Recommended

Recommended

More Related Content

Similar to TISI Burkenroad Report

Similar to TISI Burkenroad Report (20)

TISI Burkenroad Report

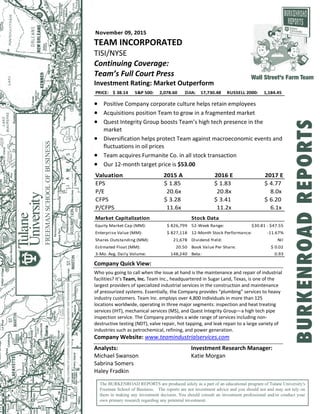

- 1. November 09, 2015 TEAM INCORPORATED TISI/NYSE Continuing Coverage: Team’s Full Court Press Investment Rating: Market Outperform PRICE: $ 38.14 S&P 500: 2,078.60 DJIA: 17,730.48 RUSSELL 2000: 1,184.45 Positive Company corporate culture helps retain employees Acquisitions position Team to grow in a fragmented market Quest Integrity Group boosts Team’s high tech presence in the market Diversification helps protect Team against macroeconomic events and fluctuations in oil prices Team acquires Furmanite Co. in all stock transaction Our 12‐month target price is $53.00 Valuation 2015 A 2016 E 2017 E EPS $ 1.85 $ 1.83 $ 4.77 P/E 20.6x 20.8x 8.0x CFPS $ 3.28 $ 3.41 $ 6.20 P/CFPS 11.6x 11.2x 6.1x Market Capitalization Stock Data Equity Market Cap (MM): $ 826,799 52‐Week Range: $30.81 ‐ $47.55 Enterprise Value (MM): $ 827,118 12‐Month Stock Performance: ‐11.67% Shares Outstanding (MM): 21,678 Dividend Yield: Nil Estimated Float (MM): 20.50 Book Value Per Share: $ 0.02 3‐Mo. Avg. Daily Volume: 148,240 Beta: 0.93 Company Quick View: Who you going to call when the issue at hand is the maintenance and repair of industrial facilities? It’s Team, Inc. Team Inc., headquartered in Sugar Land, Texas, is one of the largest providers of specialized industrial services in the construction and maintenance of pressurized systems. Essentially, the Company provides “plumbing” services to heavy industry customers. Team Inc. employs over 4,800 individuals in more than 125 locations worldwide, operating in three major segments: inspection and heat treating services (IHT), mechanical services (MS), and Quest Integrity Group—a high tech pipe inspection service. The Company provides a wide range of services including non‐ destructive testing (NDT), valve repair, hot tapping, and leak repair to a large variety of industries such as petrochemical, refining, and power generation. Company Website: www.teamindustrialservices.com Analysts: Investment Research Manager: Michael Swanson Katie Morgan Sabrina Somers Haley Fradkin The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment. Wall Street's Farm Team BURKENROADREPORTS

- 3. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 3 Table 1: Historical Burkenroad Ratings and Prices Report Date Stock Price* Rating 12‐Month Target Price 11/14/2014 $42.93 Market Underperform $42.00 10/29/2013 $38.29 Market Perform $39.00 11/19/2012 $32.31 Market Perform $44.00 11/23/11 $24.51 Market Outperform $31.00 10/22/10 $18.51 Market Perform $21.31 11/10/09 $16.35 Market Perform $18.51 11/18/08 $22.40 Market Outperform $33.21 12/05/07 $30.28 Market Outperform $42.20 10/30/06 $15.40 Market Outperform $30.80 01/14/05 $7.86 Market Perform $15.72 04/13/04 $6.99 Market Outperform $13.98 11/22/02 $3.75 Buy $7.50 *Price at time of report date INVESTMENT THESIS We established a target price of $53.00 and market rating of Market Outperform for Team Inc. We believe that Team is positioned to have future revenue growth through both organic growth and strategic acquisitions. Furthermore, the development of the Quest Integrity Group technology will differentiate Team Inc. in the industrial services industry. These advances, combined with a positive and effective Company culture, help the Company to retain employees and to produce quality work. These competitive advantages support our positive outlook on future earnings for Team Inc. Positive corporate culture helps retain employees Team operates in a highly fragmented industry with many companies offering similar types of services. The suppliers for the Company’s operations are the skilled laborers. These laborers are in high demand in the industrial services industry and will often switch companies for a higher pay grade. Team looks to retain its valuable employees by creating a positive company culture, providing competitive pay, and maintaining notably safe working conditions. One measure the Company uses to promote this culture is the low reported accident rate. In fact, the safety of workers in the field is one of Team’s core values. This emphasis on safety helps the Company to retain employees and create a safe positive company culture.

