Recommended

More Related Content

Viewers also liked

Viewers also liked (20)

Similar to Gulf Island Fabrication INC. Burkenroad Analyst Report

Similar to Gulf Island Fabrication INC. Burkenroad Analyst Report (20)

Gulf Island Fabrication INC. Burkenroad Analyst Report

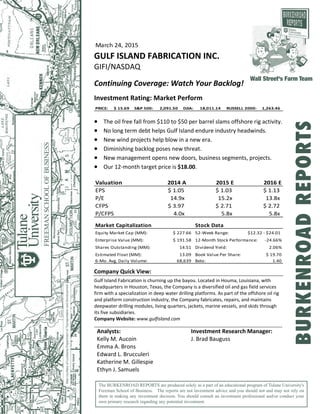

- 1. March 24, 2015 GULF ISLAND FABRICATION INC. GIFI/NASDAQ Continuing Coverage: Watch Your Backlog! Investment Rating: Market Perform PRICE: $ 15.69 S&P 500: 2,091.50 DJIA: 18,011.14 RUSSELL 2000: 1,263.46 The oil free fall from $110 to $50 per barrel slams offshore rig activity. No long term debt helps Gulf Island endure industry headwinds. New wind projects help blow in a new era. Diminishing backlog poses new threat. New management opens new doors, business segments, projects. Our 12‐month target price is $18.00. Valuation 2014 A 2015 E 2016 E EPS $ 1.05 $ 1.03 $ 1.13 P/E 14.9x 15.2x 13.8x CFPS $ 3.97 $ 2.71 $ 2.72 P/CFPS 4.0x 5.8x 5.8x Market Capitalization Stock Data Equity Market Cap (MM): $ 227.66 52‐Week Range: $12.32 ‐ $24.01 Enterprise Value (MM): $ 191.58 12‐Month Stock Performance: ‐24.66% Shares Outstanding (MM): 14.51 Dividend Yield: 2.06% Estimated Float (MM): 13.09 Book Value Per Share: $ 19.70 6‐Mo. Avg. Daily Volume: 68,639 Beta: 1.40 Company Quick View: Gulf Island Fabrication is churning up the bayou. Located in Houma, Louisiana, with headquarters in Houston, Texas, the Company is a diversified oil and gas field services firm with a specialization in deep water drilling platforms. As part of the offshore oil rig and platform construction industry, the Company fabricates, repairs, and maintains deepwater drilling modules, living quarters, jackets, marine vessels, and skids through its five subsidiaries. Company Website: www.gulfisland.com Analysts: Investment Research Manager: Kelly M. Aucoin J. Brad Bauguss Emma A. Brons Edward L. Brucculeri Katherine M. Gillespie Ethyn J. Samuels The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment. Wall Street's Farm Team BURKENROADREPORTS

