The basic of accounting

•Download as DOCX, PDF•

1 like•453 views

The basic of accounting is the part of my book "The system of accounting" volume III enlightened on payment and receipt made by cash and accrual as well as cash flow and fund flow concept in accounting.

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (15)

Similar to The basic of accounting

Similar to The basic of accounting (20)

More from AQEEL RAZA

More from AQEEL RAZA (20)

Recently uploaded

Recently uploaded (20)

The basic of accounting

- 1. THE SYSTEM OF ACCOUNTING Volume III THE BASIS OF ACCOUNTING WRITTEN BY: SYED AQEEL RAZA MASTER OF COMMERCE & POLITICS

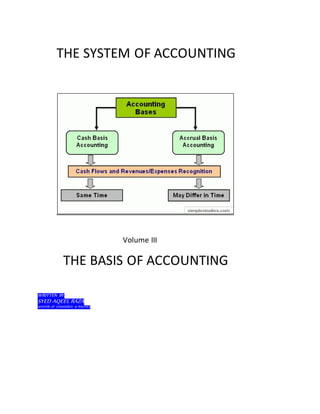

- 2. THE BASIS OF ACCOUNTING ACCOUNTING FOR BASES All accounting system is based on payment and receipt by cash and bank which depends on cash and accrual base accounting and sometime requires cash and accrual base mix accounting to remove draw backs of cash accounting. CASH BASE ACCOUNTING In general, any item which a bank accepts at the face valve of deposit or which may be transferred to another party at face value may be considered cash. In cash base accounting system, transactions are recognized on receipt and payment of cash or a company records cash receipts in the period that they are received and expenses in the period in which they are paid. Revenues and expenses are reported in income statement when the cash is received and expenses occurred. It is usually applied or followed by individual or small and non- manufacturing businesses. If a business expands, it may move to accrual method of accounting. Cash accounting is the opposite of accrual accounting wherein revenue and expenses are recorded when they are incurred but controlled under cash accounting because the revenue and expense which were recorded in their respective accounts as they incurred and the effect in their accounts receivable or payable is paid by cash or bank. <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 3. THE BASIS OF ACCOUNTING Cash accounting has some draw backs; - Daley in recognition of income If a cheque from customer and a cheque to supplier is received and given on the 30th of the month but could not cashed or deposited at the bank, it will be recognized in next month. - Delay in recognition of taxable income A business receives a cheque from a customer near the end of it fiscal year, but does not cash it until the next year will make cause of recognition of taxable income in the current year. - Delay of expenses in recognition of taxable income. A business pays its suppliers early in order to recognize more expenses in the current fiscal year which will reduce its taxable income in the current year. - Unable to present profitability The delay in recording revenue and expenses will make the cause of presenting accurate profitability which will also affect on company’s budget. <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com> THE BASIS OF ACCOUNTING