- 8. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 8 Key Metrics Team services its clients through three business segments: the Inspection and heat treating group, mechanical services group, and Quest Integrity Group. In the large industrial services industry, Team is a sizeable and more comprehensive player relative to the other firms. For example, in the non‐destructive testing (NDT) market, Team has a 10.6% market share, second only to Mistras Group, which has a 16.5% share. Because demand in this market is growing as petrochemical production remains high and industrial output increases, so is the demand for Team’s services. Furthermore, demand is projected to grow as production increases. Team also operates in the highly fragmented valve installation and manufacturing market. The demand for, and domestic production of valves is increasing as measured by the Industrial Production Index. With the expansion of industrial output, expected demand for valves is increasing. Due to the high market fragmentation, however, no one company, including Team Inc., accounts for more than 2.1% of total production. Still, Team’s variety of products and services allows the Company to brand itself as a one‐stop shop for all industrial service needs. The increase in the Industrial Production and Capacity Utilization Index for the oil industry suggests that strong oil production levels will drive Team Inc.’s main business segments. Figure 4 illustrates Team’s market share range within its various service segments. Figure 4: Team Inc. Range of Market Share by Segment Before Furmanite Merger Source: Team Inc. Investor Presentation 2015 Threat of Entry The industrial services industry has moderately high barriers to entry. The industry’s large number of suppliers, coupled with the need for highly skilled labor and specialized technology, are formidable barriers to entry. With such a large and saturated market, little opportunity exists for a new company to enter and undermine the status quo. The firms currently operating in this space offer a wide variety of services in all areas of the market. Inspection & Assessment Turnaround Services On‐Stream Services Team Inc. 12‐25% Team Inc. 10‐12% Team Inc. 10‐15%

- 14. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 14 For the past three fiscal years, no single customer has accounted for more than 10% of consolidated revenues. The diverse customer base allows for many streams of recurring revenue from all business segments. Although mergers and acquisitions (M&As) are not essential to Team’s growth profile, revenue from acquisitions has accounted for 34% of the Company’s total sales growth over the past ten years. Furthermore, the industry’s highly fragmented nature makes M&A an attractive option for growth by Team, allowing it to grow both organically and through acquisitions, ultimately strengthening its market share. Thus, with an average of nearly one acquisition a year, Team is beginning to consolidate an extremely vast industry. Financial Performance Fiscal year 2015 produced a record year for Team with strong earnings. Adjusted earnings rose 35% from $31.5 million in 2014 to $43.3 million in 2015. Additionally, revenues rose 12% to $842 million from $749.5 million in 2014. Although the Company is looking forward to another record year in 2016, the current rise in the U.S. dollar against other currencies may affect the Company’s overseas operations and disturb Team’s 2016 profitability. Latest Developments November 2, 2015‐ Team announces the acquisition of Furmanite Co., one of Team’s largest competitors. A stock‐for‐stock purchase agreement valued at $335 million will take effect in the first calendar quarter of 2016. August 10, 2015‐ Team’s Board of Directors welcomed Michael Lucas, President and CEO of Powell Industries. He is replacing Jack Johnson, who will retire from his seat on the Board at the end of this term. July 6, 2015‐ Team Inc. announced the acquisition of Qualspec Group through a stock purchase agreement. Qualspec was one of Team’s competitors in the non‐destructive testing (NDT) inspection market. January 13, 2015‐ After a strong 2015 fiscal year, Team relaunched its stock repurchase program. Recent Projects Inspection ‐ Team was selected to carry out the Turkey Point & St. Lucie Nuclear power plant capacity uprating project. Using gamma ray technology, the Company measured thickness of walls and looked for imperfections. Team completed the project with no injuries or accidents. Concrete Repair ‐ Con‐Agra selected Team to restore its 4,000 square foot concrete floor complete with non‐slip protection. Valve Insertion ‐ The MetLife stadium, in New Jersey selected Team’s 8” InsertValveTM as a solution for isolating its hot water supply without a loss in pressure. Hot Tap/Line Stop ‐ A repeat customer hired Team to replace a portion of pipeline while it remained in operation. Through a bypass and Team’s Sealtite II line stop fittings, Team was able to complete one of the longest replacements of an operational pipeline.

