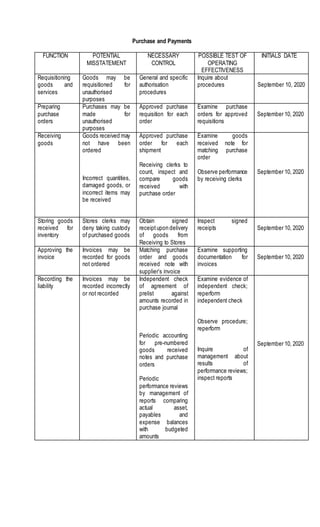

1. Purchase and Payments

FUNCTION POTENTIAL

MISSTATEMENT

NECESSARY

CONTROL

POSSIBLE TEST OF

OPERATING

EFFECTIVENESS

INITIALS DATE

Requisitioning

goods and

services

Goods may be

requisitioned for

unauthorised

purposes

General and specific

authorisation

procedures

Inquire about

procedures September 10, 2020

Preparing

purchase

orders

Purchases may be

made for

unauthorised

purposes

Approved purchase

requisition for each

order

Examine purchase

orders for approved

requisitions

September 10, 2020

Receiving

goods

Goods received may

not have been

ordered

Incorrect quantities,

damaged goods, or

incorrect items may

be received

Approved purchase

order for each

shipment

Receiving clerks to

count, inspect and

compare goods

received with

purchase order

Examine goods

received note for

matching purchase

order

Observe performance

by receiving clerks

September 10, 2020

Storing goods

received for

inventory

Stores clerks may

deny taking custody

of purchased goods

Obtain signed

receiptupon delivery

of goods from

Receiving to Stores

Inspect signed

receipts September 10, 2020

Approving the

invoice

Invoices may be

recorded for goods

not ordered

Matching purchase

order and goods

received note with

supplier’s invoice

Examine supporting

documentation for

invoices

September 10, 2020

Recording the

liability

Invoices may be

recorded incorrectly

or not recorded

Independent check

of agreement of

prelist against

amounts recorded in

purchase journal

Periodic accounting

for pre-numbered

goods received

notes and purchase

orders

Periodic

performance reviews

by management of

reports comparing

actual asset,

payables and

expense balances

with budgeted

amounts

Examine evidence of

independent check;

reperform

independent check

Observe procedure;

reperform

Inquire of

management about

results of

performance reviews;

inspect reports

September 10, 2020

2. Trade Payables

Errors and irregularities include:

1. Purchases may have been recorded to the wrong account

2. A liability may have been setup for a fictitious company

3. The purchase and liability may have been recorded in the wrong accounting period

4. A purchase or liability may have been omitted

5. Purchases may have been recorded butthe merchandise may notbeen received.

YES NO COMMENTS

Has a purchase requisition to be raised for all

purchases?

With this document, procurement doesn’t order goods

directly from vendors but instead initiates a formal

process. And that process is what provides the

company internal control over the purchasing process

Is the purchase requisition pre-numbered? Financial documents should be pre-numbered to

ensure all transactions are recorded and accounted

for.

Has a purchase order to be raised for all

purchases?

It necessary to be recorded in the books by the

account manager

Are purchase orders pre-numbered? Pre-numbered purchase orders ensure the

completeness and identify “missing” orders.

Do purchase orders have to be approved? For any purchase order to be a legally binding contract,

it must pass the internal approval processes ofboth

the buyer and vendor.

Are vendor’s monthly statements reconciled to

the purchase ledger?

Reconciling your vendor statements allows you to

ensure that there are no mistakes or inaccuracies

between what the vendor is charging you and the

inventory, services or supplies you received

Do adjustments to accounts payable require

the approval ofa responsible official?

It is required that adjustments to accounts payable be

approved by a responsible official.

Are all vendors’ invoices checked for proper

pricing, extensions,footings, and terms?

Invoices are checked occasionally.

Does the company ensure that claims for

damaged merchandise are processed

promptly?

When there is any problem with the delivery, then the

goods are returned with the driver and the purchase

ledger clerk is informed.

Are unmatched invoices, receiving reports,

and purchase invoices reviewed periodically?

Timely payments are ensured by periodic reviews of

files of unmatched receiving reports and invoices and

by the aging of open accounts payable

Are supporting documents reviewed by

cheque signers prior to payment?

It should be reviewed from Purchase Ledger to the

authorization ofthe paymentand before it is signed by

the cheque signers.

Are supporting documents stamped

“cancelled” by the cheque signers?

Cheque is passed to the cheque signers together with

the supporting documents

Are cheques mailed directly by the person

signing the cheque and notreturned to the

preparers?

It is returned to the preparers to write in the cash book

and post the cheque to the supplier