- 4. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 4 Table 1: Historical Burkenroad Ratings and Prices Date Rating Price* 03/14/14 Market Perform $24.00 04/02/13 Market Outperform $26.00 04/03/12 Market Outperform $37.00 03/23/11 Market Perform $34.10 04/06/10 Market Perform $25.49 04/02/09 Market Outperform $13.79 04/15/08 Market Perform $37.19 04/13/07 Market Outperform $43.14 04/10/06 Market Perform $23.63 03/15/05 Market Perform $23.70 03/26/04 Market Outperform $19.03 11/22/02 Market Outperform $16.09 02/15/02 Buy $12.50 *Price at time of report date INVESTMENT THESIS Gulf Island’s near future is clouded by the effect of the sharp decline in oil price on offshore rig activity, but decisions by new management and diversification efforts indicate a more favorable long‐term outlook. The oil price plunge in the last quarter brings into question the fiscal feasibility of the expensive deep water drilling industry, a main component to Gulf Island operations. This is already impacting rig activity in the Gulf of Mexico, which is a critical revenue source for the Company. Additionally, the Company’s backlog has been steadily decreasing and, paired with possible suspensions or terminations of existing projects because of low oil prices, could cause trouble. Gulf Island’s lack of long‐term debt cushions the blow of rough industry conditions and allows the Company to focus more on adapting rather than merely surviving. As such, the Company is expanding into alternative energy wind projects in order to diversify operations. Additionally, new management is very experienced in the oilrig and platform construction industry and is already making an impact by focusing on improving margins. The oil free fall from $100 to $50 per barrel slams offshore rig activity Although Gulf of Mexico rig count is remaining relatively steady, rig activity has been severely impacted by the plunge in oil prices. Marketed utilization measures the percentage of oil rigs in use compared to the marketed supply of oil rigs available. According to IHS Petrodata, the marketed utilization for Gulf of Mexico Rigs changed from 95.3% in 2013 to 79% as of January 2015. The sharp decrease in marketed utilization is a concerning trend for Gulf Island and the entire oil rig and platform construction industry. If companies are not using rigs that are already deployed, then increased demand for existing rigs and fabrication of more rigs is unlikely. Oil prices in the $65 to $75 per barrel range would likely stimulate more deep water drilling activity, but prices as of February 2015 were below $50 per barrel.

- 13. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 13 Products and Services Gulf Island Fabrication specializes in building offshore drilling and production structures. These structures include platforms, deck sections of fixed and floating platforms, piles, and utility modules. Gulf Island’s subsidiaries operate in various functions of the fabrication process. Lines of business include construction and repair of marine support vessels, offshore and inland construction services, steel production and sales, and contracted labor services. Additionally, Gulf Island Fabrication services existing platforms by providing scaffolding, painting, pipe insulation, and loading and unloading services. Vertical integration allows Gulf Island to monitor and control its costs closely. The target customers for Gulf Island Fabrication are oil and gas drilling companies seeking the fabrication of offshore production structures in the central and western parts of the Gulf of Mexico. The Company’s large fabrication space, over 650 acres combined across its five subsidiary fabrication facilities described in Table 2, allows it to build some of the largest offshore structures in the Gulf. Table 2: Gulf Island Subsidiaries Name Area of Production Location Gulf Island, LLC Fabrication Houma, LA Dolphin Services, LLC Fabrication and Service Provider Houma, LA Dolphin Steel Sales, LLC Steel Customization and Sales Houma, LA Gulf Island Marine Fabricators, LLC Construction and Repair of Marine Vessels Houma, LA Gulf Marine Fabricators, LP Fabrication Ingleside, TX & Aransas Pass, TX Source: Company Website Strategy Gulf Island Fabrication’s strategy centers on offering its customers superior value through quality facilities and equipment, knowledgeable personnel, and efficient services. The Company’s 650‐acre fabrication space among its five subsidiaries allows the Company to provide its customers with some of the largest offshore structures in the Gulf. Barriers to entry are relatively low for domestic competition to enter the market for smaller offshore structures. However, Gulf Island has sufficient expertise, an ideal location, and appropriate facilities to produce larger equipment for water depths beyond 300 feet, a distinct competitive advantage. In addition, Gulf Island offers a trustworthy reputation and safety record that facilitates strong customer relations. From a financial perspective, Gulf Island’s goal is to maintain a strong balance sheet that mitigates risk and provides financial flexibility. The Company maintains substantial cash reserves and avoids long‐term debt. At the end of the third quarter of 2014, Gulf Island had $26.7 million in cash, no long‐term debt, and a market capitalization of $238.34 million.