- 15. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 15 PEER ANALYSIS Due to the large and diverse state of the industrial services industry, many firms compare to Team, but few are identical in size and services. Team is one of the larger firms in the industry and offers a more comprehensive list of services than most of its peers. While there are many firms in the industry that focus on one area of industrial services, Team, along with Furmanite Co. and Mistras Group, are the only identified “all inclusive” firms. Therefore, we chose a peer group of Furmanite Co., Mistras Group, and Exponent Inc. to analyze Team’s position relative to competitors, as seen in Table 2. Table 2: Peer Comparison Company Ticker Revenue EPS Market Cap (Mil) Debt/ EBITDA D/E P/E (ttm) Team TISI $842.0 $1.95 $810.42 0.86 23.40 18.15 Furmanite* FRM $529.20 $0.30 $295.13 1.93 45.13 27.57 Mistras MG $711.25 $0.56 $531.30 2.09 54.21 26.92 Exponent EXPO $304.70 $1.51 $1040.00 0.00 0.00 32.39 *Furmanite Co. pending acquisition by Team Inc. Source: Bloomberg October 2, 2015 (Year Ending) Furmanite Corporation (FRM/NYSE) Furmanite Corporation offers its customers a wide range of technical and industrial services. It operates in two segments: technical services and engineering & project solutions. Furmanite is based in Houston, Texas and has over 40 locations worldwide. Like Team, Furmanite can provide services to a variety of industries because of its long list of offerings including: on‐site and on‐line plant and pipeline maintenance, industrial plant turnaround maintenance, leak sealing, hot tapping, line stopping, bolting, field heat treating, valve testing, valve repair, and more. The company primarily services petroleum refineries, offshore drilling rigs, chemical plants, and electric power generating plants. Furmanite maintains contracts for continuous service provision around the world. It has operations in the Americas, Europe, the Middle East, Africa, and the Asia‐ Pacific. In terms of revenues, Team has outperformed Furmanite in the last three fiscal years by about $300 million. Mistras Group (MG/NYSE) Mistras Group (MG) is Team’s closest competitor in the non‐destructive services industry, which includes companies that primarily perform non‐destructive tests and inspections on industrial assets. With 16.5% market share, Mistras is the only company to maintain a larger share of the NDT market than Team. Mistras is also Team’s closest competitor in terms of product and service offerings. Like Team, the company operates in three major segments: services, products and systems, and international operations. The two companies also share a similar customer base, consisting of clients in the oil and gas market, power generation and transmission, and industrial processing.

