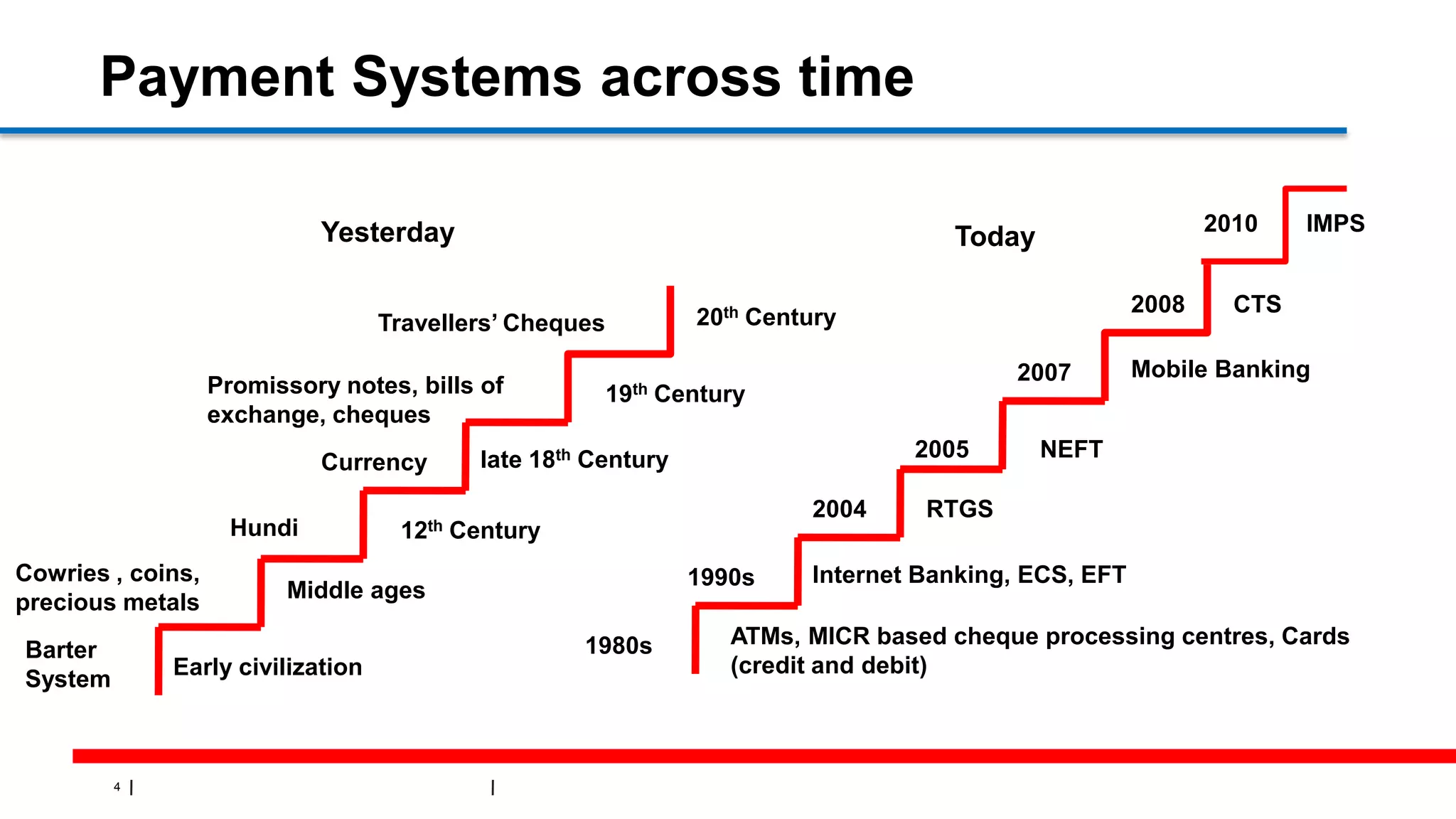

This document provides an overview of payment systems in India, including existing systems like ECS, NEFT, RTGS and emerging mobile payment systems like IMPS. It defines key payment system stakeholders and classifications. Specific sections describe the process, advantages and disadvantages of IMPS mobile payments. Comparisons are made between IMPS and other electronic payment methods. The document also discusses future payment trends focused on increasing convenience, affordability, confidence and consumer protection in digital financial services.

