent on oil prices

Evolution’s financial success is largely dependent on the market price of oil. Energy prices can

be volatile in the short term because of geopolitical and economic uncertainties. This volatility

impacts Evolution’s market price because oil is the firm’s main generator of revenues.

Additionally, Evolution has refrained from implementing any hedges on its oil production,

making the firm even more vulnerable to a price drop in oil.

Continuous Delhi Field enhanced recovery production to drive growth

Currently, the Delhi Field is Evolution’s main asset. Purchased in 2003, the Delhi Field

encountered some stoppages around the end of 2013 but has since stabilized. Enhanced

recovery well production remains steady and recent annual performance has met

expectations.

4. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

4

Delhi proved and probable reserve volumes have grown 8%, to 22.6 million barrels of oil. The

Delhi field has a reserve life index of approximately 18 years. Evolution will rely heavily on the

continued success of the well for the next 18 years because the firm is not actively seeking new

projects.

Delhi Field reaches payout status

In 2006, Evolution Petroleum entered into an agreement with Denbury Resources to redevelop

the Delhi Field. The agreement dictated a revenue sharing arrangement where Evolution

assumes none of the cost and receives a portion of the revenue until Denbury receives its full

investment, plus any predetermined amount of return. Evolution received a 7.4% royalty

interest from all gross revenues and paid no capital or operating expenses. The terms of the

agreement are beneficial to Evolution because they allow the Company to generate significant

revenue, while Denbury maintains the well. Denbury pays the majority of costs for the Delhi

Field, resulting in expected post‐reversionary cash flows for Evolution considerably greater

than net capital expenditures. The 23.9% reversionary working interest in the field activated

during October, 2014. This revision is expected to result in an approximate 360% increase in

yearly revenue.

Future of GARP® has promising commercialization prospects

As of December 2013, management completed a corporate restructuring initiative, which

included: its divestment of all non‐Gas Assisted Rod Pump (GARP®) operated properties,

compensation for engineering‐related employees to leave the Company, and the appointment

of several C‐Suite members to lead the commercialization of GARP®. Evolution’s proprietary

and patented GARP® technology is at the forefront of Evolution’s business plan.

GARP® technology requires relatively minimal capital investment to commercialize and offers

considerable growth potential. Compared to the fourth quarter ended June 2013, revenue

from previous GARP® installations grew by 64% and daily sales volumes increased 201%.

Recently, Evolution has installed three GARP® wells, which will contribute to revenue growth in

2015. In recent commercialization efforts, management sought to educate industry

professionals about GARP® in an effort to increase implementation of the technology. As a

result of these efforts, two additional wells are scheduled to implement the technology in the

coming months.

Future cash flows structures from GARP® technology remain in the planning stages.

Management expects to provide forthcoming installations on a fee basis but is considering

alternative business structures. One consideration is assuming all capital expenditures for

GARP® installation on additional wells, in exchange for compensation on a production basis.

5. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

5

Firm maintains conservative financial structure

Evolution is an attractive company because of the firm’s unlevered financial structure, risk‐

averse operations, and significant cash flow. First, the Company’s capital structure of

maintaining zero‐debt minimizes bankruptcy risk. Furthermore, Evolution invests in projects

that do not involve large capital expenditures and evades speculative decisions. As a result,

Evolution is able to offer higher return on invested capital. Management built Evolution on this

platform, making the firm an attractive asset for other companies.

VALUATION

Our analyst team gives Evolution Petroleum a Market Perform rating. Our 12‐month target

stock price projection is $10.00. We used the present value of estimated future oil and gas

returns, net of estimated direct expenses, discounted at an annual rate of 10% over seven

years.

PV‐10

The PV‐10 model is a standard valuation measure for the exploration & production industry.

This model takes the present value of cash flows from production, net of operating expenses,

discounted at the annual 10% industry standard.

Our PV‐10 model uses two sources to determine projections of prices and productions. The

Burkenroad price deck is used to determine future prices of oil and production estimates are

calculated based upon information supplied by the Company. The Burkenroad price deck is

determined by the NYMEX West Texas Intermediate futures contract prices combined with the

U.S. Energy Information Administration (EIA) Short‐Term Outlook forecasts and the EIA Annual

Energy Outlook to derive long‐term prices of oil, natural gas, and natural gas liquids. After

calculating cash flows, we discounted by 10% to arrive at a rounded price of $10.00.

INDUSTRY ANALYSIS

Companies operating in the petroleum industry explore, extract, refine, and transport

petroleum products. The three main sectors in this industry are upstream, midstream, and

downstream. Upstream companies explore, extract, or produce oil and natural gas liquids

(NGL). Midstream companies transport, store, and serve as the middle man between upstream

and downstream companies. The downstream companies refine the products and sell them to

end users.

6. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

6

Major companies in the industry include Royal Dutch Shell, ExxonMobil, Chevron, and British

Petroleum. These companies are well‐integrated and operate in all three sectors. Evolution

Petroleum is an upstream company because the majority of its revenues come from

extraction.

Extraction & Production Industry

The U.S. oil drilling and gas extraction industry had revenues of $393.3 billion in 2013 and

analysts expect that figure to grow by 3.6 % to $407.7 billion in 2014. Expected growth rates

for crude oil and NGL production in 2014 are 13% and 10%, respectively. The International

Energy Agency forecasts that the U.S. will lead the world in oil production by 2017 and has the

potential to be a net oil exporter, dependent on the regulatory environment. Favorable sector

forecasts are a result of improvements in industry technology and techniques, a reduction in

U.S. dependence on foreign oil, and the generally positive movements of key industry drivers.

Key Drivers of the Oil and Gas industry:

• Price of crude oil

• Price of natural gas

• Regulations in the Petrochemical Manufacturing industry

• Total global vehicle miles

• Trade‐weighted index

In October 2014, the International Monetary Fund forecasted the average 2015 price of oil to

be $99.36 per barrel. Similarly, the U.S. Department of Energy expects the price of NGLs to

increase an average of 2.6% annually through 2019. According to Bureau of Transportation

statistics, total global vehicle miles are projected to be 3.13 trillion in 2015. International crude

oil prices continued on a downward trajectory from September through November 2014,

falling under $100 per barrel (bbl) for the first time since June 2012. In October 2014, Goldman

Sachs forecasted oil prices would fall to $70 in 2015. The value and stock price of exploration

and production (E&P) companies are correlated with changing oil and NGL prices. Additionally,

the industry is subject to numerous Federal and state‐level regulations and changing laws

could significantly impact E&P companies in the future.

Macroeconomic Trends

Global economic and political factors affect product prices. An example is the Organization of

Petroleum Exporting Countries (OPEC) which consists of 12 countries holding substantial oil

exports. OPEC leverages political ties to control product prices. In October 1973, the

organization established a trade embargo which heavily impacted prices.

8. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

8

Figure 2: Projected World Energy Consumption in Quadrillion Btus

Source: EIA, International Energy Outlook 2014

Oil Prices Are Dependent on Numerous Conditions

Volatility in oil prices stem from geopolitics, economic uncertainties, government action, and

climate. In the short term, prices may be volatile due to supply and demand disruptions. As of

August 2014, the EIA increased its forecasts for next year’s oil prices. The two primary

benchmarks for oil prices are West Texas Intermediate (WTI) and Brent. WTI oil forecasts for

2015 average $90.55, down from October’s estimate of $95.17. Brent oil is projected to rise

from $104.92 to $105.

In addition, Petroleum product prices face potential disruption when major suppliers are in

areas of political unrest. The Strait of Hormuz accounts for 20% of global oil flow on a daily

basis; the Strait processed about 17 million barrels per day (bbl/d) in 2011. This key

transportation hub faces security issues, which could impact the shipment of oil and influence

product prices.

Ever‐changing Regulatory Environment

Government regulations play an important role in the oil and natural gas industry. Laws and

regulations change over time due to a variety of factors including the political landscape and

environmental consequences of extraction and consumption of fossil fuels. Although future

regulations could threaten the profitability of E&P companies, the states which the Company

operates in, Texas and Louisiana, promote the growth of the oil and gas industry through

taxation incentives.

9. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

9

The legislative issue of most concern for E&P companies today is hydraulic fracturing. Recently,

the Environmental Protective Agency (EPA) ruled that hydraulically fractured gas wells may

continue to flare byproducts until January 1, 2015. Upon that date, companies must capture

95% of the volatile organic compounds emitted annually by their wells or face fines. This has a

significant impact on the daily operations of E&P companies.

Customers

The customer base of upstream companies is predominantly comprised of two groups:

midstream and downstream companies. E&P companies acts as the supplier of the raw

commodity. Midstream companies enable product transportation while downstream

companies facilitate the refining and finishing of petroleum products. Evolution’s customers

also include other E&P companies that lease out Evolution Petroleum’s proprietary Gas

Assisted Rod Pump (GARP®) technology.

Evolution receives an overwhelming majority of its revenue from a single customer. In fiscal

year 2014, Plains Marketing LP, a midstream company, accounted for 96% of Evolution

Petroleum’s revenues. However, Evolution’s business risk regarding Plain Marketing is minimal

since the Company’s main product offering, Louisiana Light Sweet Oil, is considered highly

desirable.

Competitors

Competitors within the oil and natural gas industry focus on two main tasks: the acquisition of

oil prospects and acreage, and the successful retrieval of oil and natural gas. Evolution

Petroleum competes with a large range of E&P companies spanning small market capitalization

firms to some of the largest companies in the world. Evolution Petroleum and companies of

similar size face a disadvantage to larger companies who have more extensive staffs and larger

capital resources. Larger companies with higher monetary and human capital can afford to do

more tasks in‐house and minimize outsourcing. Though outsourcing can minimize liabilities,

larger companies have the ability to increase efficiency by monitoring their operations more

closely. Furthermore, larger companies that conduct all their operations themselves can realize

additional revenues that they would otherwise have to share with partnered firms. Because of

its limited resources and conservative management approach, Evolution prefers to share

revenues with contracted partners.

10. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

10

Minimal Threat of New Entrants

The threat of companies entering the E&P industry is minimal. The largest barrier for potential

entrants is the high capital expenditures necessary to compete in the industry. Particularly,

entrants must fund the process of finding reserves, drilling profitable wells, buying licenses,

implementing advancing technology, and transporting the product. The capital‐intensive

environment and number of established firms make the threat of entry low.

On top of capital requirements, companies in the E&P industry must attract talented and

experienced human capital. Many firms have engineers, geophysicists, and other professionals

capable of providing field expertise and knowledge. Such experts are able to approximate the

expenditure and profitability of projects.

Bargaining Power of Suppliers

Suppliers for E&P companies provide field services and equipment for exploration activities.

The large amount of service providers for E&P weakens supplier bargaining power due to

competitive market pricing. Firms which focus on providing services for secondary and tertiary

recovery companies, such as Evolution, have higher bargaining power than suppliers for

regular E&P companies. Evolution uses horizontal drills and hydraulic fracturing machines.

These structures are more expensive and difficult to maintain than regular wells. Therefore,

these specialized suppliers have the capability to negotiate prices more than suppliers of

traditional E&P companies.

Bargaining Power of Buyers

Market prices for crude oil and natural gas determine the bargaining power of buyers. This

bargaining power is low because the market is independently volatile. However, quality of raw

product gives buyers some bargaining power. Oil density and sulfur content are the

determining factors of product quality. Oil that contains more sulfur and is more dense is less

favorable. Buyers will demand lower prices for lower quality to compensate for the capital

expenditures incurred during the refining process. Based on quality, Evolution receives a

premium on its Delhi Louisiana Light Sweet oil.

ABOUT EVOLUTION

Evolution Petroleum Corporation (EPM/NYSE) is a petroleum recovery and production

company focused on extracting oil and gas resources from underdeveloped onshore sites. The

Company maintains rights and operates in underdeveloped onshore fields in Texas, Louisiana,

and Oklahoma. Evolution Petroleum is headquartered in Houston, Texas and employs eleven

full‐time staff, not including contract personnel, and outsourced service providers.

15. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

15

Latest Developments

GARP® Gains Recognition

A major development in the E&P industry, specifically related to Evolution, is the

implementation of GARP® technology in wells. This year, GARP® received the 2014 Exploration

and Production Special Meritorius Award for Engineering Innovation. The patented technology

was recognized as an innovative, sustainable, and practical solution to improving the efficiency

and profitability of tertiary recovery wells.

Delhi Leak and Litigation

In June 2013, Denbury resources discovered an underground fluid release in the Delhi Field.

Denbury suspended operational activities in the leak area, lowering pressure and oil

production in wells within affected areas. This impacted the predicted timing of the additional

royalty payout outlined in the reversionary agreement. Denbury disclosed a gross $120 million

of additional costs before insurance reimbursement. The combination of effects lowered

Evolution’s present value of proved reserves, subsequently increasing probable reserves. As a

result, the working interest change was delayed into late 2014. Evolution is currently entering

the discovery phases of a lawsuit against Denbury to enforce the agreement made in 2006.

October 2014 Oil Volatility

Current market conditions directly impact Evolution’s stock price because oil is the firm’s main

generator of revenue and the price of oil recently declined to four‐year lows. This decrease in

price was due to several factors, including Saudi Arabian producers selling product at a

discount. On October 27th, 2014, Goldman Sachs forecasted oil prices would fall further to $70

in 2015. With the value of oil products uncertain, Evolution’s market price dropped nearly 20%

within a six‐week span.

PEER ANALYSIS

Evolution Petroleum’s business strategy is unique within the upstream industry as the

Company solely focuses on production. Because Evolution only invests in previously developed

oil wells, the Company does not participate in speculative projects. The selection of peer

companies within the upstream sector shown in Table 2 is based on a combination of factors

including: market capitalization, business operations, geographic location, and petroleum

products.

16. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

16

Table 2: Peer Comparison

Company Ticker

Market

Capitalization

P/E P/BV

EV/

EBITDA

D/E ROE

Div.

Yield

Proved

Reserves

(MBOE)

Evolution

Petroleum

EPM 299.40MM 101.44 1.591 40.99 0% 6.7% 4.38% 13,289

Approach

Resources

AREX 549.20MM 22.6 1.65 7.07 35.19% 10.5% N/A 114,700

Denbury

Resources

DNR 5,110 MM 26.18 .98 8.58 63.02% 3.77% 1.7% 468,300

Royale Energy ROYL 43.44M 41.64 134.67 N/A 178.9% 4.3% N/A 652,371

Saratoga

Resources

SARA 32.85MM 0.23 1.591 7.62 62.06% 5.48% N/A 17,200

Yuma Energy YUMA 301.28MM 171.67 2.16 N/A 0% 1.45% N/A 449

Peer Average 1,207MM 52.46 28.21 7.76 68% 5.1% 1.7% 250,604

Source: Bloomberg October 2014

Evolution Petroleum has a price to earnings ratio of 104.44x and a return on equity of 6.7%,

the second highest among its peers in both categories. The high price to earnings (P/E) ratio is

testament to investor’s beliefs in the Company’s growth prospects. Evolution also has the

highest enterprise value to earnings before interest, taxes, depreciation, and amortization

(EBITDA) ratio and the highest dividend yield among its peers, 40.99x and 4.38%, respectively.

The majority of Evolution’s peers carry debt with an average debt‐to‐equity ratio of 68%, but

Evolution, like its peer Yuma, carries no debt.

Approach Resources Inc. (AREX/NASDAQ)

Approach Resources is a small cap energy company from Fort Worth, Texas. The company

engages in the acquisition, exploration, development, and production of unconventional oil

and gas reserves in west and east Texas. Similar to Evolution, Approach focuses on low‐cost,

unconventional techniques, which reduces risks and improves margins. With a market

capitalization of $549.18 million, Approach is approximately double the size of Evolution.

Unlike Evolution, Approach continues to explore by drilling 16 new wells during the second

fiscal quarter of 2014. Approach operates 741 producing wells.

Denbury Resources Inc. (DNR/NYSE)

Denbury Resources Inc. is an oil and natural gas company headquartered in Plano, Texas. The

firm operates in two areas: the Rocky Mountains and the Gulf Coast. In relation to Evolution,

Denbury is both a direct competitor and contracted operator. Similar to Evolution, Denbury

specializes in Enhanced Oil Recovery (EOR), which is a form of tertiary recovery. Furthermore,

EOR uses CO2 technology to extract undeveloped petroleum reserves. Denbury and Evolution

have a joint venture in the Delhi Field, Evolution’s main producing field.

17. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

17

Although Denbury and Evolution operate similarly, Denbury operates on a larger scale with a

market capitalization of $5.11 billion. On December 31, 2013, proved oil and natural gas

reserves were 468 million barrels of oil equivalent (MMBOE).

Royale Energy, Inc. (ROYL/NYSE)

Royale Energy, Inc. is an oil and natural gas producer headquartered in San Diego, California.

Compared to Evolution Petroleum, Royale has half as many outstanding shares with 14.9

million shares and one‐sixth the market capitalization at $38.85 million. At the end of 2013,

Royale had 19 full‐time employees. The Company engages in three lines of business: drilling of

exploratory wells, acquiring lease interests and proved reserves, and producing hydrocarbon

products for distribution. The company mainly focuses on primary and secondary recovery of

oil and natural gas. Operations are predominantly in Northern California but the Company also

pursues lease interests in Utah, Louisiana, Texas, Oklahoma, and Alaska. The company has

652,371 MMBOE in proved reserves.

Saratoga Resources Inc. (SARA/NYSE)

Saratoga Resources is an oil and natural gas company engaged in the acquisition, development,

exploitation, and production of natural gas and crude oil properties in southern Louisiana and

the Gulf of Mexico shelf. The Houston‐based company has a total 52,103 acres under leases

and engages in numerous low‐risk opportunities. The company has 86 total producing wells

but will increase production with a recent purchase of 20,000 acres in the Central Gulf of

Mexico.

Yuma Energy Inc. (YUMA/NYSE)

Yuma Energy is an oil and gas company headquartered in Houston, Texas with 27 employees.

Yuma focuses on exploration and development of unconventional and conventional oil and

gas, targeting the gulf coast and California. Yuma recently finalized a merger with Pyramid Oil

Company increasing projected cash flows and production. Unlike Evolution, Yuma uses 3‐D

seismic surveys to identify high‐impact, deep‐onshore prospects located beneath known

producing trends. This method classifies all of Yuma’s production as primary recovery. Yuma

has developing assets in the Bakken in North Dakota, an unconventional liquids rich resource

play.

MANAGEMENT PERFORMANCE AND BACKGROUND

Evolution Petroleum’s skilled management team has an average of 25 years’ experience in the

industry, specifically in petroleum engineering and energy financial management.

18. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

18

Management’s conservative style is demonstrated by the firm’s zero debt capital structure and

the Company’s commitment to projects with proven profitability. Evolution employees own

27.85% of shares outstanding in the Company. Evolution’s management are invested in the

Company’s future and are aligned with the interests of shareholders.

Return on Invested Capital

Return on Invested Capital (ROIC) is a measurement of how well a company uses capital to

generate returns. A lower ROIC means a company is not efficiently using its capital to generate

returns while a higher multiple shows a company is more profitable with its capital. When

analyzing ROIC, capital structure must be considered since a company’s financing can

significantly alter ROIC figures.

ROIC is often an ideal ratio for analyzing oil and gas companies that invest large amounts of

capital to fund new drilling efforts. Unlike its competitors, Evolution does not participate in

new drilling efforts. Instead, Evolution enters partnerships to minimize capital expenditures.

Thus, the Company’s ROIC is inflated. Table 3 compares Evolution’s ROIC to the ROIC of its

peers from years 2011 to 2013.

Table 3: Return On Invested Capital

Company 2013 ROIC 2012 ROIC 2011 ROIC

Evolution Petroleum 13.15% 12.85% (.74)%

Approach Resources 9.58% 1.51% 2.24%

Denbury Resources 6.06% 8.37% 9.52%

Royale Energy 274.65% (191.60)% (32.27)%

Saratoga Resources (5.80)% 4.08% 22.37%

Yuma Energy 1.45% 7.56% 11.72%

Peer Average 57.19% (42.90)% 2.72%

Source: Thomson One October 2014

Robert Herlin

Chairman of the Board, Chief Executive Officer (59)

Robert Herlin has served as Chief Executive Officer of Evolution Petroleum since 2003 and as

Chairman of the Board since 2010. With over 30 years in the petroleum industry, Mr. Herlin

has engineering, energy, and finance experience. He oversees all financial, strategic, and

operational activities. Herlin obtained his Masters of Business Administration (MBA) from

Harvard University after obtaining Bachelor of Science (BS) and Master of Engineering (ME)

degrees in chemical engineering from Rice University.

19. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

19

Randall Keys

President, Chief Accounting Officer, Chief Financial Officer (54)

Randall Keys has been with Evolution since January 2014 and became President in September

2014. Mr. Keys has 28 years of experience in financial management of small‐cap public

petroleum companies. He directs daily operations of the Company and manages marketing for

the NGS Technologies subsidiary that is commercializing the Company’s GARP® technology. He

obtained BS and ME degrees in chemical engineering from Rice University and an MBA from

Harvard University.

Daryl Mazzanti

Vice President of Operations (52)

Daryl Mazzanti joined Evolution in 2005 to administer its oil and gas field operations. Mazzanti

holds over 20 years of oil and gas operations experience and has managed operations for

several petroleum companies. Prior to Evolution, Mazzanti managed Andarko Petroleum’s U.S.

business development by overseeing operations at Andarko’s Austin Chalk site. Mazzanti takes

a leading position in Evolution’s lateral drilling and lifting by facilitating the commercialization

of GARP®. Mazzanti holds a BS degree in petroleum engineering from the University of

Oklahoma.

David Joe

Vice President, Chief Administrative Officer, Controller, Corporate Secretary (49)

David Joe became a part of Evolution in mid‐2005 to facilitate the reporting of Evolution’s

financial activity. Previously, Joe was a Client Manager for P2 Energy Solutions, providing

outsourced accounting services to the petroleum industry. Joe coordinates Evolution’s

accounting services, financial activity, and corporate audits. Joe holds over 20 years of

experience in oil and gas accounting. Joe received a Bachelor of Business Administration (BBA)

in accounting from the University of Texas at Austin and is a Certified Accredited Petroleum

Accountant.

Board of Directors

The current Evolution Petroleum board of directors holds over 100 years of combined

experience in the oil and gas industry. The five members have held leadership positions in

other petroleum firms and hold large equity stakes in the Company (see Table 4).

20. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

20

Table 4: Evolution’s Board of Directors

Board Member Board Position Professional Affiliation

Robert Herlin Chairman CEO of Evolution

Edward DiPaolo

Lead Director & Chairman of

Nominating/Governance

Senior Adviser for Duff

& Phelps Securities

Gene G. Stoever Chairman of Audit Committee

Retired Audit Partner

KPMG

William E. Dozier Chairman of Compensation Committee

Independent oil and

gas Consultant

Kelly Loyd

Member of the Compensation

Committee, Member of the Nominating

and Corporate Governance Committee

Manager at JVL

Advisors

Source: Thompson One October 12, 2014

SHAREHOLDER ANALYSIS

As of September 10, 2014, Evolution Petroleum had 32,793,414 shares outstanding.

Evolution’s shareholders are primarily value investors. Institutional investors held the majority

of Evolution stock, approximately 72%, as of October 10, 2014. Insider investors held the

remaining 27.85%.

Investor Analysis

The total number of shares held by the top‐ten investors is 17,997,139 shares outstanding, or a

54.99% equity stake in Evolution. JVL Advisors is the largest institutional holder with 10.4% of

outstanding shares. Eric McAfee, the second largest stockholder and a member of Evolution’s

board, owns 8.59% of outstanding shares.

The categorical breakdown of Evolution Petroleum owners, as of October 10, 2014, is as

follows (see Table 5): 64.41% are investment advisors, 26.84% are individual investors, and

7.70% are hedge fund managers. Table 5 shows the investment styles of the firms that own

Evolution Petroleum’s shares, with hedge funds comprising 21.1% and Growth at Reasonable

Price investors comprising 15.05%. Approximately 98% of Evolution’s investors are located in

the U.S.

21. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

21

Table 5 ‐ Investment Styles of Investors

Investment Style Investors Outstanding Shares Shares

Hedge Fund 21 21.10% 6,919,569

Growth at Reasonable Price 19 15.05% 4,935,903

Deep Value 9 11.47% 3,760,793

Core Value 15 10.58% 3,470,382

Core Growth 26 8.87% 2,910,403

Index 19 6.76% 2,215,674

Broker‐Dealer 14 1.79% 586,918

Aggressive Growth 3 0.36% 118,911

Source: Thompson One October 10, 2014

Institutional Holdings

Total institutional holdings have increased from 58% at the beginning of fiscal 2014 to 72% as

of October 2014. There have been eight self‐offs by institutional investors in the last 12

months; however, the ownership of institutional investors has increased. The largest sell offs

were 325,610 shares by Reinhart Partners and 315,633 shares by Nantahala Capital

Management. Table 6 shows the largest institutional shareholders as of March 27, 2014. JVL

Advisors is the largest institutional shareholder with 10.4% of shares outstanding. River Road

Asset Management is the second largest institutional shareholder with 5.57% of shares

outstanding.

22. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

22

Table 6 ‐ Top Institutional Holders

Top Institutional Holders Shares Outstanding Shares

JVL Advisors, L.L.C. 3,392,276 10.40%

River Road Asset Management, LLC 1,826,832 5.57%

Wellington Management, LLC 1,730,617 5.28%

Neuberger Berman Group, LLC 1,465,050 4.47%

Thomson Horstmann & Bryant, Inc. 1,024,421 3.14%

Brandywine Global Investment Management, LLC 920,762 2.82%

Kennedy Capital Management, Inc. 808,601 2.48%

Lazard Asset Management LLC 787,900 2.42%

Nantahala Capital Management, LLC 713,213 2.19%

Cortina Asset Management, LLC 626,797 1.92%

Source: Bloomberg October 10, 2014

Insider Holdings

Total insider holdings amount to 27.85% of shares outstanding as of October 10, 2014. Table 7

shows the largest insider shareholders ordered by total amount of shares. Eric McAfee is the

largest insider shareholder with 8.59% of all shares outstanding. Insider positions have

increased 2.25% over the last 12 months. The largest recent purchases by insiders were Scott

Bedford increasing his position by 400,000 shares in October of 2013, and Sterling McDonald

increasing his position by 350,175 shares in January of 2014.

23. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

23

Table 7 ‐ Top Insider Holders

Top Insider Holders Shares Outstanding Shares

McAfee, Eric A 2,816,902 8.59%

Bedford, Scott 2,369,510 7.23%

Herlin, Robert S 1,642,165 5.01%

McDonald, Sterling H 759,935 2.32%

Mazzanti, Daryl V 695,676 2.12%

Davidson, Joe 253,968 0.77%

DiPaolo, Edward 186,010 0.57%

Stoever, Gene 168,839 0.51%

Dozier, William E 111,397 0.34%

Keys, Randall D 99,394 0.30%

Source: Bloomberg October 10, 2014

RISK ANALYSIS AND INVESTMENT CAVEATS

As a small Exploration and Production (E&P) company, Evolution Petroleum faces risks which

are common among companies in the oil and gas industry. The inherent operational, financial,

and regulatory risks can have significant impact on short‐term and long‐term capital

expenditures, production, cash, and revenues.

Operational Risks

Competition for Resources

E&P companies, such as Evolution, seek to grow operations by acquiring additional reserves.

The amount of production in a well decreases over its lifespan. Therefore, E&P companies

must obtain additional wells with proven reserves to grow production. Evolution faces growth

challenges since larger firms are able to allocate more capital towards expansion. Considering

Evolution’s is a small company with a capital structure of no debt, it may be challenging to

compete with firms that have more cash available.

24. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

24

Evolution’s Dependency on Key Personnel

Evolution is comprised of only nine highly‐skilled employees who contribute to the daily

functions of the corporation. Evolution’s management is responsible for facilitating deals,

guiding operations, and obtaining capital. The Company could face major operational

consequences from the loss of key personnel.

Present Risks of the Delhi Field

The Delhi Field, located in northern Louisiana, is Evolution’s most significant asset and accounts

for 90% of overall Firm production. Any unexpected issues within the Field could impact the

Firm significantly. An example of such an issue is the June 2013 fluids leak. Additionally,

Evolution’s current litigation with the Delhi Field operator could hinder future production and

disrupt the reversionary working interest agreement.

Similarly, Evolution is reliant on its operator, Denbury Resources. Because Denbury conducts all

processes in the field, Evolution does not manage the daily operations of its main source of

revenue. Considering Evolution’s lack of control and undiversified asset portfolio, the Firm is

left vulnerable.

Commodity Market Volatility

Oil and natural gas prices directly impact Evolution’s profitability. For oil and gas companies,

future revenues, cash flows, and growth rates are dependent on product prices. For E&P

companies to stay profitable, well economics must be efficient. A financially viable project

requires that extracted product values exceed production costs. In October 2014, the drop in

commodity prices directly impacted the stock price for many E&P companies. As of October 15,

2014, Evolution’s stock price had dropped by nearly 20% from the beginning of the month. E&P

companies can minimize this risk through hedging strategies. However, Evolution does not

hedge production, making the Company more vulnerable to price decreases than many of its

peers.

Minimal Customer Base

Evolution relies on product transporters to maintain established contracts. Product

transporters are midstream companies which deliver crude oil and natural gas to the

downstream portion of the business. Plains Marketing, a mid‐stream company, accounts for

90% of revenues and is Evolution’s primary customer. The continued partnership between

Plains Marketing and Evolution is important for stable future revenues.

25. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

25

Estimation of Reserves

For E&P companies, a primary concern is the calculation of crude oil and natural gas

production because production directly impacts company value. This estimation depends on

many variables, including the engineering methods, field geography, and surrounding field

performance. Consistent with industry practices, Evolution consults independent third parties

when selecting fields for operation. Forecasts from reservoir engineers are susceptible to error

and, as a result, actual production may be substantially different than projections.

Ongoing Concerns of Tertiary Recovery

Evolution acquires petroleum products through tertiary recovery. This method of recovery

harvests leftover product in partially depleted reservoirs. All E&P companies with tertiary

recovery face several uncontrollable risks, including weather conditions, changing reservoir

pressures, and other unfavorable drilling conditions. For example, the Delhi Field’s production

slowed in the summer of 2012 because of extremely high temperatures and the associated

cost of cooling the processing facility. All E&P companies face similar risks.

Uncertain Commercialization of GARP®

Evolution’s patented technology, Gas Assisted Rod Pump (GARP®), could potentially offer

extended life for many horizontal and vertical wells. The Company is attempting to

commercialize the technology. As such, Evolution has installed the technology in wells hoping

successful results will build industry reputability. However, the technology has not been

recognized as an industry‐wide form of tertiary recovery due to minimal trial runs and

uncertain results.

Regulatory Risks

Government Regulations Can Potentially Change

The political environment concerning oil and gas extraction and production is heavily

regulated. Various federal and state governments regulate Evolution’s business operations for

environmental, financial, and operational reasons. Changes in legislation could increase

operating costs, negatively impacting Evolution. Additionally, the Environmental Protection

Agency (EPA) requires E&P companies to monitor and report annual greenhouse emissions. As

such, stricter regulations and production limits could force Evolution to change its production

process.

26. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

26

EPA Regulations Provide Incentive to Innovate and Upgrade Technology

EPA policies frequently change as a result of evolving legislation. The E&P industry is heavily

regulated for the prevention of environmental damage. A recent policy change affecting E&P

companies is the requirement to reduce emissions from storage tanks, flares, and coking units.

Also, the EPA requires the active monitoring of benzene and is eliminating all emission limit

exemptions during periods of well startups, shutdowns, and malfunctions. The oil and gas

industry must continually comply with the EPA’s changing regulations and incur associated

costs.

Another regulation imposed by the EPA is for the necessary capture of volatile organic

compounds, air toxins, and methane from natural gas wells. After January 1, 2015, all

extraction companies will be required to trap and store these toxic gases. Companies will be

fined for failing to capture these gases, resulting in additional expenditures. In response to

these new requirements, Evolution has decided to construct a gas recycling plant to recover

methane, natural gas liquids (NGLs), and waterflood.