- 4. THE BASIS OF ACCOUNTING How to remove draw-backs? - As soon as the cheque from customer and the cheque to supplier is received or given must be accounted for either cashed or not in their accounts. The Invoices of sale and purchase must be accrued as and when they incurred. As far as the expenses are concerned, they may be taken or accrued at the end of the year enable account to show clear picture somehow. Hence, we can say that the draw backs of cash accounting can be removed by mix accounting system “cash and accrual accounting.” Advantage of cash accounting; - Cash accounting can also be cost-effective in case of sole proprietorship or partnership and for companies that conduct mostly cash transactions. - Cash accounting requires less staff, financial resources and easy to understand. - Cash accounting clearly represents cash flows and outflows in business than the accrual method of accounting. - Cash accounting provides tax benefits of payments received in 2015 for the work of previous year would be counted as income for 2015 tax year and reduced net income for the year 2015 tax year. <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 5. THE BASIS OF ACCOUNTING Many devices for cash and receipt has been described such as cash book, petty cash book, General Journal and special journals; cash receipt journal, cash payment journal, purchase journal, sales journal, purchase return and allowances journal, sales return and allowances journal etc. on which we have discussed on our previous version. All payments and receipt are done by cash with the company and the cash with bank. The cash in the company is applied in small cash payments and small receipts in cash is also used in it but the payment to suppliers from whom we purchase goods is paid by bank issuing cheque in the name of supplier which goes in clearing and after processing the amount is transferred to supplier account and so on the cheque we deposit of the customer which we receive against sale or services rendered comes to our account. Therefore, cash and bank are two name of one thing “cash” must be compared with company cash book and bank book and it is also necessary to have a complete knowledge regarding the bank procedures and documents used for banking. There are many kinds of bank accounts used for keeping cash and operating for personal and business but profit and loss sharing account (PLS) and Current Account (CD) are mostly used in business which are described below to have complete knowledge of them; <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 6. THE BASIS OF ACCOUNTING PROFIT AND LOSS SHARING ACCOUNT (PLS A/C) This kind of account can be operated by any person, firm or organization by depositing minimum balance Rs.100/=or above which allows profit variable on the amount deposited over a specified period and keeps in share the loss as the case may be to the account holder. The account holder can withdraw or deposit the amount up to the limit prescribed. This account is operated under interest free system but the interest is under question. CURRENT ACCOUNT (CD A/C) This accountis usually operated by the business man and can be opened by Rs.1000/= as an initial deposit at the time of opening the account. The bank issues cheque book 25, 50, 100 leafs as per requirement. There is no interest on this account. Besides, profit and loss sharing account and current account, bank introduces many other accounts like; - Home safe accounts - Student saving account - Saving account - Islami Banking account - Fixed Deposit Account - Credit card - Debit card - Visa card <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 7. THE BASIS OF ACCOUNTING Banks also issues certificates having interest on completion of specified period. Bank uses many forms or documents to make transaction from him but the following forms are used mainly to operate any account or doing transaction: - Cheque book - Pay-in-slip/deposit slip book - Pay order/demand draft making form - On line transfer form BANK’S INTEREST AND CHARGES The bankers enjoys higher rate of interest or profit and allows small rate of interest or profit to the account holder by whose money he enjoys big income. The bank deposit or transfer the amount of interest in the account and informs the account holder by credit memo. The bank also deducts charges of different nature from his account holders in making transaction through bank from which some are mentioned here; Cheque book charges Minimum balance charges Commission Excise duty