- 16. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 16 Mistras Group provides services such as traditional NDT, advanced NDT, destructive testing, and mechanical integrity services to a range of industries including public infrastructure, aerospace and defense, oil and gas, transportation, fossil and nuclear power, and pharmaceuticals. The company has over 100 locations worldwide. Exponent Inc. (EXPO/NASDAQ) Exponent Inc., headquartered in Menlo Park, California, is an engineering consulting firm that provides an in‐depth analysis of complex problems in a variety of fields, such as medical/health advancements, and structural damage response. The company does not do any physical repairs or construction. Instead, it focuses on the engineering and science aspects of a given problem. Therefore, overlap exists between Team’s services and Exponent’s services, but the two companies are not identical. For example, Team focuses more heavily on the physical construction than Exponent does. Like Team, Exponent Inc. has a majority of its offices in the U.S., but it also has several international offices—in Switzerland, Germany, China, and the U.K. Exponent has an employee base of 900, nearly one‐quarter the size of Team’s workforce. MANAGEMENT PERFORMANCE AND BACKGROUND Team Inc.’s rapid growth and expansion is a product of the Company’s experienced corporate team and operational strategy. Its management techniques are effective, which is evident in the near $800 million increase in revenues over the past ten fiscal years. Return on Invested Capital The return on invested capital (ROIC) ratio measures how well the Company is utilizing its capital to generate returns. Table 3 measures Team’s ROIC in comparison to its peers and major competitors. Team’s ROIC took a downward turn from 2013‐2014 due to the increase in engineering and development costs attributed to the Quest Integrity Group’s demand for high tech tools. These tools require a high amount of capital both for current maintenance and for future development. Table 3: Return on Invested Capital Company 5/1/2015 5/1/2014 5/1/2013 5/1/2012 5/1/2011 Team 10.28% 8.61% 9.43% 10.83% 10.53% Mistras Group 4.99% 7.44% 4.77% 10.09% 9.94% Furmanite Corp 6.14% 9.10% 1.39% 17.55% 8.61% Exponent 15.75% 14.80% 17.02% 17.01% 15.04% Source: Bloomberg October 8, 2015

- 17. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 17 Ted W. Owen Chief Executive Officer, President and Director (63) Ted Owen joined Team Inc. in February 1998. In July 2014, Mr. Owen was promoted to President of the Company from his former position, Executive Vice President and Chief Financial Officer. He has also held both Secretary and Treasurer roles in the Company. The wide range of job opportunities has granted him extensive experience as a leader at Team. Greg L. Boane Chief Financial Officer, Senior Vice President and Treasurer (51) Greg Boane has served as Chief Financial Officer and Treasurer at Team since November 2014. Mr. Boane previously served as Vice President of Finance at Cameron International Corporation, and as Accounting Vice President at Grant Prideco. Peter W. Wallace President of Mechanical Services (52) Peter Wallace has been a Team Inc. employee for 28 years. Mr. Wallace was the leader of Team’s Field Service Operations and in 2010, before his promotion to Executive Vice President and Chief Operating Officer. He also worked as the Senior Vice President of Commercial Support and Business Development. Arthur F. Victorson President of Inspection and Heat Treating Services (53) In 2004, Arthur Victorson joined the Company as the Vice President of the Heat Treating and Inspection Service division and has since been promoted to President of those segments. Jeffrey L. Ott President of Quest Integrity Group (52) Jeffery Ott was a Private Equity Manager at Deutsche Bank before transitioning to Team in January 2007 during the acquisition of Quest Integrity Group. Mr. Ott has served as the President of the branch since 2010. He has also served as Team’s Executive Officer since 2013. Andre C. Bouchard Senior Vice President of Administration, General Counsel, and Secretary (50) Andre Bouchard joined Team in 2008 and since then has held several positions including the Senior Vice President of Administration, General Counsel, and Secretary. Prior to joining Team, Mr. Bouchard worked for the Southern Union Company for 14 years.

- 18. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 18 Board of Directors Team’s Board of Directors has seven members who either serve a three‐year term or sit on the Board until a new member is elected. These Board Members may be reelected with no term limits. Each member has a significant background in relevant industries such as law, real estate, or finance. The members include: Phillip Hawk, Ted Owen, Sidney Williams, Vincent Foster, Louis Waters, Emmett J. Lescroart, Michael Lucas, and Jack Johnson Jr. Table 4 shows the distribution of stock options to top management and the Board of Directors at Team. Table 4: Board of Directors Name Total Annual Compensation ($) Stock Awards ($) Total ($) Total Options Outstanding Phillip Hawk 463,328 625,024 1,289,605 120,000 Ted Owen 352,312 232,014 639,708 73,000 Sidney Williams 55,000 70,000 125,000 30,000 Vincent Foster 60,000 70,000 130,000 35,000 Louis Waters 50,000 70,000 120,000 30,000 Emmett Lescroart 45,000 70,000 115,000 30,000 Michael Lucas 40,000 70,000 110,000 30,000 Jack Johnson, Jr. 57,500 70,000 127,500 30,000 Source: Bloomberg October 7, 2015 SHAREHOLDER ANALYSIS As of October 7, 2015, Team Inc. has approximately 20,910,719 shares of common stock outstanding. Insiders hold 5.44% of those shares and institutional investors hold 84.90%. The Company has approximately 19,260,000 shares float and no preferred stock issued. The top nine investors in the Company are institutional investors. The tenth largest holder is Neuberger Berman Genesis, a mutual fund. Seven of the top ten institutional investors have increased shares in Team since 2014 (see Table 5). Most notably, the largest holder, Government Pension Fund of Norway, increased its stake by 115.45%. These increased positions suggest that the institutional investors have a bullish projection for the Team stock, as these funds aim to hold companies with sustainable growth potential.

- 19. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 19 Table 5: Institutional Holders of Team Inc. Stock Institution Shares Held Percent Ownership Percent Change From 2014‐2015 Value (In USD) Government Pension Fund of Norway 4,659,268 22.92% 115.45% 155,153,624.40 EdgePoint Investment Group, Inc. 1,607,194 7.73% 5.96% 53,519,560.20 Vanguard Group, Inc. 1,296,182 6.23% 2.83% 43,162,860.60 Ariel Investments, LLC 1,135,129 5.46% (1.11%) 37,799,795.70 EdgePoint Investment Management Inc. 986,236 4.77% 0% 32,841,658.80 Neuberger Berman LLC 941,768 4.53% (0.86%) 31,360,874.40 Pyramis Global Advisors, LLC 896,015 4.31% 27.94% 29,837,299.50 T. Rowe Price Associates, Inc. 759,056 3.65% 1.17% 25,276,564.80 Dimensional Fund Advisors, Inc. 751,875 3.62% 4.71% 25,037,437.50 Mackenzie Investments 681,540 3.28% 1.75% 22,695,282.00 Source: Morningstar October 2, 2015 Team’s insider owners control 3.95% of the stock. The change from 2014 is a 300.7% increase with most of that change attributed to Jeffrey Ott’s recent 812.25% increase in shares. The percent change resulting from these trades represents a slight increase of 0.68% in insider ownership (see Table 6). Table 6: Insider Ownership of Team Inc. Stock Name Position Shares Held % Shares Outstanding Market Value (In USD) Jeffrey Ott President, Quest Integrity Group 300,030 1.43% 10,609,060 Louis Waters Lead Independent Director 179,101 0.86% 6,333,011 Sidney Williams Independent Director 112,423 0.54% 3,975,277 Ted Owen CEO, President and Director 49,640 0.24% 1,755,270 Emmett Lescroart Independent Director 47,888 0.23% 1,693,319 Vincent Foster Independent Director 43,793 0.21% 1,548,520 Philip Hawk Executive Chairman of the Board 30,155 0.14% 1,066,280 Peter Wallace President, Mechanical Services 20,973 0.1% 741,605 Arthur Victorson President, Inspection and Heat Treating 20,420 0.1% 722,051 Andre Bouchard Executive VP, Administration, Chief Legal Officer, and Secretary 17,607 0.08% 622,583 Source: Morningstar October 7, 2015