FINANCIAL RISKS

Leverage Risk Analysis

Leverage ratios measure a company’s debt in relation to its equity. These metrics show how

companies finance their operations and meet their financial obligations. Table 8 uses the debt‐

to‐equity ratio, debt ratio, and the interest coverage ratio to show the leverage comparison

between Evolution and its peer group. Companies that have a low debt‐to‐equity and debt

ratio are financed with less debt. A higher interest coverage ratio shows a company better

positioned to pay future interest payments. Evolution has a zero debt capital structure,

resulting in zero debt to equity and debt ratios. The Company’s interest coverage ratio is higher

than all of its peers because it is unlevered.

27. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

27

Table 8: Leverage Ratios Comparisons

Company Debt to Equity Ratio Debt Ratio Interest Coverage Ratio

Evolution Petroleum 0 0 98.728

Approach Resources 35.187 26.028 3.021

Denbury Resources 62.187 38.343 3.934

Royale Energy 151.192 60.189 (4.360)

Saratoga Resources 479.103 82.732 0.2796

Yuma Energy 0 0 0

Peer Average 145.53 41.46 .57

Source: Bloomberg October 16, 2014

Liquidity Risk Analysis

A company’s liquidity ratio measures how quickly it can pay off its short‐term debts with its

current assets. The higher the liquidity, the greater a company’s ability to pay off its debt. In

Table 9, we use all three ratios to compare Evolution to its peer group. Evolution's liquidity

ratios surpass its peers since it is unlevered.

Table 9: Liquidity Ratios Comparisons

Company Current Ratio Quick Ratio Cash Ratio

Evolution Petroleum 8.77 8.47 7.98

Approach Resources 1.07 0.97 0.70

Denbury Resources 0.61 0.13 0.02

Royale Energy 0.66 0.57 0.43

Saratoga Resources 2.01 1.95 1.62

Yuma Energy 4.79 3.71 3.46

Peer Average 1.83 1.47 1.24

Source: Bloomberg October 16, 2014

28. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

28

FINANCIAL PERFORMANCE AND PROJECTIONS

Evolution’s financial performance and projections are based on our team’s assumptions about

the volatile energy market and the Company’s future production from the Delhi Field. We

forecast Evolution’s 12‐month stock price to be $10.00. To arrive at this price, we accounted

for the recent significant drop in oil price in our energy forecast. We also assumed that

production from Delhi will remain consistent with typical tertiary well production and peak in

2023. Additionally, we accounted for an increase in revenues due to the reversionary working

interest activation in November, 2014. Lastly, considering the potential to commercialize its

Gas Assisted Rod Pump (GARP®) technology, we have forecasted a 20% increase in GARP®

revenues per year.

Commodity Prices

Our research team utilized publically available data from the NYMEX West Texas Intermediate

(WTI) futures contract prices as of October 13, 2014 combined with U.S. Energy Information

Administration (EIA) Short‐Term Outlook forecasts as of October 6, 2014, and the EIA Annual

Energy Outlook as of May 7, 2014 to derive long‐term prices of oil, natural gas, and natural gas

liquids (NGL). Using these 11‐year price curves, we forecast that the price of Evolution’s

Louisiana Light Sweet crude oil will rise from $88.28 to $131.78 in 2025. Additionally, we

forecasted that the spread between the WTI and Louisiana Light Sweet Crude will narrow to a

point where the difference is minimal by 2020. We expect natural gas prices to increase to

$6.45 by 2025 and NGL prices to increase to $46.86 by 2025.

Operating Activity

We predict that production from the Delhi Field will remain consistent with typical tertiary well

production. In 2023, we forecasted well production to peak at 730,000 barrels of oil (Bls) and

1,403,846 barrels of oil equivalent (boe). The reversionary working interest agreement with

Denbury came into effect in November 2014. The Company now receives 26.5% of operating

revenue from the well while incurring 23.9% of operating costs. Lastly, we forecasted revenues

from GARP® to increase 20% per year reaching $3.5 million in 2024.

Investing Activity

We believe Evolution’s management team will continue to take a conservative approach to

investing decisions. As such, we forecast Evolution’s cost of production to be $9 per boe at the

Delhi Field’s peak in 2023. Also, we predict investment activities in expanding GARP® will grow

alongside increasing revenues to $2.2 million for the year 2024.

29. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

29

Financing Activity

Management maintains a zero debt capital structure and our team is confident that this

conservative approach will persist into the future. We believe the Company will utilize internal

cash flows from the Delhi field to fund capital expenditures for the field as well as the

expansion of GARP®.

SITE VISIT

On October 24, 2014, our Burkenroad analyst team traveled to Evolution Petroleum’s

headquarters in Houston, Texas to meet with management. Randall Keys, Chief Financial

Officer, and David Joe, Controller, spoke with us about the Company’s restructuring of

operations, financial strategies, and near‐future goals. Mr. Keys emphasized that Evolution will

continue to payout a majority of its earnings from the Delhi field in the form of dividends.

Additionally, the Company intends on expanding Gas Assisted Rod Pump (GARP®) into the

leading tertiary recovery service of the oil and gas industry.

The recent drop in oil prices has slightly shifted the focus away from expanding projects to

harvesting current operations. This transition will contribute to GARP®’s potential as the

product enables efficient harvesting of fields. The slow‐to‐change oil and gas industry is

hesitant to fully integrate the technology. However, a prospective tipping point exists if a

Master Limited Partnership (MLP) implements GARP® on the majority of its wells. Evolution’s

management believes that many companies would integrate the technology after adoption by

an MLP. A large opportunity base for GARP® technology is the 15,000 domestic horizontal wells

drilled annually since 2010.

Management considers debt unnecessary and plans to maintain a conservative financial

structure. However, management does not hedge its product because of the cap hedging

places on profits. Given that Evolution Petroleum has no debt and limited capital expenditures,

we think that the Company can afford to remain unhedged in the long‐term.

Mr. Keys further explained that the Delhi Field and GARP® technology will remain Evolution’s

two core assets. Evolution’s break‐even price for oil production in the Delhi field is $25 per

barrel. The Company’s severance tax holiday for the Delhi field will exist until 2021,

contributing to the Company’s predominant source of revenue. Mr. Keys also discussed how

the recent drop in oil price may unearth potential availabilities of acquiring additional low risk

mineral interests; however, Evolution will likely not take advantage of such opportunities and

instead, continue turning free cash flows into increasing dividend yield.

31. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

31

INDEPENDENT OUTSIDE RESEARCH

In order to complement our research on Evolution Petroleum, we spoke with exploration and

production (E&P) industry experts and analysts. The general consensus on Evolution has been

positive, though there are significant concerns related to the Company’s growth potential.

They believe that the Company’s small size, lack of oil hedge activity, and zero debt capital

structure limit its ability to grow and be more profitable.

Anas Bennisse, who covers Evolution Petroleum at Sidoti & Company, believes that Evolution’s

partnership with Denbury in the Delhi Field has contributed substantial business risk to

Evolution. Mr. Bennisse mentioned that the June 2013 Delhi fluids leak and subsequent

production decline was one of Denbury’s many undesirable well events. Due to the fluids leak,

Evolution’s total revenues decreased 20% in 2014 compared to the prior year. Evolution has

had minimal control and influence in the operations of the one well which essentially accounts

for total revenues. Still, Evolution will benefit from the activation of the reversionary working

interest agreement because management will have a much more active role in well operations.

Despite management’s shift towards Gas Assisted Rod Pump (GARP®) as its primary growth

focus, Anas classifies GARP® as a functional technology that is exclusively implemented in old

and unpredictable wells. This speculative venture has yet to prove to be a viable growth

strategy, with a slow industry adoption rate, costs upwards of $140,000, and a 50% chance of

commercial well production success.

Throughout our research we consulted SEC filings, Bloomberg, Thomson One, EDGAR filings,

Seeking Alpha, Evolution’s website, peer and competitor websites, investor presentations,

conference calls, the Energy Information Administration’s website, and other analyst reports.

32. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

32

ANOTHER WAY TO LOOK AT IT

ALTMAN Z‐SCORE

In 1968, Edward Altman, a finance professor at New York University Stern, developed a

metric called the Altman Z‐Score. This formula provides a standardized measurement used

to predict the probability that a firm will go bankrupt within the next two years. The analysis

evaluates corporate credit risk based on five financial ratios: working capital/total assets,

retained earnings/total assets, earnings before interest and taxes (EBIT)/total assets, market

value of equity/book value of total liabilities, and sales/total assets. Companies which score

less than 1.81 fall in the “distress” zone and have a high risk of bankruptcy. Scores between

1.81 and 2.99 are in the “grey” zone. An Altman Z‐Score greater than 2.99 indicates a

company is currently financially sound.

Evolution’s Z‐Score of 17.73 indicates the Company has an extremely low chance of

bankruptcy. Four of Evolution's five peers fall into the distressed range, and are in danger of

going bankrupt. Evolution's comparably high Z‐Score is attributable to its zero debt

structure.

Table 10: Z‐Score Comparison

Company Ticker Altman Z‐Score

Evolution Petroleum EPM 17.73

Yuma Energy YUMA 5.82

Approach Resources AREX 1.50

Denbury Resources DNR 1.26

Saratoga Resources SARA .32

Royale Energy ROYL (2.30)

Peer Average 1.32

Source: Bloomberg November 3, 2014

34. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

34

WWBD?

What Would Ben (Graham) Do?

Ben Graham, the father of value investing, invented a form of analysis which identifies stocks

undervalued by the market. His fundamental equity analysis requires a stock to pass eight

hurdles. The first six hurdles determine whether or not the stock is underpriced, while the

remaining two focus on potential growth of the stock. To be considered an attractive

investment to Graham, the stock must pass at least four of the eight hurdles.

Evolution Petroleum passes four of Ben Graham’s eight hurdles. The company has a dividend

yield which is higher than one half the current yield on a 10‐year Treasury note, total debt

less than book value, a current ratio higher than two, and a higher than 7% growth in

earnings over the past five years. Therefore, as shown in Figure 6, Ben Graham would

consider the possibility of investing in Evolution.

Figure 7: Ben Graham Analysis

35. Evolution Petroleum Corp. (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

35

Earnings per share (ttm) 0.08$ Price: 9.14$

Earnings to Price Yield 0.88%

10 Year Treasury (2X) 4.74%

P/E ratio as of 9/30/10 (64.4)

P/E ratio as of 9/30/11 170.5

P/E ratio as of 9/30/12 55.7

P/E ratio as of 9/30/13 54.4

P/E ratio as of 9/30/14 131.1

Current P/E Ratio 113.6

Dividends per share (ttm) 0.41$ Price: 9.14$

Dividend Yield 4.46%

1/2 Yield on 10 Year Treasury 1.19%

Stock Price 9.14$

Book Value per share as of 9/30/14 1.67$

150% of book Value per share as of 9/30/14 2.51$

Interest‐bearing debt as of 9/30/14 ‐$

Book value as of 9/30/14 62,075,853$

Current assets as of 9/30/14 62,075,853$

Current liabilities as of 9/30/14 11,792,070$

Current ratio as of 9/30/14 5.3

EPS for year ended 9/30/14 0.07$

EPS for year ended 9/30/13 0.20$

EPS for year ended 9/30/12 0.14$

EPS for year ended 9/30/11 0.04$

EPS for year ended 9/30/10 (0.09)$

EPS for year ended 9/30/14 0.07$ ‐65%

EPS for year ended 9/30/13 0.20$ 43%

EPS for year ended 9/30/12 0.14$ 250%

EPS for year ended 9/30/11 0.04$ ‐144%

EPS for year ended 9/30/10 (0.09)$

Stock price data as of November 12, 2014

No

EVOLUTION PETROLEUM CORPORATION (EPM)

Ben Graham Analysis

Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury

No

Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs

No

Hurdle # 3: A Dividend Yield of 1/2 the Yield on 10 Year Treasury

Yes

Hurdle # 4: A Stock Price less than 1.5 BV

No

Hurdle # 5: Total Debt less than Book Value

Yes

Hurdle # 6: Current Ratio of Two or More

Yes

Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years

Yes

Hurdle # 8: Stability in Growth of Earnings

36. Evolution Petroleum (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

36

EVOLUTIONPETROLEUMCORPORATION(EPM)

AnnualandQuarterlyEarnings

Revenues:

Crudeoil

Artificallifttechnology

OtherProperties

Naturalgasliquids

2012A

13,729,147$

132,344

2,685,924

620,187

2013A

18,555,517$

375,063

1,755,821

253,167

2014A30‐SepA31‐DecE31‐MarE30‐JunE2015E30‐SepE31‐DecE31‐MarE30‐JunE2016E

16,699,604$3,868,602$9,350,014$12,195,671$12,331,178$37,745,465$13,352,607$13,352,607$13,062,333$13,207,470$52,975,018$

623,332115,856187,000187,000187,000676,855203,056203,056203,056203,056812,226

141,51020,36920,3695,0925,0925,0925,09220,369

115,1721,819,2811,779,7321,799,5065,398,5191,960,7691,960,7691,918,1431,939,4567,779,137

2015E2016E

Naturalgas

Totalrevenues

Operatingcosts

Artificiallifttechnology

794,436

17,962,038

124,703

410,352

21,349,920

390,238

93,8901,643,7981,608,0631,625,9314,877,7921,852,9001,852,9001,812,6191,832,7607,351,179

17,673,5084,004,82713,000,09315,770,46515,943,61548,719,00017,374,42517,374,42517,001,24517,187,83568,937,929

609,221197,360197,360197,360197,360789,440203,281203,281203,281203,281813,123

ProductioncostsDelhi

Productioncosts‐otherproperties1,650,2961,390,500

1,651,6111,862,8151,952,6925,467,1172,091,4262,080,8952,005,0532,058,5648,235,938

584,35288,02288,022

Productiontaxes51,90858,11060,460170,47864,27463,47460,70561,861250,314

Depreciation,depletionandamortization

Accretionofassetretirementobligations

RestructuringCharges

1,136,974

77,505

1,300,207

72,312

1,228,685369,350412,903465,704488,1731,736,129548,999546,235526,326540,3732,161,934

41,6264,6362,3522,1271,90211,0171,6791,4561,2351,0155,385

1,293,186

Generalandadministrativeexpenses6,143,2867,495,3098,388,2911,504,5931,515,8771,527,2471,538,7016,086,4181,550,2411,561,8681,573,5821,585,3846,271,075

Totaloperatingcosts

Income(loss)fromoperations

9,132,764

8,829,274

10,648,566

10,701,354

12,145,3612,163,9613,832,0104,113,3614,239,28814,348,6204,459,9004,457,2094,370,1824,450,47817,737,769

5,528,1471,840,8669,168,08311,657,10411,704,32734,370,37912,914,52512,917,21612,631,06212,737,35751,200,160

Interestexpense

Interestincome

Deferredloancostamortizationandbankfees

Netincome(loss)beforeincometaxes(ebt)

Incometaxbenefit(provision)

Netincome(loss)attributabletotheCompany

DividendsonPreferredStock

Netincome(loss)attributabletocommonshareholders

Netincome(loss)pershareofcommonstock:

Basic

Diluted

Averagesharesoutstanding:

Basic

Diluted

9,355

(5,577)

8,833,052

(3,700,922)

5,132,130

630,391

4,501,739$

0.17$

0.14$

27,784,298

31,609,929

(65,745)

22,580

10,658,189

(4,029,761)

6,628,428

674,302

5,954,126$

0.21$

0.19$

28,205,467

31,975,131

(69,092)(18,460)(16,500)(16,500)(16,500)(67,960)(16,500)(16,500)(16,500)(16,500)(66,000)

30,25612,7636,4103,3064,29726,7765,5306,8518,3559,83530,570

5,489,3111,835,1699,157,99311,643,91011,692,12434,329,19612,903,55512,907,56712,622,91712,730,69251,164,730

(1,891,998)(706,159)(3,461,721)(4,401,398)(4,419,623)(12,988,901)(4,877,544)(4,879,060)(4,771,463)(4,812,201)(19,340,268)

3,597,3131,129,0105,696,2727,242,5127,272,50121,340,2948,026,0118,028,5067,851,4557,918,49031,824,462

