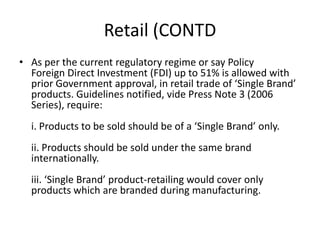

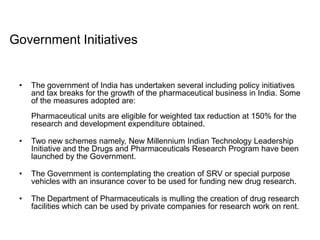

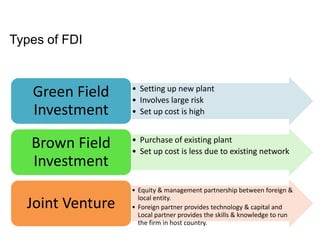

FDI in the Indian pharmaceutical industry has grown significantly in recent years. The government has undertaken initiatives like tax reductions for R&D spending to encourage growth. While India has a strong manufacturing base and skilled workforce, it lacks investment in research. FDI allows foreign companies to set up manufacturing facilities through greenfield investments or purchase existing plants through brownfield investments. Joint ventures also provide opportunities for technology transfer and skills development. Mauritius is a major source of FDI in the Indian pharmaceutical sector.