- 21. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 21 Regulatory Risks Environmental Regulations The increase in environmental requirements is both an opportunity and a risk for Team. The Company enjoys a boost in demand due to the increased demand for testing and ensuring plants are meeting codes. However, the regulations can also stifle production in the facilities that Team services, reducing demand for Team’s services. Additionally, Team must adhere to certain regulations. The environmentally questionable nature of the industries the Company serves means Team is subject to those industries’ regulations. For example, the U.S. government and the Environmental Protection Agency highly regulate the petrochemical industry, where Team conducts a large portion of its business. Team must comply with the regulations imposed on this industry when completing jobs. More regulations mean more safety/operating protocols and likely longer job times and higher prices. The uncertainty of the future expansion of environmental regulations at the upcoming global environmental summit (COP21) is also a concern for Team. These summits will likely bring more regulation to U.S. and to international businesses. The affect these new regulations will have on Team remains uncertain, but there is potential they could negatively affect demand for Team’s services. Financial Risks Liquidity and Leverage Risk Team’s fiscal year 2015 current ratio is 3.165. This figure means that the Company’s assets outnumber its liabilities by just over 3 to 1. This is considered a good current ratio and suggests the firm is sufficiently capable, for now, of repaying its liabilities with its assets. Although this ratio is the lowest Team has reported since February 2009, the ratio is still in Team’s average five year range. Compared to historical ratios and competitors, Team’s current ratio and debt‐to‐ equity ratios are equal to or better than the ratios of its competitors (as seen in Table 7). Table 7: Key Liquidity Ratios of Market Leaders Ratio Team Furmanite Co. Mistras Group Current 3.165 3.72 1.83 Debt‐to‐Equity 23.40% 47.21% 54.21% Source: Morningstar October 9, 2015 The Company also has a relatively low debt‐to‐equity ratio at 23.40%. This means that the Company finances most of its projects through either cash or equity. The only nominal increase in shares outstanding suggests that Team does most of its financing with cash. The relatively low debt amount allows Team to operate without a large and immediate obligation to debt holders and the fear of bankruptcy upon a default.

- 24. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 24 ANOTHER WAY TO LOOK AT IT ALTMAN Z‐SCORE Edward Altman, a finance professor at New York University, created the Altman Z‐Score in 1967. The score tests the firm for bankruptcy risk. The measure aims to identify the firm’s credit‐riskiness through the analysis of five ratios— working capital/total assets, retained earnings/total assets, EBIT/total assets, market capitalization/book value of total liabilities, and sales/total assets. These ratios are then weighted using Altman’s multipliers of 1.2, 1.4, 3.3, 0.6, and 1.0, respectively. Summing all these weighted ratios derives the final Altman Z‐ Score of a firm. A score of 1.8 or under means the firm is in high risk of default. A score of 3 or above suggests the firm’s credit is safe and the firm is unlikely to enter bankruptcy. Altman describes a score between 1.8 and 2.99 as the “grey area,” and says these firms show an uncertain probability of bankruptcy. Team Inc. has routinely posted a high and healthy Z‐Score. The Company’s Z‐Score for 2015 is 5.52—well above the requisite score of 3 for investors to consider a firm safe from bankruptcy. However, the Z‐Score shows a slight dip from 2014 after four years of increasing Z‐Scores (see Table 8). The dip does not indicate that the firm is approaching the uncertain range, or bankruptcy. An unfavorable macroeconomic environment is one explanation for the dip. The dip comes from a decrease in the market capitalization to BV of total equity ratio. So alternatively, the slight decrease in the Z‐score may mean that the market is slightly less confident in the Company’s financial plan. A decrease in confidence likely comes from the recent acquisition of Qualspec, the announcement of the acquisition of Furmanite, and speculation regarding future acquisitions. Table 8: Altman Z‐Scores 2011‐2015 Source: Bloomberg November 9, 2015 Ratio 2011 2012 2013 2014 2015 Multiplier Working Capital to Total Assets 0.367 0.389 0.378 0.358 0.377 1.2 Retained Earnings to Total Assets 0.355 0.377 0.401 0.417 0.462 1.4 EBIT to Total Assets 0.119 0.145 0.121 0.107 0.137 3.3 Market Cap to BV of Total Liabilities 2.766 3.338 4.401 5.113 4.305 0.6 Sales to Total Assets 1.429 2.766 1.552 1.546 1.607 1.0 Altman Z‐Score 4.055 4.731 5.358 5.751 5.518