Withholding tax – filler Withholding tax- non-filler Pay order making charges Demand draft making charges On line transfer charges Postage charges <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 8. THE BASIS OF ACCOUNTING BANK STATEMENT A copy of the account for a period, monthly, half yearly or annually is sent by the bank to the account holder for checking of withdrawals, deposits and balance which is reconciled by company’s cash book. BANK RECONCILIATION The bank reconciliation is the matching statement of two balances at the end of the month or year such as cash book balance and bank statement balance. It is made to search the causes of disagreement in balances and to test the accuracy of the transactions posted in cash book. In case of any unknown discrepancy or difference, the bank is informed within a reasonable time. The balance in cash book and in bank statement may differ; - Cheques issued but not presented to the bank for payment on the end date of the bank statement. - Cheques deposited into the bank but not collected the amount till the end of the date of bank statement. - Interest of the bank not recorded into cash book. - Bank charges, mark-up on over draft are not recorded in the cash book. - Cheques issued but not recorded in the cash book. - Wrong posting of amount by the bank in the account. - Wrong positing of amount in the cash book. - Unknown collection or credit shown in bank statement. - Unknown payment or debit shown in bank statement. - Bank commission, excise duty, cheque book charges, pay order charges, demand draft charges, any instrument making charges, and tax on cash withdrawn are ascertained on seeing the bank statement. - Many other causes of disagreement with cash and bank. - <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 9. THE BASIS OF ACCOUNTING METHOD OF BANK RECONCILIATION STATEMENT There are two method are applied for bank reconciliation wherein; o Correct method o Adjusted method In corrected method, the items which are shown in bank statement but not in cash book will be recorded in cash book before making bank reconciliation or on the way of finding out difference at once and in adjusting method after making bank reconciliation statement but the main object is to determine the correct balance of both cash book and the bank statement. PROCEDUTURE OF BANK RECONCILIATION Keep two books before you and examine each other by ticking the amount, cheque number, bank deposit slip number and any other reference match with cash book and bank statement. The ticked items are agreed but un- ticked items are under question and need clarification. Following are the steps and points for making bank reconciliation statement; - At first, both the balances are written like balance as per cash book (business record) and balance as per bank statement (Bank record) for example; Bank statement Cash book Balances 24,750 18,000 <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 10. THE BASIS OF ACCOUNTING 1- Out-standing cheques, unpaid cheques, un-presented cheques Out-standing cheques or unpaid cheques are the cheques which are issued for payment but not presented or collected by the party to whom the cheque is issued remained unpaid by the bank before the end of the month or end date of bank statement June 30, 2015. The out-standing cheques or unpaid cheques are reduced by the bank as and when they are presented by the party. The Cash book had already been reduced by the cheques as and when they were issued and the bank book would be reduced as and when they were presented in bank. Cheques issued for payment, but not presented for payment before June 30, 2015 as detailed below; Cheque No. 500500 Rs. 1, 000 Cheque No. 500510 Rs.2, 000 Cheque No. 500515 Rs.3, 000 Cheque No. 500518 Rs. 5,000 Bank statement Cash book Balances 24,750 18,000 Less: un-presented cheques Cheque No. 500500 Rs. 1, 000 Cheque No. 500510 Rs.2, 000 Cheque No. 500515 Rs.3, 000 Cheque No. 500518 Rs. 5,000 (-) 11, 000 <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 11. THE BASIS OF ACCOUNTING 2- Deposit in transit, uncollected cheques The deposit in-transit or uncollected cheques are the cheques which will be added in bank book but added in cash book and as and when the amount will be transferred from the bank of other branch or bank. Hence, the cheques which are in transit or uncollected are added in the column of bank statement. The reason of not showing in bank statement is deposit to near date of end date of statement or some reasons having