Camels framework

•Download as PPTX, PDF•

0 likes•575 views

Financial ratios involved in CAMELS framework

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Camels framework

Similar to Camels framework (20)

More from yogesh ingle

More from yogesh ingle (20)

Recently uploaded

Recently uploaded (20)

Camels framework

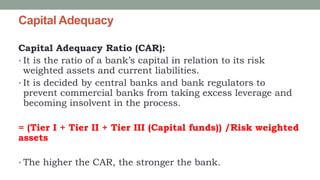

- 1. Capital Adequacy Capital Adequacy Ratio (CAR): • It is the ratio of a bank’s capital in relation to its risk weighted assets and current liabilities. • It is decided by central banks and bank regulators to prevent commercial banks from taking excess leverage and becoming insolvent in the process. = (Tier I + Tier II + Tier III (Capital funds)) /Risk weighted assets • The higher the CAR, the stronger the bank.

- 2. 1. Tier I Capital: Actual contributed equity plus retained earnings. 2. Tier II Capital: Preferred shares plus 50% of subordinated debt. 3. Tier 3 capital: Debts may include a greater number of subordinated issues, undisclosed reserves and general loss reserve 4. Risk Weighted Assets (RWA) comes from the Basel Norms for regulating Bank's capital requirement for managing credit risk. The riskiness also varies on the basis of type of loan. So these assets are given different weightage based on there riskiness to arrive at Risk Weigtage Assets

- 3. Debt equity ratio: It indicates how much of the bank business is financed through debt and how much through equity. • Debt – Equity ratio = Borrowings_______ X 100 Share capital + Reserves Higher ratio indicates less protection for the creditors and depositors in the banking system.

- 4. • Advances to assets: This ratio indicates a bank’s aggressiveness in lending which ultimately results in better profitability. Total advances also include receivables. =Total Advances/Total Asset The higher the ratio indicates aggressiveness of bank in lending advances .

- 5. • Government Securities to Total Investments • The risk held in the investments of banks is reflected by this ratio. • It is assumed that Government securities are most secured and risk free debt instruments . = Government Securities / Total Investments • It means higher the investment in government securities will result in lower risk and vice versa

- 6. • Coverage ratio The Coverage ratio measures the availability of capital to meet risk of loss asset. = Total Assets/ Total Debt As a rule of thumb, utilities should have an asset coverage ratio of at least 1.5,

- 7. Assets Quality • Gross NPAs to Gross Advances ratio (%): Gross NPAs X 100 Gross Advances • Net NPA to Total Assets (%): Gross NPAs- Provisions X 100 Total Assets • Total Investments to Total Asset • Standard Advances to Total Advance

- 8. Management Efficiency Business Per Employee :This tool measures the efficiency of all the employees of a bank in generating Business for the bank. Sum of total deposits and total advances X 100 No. of employees Profit per Employee: This ratio measures the efficiency of employees at the branch level Net profit X 100 No. of employees

- 9. • Credit (Advances) Deposit Ratio: • The ratio measures the efficiency of management in converting the deposits available with the bank (excluding other funds like equity capital, etc.) into high Earning advances. • Total deposits include demand deposits, savings deposits; term Deposits and deposits of other banks. Total advances also include the receivables. • Return On Net Worth (%) = Net Income / Shareholders’ Equity

- 10. EARNING QUALITY • Return On Assets: • NIM to Total Assets (%) : A higher spread indicates the better earnings given the total assets. Interest income includes dividend income and interest expended included interest paid on deposits, loan from the RBI, and other short-term and long term loans • Operating Profit to Total Assets: • Interest Income to Total Income :

- 11. LIQUIDITY • Liquid Assets to total Assets (%) • Government securities to Total Assets (%) • Liquid Assets to Total Deposits (%) • Liquid Assets to Demand Deposits (%): It measures the balance at banks and RBI. Balance at Bank includes cash in hand (including foreign currency notes) balance with RBI include current account, other account. The Total assets include the revaluation of all the assets