- 26. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 26 WWBD? What Would Ben (Graham) Do? The British‐American “father of value investing,” Ben Graham, was raised in an environment lacking financial security. After graduating from Columbia University, Graham went to Wall Street where he developed many successful investment strategies to combat this insecurity. His fundamental belief was crafted into the “margin of safety” formula, the difference between an investment price and intrinsic value of a stock. According to Graham, if an individual stock surpasses at least four of the eight hurdles, Mr. Graham would consider investing. His intention was to discover undervalued stocks that are heading towards sustained future growth. The first four hurdles measure a stock’s potential reward and the second four hurdles assess the risk of investing in a particular stock. On November 9, 2015, Ben Graham would consider purchasing Team Inc. stock because it sufficiently passes four of the eight hurdles: earnings to price yield of 2X the yield on the Ten‐ Year Treasury, a price to earnings ratio down to one‐half of the stock’s highest in five years, current ratio of 2 or more, and an earnings growth of greater than or equal to 7% over the past two years. However, the fluctuating stock price is currently more than 1.5 times its book value. Even at the current lower than average price, Ben Graham would not believe this option was discounted enough to be worth an investment. Additionally, since Team does not issue dividends, the Company does not pass Graham’s dividend hurdle. Currently, Team’s interest‐bearing debt is $359.1 million and its book value is $329.7 million, which places Team 10% above the maximum level Graham considers acceptable. When seeking out investments with the potential for future growth, Ben Graham would be hesitant to invest in a company with this level of debt. In addition, due to the recent company acquisitions and the volatile economy, the rate of earnings has not increased at a consistent level, which Ben Graham would consider a significant risk. All financials considered, Mr. Graham would potentially consider investing in Team Inc. Figure 9: Ben Graham’s Investment Dial

- 27. Team Incorporated (TISI) BURKENROAD REPORTS (www.burkenroad.org) November 9, 2015 27 Earnings per share (ttm) 9.41$ Price: 38.14$ Earnings to Price Yield 24.68% 10 Year Treasury (2X) 4.72% P/E ratio as of 5/31/11 17.4 P/E ratio as of 5/31/12 16.8 P/E ratio as of 5/31/13 23.6 P/E ratio as of 5/31/14 29.9 P/E ratio as of 5/31/15 21.5 Current P/E Ratio 4.1 Dividends per share (ttm) ‐$ Price: 38.14$ Dividend Yield Nil 1/2 Yield on 10 Year Treasury 1.18% Stock Price 38.14$ Book Value per share as of 8/31/15 15.77$ 150% of book Value per share as of 8/31/15 23.65$ Interest‐bearing debt as of 8/31/15 359,100$ Book value as of 8/31/15 329,699$ Current assets as of 8/31/15 301,256$ Current liabilities as of 8/31/15 84,909$ Current ratio as of 8/31/15 3.5 EPS for year ended 5/31/15 1.85$ EPS for year ended 5/31/14 1.40$ EPS for year ended 5/31/13 1.53$ EPS for year ended 5/31/12 1.59$ EPS for year ended 5/31/11 1.32$ EPS for year ended 5/31/15 1.85$ 32% EPS for year ended 5/31/14 1.40$ ‐8% EPS for year ended 5/31/13 1.53$ ‐4% EPS for year ended 5/31/12 1.59$ 20% EPS for year ended 5/31/11 1.32$ Stock price data as of November 9, 2015 TEAM INC. (TISI) Ben Graham Analysis Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury Yes Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs Yes Hurdle # 8: Stability in Growth of Earnings No Hurdle # 5: Total Debt less than Book Value No Hurdle # 6: Current Ratio of Two or More Yes Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years Yes Hurdle # 3: A Dividend Yield of 1/2 the Yield on 10 Year Treasury No Hurdle # 4: A Stock Price less than 1.5 BV No