![16

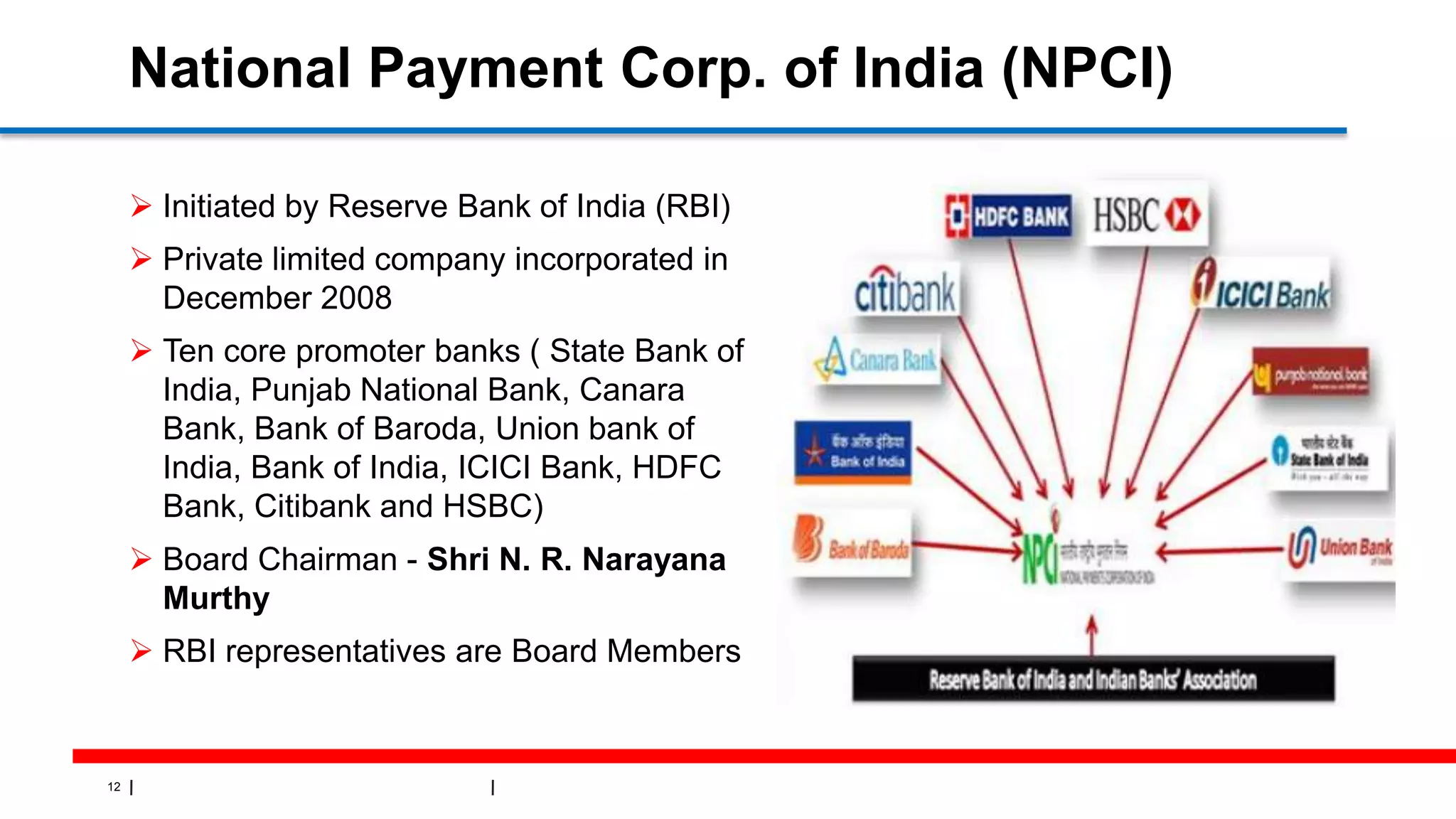

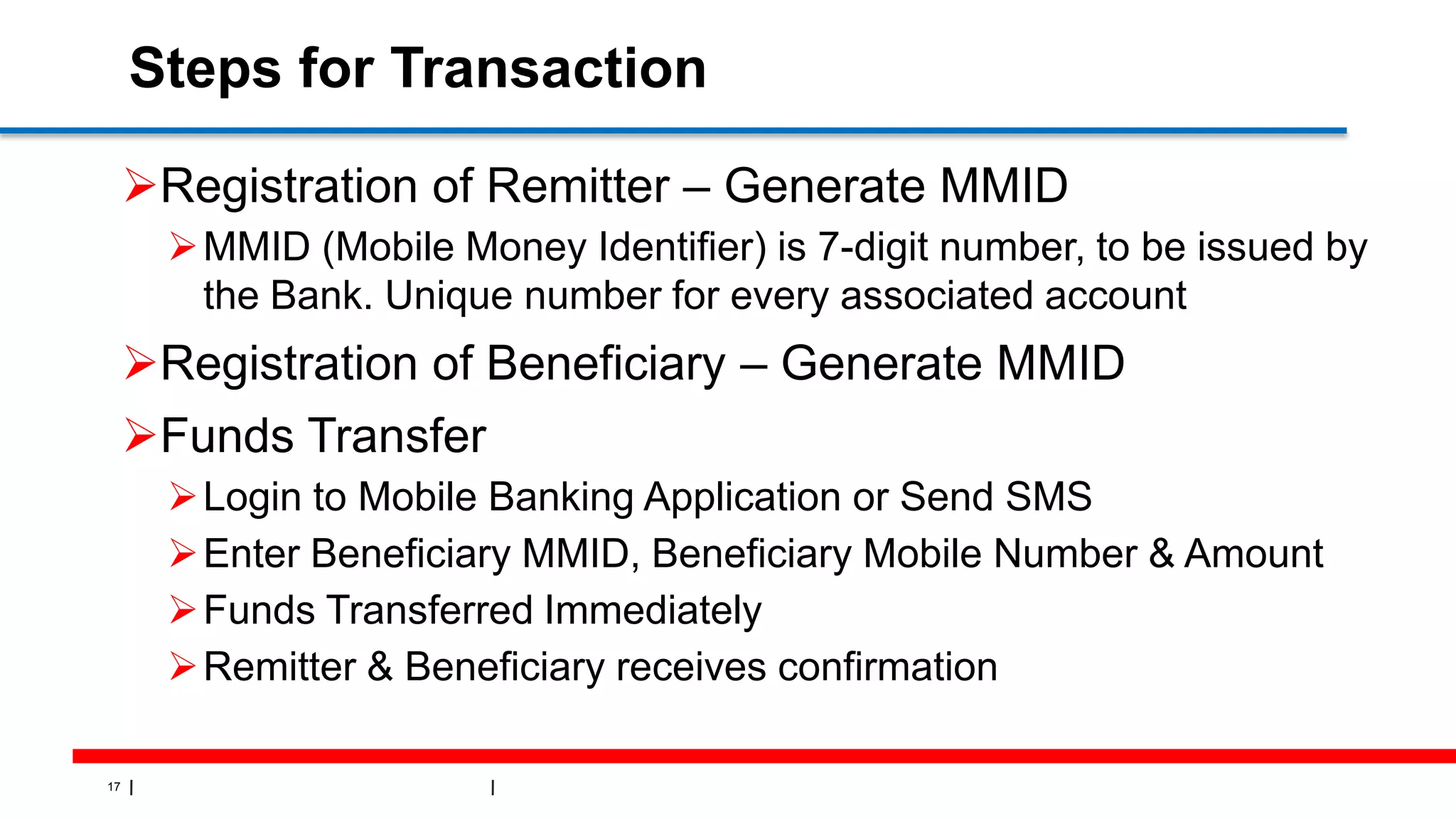