objections wherein insufficient balance, wrong date, amount difference in figures and words and many other reasons. Cheque deposited into bank but not shown in bank statement or bank collection; No.130025 dt: 28/6 Rs.3000/= No.313454 dt: 29/6 Rs.2000/= No. 505352 dt: 30/6 Rs. 1500/= Bank statement Cash book Balances 24,750 18,000 Less: un-presented cheques Cheque No. 500500 Rs. 1, 000 Cheque No. 500510 Rs.2, 000 Cheque No. 500515 Rs.3, 000 Cheque No. 500518 Rs. 5,000 (-) 11, 000 Add: deposit-in-transit No.130025 DT: 28/6 Rs.3000/= No.313454 DT: 29/6 Rs.2000/= No. 505352 DT: 30/6 Rs. 1500/= (+) 6,500 <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 12. THE BASIS OF ACCOUNTING 3- Bank deductions such as collection charges, commission, excise duty, withholding tax, postage, cheque book charges, etc. On viewing bank statement, we ascertained that bank has deducted many charges in shape of collection charges, commission, excise duty, withholding tax, postage, cheque book charges, pay order making charges, demand draft making charges, on line transfer charges, etc. etc. if these charges are not recorded in cash book, we record them and they will reduce the balance of cash book. Bank deducted following charges during the month of June 2015 which are not shown in cash book; 10/6 Cheque Book charges 150/= 15/6 Bank commission Rs.100/= 16/6 Tax on Cash withdrawn Rs.50/= 25/6 on line transfer charges Rs.100/= (-) 400 Bank statement Cash book Balances 24,750 18,000 Less: un-presented cheques Cheque No. 500500 Rs. 1, 000 Cheque No. 500510 Rs.2, 000 Cheque No. 500515 Rs.3, 000 Cheque No. 500518 Rs. 5,000 (-) 11, 000 <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 13. THE BASIS OF ACCOUNTING Add: deposit-in-transit No.130025 dt: 28/6 Rs.3000/= No.313454 dt: 29/6 Rs.2000/= No. 505352 dt. 30/6 Rs. 1500/= (+) 6,500 10/6 Cheque Bookcharges150/= Less:Bank chargesand Tax 10/6 Cheque Book charges 150/= 15/6 Bank commissionRs.100/= 16/6 Tax on Cash withdrawnRs.50/= 25/6 on line transferchargesRs.100/= (-) 400 4- Bank collection not recorded in cash book. The bank collections such as bank interest on deposit, notes receivable, interest on notes receivable and bank interest on notes if shown in bank statement but not shown in cash book shall increase the balance of cash book. Bank collected following but not recorded in cash book. 20/6 Bank interest on deposit 100/= 25/6 notes receivable 1000/= 25/6 interest on notes receivable 50/= <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 14. THE BASIS OF ACCOUNTING Bank statement Cash book Balances 24,750 18,000 Less: un-presented cheques Cheque No. 500500 Rs. 1, 000 Cheque No. 500510 Rs.2, 000 Cheque No. 500515 Rs.3, 000 Cheque No. 500518 Rs. 5,000 (-) 11, 000 Add: deposit-in-transit No.130025 dt: 28/6 Rs.3000/= No.313454 dt: 29/6 Rs.2000/= No. 505352 dt: 30/6 Rs. 1500/= (+) 6,500 Less:Bank chargesand Tax (C. Book) 10/6 Cheque Book charges 150/= 15/6 Bank commissionRs.100/= 16/6 Tax on Cash withdrawnRs.50/= 25/6 on line transferchargesRs.100/= (-) 400 Add: Bank collection not record in C. Book 20/6 Bank interest on deposit 100/= 25/6 notes receivable 1000/= 25/6 interest on notes receivable 50/= (+) 1,150 <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 15. THE BASIS OF ACCOUNTING 5- Bank debit and credit not known Because of having on line most of the transactions, the amount could not be identified by some reasons and needs to be settled later but made the cause of increase and decrease in balance of bank book not in cash book. The difference of two balances may keep on temporary in bank reconciliation shortly and later on in suspense account as “unknown parties” and find out the difference of the matter. As soon they are identified must be moved to their right place. Bank can also debit the amount of any cheque of the other party wrongly in bank statement must be notified to bank for correction immediately. Less: unknown debit (Cash Book) Unknown debit shown in bank book) # 430449 18/6 Rs. 2000/= Add: unknown credit (in cash book) Unknown credit shown in bank book # 535383 28/6 Rs.1000/= # 494693 30/6 Rs.1500/= Bank statement Cash book Balances 24,750 18,000 Less: un-presented cheques Cheque No. 500500 Rs. 1, 000 Cheque No. 500510 Rs.2, 000 Cheque No. 500515 Rs.3, 000 Cheque No. 500518 Rs. 5,000 (-) 11, 000 Add: deposit-in-transit No.130025 dt: 28/6 Rs.3000/= No.313454 dt: 29/6 Rs.2000/= No. 505352 dt: 30/6 Rs. 1500/= (+) 6,500 <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 16. THE BASIS OF ACCOUNTING Less:Bank chargesand Tax (C .Book) 10/6 Cheque Book charges 150/= 15/6 Bank commissionRs.100/= 16/6 Tax on Cash withdrawnRs.50/= 25/6 on line transferchargesRs.100/= (-) 400 Add: Bank collection not record in C. Book 20/6 Bank interest on deposit 100/= 25/6 notes receivable 1000/= 25/6 interest on notes receivable 50/= 1,150 Less: unknown debit (Cash Book) Unknown debit shown in bank book) # 430449 18/6 Rs.2000/= (-) 2,000 Add: unknown credit (in cash book) Unknown credit shown in bank book # 535383 28/6 Rs.1000/= # 494693 30/6 Rs.1500/= 3,500 Corrected balance 20,250 20,250 BANK RECONCILIATION STATEMENT Balance as per cash Bank Statement 24,750.