674,302168,576168,576168,576168,576674,304168,576168,576168,576168,576674,304

2,923,011$960,434$5,527,696$7,073,936$7,103,925$20,665,990$7,857,435$7,859,930$7,682,879$7,749,914$31,150,158$

0.09$0.03$0.17$0.22$0.22$0.63$0.24$0.24$0.24$0.24$0.95$

0.09$0.03$0.17$0.22$0.22$0.63$0.24$0.24$0.23$0.24$0.95$

30,895,83232,682,40132,574,05932,594,11132,614,29232,624,41432,634,59632,655,01932,675,50032,695,98032,706,220

32,564,06732,826,25032,724,05932,744,11132,764,29232,774,41432,784,59632,805,01932,825,50032,845,98032,856,220

SELECTEDCOMMON‐SIZEAMOUNTS

Productioncosts‐otherproperties

Productiontaxes

Depreciation,depletionandamortization

9.19%

0.00%

6.33%

6.51%

0.00%

6.09%

3.31%2.20%0.00%0.00%0.00%0.18%0.00%0.00%0.00%0.00%0.00%

0.00%0.00%0.40%0.37%0.38%0.35%0.37%0.37%0.36%0.36%0.36%

6.95%9.22%3.18%2.95%3.06%3.56%3.16%3.14%3.10%3.14%3.14%

Generalandadministrativeexpenses34.20%35.11%47.46%37.57%11.66%9.68%9.65%12.49%8.92%8.99%9.26%9.22%9.10%

Income(loss)fromoperations49.16%50.12%31.28%45.97%70.52%73.92%73.41%70.55%74.33%74.35%74.29%74.11%74.27%

Netincome(loss)beforeincometaxes(ebt)49.18%49.92%31.06%45.82%70.45%73.83%73.33%70.46%74.27%74.29%74.25%74.07%74.22%

Netincome(loss)attributabletocommonshareholders

YEARTOYEARCHANGE

Totalrevenues

Productioncosts‐otherproperties

Productiontaxes

Depreciation,depletionandamortization

Accretionofassetretirementobligations

Generalandadministrativeexpenses

Totaloperatingcosts

Income(loss)fromoperations

25.06%

467.47%

373.86%

n/a

456.96%

366.93%

351.96%

367.18%

629.45%

27.89%

18.86%

‐15.74%

n/a

14.36%

‐6.70%

22.01%

16.60%

21.20%

16.54%23.98%42.52%44.86%44.56%42.42%45.22%45.24%45.19%45.09%45.19%

‐17.22%‐13.57%195.98%263.63%269.88%175.66%333.84%33.65%7.80%7.80%41.50%

‐57.98%‐78.52%n/an/an/a‐84.94%n/an/an/an/an/a

n/an/a298.31%600.88%‐303.39%n/an/a22.28%4.47%2.32%46.83%

‐5.50%19.27%26.21%49.35%74.33%41.30%48.64%32.29%13.02%10.69%24.53%

‐42.44%‐64.14%‐81.06%‐77.92%‐71.39%‐73.53%‐63.79%‐38.07%‐41.92%‐46.65%‐51.12%

11.91%‐22.00%‐42.63%‐33.72%1.71%‐27.44%3.03%3.03%3.03%3.03%3.03%

14.06%‐18.95%‐15.79%38.06%117.88%18.14%106.10%16.32%6.24%4.98%23.62%

‐48.34%‐6.26%‐5899.10%758.70%394.94%521.73%601.55%40.89%8.36%8.83%48.97%

Other:

Production‐oil(bbls)Delhiroyalty

Production‐oil(bbls)includingDelhiroyalty

Production‐NGLs(bbls)

Production‐gas(mcf)

ProductioninequivalentunitsincludingDelhiroyaltyproduction(BOE)

Dailyproductionrate(BOE/d)

136,075

151,081

12,611

266,777

208,155

570.29

180,658

196,379

7,272

139,006

226,819

621.42

164,22437,687103,560135,646140,069408,531144,631144,519140,863142,381571,026

169,74538,543105,913138,729143,253417,816147,919147,804144,065145,617584,004

3,46059,96358,73758,788173,25262,96662,92660,95161,609247,114

26,105420,409400,016436,6651,228,663487,605466,725425,498443,7671,750,281

177,55638,543235,944264,135274,818795,844292,152288,517275,932281,1871,122,831

486.45418.952,564.612,934.843,019.982,180.403,175.573,136.063,032.223,089.973,076.25

Oil%ofproduction

NGL%ofproduction

Gas%ofproduction

72.58%

6.06%

21.36%

44.89%52.52%52.13%52.50%50.63%51.23%52.21%51.79%52.01%

25.41%22.24%21.39%21.77%21.55%21.81%22.09%21.91%22.01%

29.70%25.24%26.48%25.73%27.82%26.96%25.70%26.30%25.98%

OperatingcostperBOEincludingDelhiproduction

OperatingcostperBOEexcludingDelhiproduction22.90$30.12$

7.00$7.05$7.11$7.11$7.16$7.21$7.27$7.32$7.32$

43.83$102.77$0.23$

Depreciation,depletionandamortizationrate7.10$10.83$13.83$14.52$1.75$1.76$1.78$1.87$1.88$1.89$1.91$1.92$2.02$

Burkenroadoilpriceforecast

Burkenroadgaspriceforecast

Naturalgasliquidspriceforecast

100.37$88.28$87.91$86.08$90.34$90.27$90.34$90.67$90.70$90.71$

3.60$3.91$4.02$3.72$3.97$3.80$3.97$4.26$4.13$4.20$

32.00$30.34$30.30$30.61$31.16$31.14$31.16$31.47$31.48$31.48$

37. Evolution Petroleum (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

37

EVOLUTIONPETROLEUMCORPORATION(EPM)

AnnualandQuarterlyBalanceSheets

Currentassets

Cashandcashequivalents

Certificatesofdeposit

30‐Jun‐12A

14,428,548$

250,000

30‐Jun‐13A

24,928,585$

250,000

30‐Jun‐14A30‐SepA31‐DecE31‐MarE30‐JunE30‐Jun‐15E30‐SepE31‐DecE31‐MarE30‐JunE30‐Jun‐16E

23,940,514$21,368,144$11,019,199$14,323,126$18,432,397$18,432,397$22,835,600$27,849,402$32,782,611$37,563,761$37,563,761$

2015E2016E

Oilandnaturalgassalesreceivable

Jointinterestpartnerreceivable

1,343,347

96,151

1,632,853

49,063

1,456,1461,268,1224,513,3015,415,5915,475,0515,475,0516,098,9796,031,9575,838,2425,902,3175,902,317

Incometaxreceivable92,885281,970

Otherreceivables1909181,06623,52423,52423,52423,52423,52423,52423,52423,52423,52423,524

Deferredtaxasset

Prepaidexpensesandothercurrentassets

Totalcurrentassets

Oilandnaturalgasproperties,net

Otherpropertyandequipment,net

Totalpropertyandequipment,net

Advancestojointinterestoperatingpartner

325,235

233,433

16,769,789

40,476,172

92,271

40,568,443

1,366,921

26,133

266,554

27,436,076

38,789,032

52,217

38,841,249

26,059

159,624159,624156,033152,442148,851148,851145,260141,669138,078134,488134,488

747,453632,706637,451642,232647,049647,049651,902656,791661,717666,680666,680

26,304,80323,452,12016,349,50820,556,91524,726,87224,726,87229,755,26534,703,34339,444,17244,290,76944,290,769

37,822,07037,651,45037,241,36036,778,46936,293,10836,293,10835,746,92135,203,49934,679,98534,142,42434,142,424

424,827444,942444,942444,942444,942444,942444,942444,942444,942444,942444,942

38,246,89738,096,39237,686,30237,223,41136,738,05036,738,05036,191,86335,648,44135,124,92734,587,36634,587,366

Otherassets

Totalassets

Currentliabilities

Accountspayable

JointInterestadvances

Accruedpayroll

Royaltiespayable

250,333

58,955,486$

407,570$

3,217,975

1,005,624

294,013

252,912

66,556,296$

642,018$

127,081

1,385,494

91,427

464,052527,341527,341527,341527,341527,341527,341527,341527,341527,341527,341

65,015,752$62,075,853$54,563,151$58,307,667$61,992,263$61,992,263$66,474,470$70,879,125$75,096,440$79,405,477$79,405,477$