- 15. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 15 The repercussions of the Deepwater Horizon incident increased regulation in the industry. The U.S. government is restricting the creation of new rigs, so the demand for retrofitting existing rigs is increasing. Gulf Island Fabrication is able to compete in this new environment through state of the art machinery that has been installed and is ready for use. Gulf Island Fabrication is also considering expanding into floating liquefied natural gas (FLNG), petro chemicals, and refined oil products through potential joint ventures, mergers, or subcontracts. However, no mergers or acquisitions are publicly ongoing at this time. PEER ANALYSIS Gulf Island Fabrication operates in a private‐firm dominated industry; therefore, identifying a peer group is challenging. Because of a lack of data on privately owned companies in the industry, the peer group we selected for Gulf Island contains companies that offer similar products and services, but that may be larger than the Company. The peer group that we selected for Gulf Island consists of McDermott International, Inc. (MDR), Dril‐Quip, Inc. (DRQ), and Conrad Industries, Inc. (CNRD). These four companies are all strongly impacted by oil prices, which drive drilling activity in the Gulf of Mexico and in international waters. Selected financial measures of Gulf Island and its peers are shown in Table 3. Table 3: Peer Analysis Ticker Symbol Market Cap ($MM) EV ($MM) P/E (x) P/BV (x) EV/ EBITDA (x) D/E (%) Dividend Yield (%) ROE (%) Gulf Island Fabrication, Inc. GIFI 245.83 215.90 19.83 0.85 4.89 0.00 2.40 4.30 McDermott International, Inc. MDR 520.44 863.30 N/A 0.35 N/A 6.15 N/A 21.80 Dril‐Quip DRQ 2,882.30 2,584.50 15.00 2.31 8.73 0.00 N/A 16.10 Conrad Industries, Inc. CNRD 193.10 119.8 7.00 1.75 2.73 1.03 N/A 21.80 Averages 960.42 945.88 13.94 1.32 5.45 1.80 2.40 16.00 Source: Bloomberg, January 29, 2015 McDermott International, Inc. (MDR/NYSE) McDermott International, Inc., concentrates on engineering, procuring, constructing, and installing (EPCI) projects for offshore oil and gas companies worldwide. The company operates both domestically and internationally in four offshore business segments: Asia Pacific, Atlantic, Caspian, and the Middle East. The company was founded in 1923 as J. Ray McDermott & Company, Inc., in Luling, Texas. In 1932, the company relocated its headquarters to Houston, Texas, following the boom in oil exploration in the area. McDermott currently has 16 significant subsidiaries, allowing McDermott to offer fully integrated EPCI services. McDermott’s market capitalization of $520 million is almost double Gulf Island’s market capitalization. Further, the company’s debt‐to‐equity ratio of 6.15 is the highest in the peer group and is substantially higher than Gulf Island, which has no long‐term debt.

- 17. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 17 Table 4: ROIC Analysis Year Gulf Island Fabrication, Inc. (GIFI) McDermott International, Inc. (MDR) Dril‐Quip (DRQ) Conrad Industries, Inc. (CNRD) Peer Average 2014 4.82% ‐‐ 16.28% 24.11% 20.20% 2013 2.43% ‐‐ 14.32% 24.11% 19.22% 2012 ‐‐ ‐‐ 11.71% 19.04% 15.38% 2011 ‐‐ 7.48% 10.68% 19.31% 12.49% 2010 3.05% 16.10% 13.08% 11.85% 13.68% 2009 6.99% 17.02% 16.38% 16.41% 16.60% Average 4.19% 13.53% 13.23% 18.24% 15.00% Source: Bloomberg February 12, 2015 Kirk J. Meche President, Chief Executive Officer, and Director (51) Kirk J. Meche was recently appointed CEO at the beginning of 2013. He has also served as the President of Gulf Island since 2009. Meche previously worked as the COO from 2009 to the end of 2012 and Executive Vice President of Operations from 2001 to 2009. He has worked with many of Gulf Island’s subsidiaries, including Gulf Marine, Gulf Island, L.L.C. and Southport. Meche began working with Gulf Island in 1996 as a Project Manager after leaving McDermott International, where he worked as an engineer. Jeffrey M. Favret Chief Financial Officer, Treasurer, and Vice President (52) Jeffrey M. Favret joined Gulf Island as CFO in April of 2013. He previously worked at FMC Technologies as the Director of Finance within the Energy Infrastructure before leaving for Gulf Island. Favret has also served as the Chief Accounting Officer at Trico Marine Services, Inc. Favret started his career with Ernst & Young as a Certified Public Accountant before joining Postlethwaite & Netterville in 2007 as an Associate Director. Todd F. Ladd Chief Operating Officer (47) Todd F. Ladd was named COO in February 2014. Ladd has over 25 years of offshore platform fabrication industry experience. He previously served as Gulf Island’s Vice President and General Manager from July 2013 until he began serving as COO. Prior to his employment at Gulf Island, Ladd served as a partner and Senior Project Manager at Paloma Energy Consultants for 12 years. Ladd’s introduction to the Company occurred in April 1996, when he was hired as Project Manager for Gulf Island, L.L.C. Additionally, Ladd served as Production Engineer and Facility Engineer at McDermott Marine Construction for eight years, beginning in January 1988.