- Less: Un-present/out-standing cheques 11,000.- Add: Deposit-in-transit 6,500.- ---------- Balance as per Bank statement 20,250.- ====== <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 17. THE BASIS OF ACCOUNTING Balance as per Cash book 18,000.- Less: Bank charges 350 + 50 Tax - 400.- Add: Bank interest on deposit 100- Notes receivable 1,000.- Interest on notes receivable 50 Less: Unknown debit -2000 Add: Unknown credit 3500 -------- Balance as per Cash book 20,250 ====== The journal entries of the amount that could not be shown in ledger account must be recorded in order to match balances with cash book and bank book and provide balance for issuing cheques. Adjusting Entries; Bank charges 350 Tax on cash withdrawn 50 Bank 400 Bank 1,150 Bank profit 100 Notes receivable 1000 Interest on notes receivable 50 Unknown parties 2000 Bank 2000 Bank 3500 Unknown parties 3500 <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 18. THE BASIS OF ACCOUNTING ACCRUAL BASE ACCOUNTING In accrual base accounting, transactions are recorded in ledger under journalizing and as when they transact and reported in income statement when they earned or occurred of the period that closes accounting. Now, the cash received or paid will have no concern with revenues and expenses but receivable and payable which is the result of accrual base accounting. As far as usually expenses are concerned, the accrual of them daily is not in practice. Now, this question can be arisen that will the profit cover the transaction of the date? The answer will be no, then the accrual base accounting need to accrue all transactions on accrual basis if we require profit and loss and balance sheet on daily basis. CASH AND ACCRUAL BASE MIX ACCOUNTING In cash base accounting cash is received or paid against transactions as and when they occurred and in accrual base accounting, the journal entry of the transactions is recorded as and when it occurred before cash receipt and payment. In cash and accrual mix base accounting, usually cash is received or paid against transactions but the transactions relate to receivable or payable are journalized and remaining transactions of the date of accounting period are recorded at the time of closing accounts. It is up to entity’s requirement that it adopts the system among cash, accrual and mix accounting system. <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 19. THE BASIS OF ACCOUNTING CASH FLOW STATEMENT Generally, the income statement and balance sheet are prepared under accrual basis of accounting but the cash flow statement is one of the main financial statements among balance sheet, income statement and statement of stock holders’ equity which reports the cash generated or actual cash-like assets from operating, investing and financial activities used during the time interval. The cash flow statement includes only inflows and outflows of cash and excludes transactions that do not directly affect cash receipts and payments. The cash flow statement is the reconciliation of opening balance of cash and closing balance of cash and cash equivalent at the beginning of the period and ending of the period. The cash flow statement bases on cash report on three types of financial activities: operating activities, investing activities and financing activities. <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 20. THE BASIS OF ACCOUNTING 1- OPERATING EXPENSES Operativeactivities include production, sales and delivery of the company’s product as well as collecting payment from its customers. These activities usually deal with current assets and current liabilities and include; Cash receipts from customers Cash paid to suppliers for goods and services Cash paid to employees/Accrued wages Interest paid (can be reported under financial activities in IAS 7) Income tax paid The receipts are reduced from payments. 