1. Internal Control - Accounts Receivable and Credit Sales

Typical errors or irregularities include:

Sales amounts recorded incorrectly

Goods shipped butnotbilled to customer

Goods billed to customer butnotshipped

Sales recorded in wrong accounting period

Goods sold to customers who were bad creditrisks

Sales occurred that were not authorized

Sales posted to wrong account

Unauthorized write-offs ofreceivables may have occurred.

Internal Control Questionnaire

These questions are designed around the perfectsales system.Ifthe control does notexistthen you tick

‘No’. The auditor then uses this information to identify weaknesses in the current sales system and relate

them to what could go wrong in the accounts.

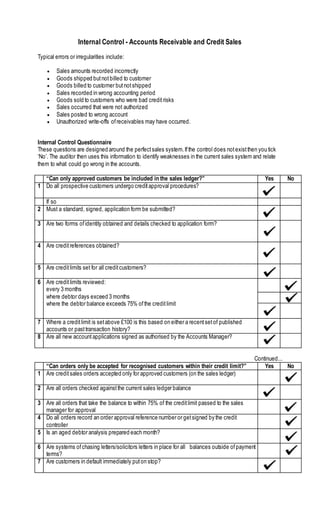

“Can only approved customers be included in the sales ledger?” Yes No

1 Do all prospective customers undergo creditapproval procedures?

If so

2 Must a standard, signed, application form be submitted?

3 Are two forms ofidentity obtained and details checked to application form?

4 Are creditreferences obtained?

5 Are creditlimits set for all creditcustomers?

6 Are creditlimits reviewed:

every 3 months

where debtor days exceed 3 months

where the debtor balance exceeds 75% ofthe creditlimit

7 Where a creditlimit is setabove £100 is this based on either a recentsetof published

accounts or pasttransaction history?

8 Are all new accountapplications signed as authorised by the Accounts Manager?

Continued...

“Can orders only be accepted for recognised customers within their credit limit?” Yes No

1 Are creditsales orders accepted only for approved customers (on the sales ledger)

2 Are all orders checked againstthe current sales ledger balance

3 Are all orders that take the balance to within 75% of the creditlimit passed to the sales

manager for approval

4 Do all orders record an order approval reference number or getsigned by the credit

controller

5 Is an aged debtor analysis prepared each month?

6 Are systems ofchasing letters/solicitors letters in place for all balances outside ofpayment

terms?

7 Are customers in default immediately puton stop?

2. “Do all goods despatched result in a customer being invoiced?” Yes No

1 Are orders recorded on a pre-numbered sales order

2 Are pre-numbered goods despatch notes raised for all goods taken from stores?

3 Can a Goods despatched note (GDN) only be raised on the basis ofan approved sales

order?

4 Are GDNs matched/retained with sales orders?

5 Does someone independentofthe warehouse check goods leaving the premises with the

related GDNs?

6 Do customers sign for all goods accepted?

7 Are any queries agreed with the driver and recorded on the GDN?

8 Do both parties sign the amendments to the GDN?

9 Are signed GDNs/orders checked back in by the warehouse and any changes approved?

10 Does the warehouse manager check the sequence ofGDNs to ensure all returned by the

driver?

11 Are all GDNs passed to the sales ledger department?

12 Are all invoices raised based on the GDN set?

13 Is a copy ofthe GDN referenced to the sales invoice number and filed in numerical order?

14 Does the accounts manager check the sequence ofprocessed GDNs each month?

15 Does the accounts manager check invoices for accuracy and validity (based on approved

sales order, GDN and price lists)

Continued...

“Are all invoices raised recorded in the sales ledger?” Yes No

1 Is the invoicing assistanta different person to the sales ledger assistant?

2 Are invoices recorded in the sales day book in numerical order

3 Does the accounts manager check the sequence ofinvoices recorded in the sales day

book, each month?

4 Are invoice sets filed in numerical order?

5 Is the sales ledger assistanta different person to the invoicing assistant?

6 Are the sales day book totals posted to the main ledger by the Accounts Manager (as

distinct from the sales ledger assistant)?

7 Is sales ledger control accountreconciliation performed by the accounts manager every

month?

8 Are statements issued monthly to active sales ledger accounts?

9 Is the statement run checked againstthe listofbalances by the accounts manager?

“Can items in the sales ledger only be cleared by valid payment, credit note or

journal entry?”

Yes No

1 Are all creditnotes approved by the sales manager?

2 Does the accounts manager review all material creditnotes issued during the month?

3. 3 Can journal entries only be entered by the Accounts Manager?

4 Are cash receipts posted from the cash book each month

5 Is sales ledger control accountreconciliation performed by the accounts manager every

month?

Continued...

“Is all cash received correctly identified, recorded, posted and promptly banked?” Yes No

1 Is all cash received in the postrecorded immediately into a cash diary, to which it is cross

referenced?

2 Do at leasttwo people open the post?

3 Is all cash received then passed immediately to the cashier, intact?

4 Is the cash receipts book written up by the cashier before lunch each day?

5 Is cash banked daily?

6 Is cash banked intact?

7 Is the time and route of the daily banking varied each day?

8 Is proper insurance held to cover loss on the premises or in transit?

9 Is fidelity insurance in place for all staff?

10 Is all cash retained on site keptin a locked safe?

11 Does the accounts manager check a sample ofthe cash diary daily takings to the cash

book?

12 Is the cash book posted to the sales ledger by someone differentto the cashier?

WEAKNESSES RECOMMENDATIONS

1. Sales amounts recorded incorrectly Management should reconcile the balances

between the general ledger, subsidiary records

and the inventory count and account for the

discrepancies.

Maintain a complete and updated subsidiary

record for each of the inventory item traded by the

Agency. Each record should contain all necessary

information relative to the inventory items

2. Sales recorded in wrong accounting

period

Make correcting entries when you find errors.

There are two ways to make correcting entries:

reverse the incorrect entry and then use a second

journal entry to record the transaction correctly, or

make a single journal entry that, when combined

with the original but incorrect entry, fixes the error.

3. Goods sold to customers who were bad

credit risks

Management can use a business strategy called

“credit control” that promotes the selling of goods

by extending creditto customers. Mostbusinesses

try to extend creditto customers with a good credit

history so as to ensure payment of the goods or

services.

4. 4. Sales posted to wrong account If you originally posted to the wrong account, you

might need to adjustthe entire entry. Or, you might

have to make a minor adjustment. If you need to

make a correcting entry, do the following:

Find out all the accounts that are affected

by the error.

Determine the amount that needs to be

adjusted.

You must make new entries for the correction. Use

the same accounts as the original posting for the

correcting entry.

5. Unauthorized write-offs of receivables

may have occurred.

Double check cash discounts and make sure

customers have earned the discounts by following

sales terms and conditions. Resolve any

differences ofinterpretations by meeting, phone, or

e-mail and confirm the agreement. Otherwise,

these will become systemic drip of profits.