441,722$611,547$811,188$811,347$818,399$818,399$844,604$840,915$836,344$842,964$842,964$

874,013363,811366,539369,288369,288372,058374,848377,660380,492380,492

444,933539,750545,676545,676594,646594,646581,874588,260588,260

Statetaxespayable91,967233,54844,17344,17344,17344,17344,17344,17344,17344,17344,17344,173

Othercurrentliabilities

Totalcurrentliabilities

Deferredincometaxes

71,768

5,088,917

6,205,093

153,182

2,632,750

8,418,969

2,558,004

2,999,7261,529,7331,664,1041,761,8091,777,5371,777,5371,855,4811,854,5821,840,0511,855,8891,855,889

9,897,27210,021,8759,912,7199,789,5099,660,3189,660,3189,514,9379,370,2929,230,9459,087,8609,087,860

Assetretirementobligations968,677615,551205,512209,028189,035169,094149,221149,221129,451109,78690,21370,74270,742

Deferredrent

Totalliabilities

Stockholders'equity:

70,011

12,332,698

52,865

11,720,135

35,72031,43440,00040,00040,00040,00040,00040,00040,00040,00040,000

13,138,23011,792,07011,805,85811,760,41311,627,07611,627,07611,539,87011,374,65911,201,20911,054,49211,054,492

Commonstock,parvalue$0.001

Preferredstockparvalue$0.001

Additionalpaid‐incapital

Retainedearnings(deficit)

28,670

317

29,416,914

18,058,909

29,410

317

31,813,239

24,013,035

32,61532,79732,58432,60432,62432,62432,64532,66532,68632,70632,706

317317317317317317317317317317317

34,632,37735,357,36235,333,01235,308,42935,283,84635,283,84635,259,26335,234,68035,210,09735,185,51435,185,514

17,212,21314,893,3077,391,37911,205,90415,048,40015,048,40019,642,37524,236,80328,652,13233,132,44833,132,448

Treasurystock

Totalstockholders'equity

Totalliabilitiesandstockholders'equity

(882,022)

46,622,788

58,955,486$

(1,019,840)

54,836,161

66,556,296$

51,877,52250,283,78342,757,29246,547,25450,365,18750,365,18754,934,60059,504,46663,895,23268,350,98568,350,985

65,015,752$62,075,853$54,563,151$58,307,667$61,992,263$61,992,263$66,474,470$70,879,125$75,096,440$79,405,477$79,405,477$

SELECTEDCOMMONSIZEBALANCESHEETAMOUNTS(%ofrevenues)

Receivables

Oilandnaturalgassalesreceivable7.48%7.65%8.24%135.23%34.72%34.34%34.34%11.24%35.10%34.72%34.34%34.34%8.56%

Prepaidexpensesandothercurrentassets1.30%1.25%4.23%15.80%4.90%4.07%4.06%1.33%3.75%3.78%3.89%3.88%0.97%

Oilandnaturalgasproperties,net225.34%181.68%214.00%940.15%286.47%233.21%227.63%74.49%205.74%202.62%203.98%198.64%49.53%

Accountspayable

Accruedpayroll

Royaltiespayable

2.27%

5.60%

1.64%

3.01%

6.49%

0.43%

2.50%15.27%6.24%5.14%5.13%1.68%4.86%4.84%4.92%4.90%1.22%

0.00%21.82%2.80%2.32%2.32%0.76%2.14%2.16%2.22%2.21%0.55%

0.00%0.00%3.42%3.42%3.42%1.12%3.42%3.42%3.42%3.42%0.85%

Assetretirementobligations5.39%2.88%1.16%5.22%1.45%1.07%0.94%0.31%0.75%0.63%0.53%0.41%0.10%

Deferredrent0.39%0.25%0.20%0.78%0.31%0.25%0.25%0.08%0.23%0.23%0.24%0.23%0.06%

SELECTEDCOMMONSIZEBALANCESHEETAMOUNTS(%oftotalassets)

Totalcurrentassets28.44%41.22%40.46%37.78%29.96%35.26%39.89%39.89%44.76%48.96%52.52%55.78%55.78%

Totalpropertyandequipment,net

Otherassets

68.81%

0.42%

58.36%

0.38%

58.83%61.37%69.07%63.84%59.26%59.26%54.44%50.29%46.77%43.56%43.56%

0.71%0.85%0.97%0.90%0.85%0.85%0.79%0.74%0.70%0.66%0.66%

Totalcurrentliabilities

Deferredincometaxes

Assetretirementobligations

8.63%

10.53%

1.64%

3.96%

12.65%

0.92%

4.61%2.46%3.05%3.02%2.87%2.87%2.79%2.62%2.45%2.34%2.34%

15.22%16.14%18.17%16.79%15.58%15.58%14.31%13.22%12.29%11.44%11.44%

0.32%0.34%0.35%0.29%0.24%0.24%0.19%0.15%0.12%0.09%0.09%

Deferredrent

Totalstockholders'equity

0.12%

79.08%

0.08%

82.39%

0.05%0.05%0.07%0.07%0.06%0.06%0.06%0.06%0.05%0.05%0.05%

79.79%81.00%78.36%79.83%81.24%81.24%82.64%83.95%85.08%86.08%86.08%

38. Evolution Petroleum (EPM) BURKENROAD REPORTS (www.burkenroad.org) November 12, 2014

38

EVOLUTIONPETROLEUMCORPORATION(EPM)

AnnualandQuarterlyStatementsofCashFlows

Inthousands

Cashflowsfromoperatingactivities:

Netincome(loss)

Adjustments:

2012A

5,132,130$

2013A

6,628,428$

2014A30‐SepA31‐DecE31‐MarE30‐JunE2015E30‐SepE31‐DecE31‐MarE30‐JunE2016E

3,597,313$1,129,010$5,696,272$7,242,512$7,272,501$21,340,294$8,026,011$8,028,506$7,851,455$7,918,490$31,824,462$

2016E2015E

Depreciation,depletionandamortization

Stock‐basedcompensation

Stock‐basedcompensationrelatedtorestructuring

1,150,454

1,475,995

1,341,055

1,531,745

1,272,778381,509412,903465,704488,1731,748,288548,999546,235526,326540,3732,161,934

1,352,322243,337350,000350,000350,0001,293,337350,000350,000350,000350,0001,400,000

376,365

Accretionofassetretirementobligations77,50572,31241,6264,6362,3522,1271,90211,0171,6791,4561,2351,0155,385

Settlementofassetretirementobligations(61,936)(90,531)(315,952)(226,008)(22,345)(22,067)(21,776)(292,196)(21,448)(21,122)(20,808)(20,485)(83,864)

Deferredrent

Deferredincometaxes

(15,401)

2,549,592

(17,146)

2,512,978

(17,145)(4,286)8,5664,280

1,344,812124,603(105,565)(119,619)(125,600)(226,181)(141,790)(141,055)(135,755)(139,494)(558,095)

Changesinassetsandliabilities:

Receivablesfromoilandnaturalgassales

Receivablesfromincometaxesandother

Duefromjointinterest

216,057

(64,194)

139,705

(289,506)

(189,813)

(9,947)

176,707188,024(3,245,179)(902,291)(59,460)(4,018,905)(623,928)67,022193,715(64,075)(427,266)

281,822(22,458)(22,458)

49,063

Prepaidexpensesandothercurrentassets

Accountspayableandaccruedexpenses

Royaltiespayable

(165,581)

379,873

(448,638)

(33,121)

538,057

(202,586)

(480,899)114,747(4,745)(4,781)(4,817)100,404(4,853)(4,889)(4,926)(4,963)(19,631)

663,645(1,345,875)(310,562)2,8889,801(1,643,747)28,974(899)(1,759)9,45235,769

444,93394,8175,926545,67648,970(12,772)6,38642,584

Incometaxespayable

Netcashprovidedby(usedin)operatingactivities

Cashflowfrominvestingactivities:

NetproceedsfromthesaleoftheTullosAssets

Developmentofoilandnaturalgasproperties

Acquisitionsofoilandnaturalgasproperties

Proceedsfromotherassetsales

Capitalexpendituresforotherequipment

Advancestojointventureoperatingpartner

9,845

10,375,406

799,610