2- INVESTING ACTIVITIES The investing activities deal with sales and purchase of fixed assets and long term investment as well as any return of investment like dividend and interest receipt and may include; Purchase of fixed assets (actual cash paid) Sale of fixed assets (accrual cash received) Interest received on investments (actual cash received) Dividend received (actual cash received) Dividend paid (actual cash paid) <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 21. THE BASIS OF ACCOUNTING 3- FINANCIAL ACTIVITIES The financial activities involve in shareholder’s equity and long term liabilities as well as dividend received and interest paid over it and may have; Issue of share capital (actual cash received) Issue of debenture (actual cash received) Cash received from long term loans (actual cash received) Payment of dividends (actual cash paid) Payment of long term loans (actual cash paid The balance sheet and income statement are the sourceof making cash flow statement and enterprises can reportcash flows fromoperating activities using direct method or indirect method. 1- DIRECT METHOD Direct method reports major classes of gross cash receipts and gross cash payments as actual. DIRECT METHOD Cash flowfrom operations xxxxx Cash flow from investing (xxxx) Cash flow from financing (xxxx) -------- Net Cash flow xxxx ===== <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 22. THE BASIS OF ACCOUNTING EXAMPLE: The cash flow statement under direct method is prepared as given balance sheet and income statement. BALNACE SHEET ASSETS 2013 2014 LIABILITIES 2013 2014 Cash & equivalents 4000 5000 Accounts payable 13000 15000 Accounts Receivable 7000 10000 Accrued Wages 2000 3000 Inventory 12000 15000 Accrued taxes 3000 2000 ------------------ ------------------ Total Current Assets 23000 30000 Total Current Liabilities 18000 20000 Net fixed assets 40000 40000 Long term debts 20000 20000 Common Stock 10000 10000 Retained earnings 15000 20000 ------------------ ------------------ 63000 70000 63000 70000 ============ ============ <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 23. THE BASIS OF ACCOUNTING INCOME STATEMENT 2014 Sales 85000 Cost of goods sold 50000 Operating Expenses 15000 Depreciation 3000 Interest 2000 70000 ------- -------- Net income before taxes 15000 Income tax -10000 --------- Net income 5000 ===== - Cash flow statement direct method - Find out net profit from balance sheet - Cash flow statement indirect method - Statement of changes in working capital - Funds Flow Statement <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 24. THE BASIS OF ACCOUNTING CASH FLOW STATEMENT - DIRECT METHOD Cash flows from operating activities ---------------------------------------------------- Cash received from customers (C-1) + 82000 Less: Cash paid to creditors (C-2) - 51000 Less: Cash paid for expenses (C-3) - 14000 ------- Cash generated from operation 17000 Less: Income tax paid (C-4) - (11000) ------- Net cash generated from operating activities 6000 Cash flows from investing activities Purchase of fixed assets (C-5) - 3000 Net cash used by investing activities (3000) Cash flows from financing activities Interest paid -2000 Net cash used by financing activities (2000) -------- Increase in net cash during the period 1000 Add: Cash and cash equivalent at beginning of period 4000 ------- Cash and cash equivalent at ending of period 5000 ==== DIRECT METHOD Cash flowfrom operations 6000 Cash flow from investing (3000) Cash flow from financing (2000) -------- Net Cash flow 1000 ===== <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 25. THE BASIS OF ACCOUNTING Calculation 1 – Cash received from customer Opening balance of a/c receivable 2013 7000 Add: Sales 2014 85000 --------- Total Credit sale 92000 Less: closingbalance of a/c receivable 2014 10000 --------- Cash (balancing) 82000 ====== Calculation 2 – Cash paid to creditors Inventory account Opening balanceof Inventory 2013 12000 Less: Inventory 2014 15000 ------- Increase in inventory 3000 Add: Cost of goods sold 2014 50000 ------- Purchases (balancing) 53000 ===== Account payable account Opening of account payable 2013 13000 Add: Purchases 53000 ------- 66000 Less: closing of account payable 2014 15000 ------- Cash (balancing) 51000 ===== <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 26. THE BASIS OF ACCOUNTING Calculation 3 - Cash paid for expenses Opening of accrued expenses 2013 2000 Add: Operating Expenses 15000 ------- Total expenses 17000 Less closing of accrued expenses 2014 