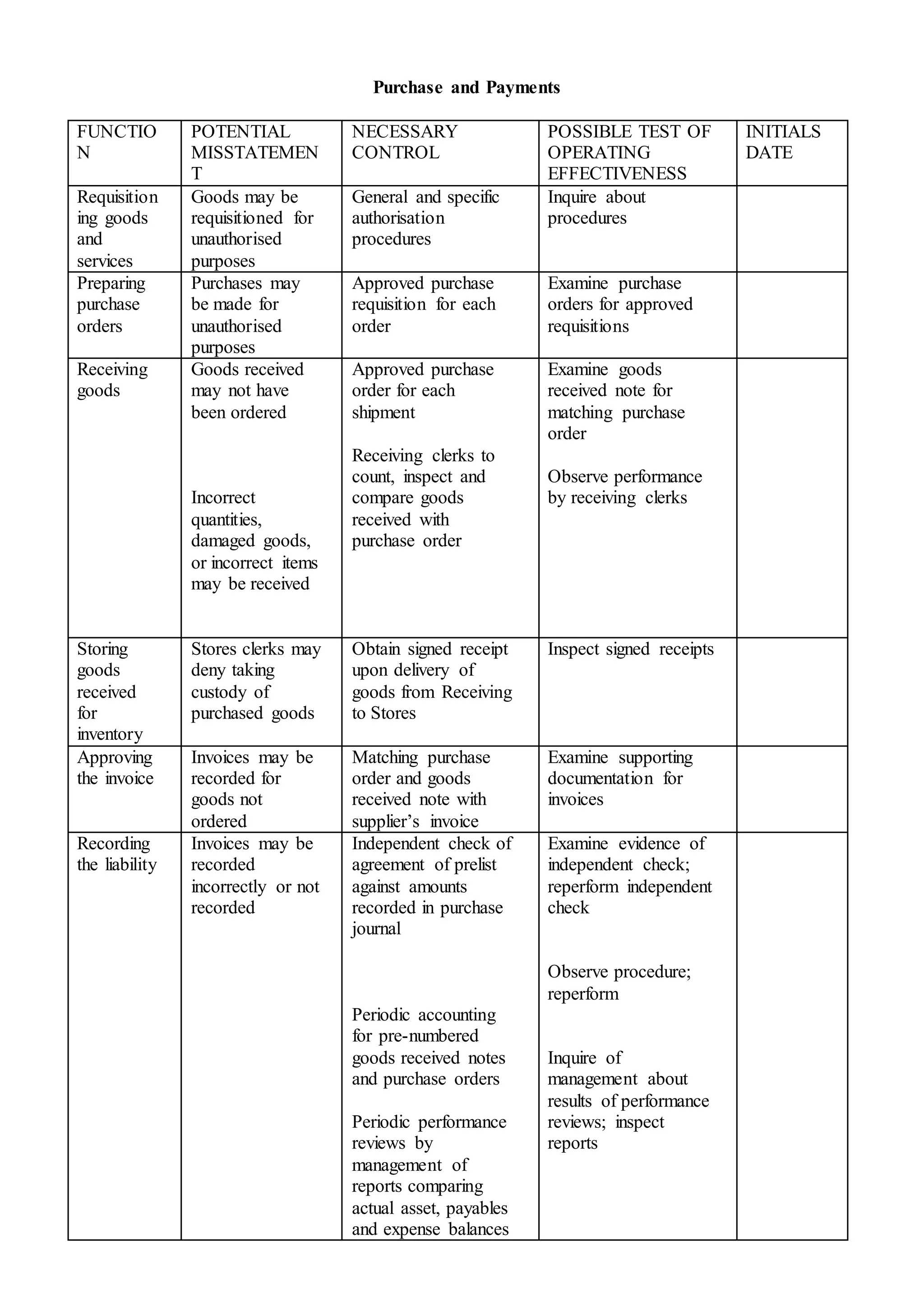

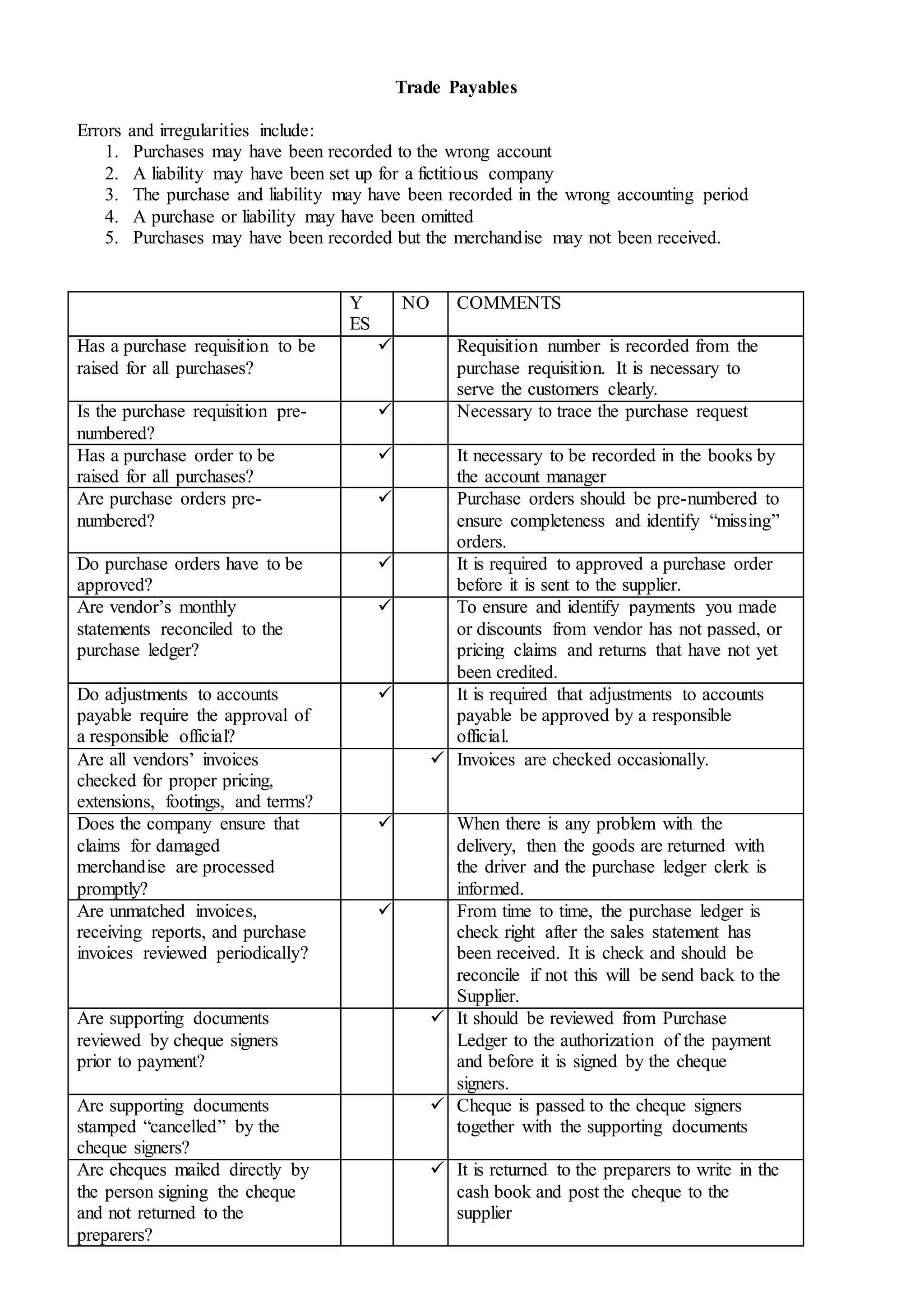

This document discusses controls related to the purchase and payment process. It identifies key functions including requisitioning goods, preparing purchase orders, receiving goods, storing goods, approving invoices, and recording liabilities. For each function it outlines potential misstatements, necessary controls, and possible tests of operating effectiveness. It also includes a checklist of controls related to trade payables, such as requiring purchase requisitions and purchase orders, approving purchases, reconciling statements, and reviewing supporting documents.