1. AUDIT PROGRAMME

TRADE PAYABLES

Name of Client Sheridan AV

Year-end 31 March 2021

Name of Auditor (s) Ailyn C. Ruaya

Trade payables are the amounts the company owes its suppliers for the

provision of goods and services. Trade payables are shown as current

liabilities. . Substantive testing should be carried out at year end on the

Statement of Financial Position to gain evidence regarding the following

assertions:

Presentation and disclosure

Accuracy classification and valuation

Rights and Obligations

Completeness and cut off

Existence or Occurrence

The following substantive tests were carried out on the trade payables showing

on the Statement of Financial Position (see attached)

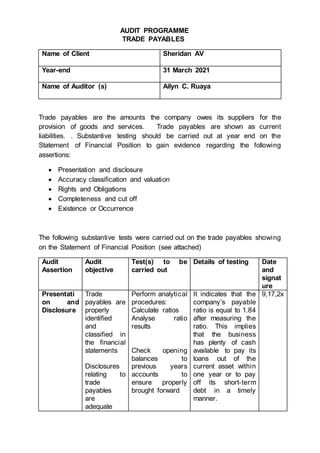

Audit

Assertion

Audit

objective

Test(s) to be

carried out

Details of testing Date

and

signat

ure

Presentati

on and

Disclosure

Trade

payables are

properly

identified

and

classified in

the financial

statements

Disclosures

relating to

trade

payables

are

adequate

Perform analytical

procedures:

Calculate ratios

Analyse ratio

results

Check opening

balances to

previous years

accounts to

ensure properly

brought forward

It indicates that the

company’s payable

ratio is equal to 1.84

after measuring the

ratio. This implies

that the business

has plenty of cash

available to pay its

loans out of the

current asset within

one year or to pay

off its short-term

debt in a timely

manner.

9,17,2x

2. Obtain a list of

trade payables

balances. Check

a sample to

underlying

records.

Test the list adds

up. Agree the list

to the control

account and to

the financial

statements

Compare

statement

presentation with

applicable

accounting

standards to

determine that

trade payables

are properly

identified and

classified in

financial

statements

Determine

appropriateness

of any disclosures

relating to trade

payables

Accuracy,

classificati

on and

valuation

Rights and

Obligation

s

Trade

payables are

stated at

correct

amount

owed

Trade

payables are

liabilities of

Vouch a sample

of trade payables

to supporting

documentation as

follows:

Vouch from list of

trade payables to

suppliers’

invoices, goods

received notes

and purchase

orders or other

It is noticed that the

trade payables are

reported at the

correct amount

owed after

confirming the

correct steps.

It is stated that the

liabilities borne by

the Company at the

date of the financial

position Statement

9,17,2x

3. the entity at

the date of

the

Statement of

Financial

Position

supporting

documentation to

ensure recorded

at correct amount

owed.

are trade payables

or monetary

obligations.

Completen

ess and

Cut off

Trade

payables

include all

amounts

owed by the

entity to

suppliers of

goods and

services at

the

Statement of

Financial

Position date

All trade

payables are

recorded in

the correct

accounting

period

Perform a search

for unrecorded

liabilities by:

Analytical review

Discussion with

management on

steps they have

taken to ascertain

all liabilities

recorded

Select a sample

of recorded

purchase

transactions from

several days

before and after

year-end and

examine

supporting

suppliers invoices

and goods

received notes to

determine that

purchases were

recorded in the

correct period

Observe the

number of the last

goods received

note issued on the

last business day

of the audit period

and trace a

sample of lower

and higher

numbered goods

received notes to

related purchase

After all trade

payables have been

checked, it is known

that all trade

payables and other

supporting

documentation are

correctly registered.

This ensures that in

the proper

accounting period,

the transactions and

creditors balances

are reported

properly and

accurately.

9,17,2x

4. documents to

determine

whether

transactions were

recorded in the

proper period

Identify any

amounts on

ageing report that

are overdue their

invoiced terms

and investigate

any reasons with

Sheridan AV.

Enquire if there

are any late

payment charges.

Existence

or

Occurrenc

e

Recorded

trade

payables

represent

amount

owed by the

entity at the

date of the

financial

statements

Perform a

payables

circularisation if

necessary (see

attached sheet)

After the amounts of

the sales invoices

and the debtors’

subsidiary ledgers

have been checked

and compared, it is

known that the

amount reported by

Rama Home in the

ledger does not

equate to or equal to

the amount reported

in the invoice.

Therefore, unless

the amount reported

is inaccurate or in

dispute, the auditor

must conduct a

payable

circularization or

negative circulation.

9,17,2x

5. From the audit work carried out I confirm that there are misstatement and

incorrect amount presented of the trade payables. Please examine the

presented data below and compare them to your records. Thus, in my view, the

trade payables are not reasonably specified.

Signed

AIlYN C. RUAYA

Auditor

6. September 17, 202x

Sheridan AV

This request is sent to you to allow our independent auditors to confirm that our

record is accurate.

This is to inform you that on the Rama Home Sales Invoice, our records on

February 05, 2021 showed a sum of ⁇ 156,720.00.If this record is the same

with your records on that date please confirm by signing and returning this form

directly to our auditors. For this aim, an addressed envelope is enclosed.If you

notice any discrepancy with the space given below, please report the

information directly to our auditor!

Yours Faithfully,

Ailyn C. Ruaya

********

Surigao City

The above amount is correct/ incorrect for the following reasons ________.

Yours Faithfully,

________________

Sheridan AV

7. HOW TO CARRY OUT A TRADE PAYABLES CIRCULARISATION

1 Select a sample of accounts for confirmation from a complete list of

suppliers

2 Confirm with client the payables you wish to circularise. Obtain

explanations where the client does not want you to circularise.

3 Send the confirmation requests. Enclose a prepaid envelope for

return to the firm. Ensure that the reply part of the letter is properly

referenced.

4 Record replies on a control sheet

5 Where replies are not received within a reasonable period send a

follow-up letter

6 Follow alternative procedures for any accounts which have an

unfavourable response or for which no response has been obtained.

7 Summarise the results and consider whether audit evidence has been

obtained for trade payables.