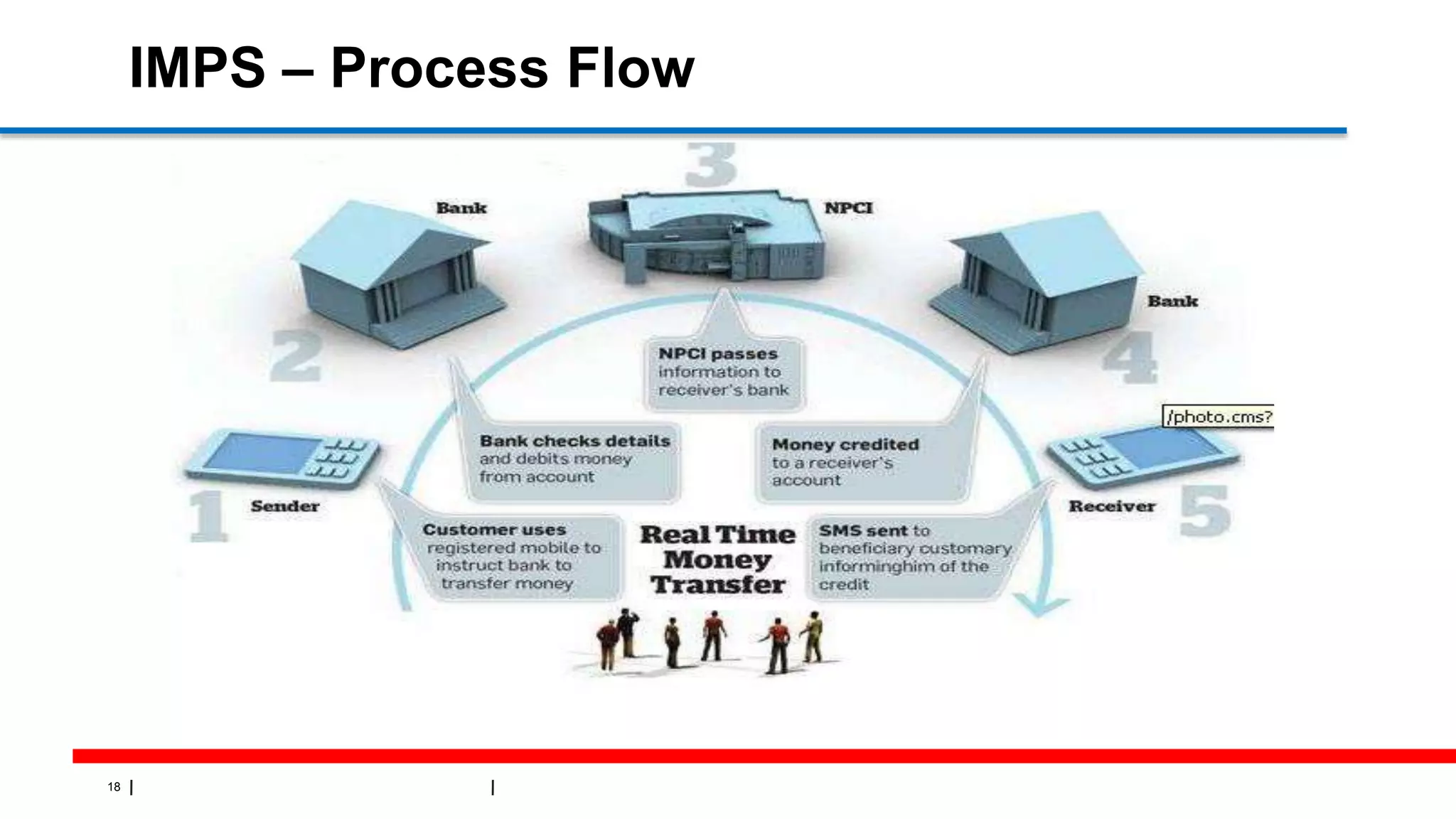

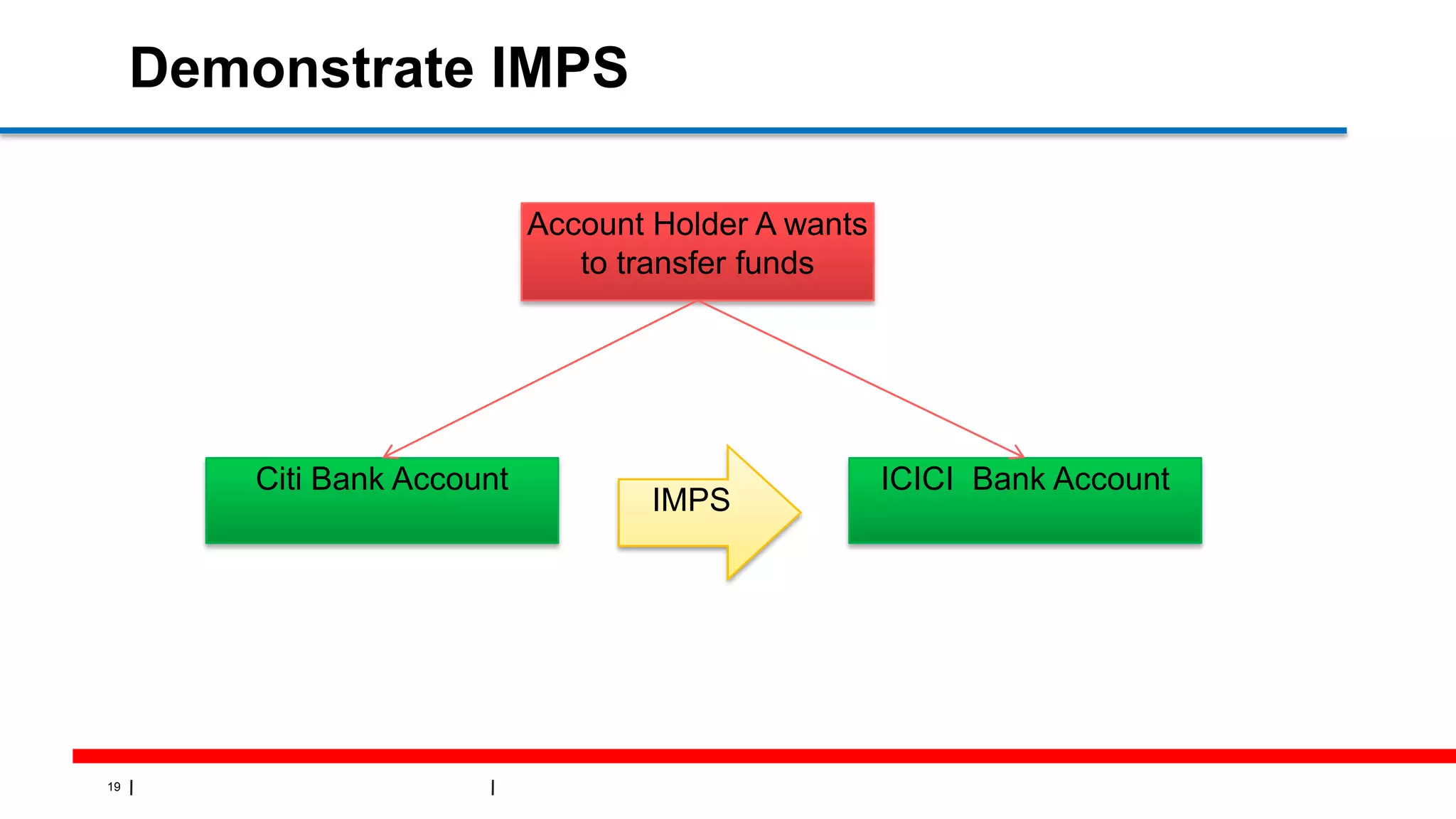

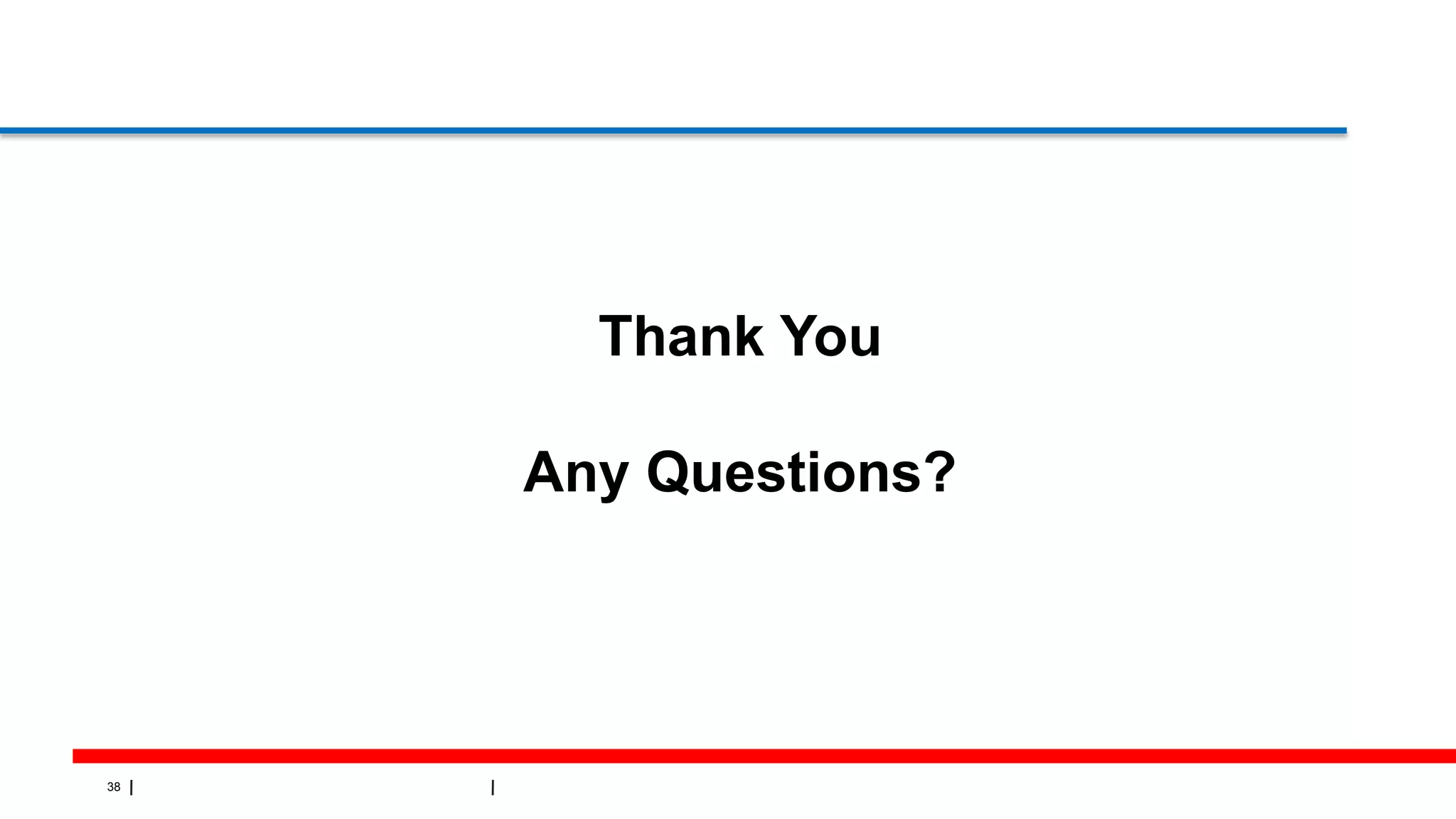

