Downloaded 703 times

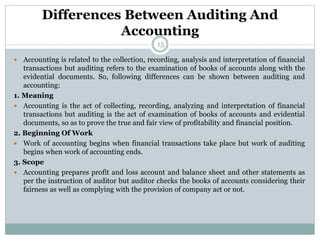

The document provides a comprehensive overview of auditing, detailing its definition, origins, development, and significance in ensuring reliable financial information for decision-making. It discusses the differences between auditing and accounting, highlights the qualities required in an auditor, and outlines the objectives and types of audits. Additionally, it addresses errors and frauds in accounting, the advantages of audits, and the regulatory framework surrounding them.