- 18. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 18 John P. Laborde Chairman of the Board (64) John P. Laborde has served as the Chairman of the Board for Gulf Island since 2013. Laborde consulted with Gulf Island extensively throughout 1996 before joining the Company as the International Marketing Manager and as Director at the end of that year. Laborde is also the President of Overboard Holdings, L.L.C. and President and CEO of All Aboard Development Corporation, which are both companies in the oil and gas exploration industry. Board of Directors The Board of Directors consists of eight directors and the Company President and CEO. John P. Laborde, who was elected to the Board in 1997, has served as Chairman since 2013. The Board elected three new directors to serve effective March 13, 2014. Additionally, Alden J. Laborde was named Director Emeritus upon his retirement from Gulf Island in 2012 in honor of his service to Gulf Island and his position as Co‐Founder of the Company. Table 5 shows the composition of Gulf Island’s Board of Directors as of February 10, 2015. Table 5: Gulf Island Fabrication Board of Directors Name Position Year Elected John P. Laborde Chairman of the Board 1997 Kirk J. Meche Director, President, CEO 2012 Gregory J. Cotter Director 1985 Michael A. Flick Director 2007 Christopher M. Harding Director 2007 Jerry D. Dumas Director 2011 William E. Chiles Director 2014 Michael J. Keeffe Director 2014 Murray W. Burns Director 2014 Source: MorningStar February 10, 2015 SHAREHOLDER ANALYSIS As of March 19, 2015, Gulf Island Fabrication (GIFI) has 14,738,900 shares of common stock outstanding with 80% of these outstanding shares owned by institutional investors and mutual funds. As illustrated in Figure 5 and detailed in Table 6, most funds investing in Gulf Island are index, core value, and growth at a reasonable price (GARP) funds. One reason why index funds hold so much of the Company is because Gulf Island is a member company for the Russell 2000 index. According to the Russell website, the Russell 2000 aims to measure the performance of the small‐cap segment of the U.S. equity universe. Both GARP and core value style funds look for stability. The top‐ten shareholders of the Company changed little in the past year and the top‐three shareholders remained the same. Though two of the top‐ three shareholders slightly decreased their stake in Gulf Island, the fact that they retained the large majority of Company holdings is a sign of continued belief in Gulf Island.