3000 ------- Cash (balancing) 14000 ====== Calculation 4 – actual tax paid Opening of accrued expenses 2013 3000 Add: tax paid for the year 2014 10000 ------- Total taxes 13000 Less: closing of accrued taxes 2000 ------- Cash (Balancing) 11000 ===== Calculation 5 – Fixed assets purchased or sold Opening of fixed assets 2013 40000 Add: depreciation 3000 Less: Closing of fixed assets 2014 (-) 40000 ------- Cash (Balancing) 3000 ===== - Calculation 6- Net profit before Retained earnings (closing) 20000 Less: Retained earnings (opening) (15000) --------- 5000 Add: Interest expense for the period 2000 Income tax for the current period 10000 ------- Income before tax and interest 17000 <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 27. THE BASIS OF ACCOUNTING <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 28. THE BASIS OF ACCOUNTING INDIRECTMETHOD Indirectmethod converts actual bases net income or loss into cash flow by using a series of additions and deductions changing in operating activities reporting increaseand decrease in assets and liabilities. Operating Activities o Net profitbefore interest and tax o Adjustment(non cash item) Add in net profit Depreciation Bad debt expenses Amortization of goodwill, patent or intangible assets Amortization of discounton debenture or share Loss on sale of fixed assets Less in net profit Gain on sale of fixed assets Dividend and interest received on investment The result of addition and deletion in net profit (Assets & Liabilities o Increase in current Assets (except cash/bank) o Decrease in current assets (except cash/bank) o Increase in current liabilities (except tax, interest & dividend p/a) o Decrease in current liabilities (except tax, interest & dividend p/a) <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 29. THE BASIS OF ACCOUNTING Cash flows from operating activities Net profit before interest & tax (C-1) 17000 Adjustment for: (non-cash items) Add: Depreciation 3000 ------- Operating profit 20000 Increase in Accounts receivable (3000) Increase in inventory (3000) Increase in accounts payable 2000 Increase in accrued wages 1000 -3000 -------- ------ Net cash generated from operating activities 17000 Less: Income Tax paid (C-2) -11000 --------- Net cash generated from operative activities 6000 Cash flows from Investing Activities Purchase of fixedassets (3000) Net cash used by investing activities (3000) Cash flows from financing activities Interest paid (2000) Net cash used by financing activities (2000) ------- Increase in net cash during the period 1000 Add: Cash and cash equivalent at beginning of period 4000 Cash and cash equivalent at ending of period 5000 ===== <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 30. THE BASIS OF ACCOUNTING FUNDS FLOW STATEMENT: The prior use of fund flow statement has been converted into cash flow statement under IAS 7 (Revised 1992) International standard of presenting financial statement. The fund flow statement is based on accrual base accounting which represents the cash and cash equivalent in funds flow analysis. Fund = working capital = current assets - current liabilities SOURCES OF FUNDS Net profit before interest & tax (C-6) 17000 Adjustment of (non-cash items) Add: - Depreciation + 3000 Income from business operation 20000 APPLICATION OF FUNDS Tax paid -11000 Purchase of fixed assets (C-5) -3000 Interest paid -2000 Net increase in working capital -16000 Net increase in working capital 4000 ===== <THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<aqeelraza@live.com>

- 31. THE BASIS OF ACCOUNTING All accounting functions are based on payments and receipts and it is up to the requirement of an entity to adopt cash base accounting systemwherein cash payments and receipt are made at same time and in accrual base accounting system requires accruing all payments and receipts before payment and receipt or payment receipt may differ in time but in cash base accounting may require accruals at the time of finalization of accounts. The cash flow and fund flow statements are made under comparison of balance sheet and income statement and they were prepared under accrual base accounting based on paid and received cash. The cash base accounting can be better for small businesses but in the business like share business, partnership business etc. wherein the capital of public is involved accrual base accounting may be adopted for actual position of funds to be paid or to be received. WRITER’S VIEW WRITTEN BY: SYED AQEEL RAZA MASTER OF COMMERCE & POLITICS