Modes of Transfer

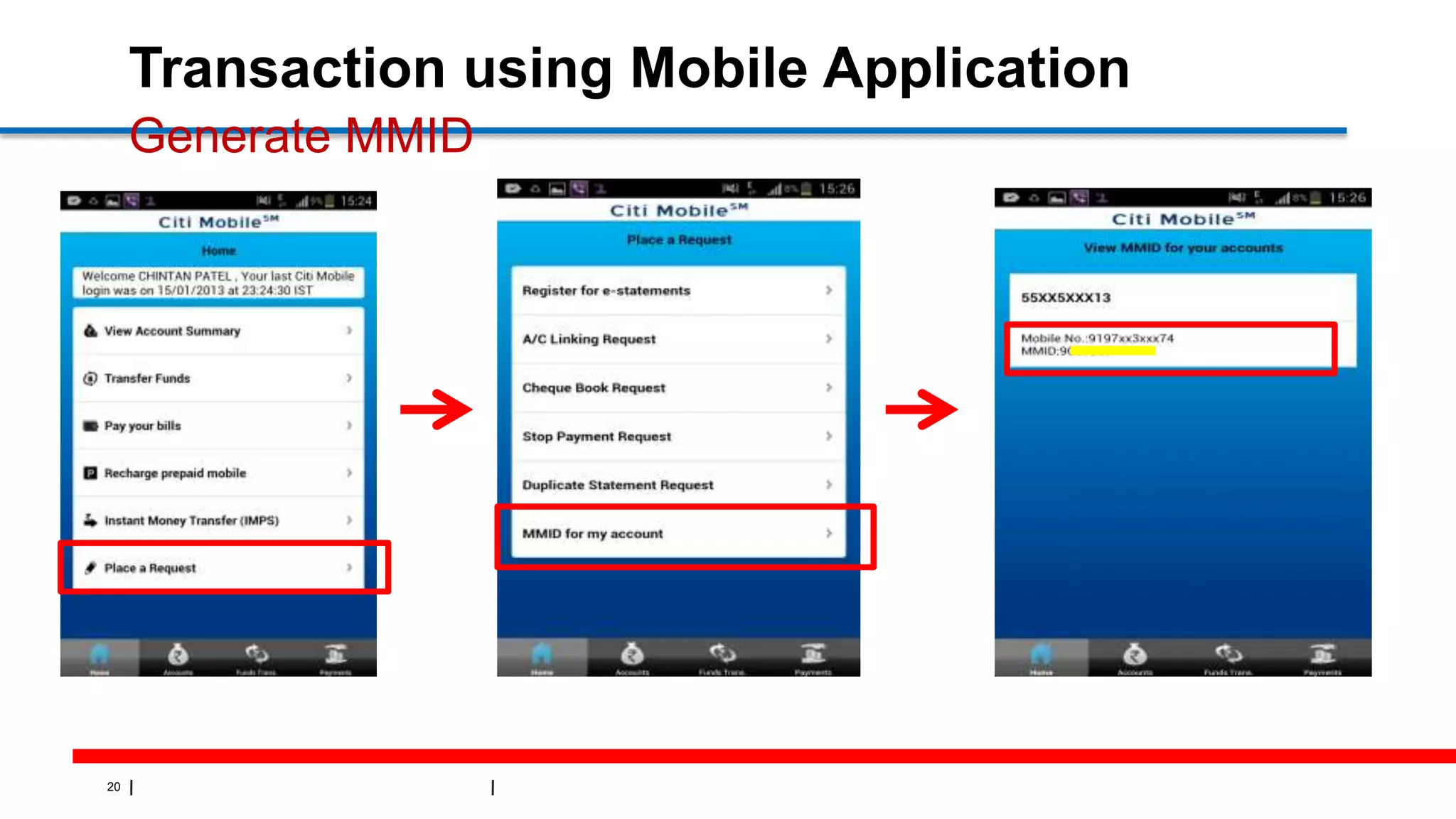

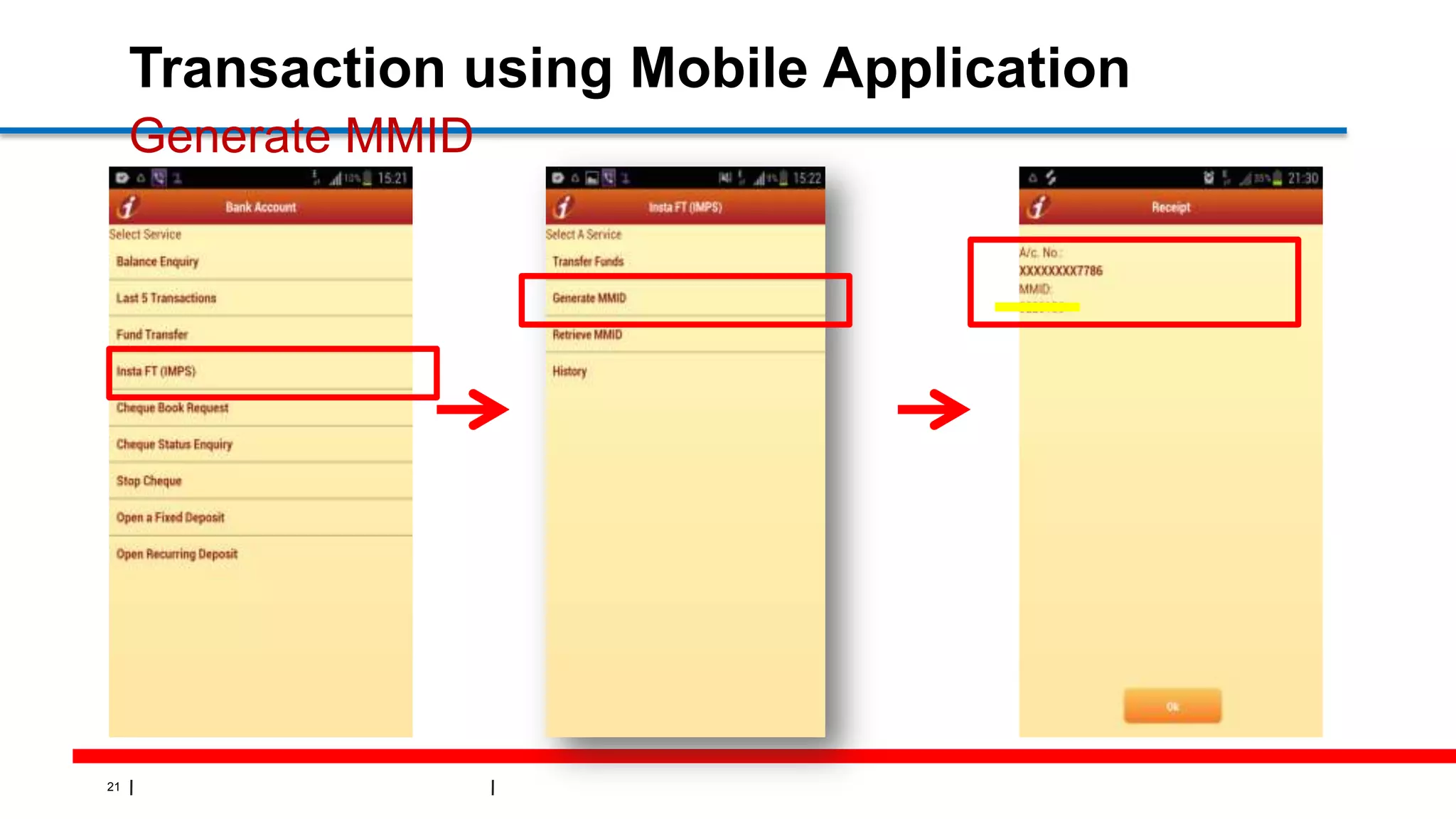

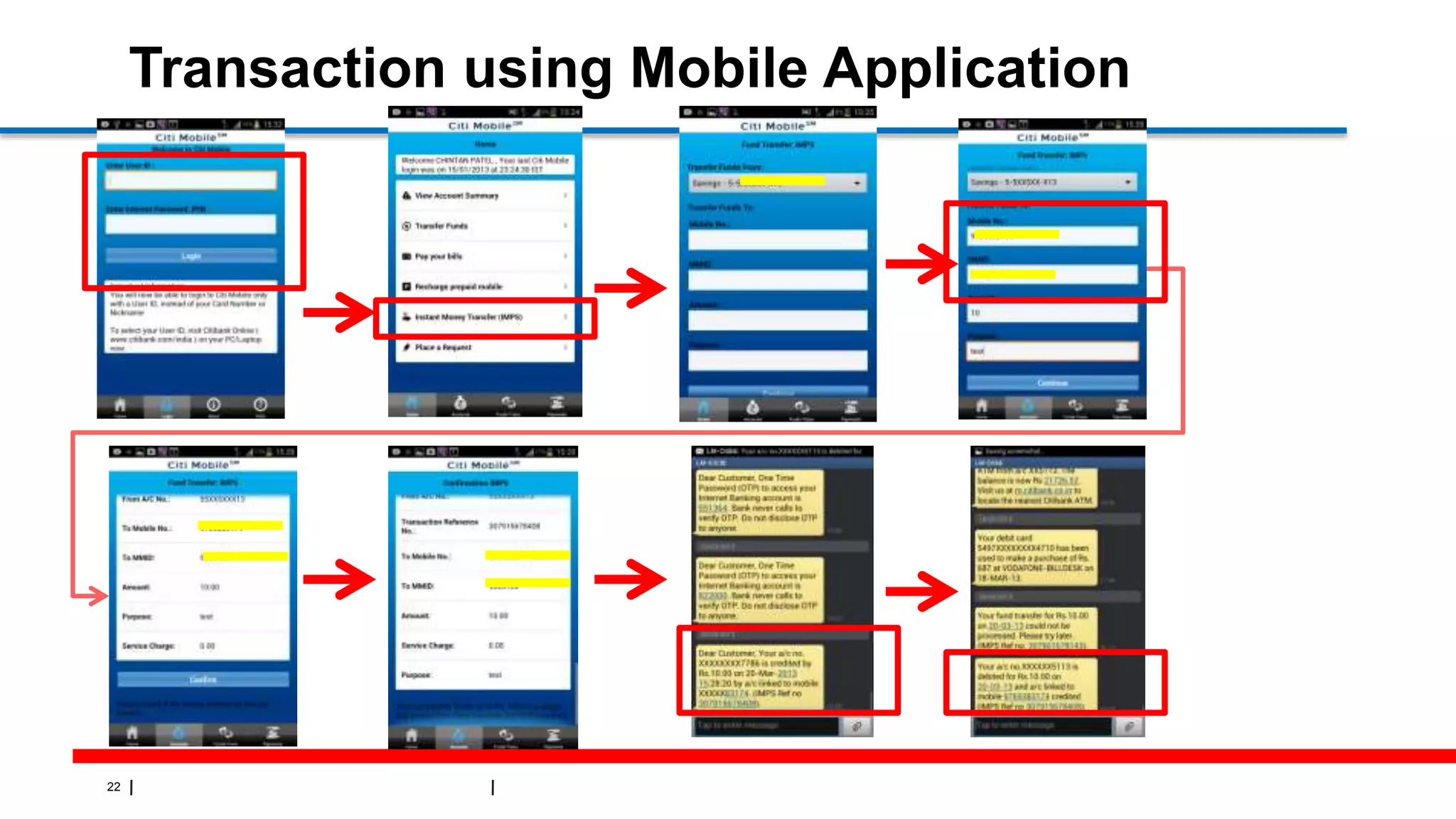

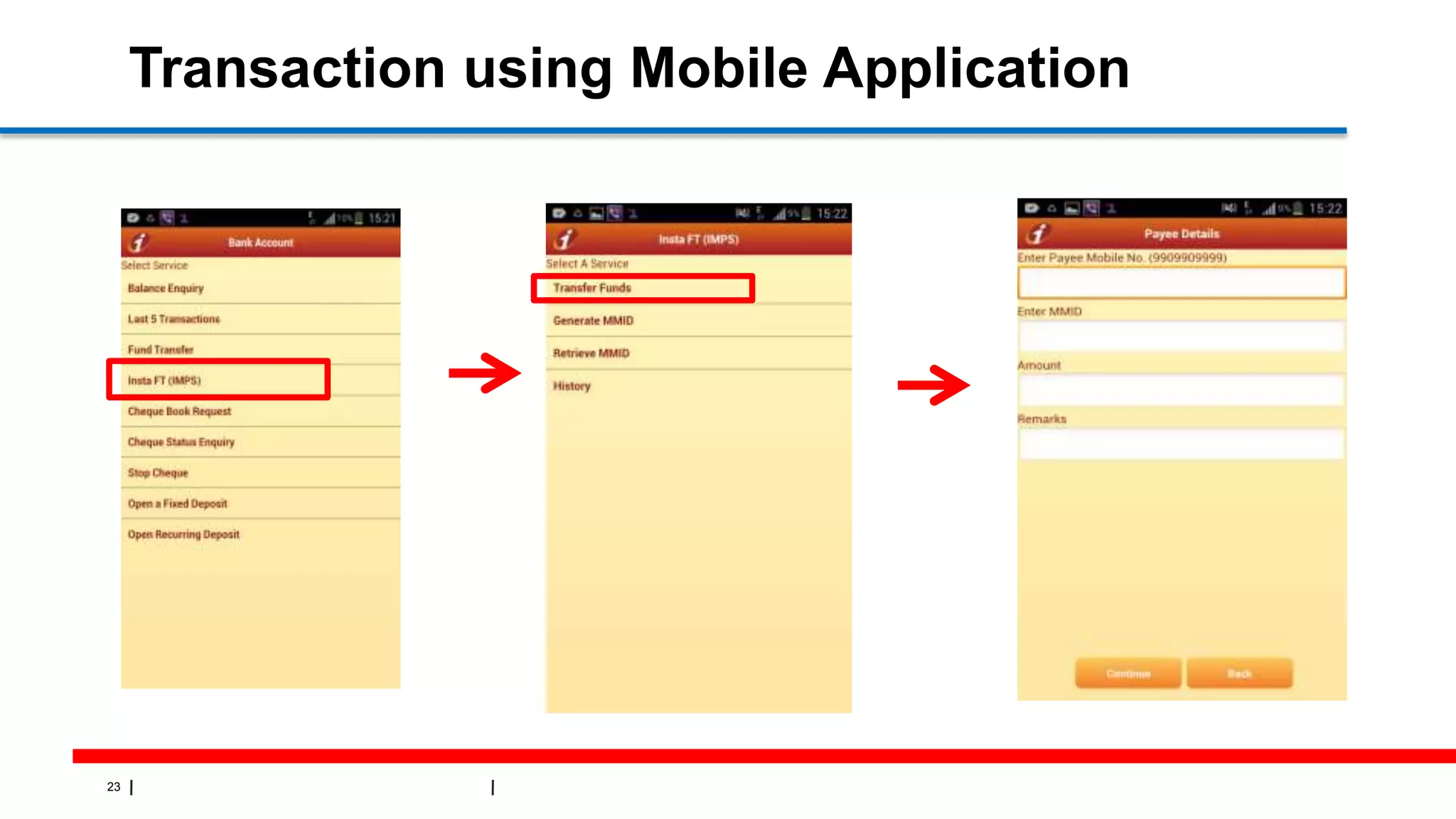

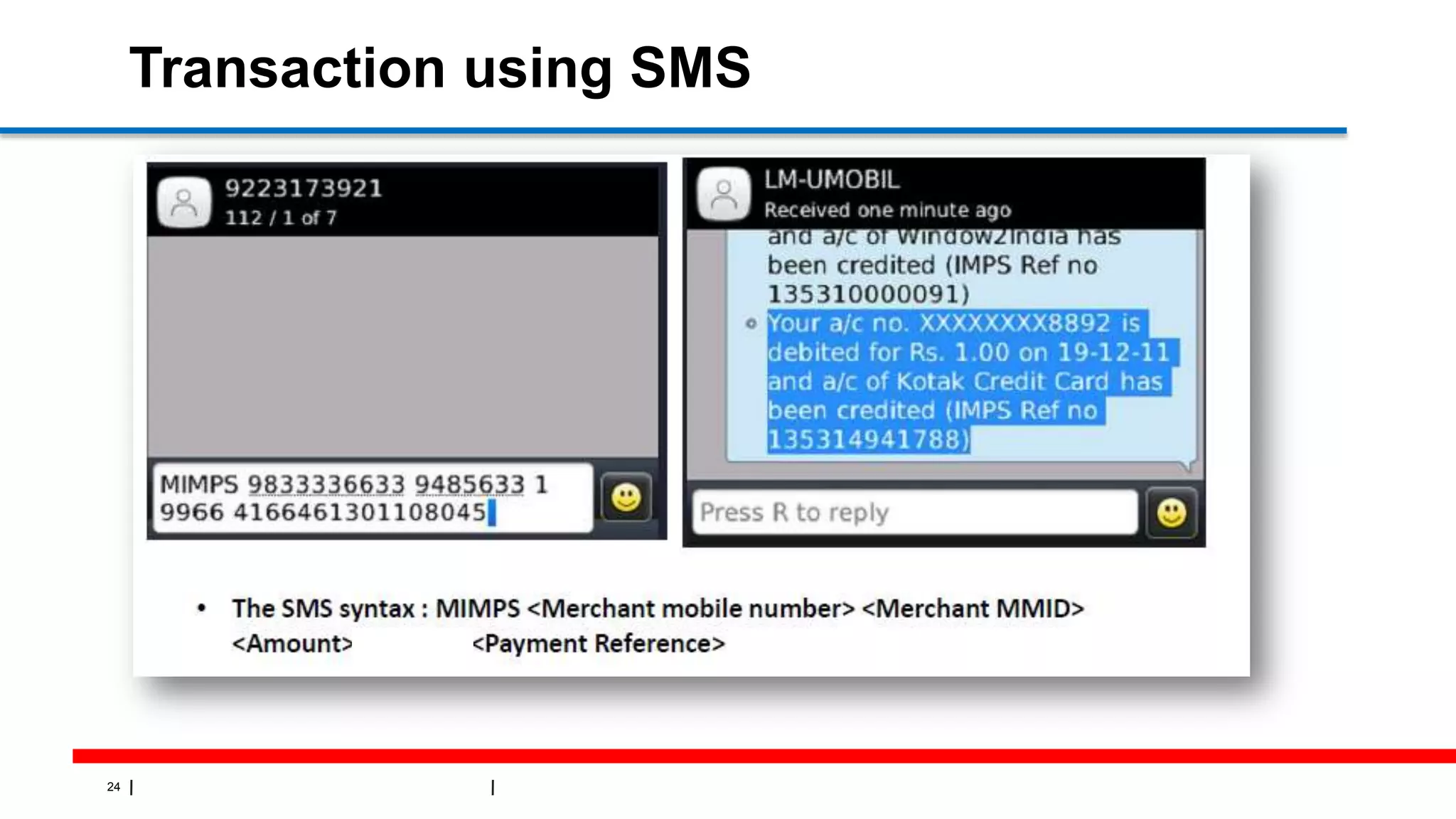

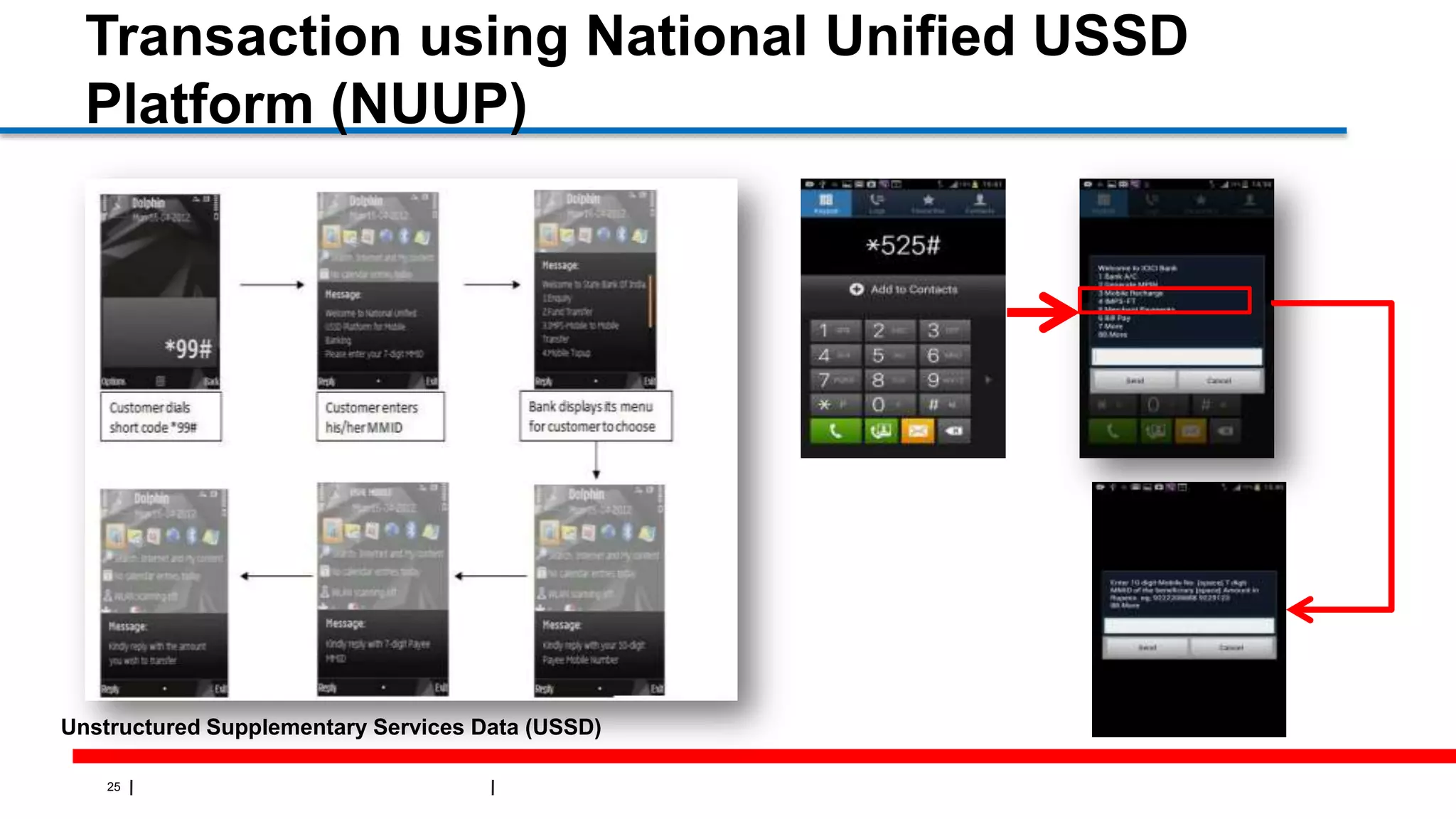

Funds Transfer using Mobile

Using Mobile Application

Using SMS

Using National Unified USSD Platform (NUUP)

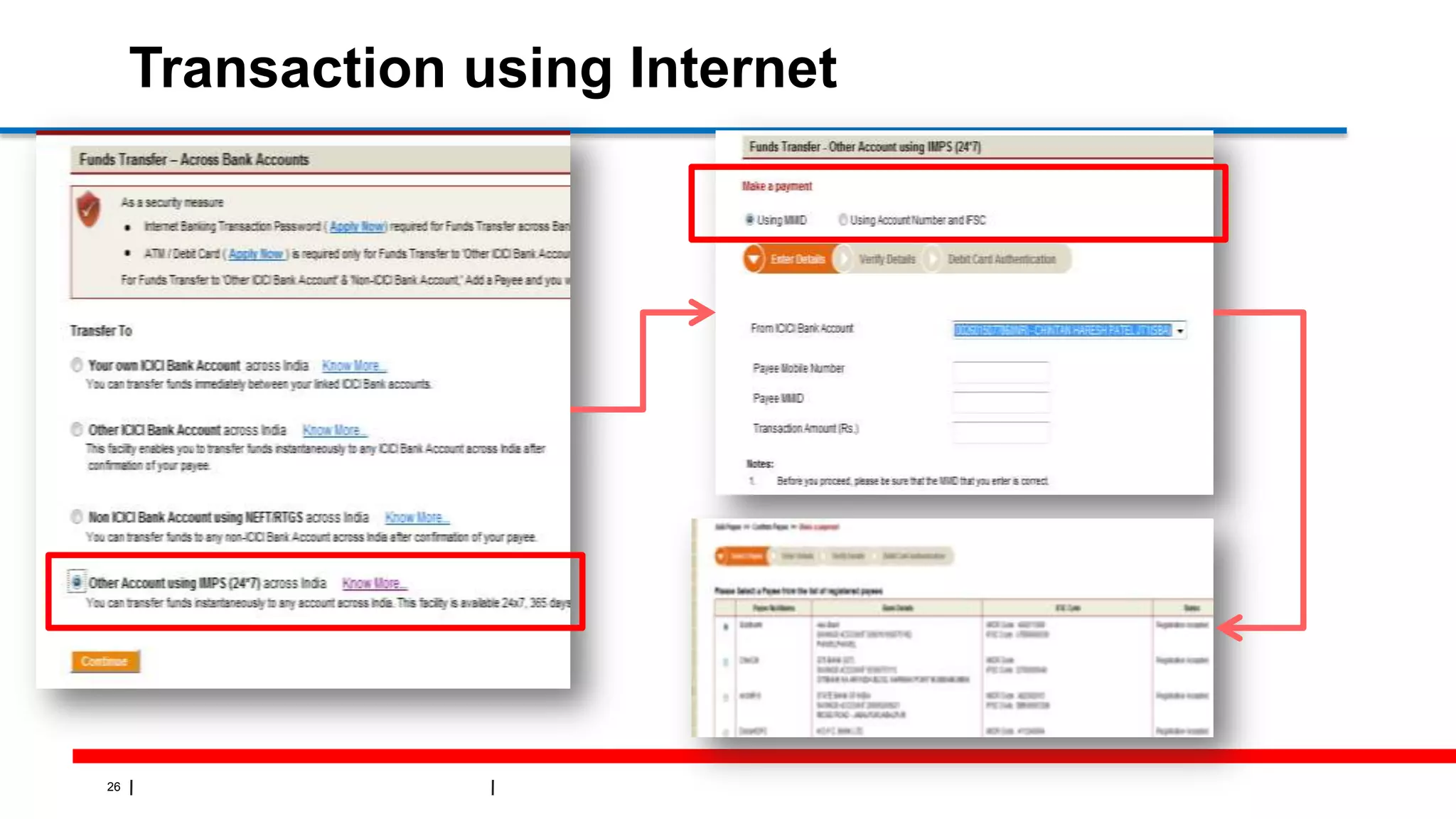

Funds Transfer using Internet

To Account registered to IMPS

To Account not registered to IMPS (Using Indian Financial System Code[IFSC])

Funds Transfer through ATM

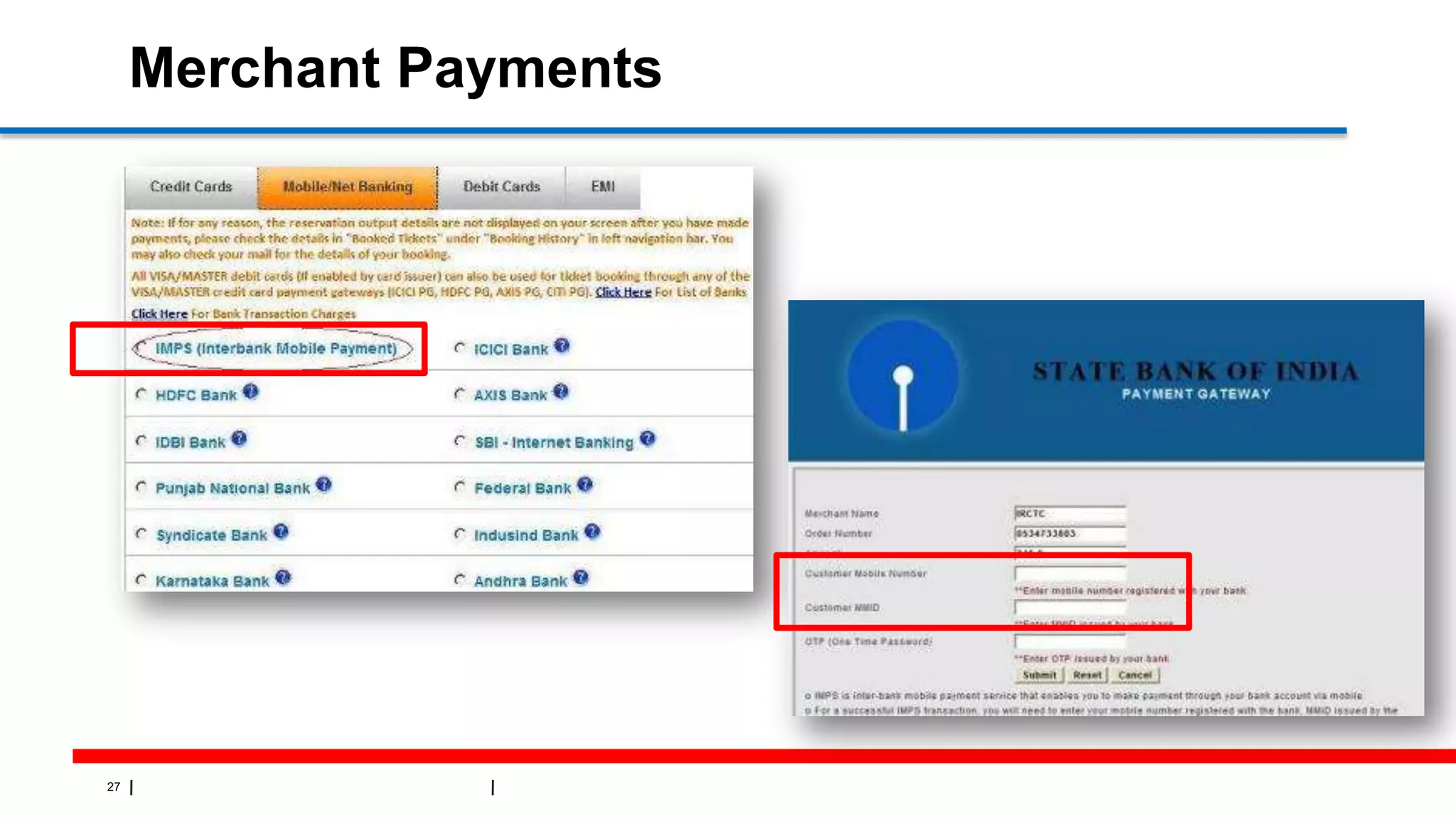

Merchant Payments through Internet – Using OTP](https://image.slidesharecdn.com/paymentsimps-130426083335-phpapp01/75/Payments-Systems-IMPS-Mobile-Payments-16-2048.jpg)

![Electronic fund trasfer [Mahak Dhakar]500048604](https://cdn.slidesharecdn.com/ss_thumbnails/electronicfundtrasfermahakdhakar500048604-171121150058-thumbnail.jpg?width=640&height=640&fit=bounds)