- 19. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 19 Figure 5: Ownership by Investment Style Source: Thompson One February 2, 2015 Table 6: Gulf Island Shareholder Investment Styles Investment Style % Shares Outstanding Investors Shares Value ($) Index 15.66 98 2,274,967 38,765,437.68 Core Value 14.22 24 2,067,515 35,230,455.60 GARP 13.40 27 1,947,225 33,180,714.00 Deep Value 4.91 3 721,886 12,300,937.44 Core Growth 3.08 24 449,235 7,654,964.40 Growth 1.55 6 225,591 3,844,070.64 Yield 0.51 3 73,647 1,254,944.88 Specialty 0.35 1 51,310 874,322.40 Aggressive Growth 0.05 7 7,369 125,567.76 Equity Hedge 0.04 1 5,882 100,229.28 Income Value 0.01 1 1,519 25,883.76 Source: Thompson One February 1, 2015 Table 7 lists the top‐ten shareholders of Gulf Island. T. Rowe Price Associates, Inc. is the number one shareholder, holding 1.8 million shares, which is 12.54% of all outstanding shares. In the past year, T. Rowe sold 4,100 as the stock price climbed to $23.50 in April of 2014. The number two shareholder is Heartland Advisors, Inc., holding 1.54 million shares constituting 10.64% of total shares outstanding. After Heartland, BlackRock holds the third largest amount of outstanding shares of the Company. Blackrock increased its position in Gulf Island by 7.87% from last year, from 1.13 million shares up to 1.22 million shares. These large investment companies include Gulf Island holdings as part of value and index funds, which account for 20% of Gulf Island ownership. Index, 15.66% Core Value, 14.22% GARP, 13.40% Deep Value, 4.91% Core Growth, 3.08% Growth, 1.55% Other, 0.96%

- 20. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 20 Table 7: Gulf Island Top‐Ten Shareholders No. Holder Name Shares Held % of Shares Outstanding 1 T. Rowe Price Associates, Inc. 1,819,380 12.54 2 Heartland Advisors, Inc. 1,543,805 10.64 3 BlackRock Institutional Trust Company, N.A. 1,127,320 7.77 4 Dimensional Fund Advisors, L.P. 950,806 6.55 5 Starboard Enterprises, L.L.C. 884,700 6.10 6 Royce & Associates, LLC 746,025 5.14 7 The Vanguard Group, Inc. 617,092 4.25 8 Killen Group, Inc. 508,057 3.50 9 DePrince, Race & Zollo, Inc. 438,680 3.02 10 Columbia Management Investment Advisers, LLC 349,936 2.41 Source: Thompson One February 2, 2015 Insider Analysis As shown below in Table 8, Gulf Island insiders own just less than 1% of Gulf Island’s stock. Kirk Meche is the largest insider owner of Gulf Island stock. Meche, the President and CEO of Gulf Island, owns roughly 0.43% of Gulf Island stock, which is equal to 62,265 shares and is valued at $1,063,486 as of February 2015. Joseph Gallagher, former Chief Financial Officer of Gulf Island, owns the second largest portion of Gulf Island stock with 31,200 shares. The remaining top insider shareholders are all major executives at Gulf Island. Table 8: Gulf Island Top‐Five Shareholders No. Holder Name Shares Held % of Shares Outstanding Value of Holdings ($) 1 Meche (Kirk J) 62,265 0.43 1,060,996 2 Gallagher (Joseph P. III) 31,200 0.21 531,648 3 Blanchard (William G.) 16,398 0.11 279,422 4 Smith (Francis A. Jr.) 15,320 0.11 261,053 5 Ladd (Todd F.) 15,000 0.10 255,600 Source: Thompson One, February 2, 2015 RISK ANALYSIS AND INVESTMENT CAVEATS Operational Risks Gulf Island Fabrication is subject to various risks that can affect the Company and its operations. Risks include fluctuating commodity prices of both steel and oil, the impacts of seasonality and weather, the small customer base, competition in the labor market, and backlog.

- 28. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 28 ANOTHER WAY TO LOOK AT IT ALTMAN Z‐SCORE The Altman Z‐Score Analysis, created by Edward Altman in 1968, measures the probability that a company will go bankrupt in the following two years. This analysis takes into consideration five financial ratios including working capital to total assets, retained earnings to total assets, earnings before interest and taxes to total assets, market value of equity to book value of total liabilities, and sales to total assets. The Analysis weights the five financial ratios according to the relative importance within the Z‐Score and the final Z‐Score falls into one of three groupings; a low risk of default with a Z‐Score above 2.99, a high risk of default with a Z‐Score of below 1.8, and a moderate risk of default with a Z‐Score between 1.8 and 2.99. Table 9 shows Gulf Island Fabrication’s Z‐Scores for the past eight years. The Company’s Z‐ Score for 2014 is 3.91, which puts Gulf Island well within the low‐risk range. This Z‐Score means that the Company is unlikely to experience a bankruptcy within the next two years. The 2014 Z‐Score is an improvement on 2013’s Z‐Score of 2.21, which was in the moderate risk range. The Company’s recurring debt, which inflates the Z‐Score, makes the Company’s future look bright. Table 9: Z Scores Year Z Score 2007 5.51 2008 3.75 2009 5.31 2010 7.26 2011 3.94 2012 3.62 2013 2.21 2014 3.91 Source: Bloomberg March 25, 2015

- 30. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 30 WWBD? What Would Ben (Graham) Do? Ben Graham was a legendary investor who championed the method of “Value Investing” throughout his career. Graham used his experience to craft a formula for choosing which stocks to invest in, which was published by Graham in Forbes Magazine in 1977 as “Last Will & Testament.” The formula focuses on evaluating eight specific hurdles that identify undervalued stocks with growth potential. The first four hurdles distinguish stocks with low price to operation ratios, while the second four hurdles assess risk. Gulf Island Fabrication, Inc. passes five of the hurdles outlined by Graham in his formula and should therefore be seriously considered as a good investment (see Figure 10). Gulf Island successfully meets four of the first five hurdles, suggesting that the market may be undervaluing the stock. The Company meets three of these hurdles considerably, with a P/E ratio significantly lower than half of its highest over the past five years and a stock price $15 lower than one and half times its book value. Most notably, Gulf Island has no debt, so its total debt is far below its book value. However, Gulf Island fails to meet either of Graham’s last hurdles that identify growth stocks. This result is unsurprising as Gulf Island is a mature, asset heavy company whose earnings depend heavily on the price of oil. Nonetheless, Gulf Island is an attractive investment under Graham’s methodology. Figure 10: Ben Graham Analysis

- 31. Gulf Island Fabrication Inc. (GIFI) BURKENROAD REPORTS (www.burkenroad.org) March 24, 2015 31 Earnings per share (ttm) 1.06$ Price: 15.69$ Earnings to Price Yield 6.73% 10 Year Treasury (2X) 3.85% P/E ratio as of 2010 29.3 P/E ratio as of 2011 (211.7) P/E ratio as of 2012 (68.0) P/E ratio as of 2013 45.2 P/E ratio as of 2014 18.3 Current P/E Ratio 14.9 Dividends per share (ttm) 0.40$ Price: 15.69$ Dividend Yield 2.55% 1/2 Yield on 10 Year Treasury 0.96% Stock Price 15.69$ Book Value per share as of 12/31/14 19.70$ 150% of book Value per share as of 12/31/14 29.56$ Interest‐bearing debt as of 12/31/14 ‐$ Book value as of 12/31/14 285,798$ Current assets as of 12/31/14 172,495$ Current liabilities as of 12/31/14 72,765$ Current ratio as of 12/31/14 2.4 EPS for year ended 2014 1.05$ EPS for year ended 2013 0.50$ EPS for year ended 2012 (0.28)$ EPS for year ended 2011 (0.13)$ EPS for year ended 2010 0.90$ EPS for year ended 2014 1.05$ 110% EPS for year ended 2013 0.50$ ‐277% EPS for year ended 2012 (0.28)$ 118% EPS for year ended 2011 (0.13)$ ‐114% EPS for year ended 2010 0.90$ Stock price data as of M arch 24, 2015 No Hurdle # 3: A Dividend Yield of 1/2 the Yield on 10 Year Treasury Yes Hurdle # 4: A Stock Price less than 1.5 BV Yes Hurdle # 5: Total Debt less than Book Value Yes Hurdle # 6: Current Ratio of Two or More Yes Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years No Hurdle # 8: Stability in Growth of Earnings Yes GULF ISLAND FABRICATION INC. (GIFI) Ben Graham Analysis Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury No Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs