Downloaded 1,060 times

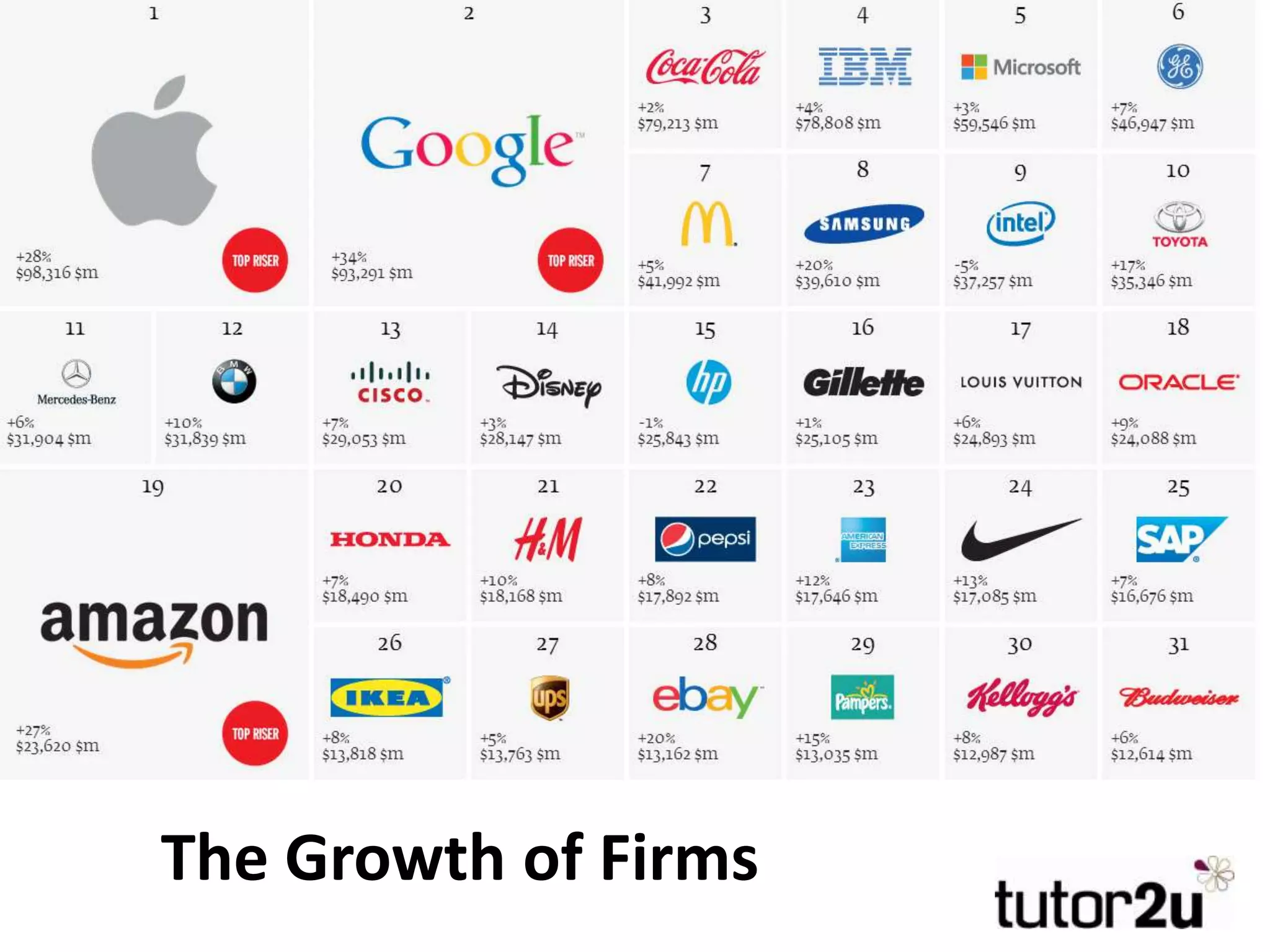

This document discusses various strategies that firms use to grow, including organic growth from within the business and external growth through mergers and acquisitions. It defines different types of integration like horizontal, vertical, and lateral integration. It provides examples of mergers and acquisitions in different industries. It also discusses the motives behind M&A activity including strategic, financial, and managerial motives. It notes potential advantages and drawbacks of acquisitions and the importance of successful integration. Other growth strategies like joint ventures and de-mergers are also covered.

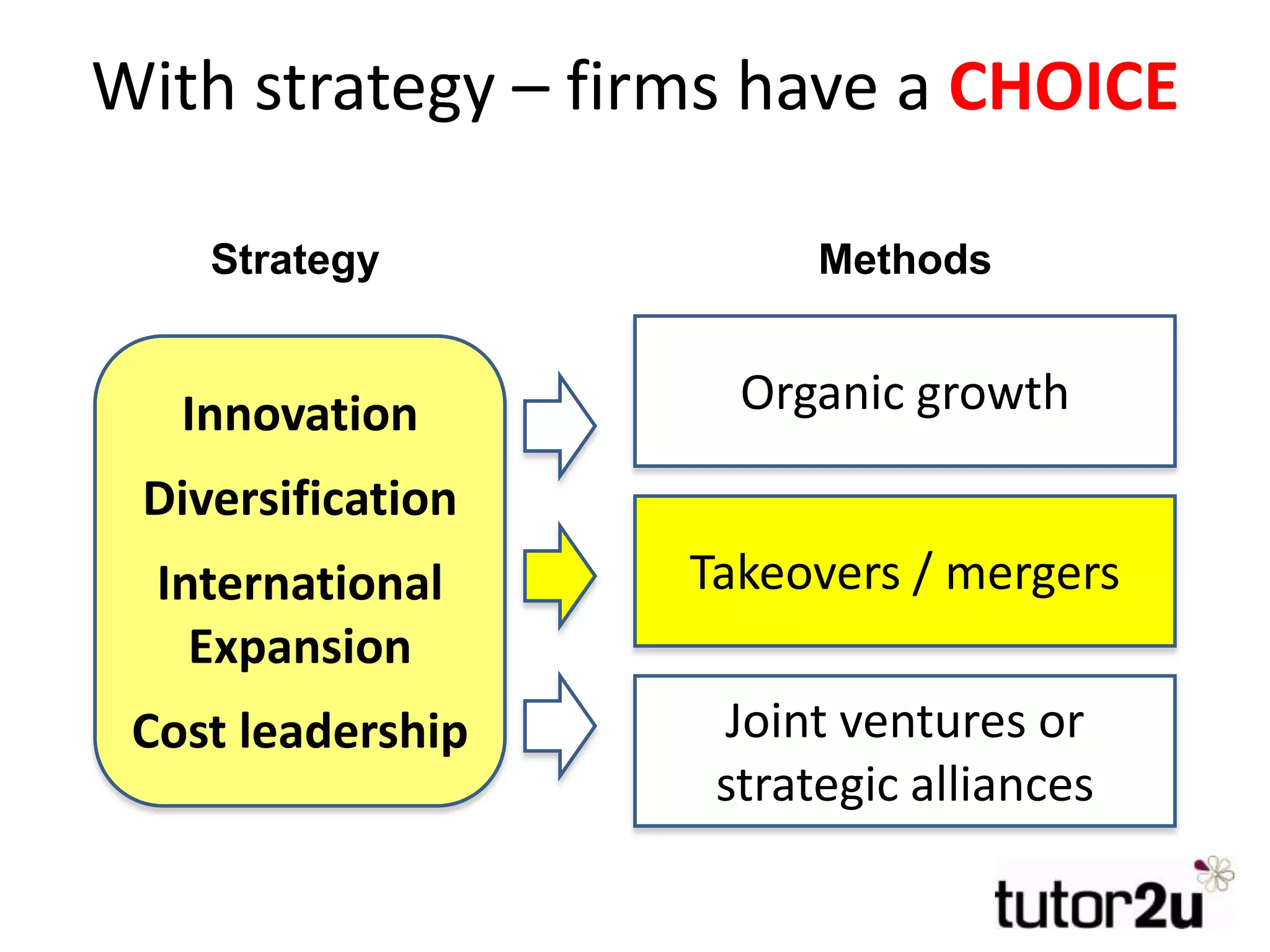

Introduction to organic and external growth strategies, emphasizing varying methods like innovation, diversification, and market expansion.

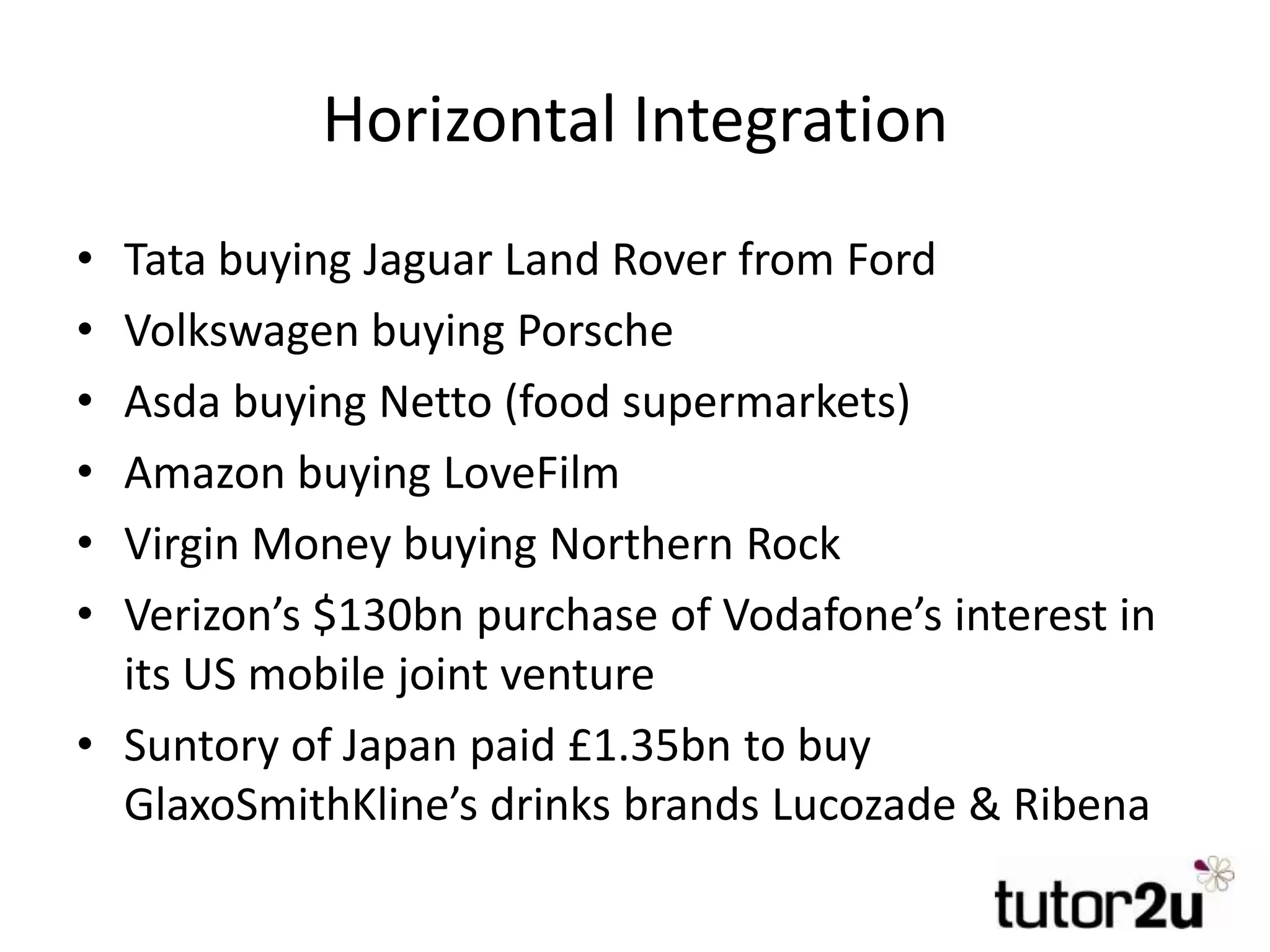

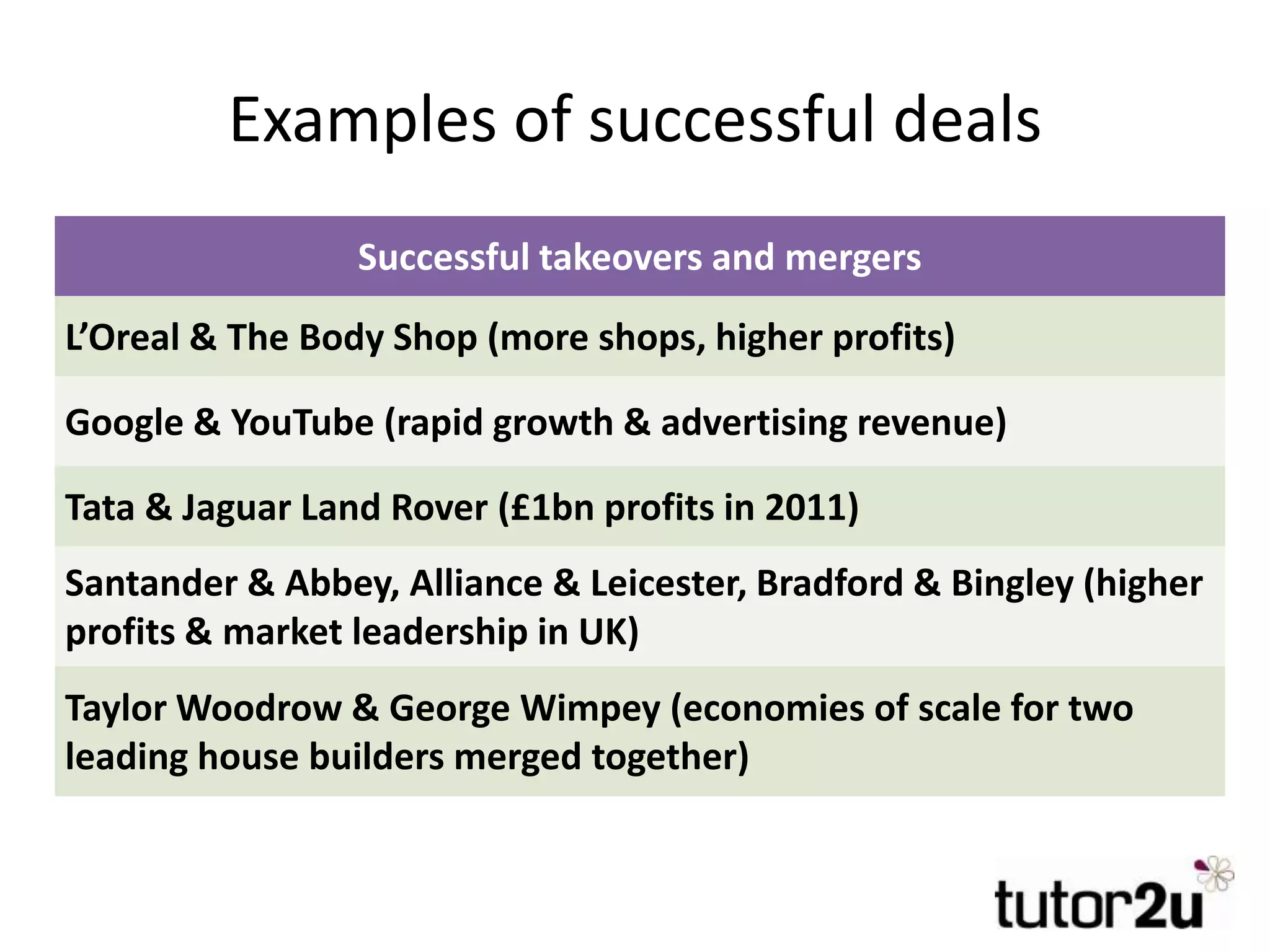

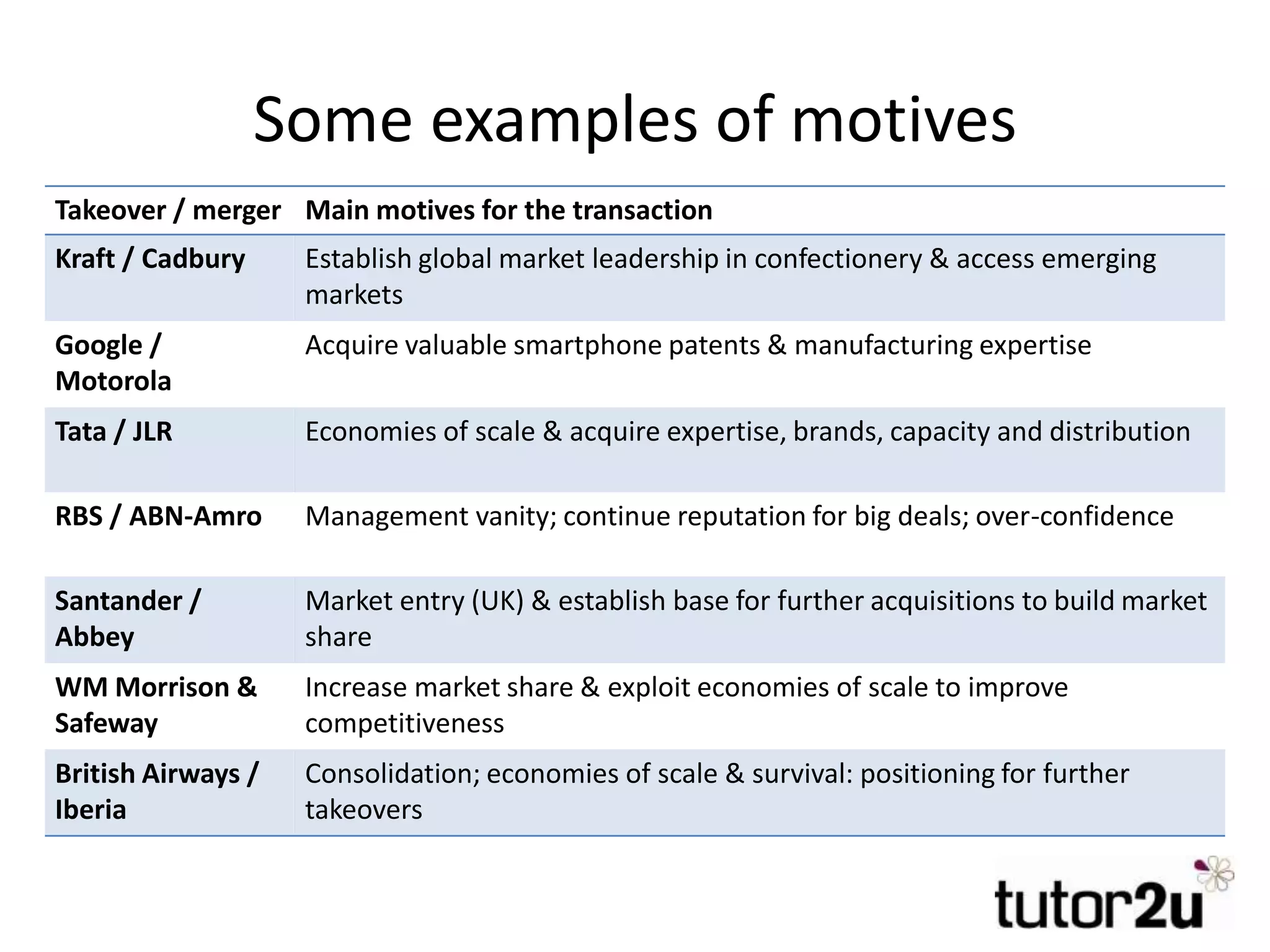

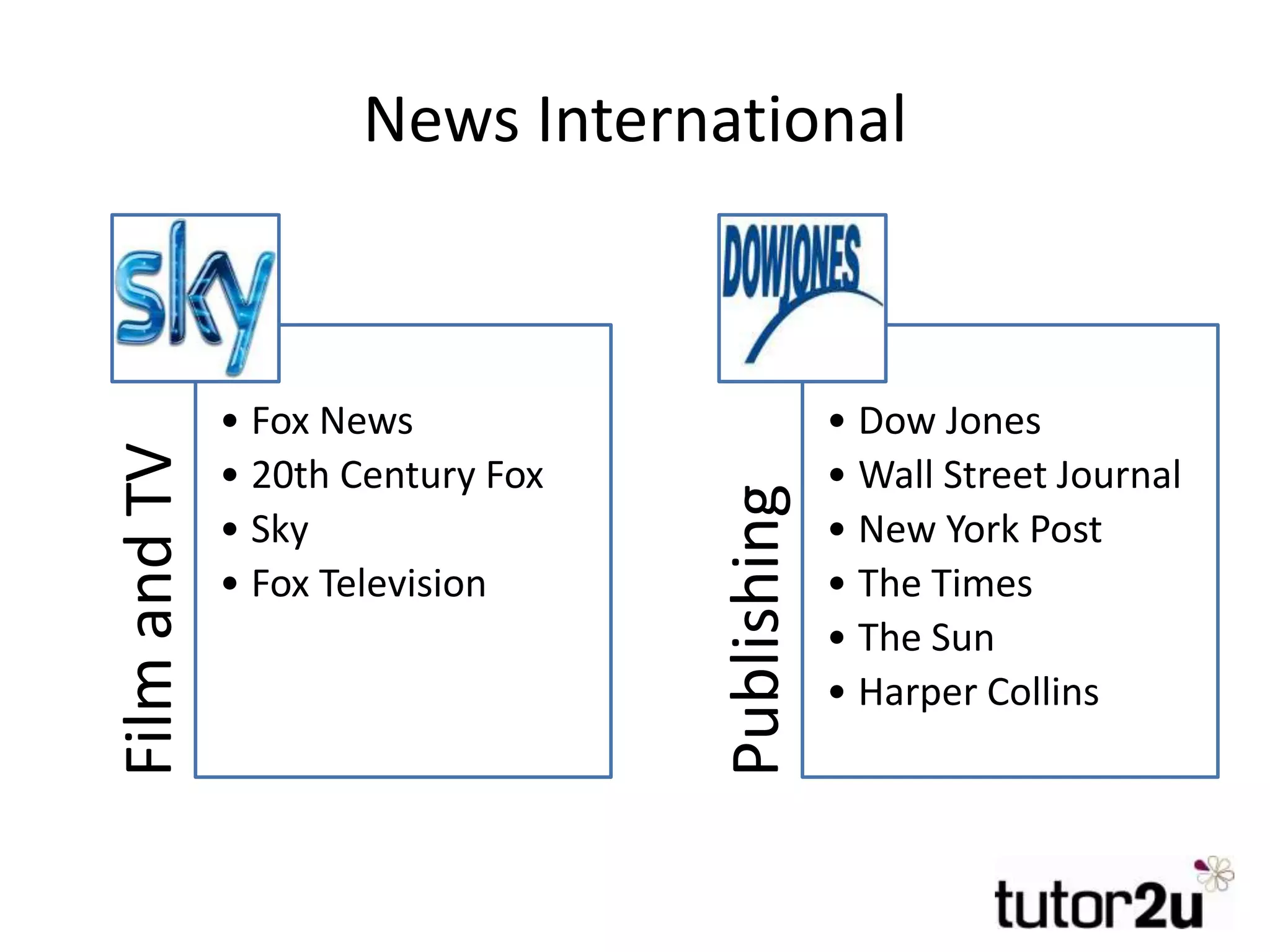

Definition and examples of horizontal integration, showcasing key mergers like Tata with Jaguar and Verizon's acquisition of Vodafone's interest.

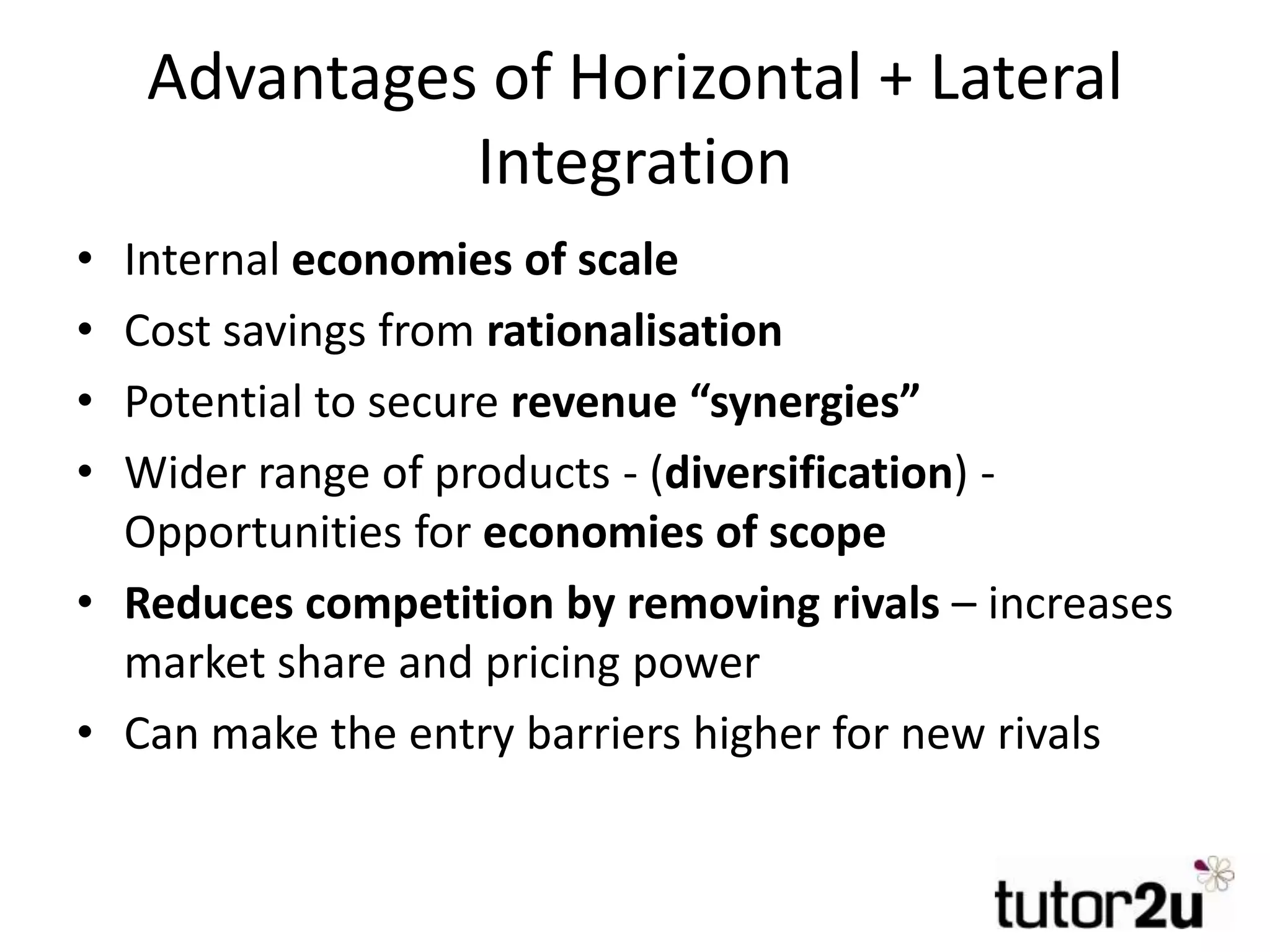

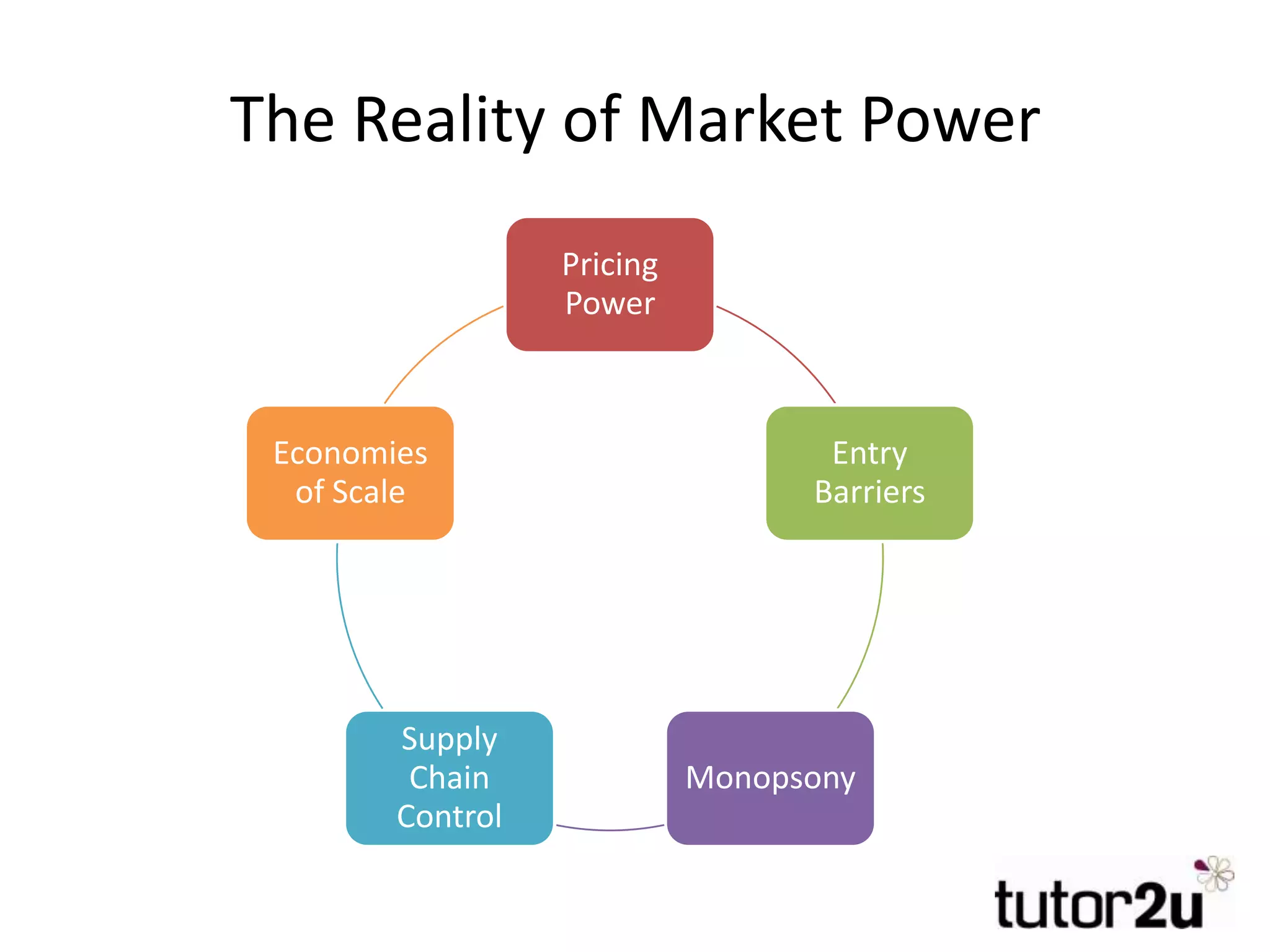

Advantages of horizontal and lateral integration include economies of scale, cost reductions, and increased market power.

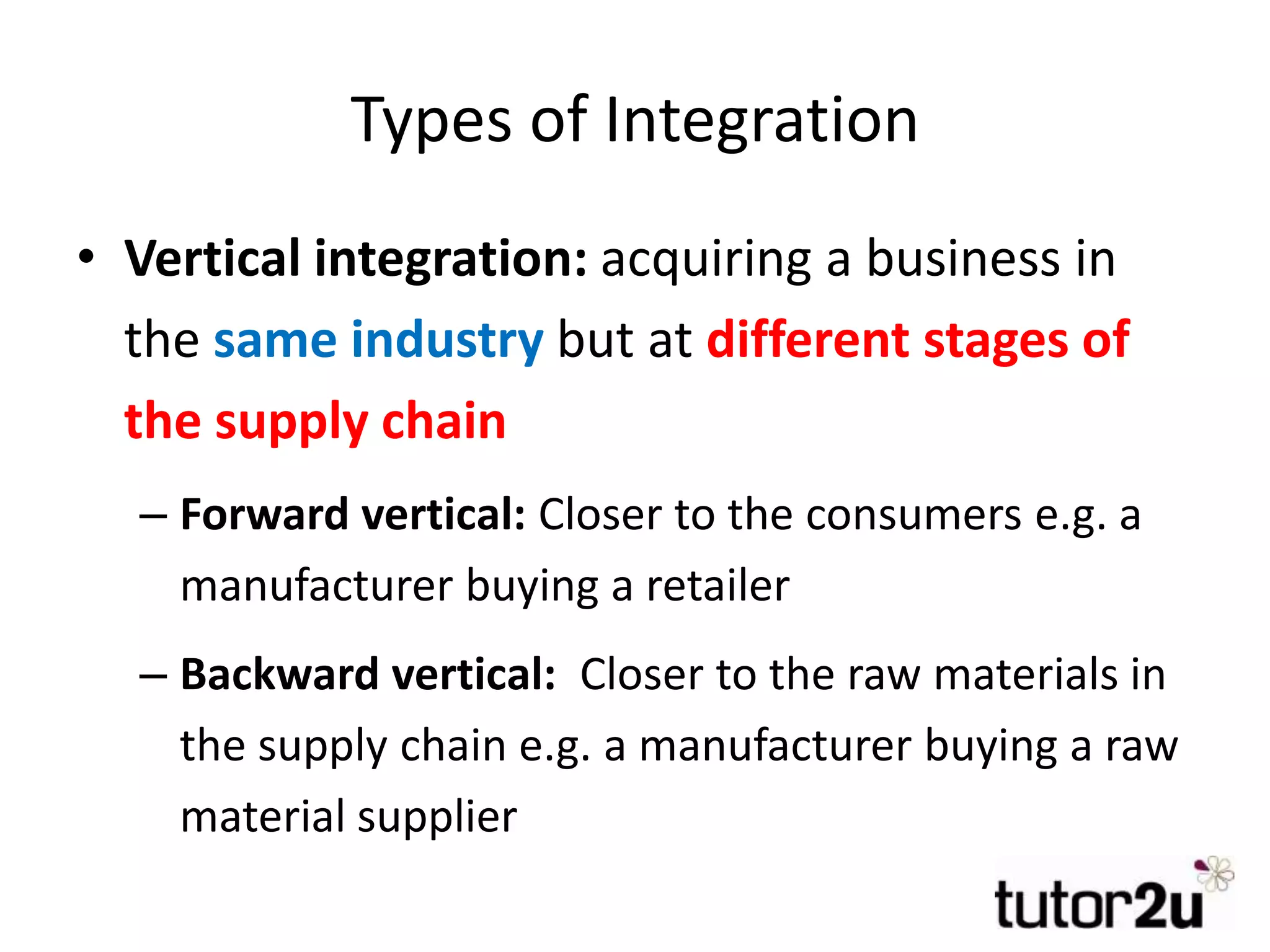

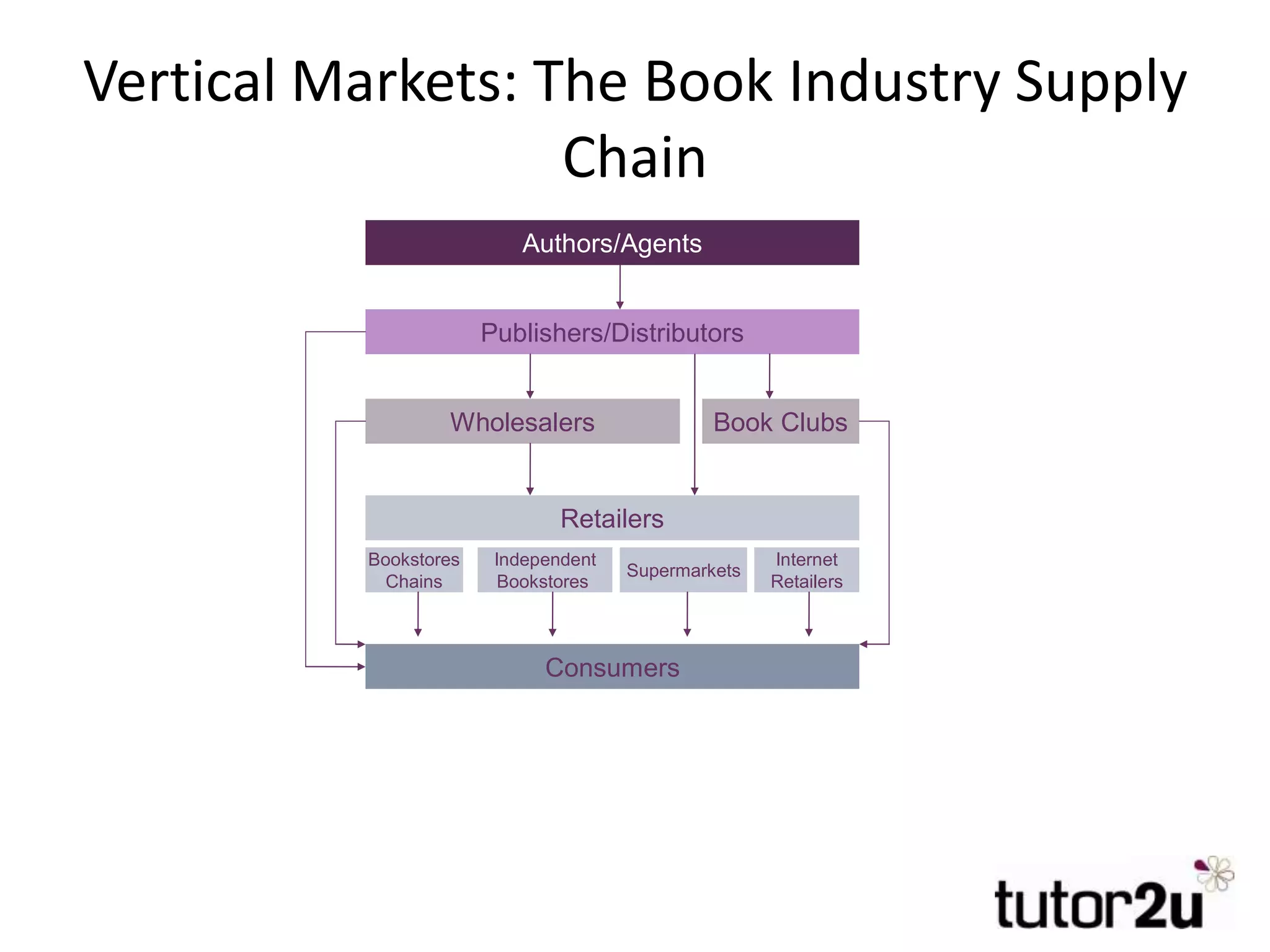

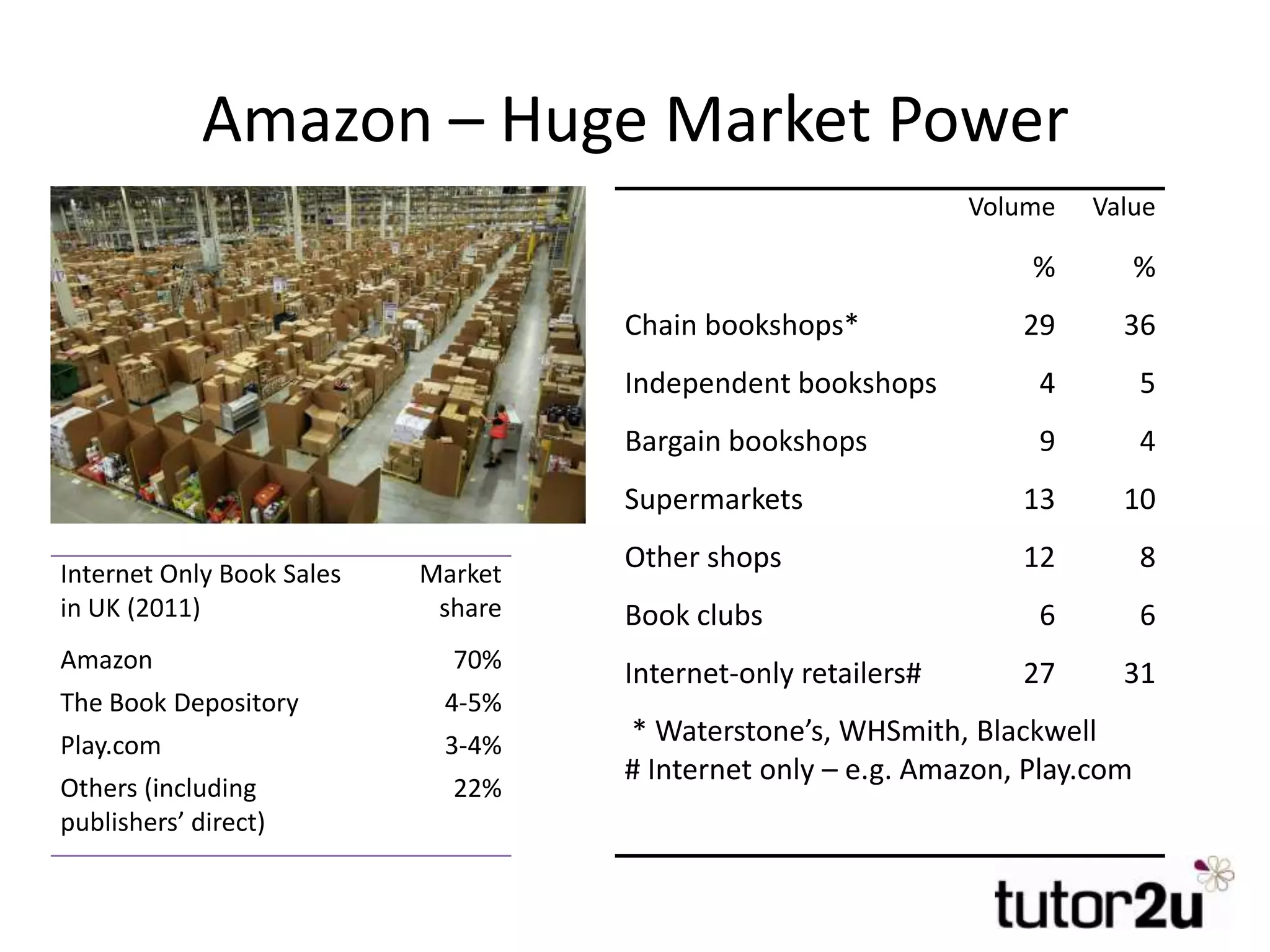

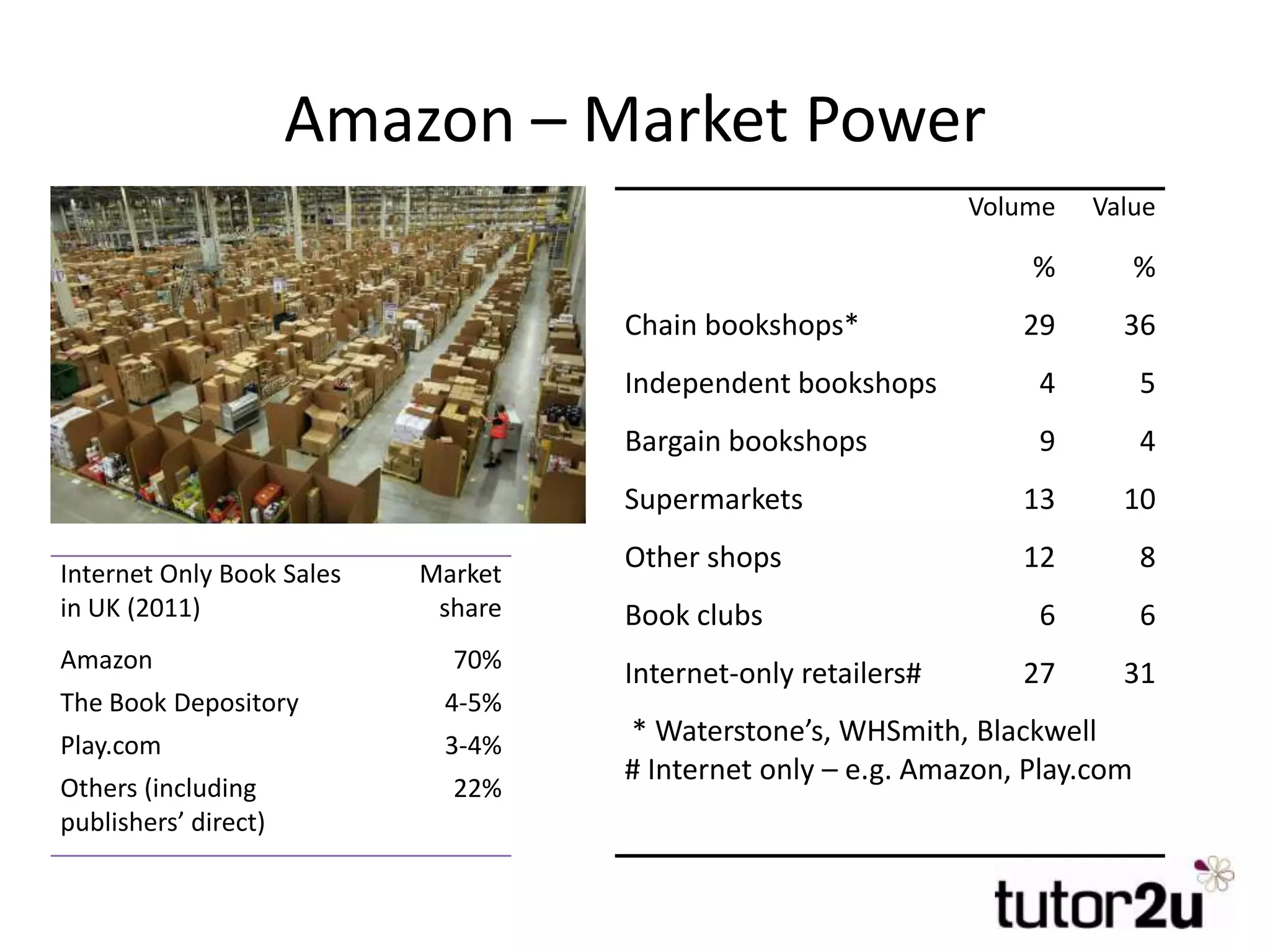

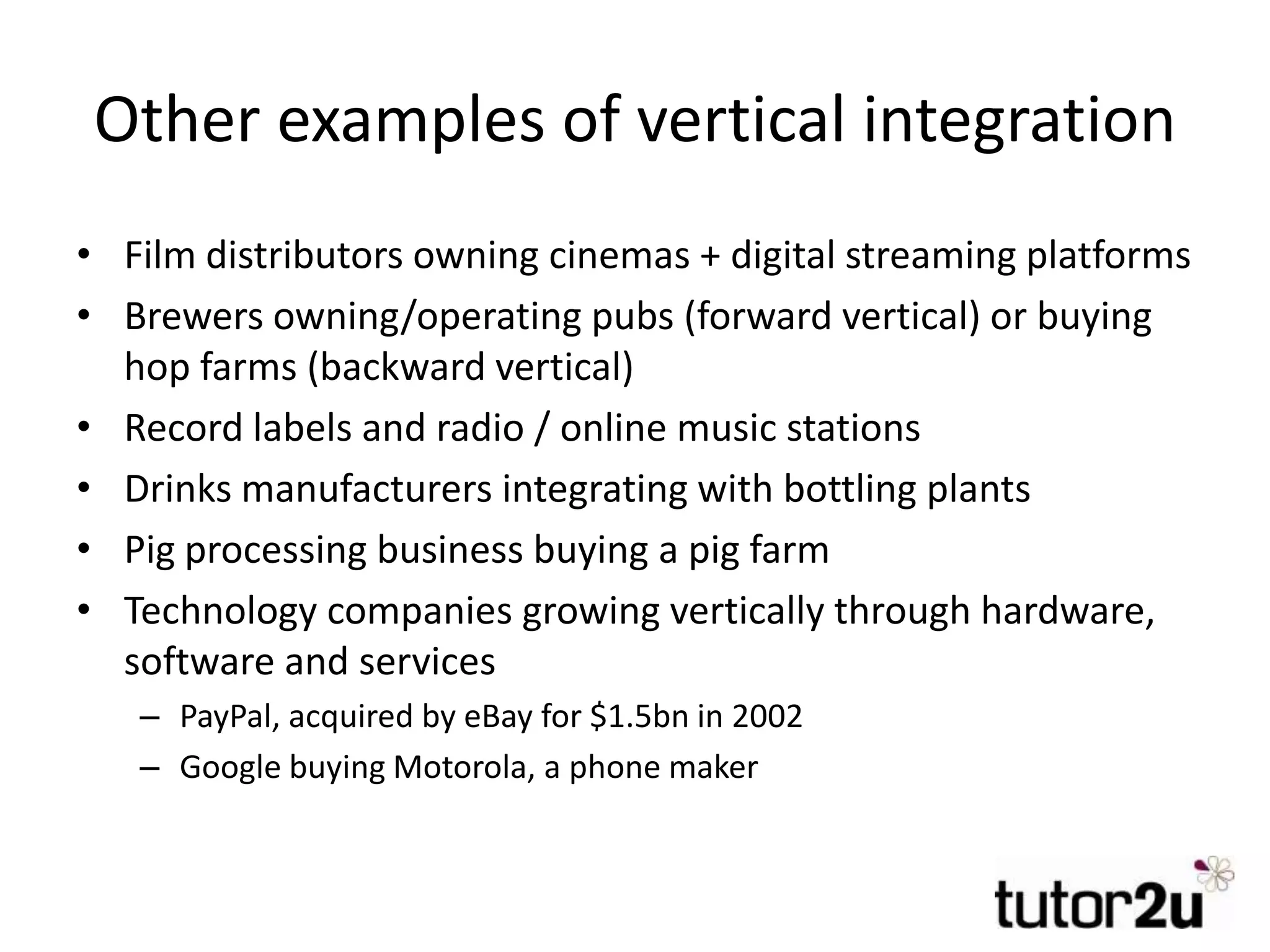

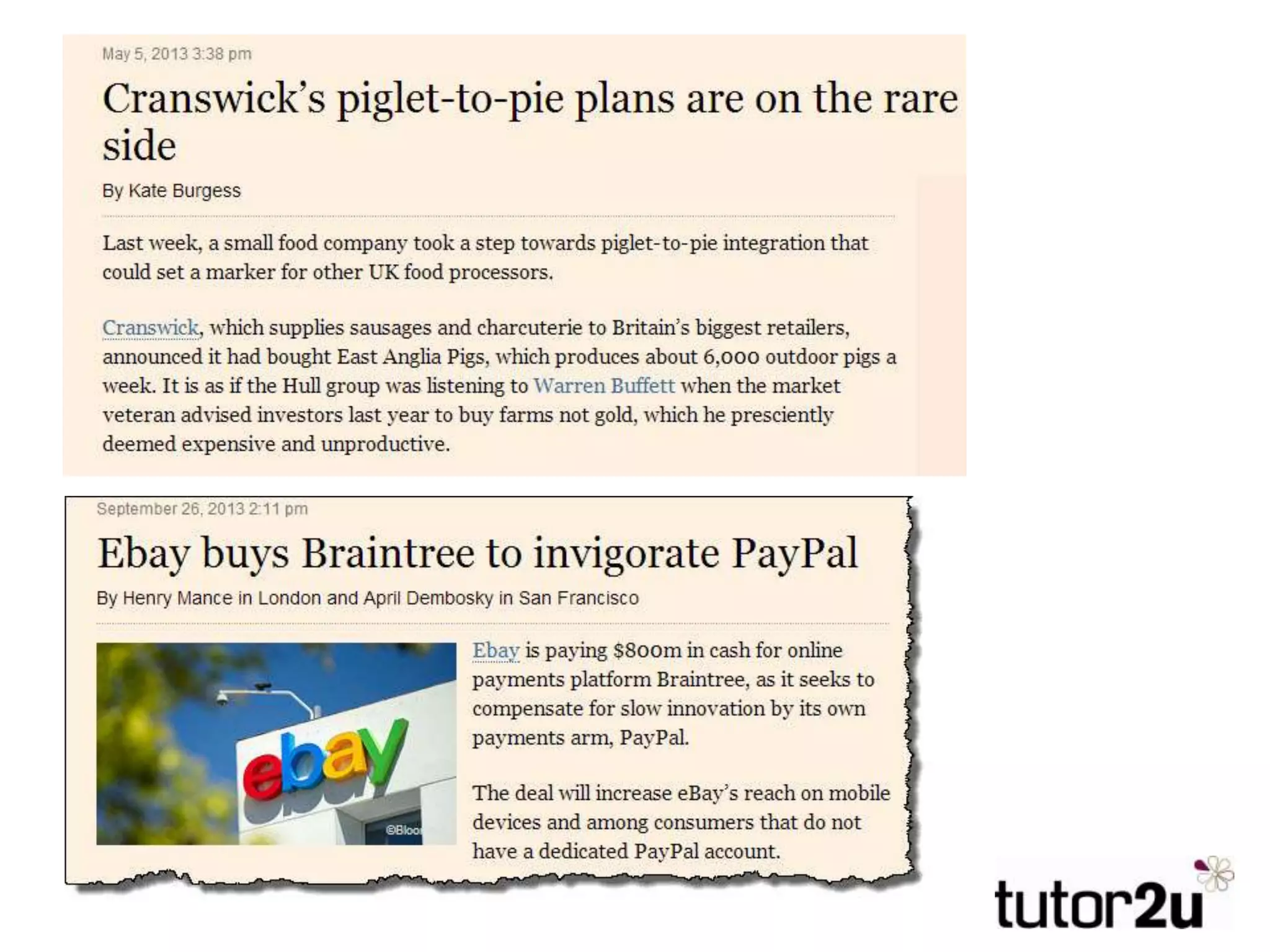

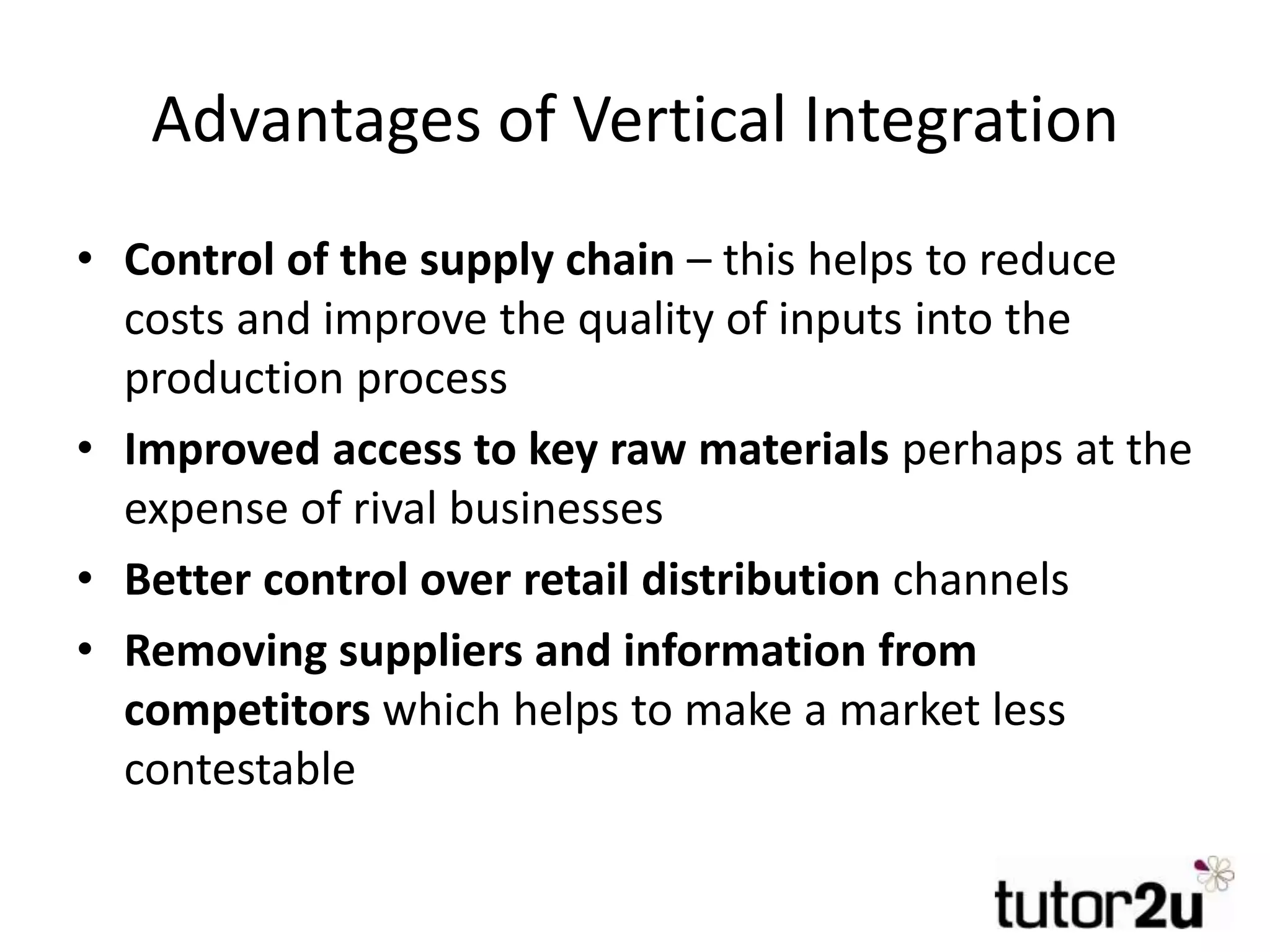

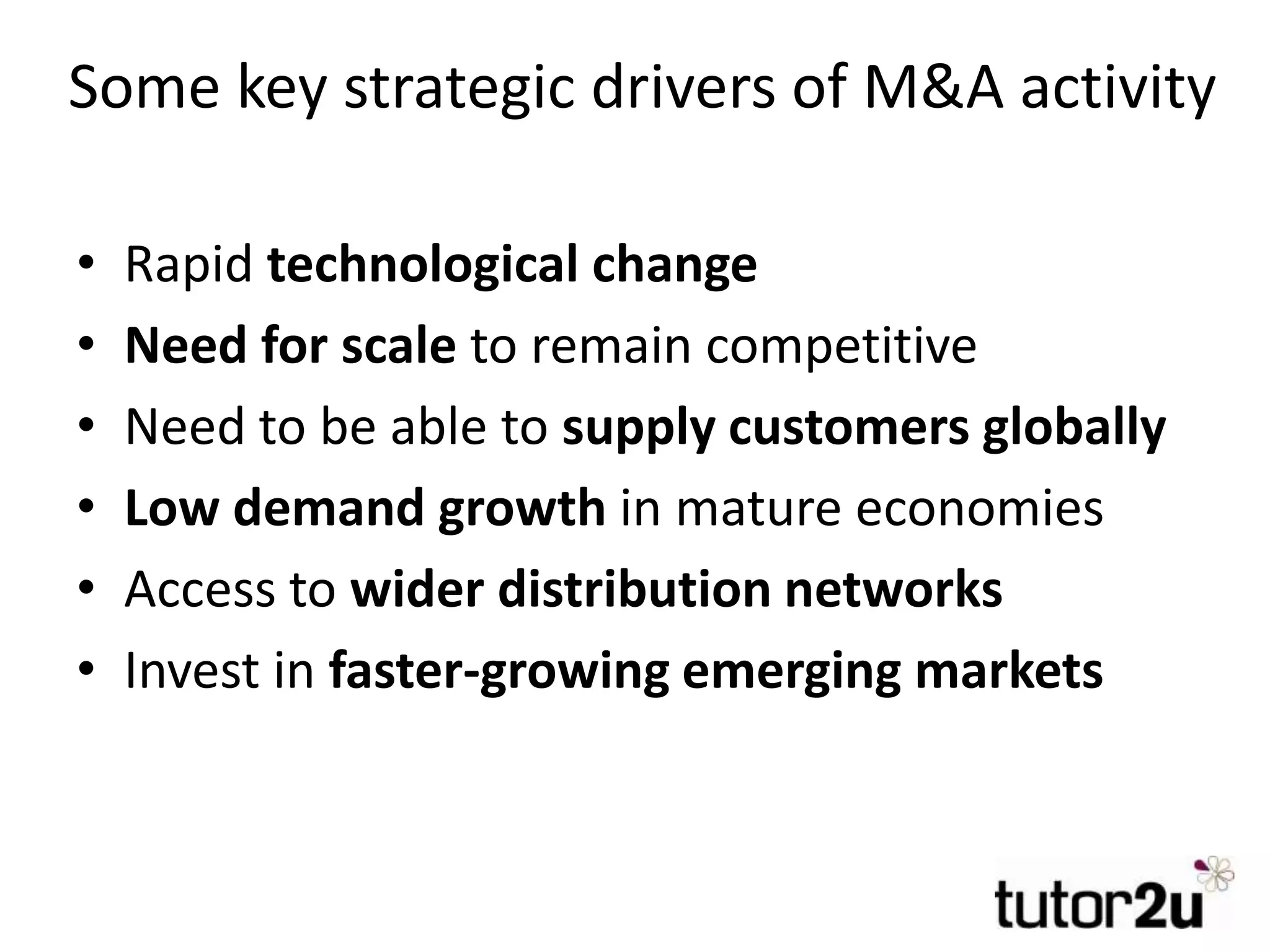

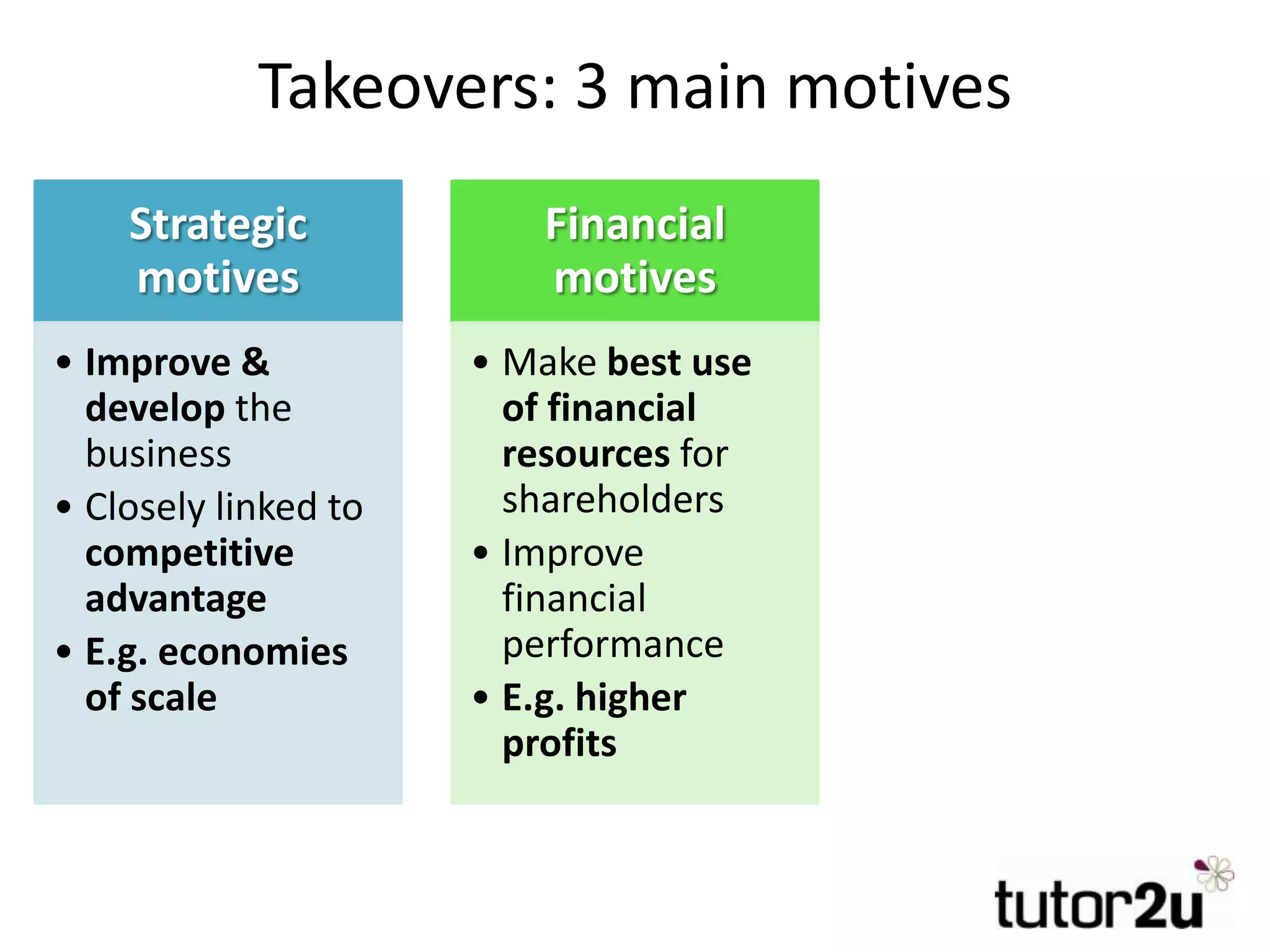

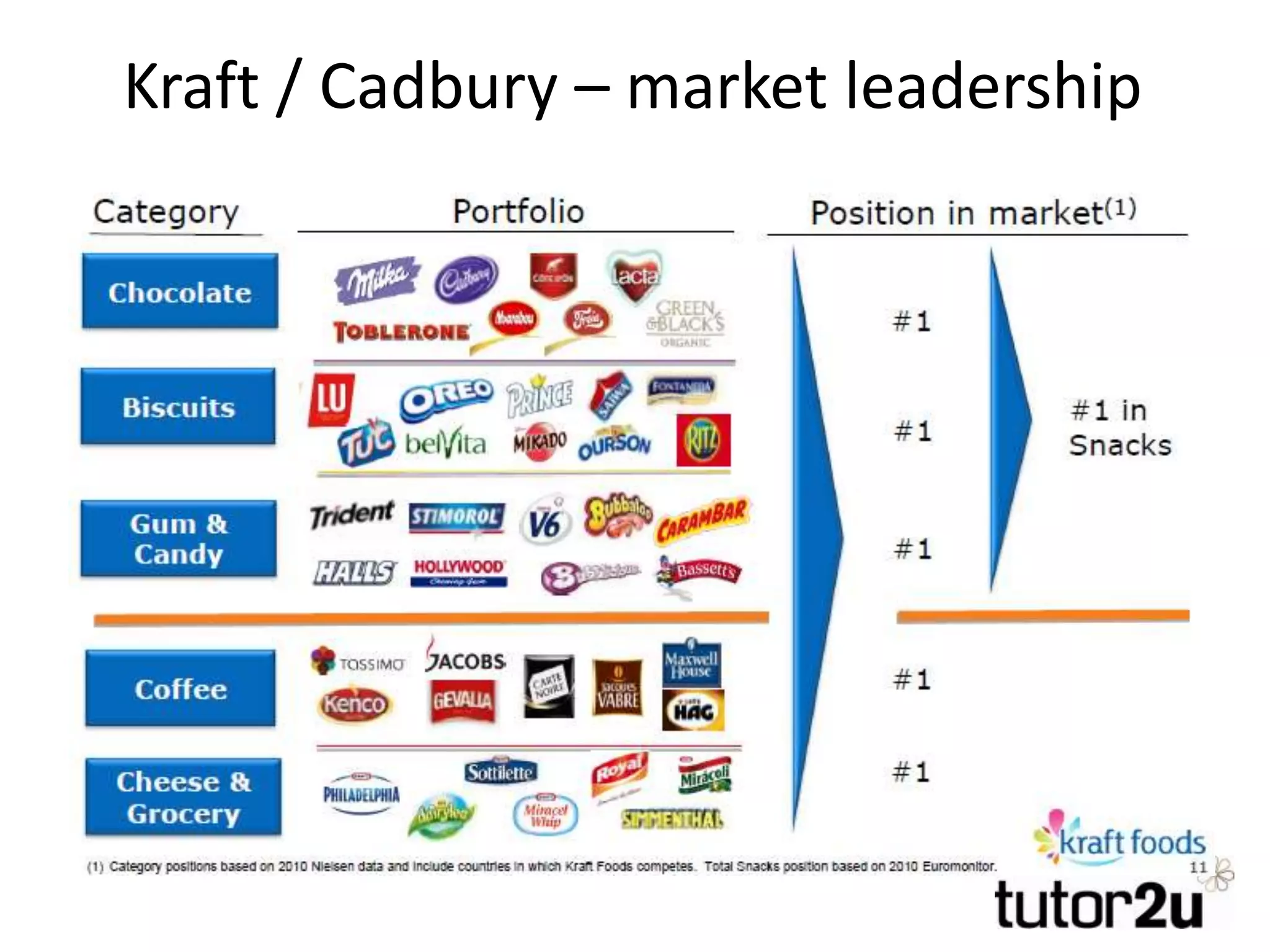

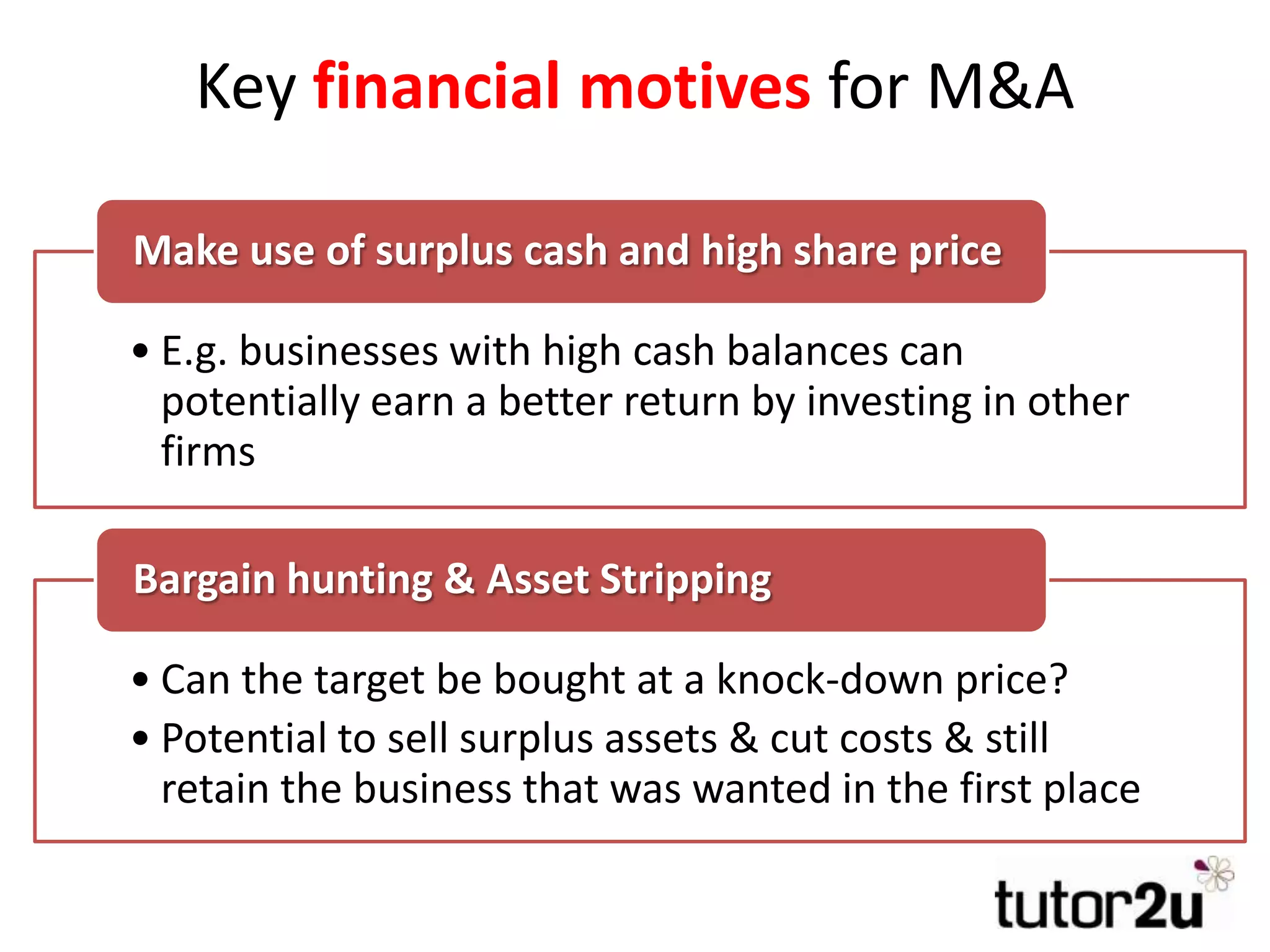

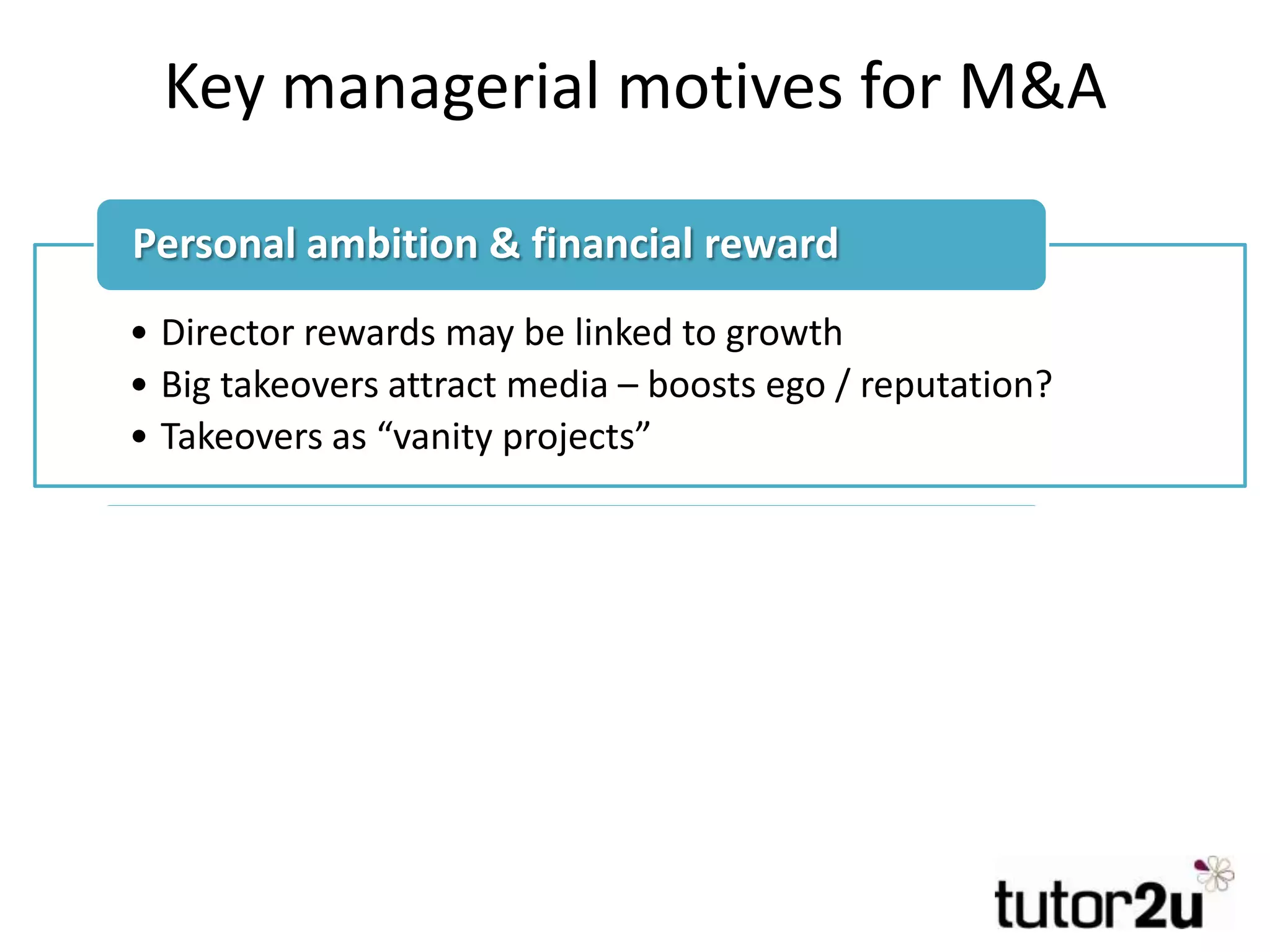

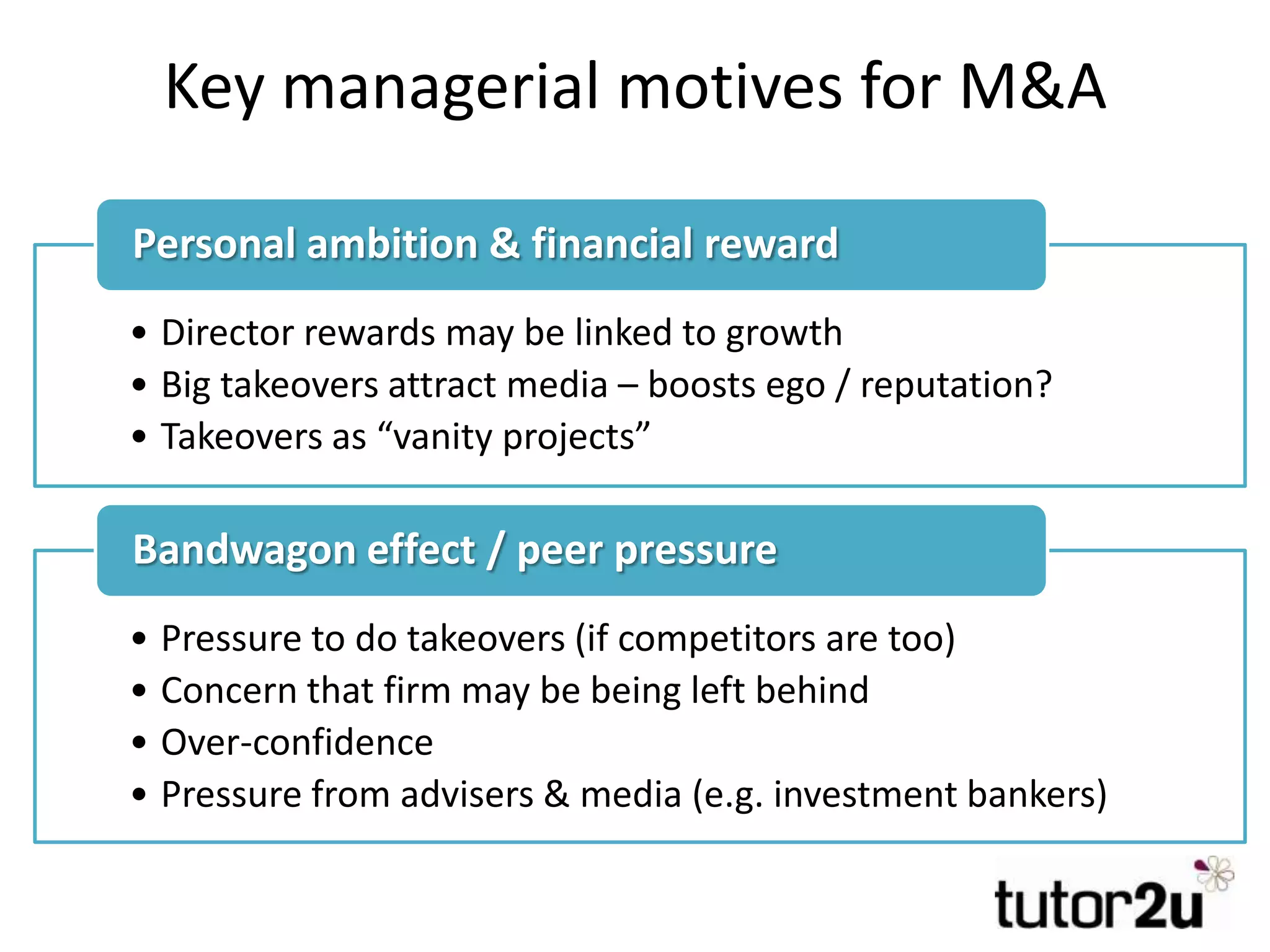

Vertical integration types: forward and backward. Highlights advantages including supply chain control, access to raw materials, and competitive positioning. Strategic, financial, and managerial motives driving M&As, stressing benefits and potential self-interest of managers.

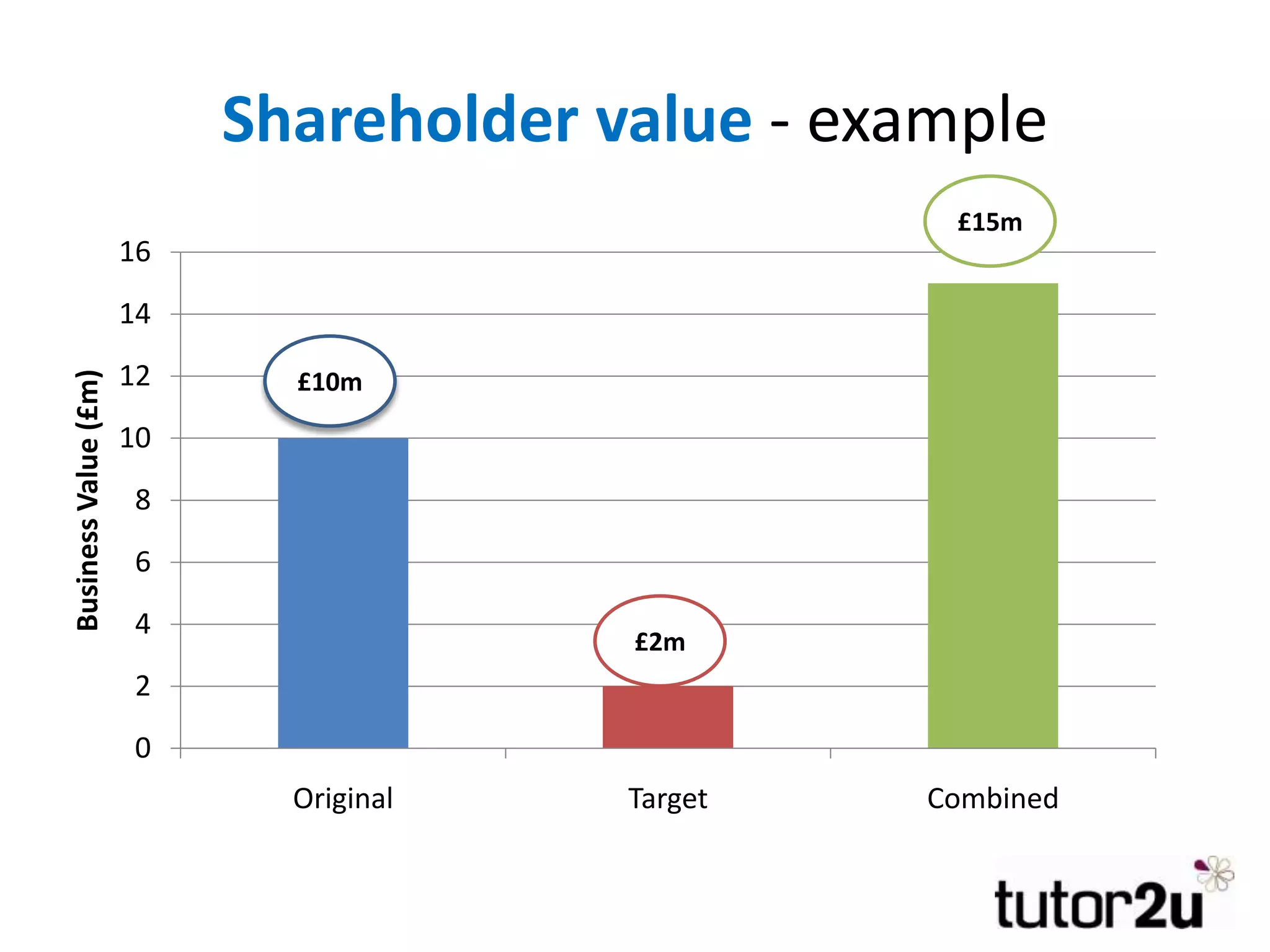

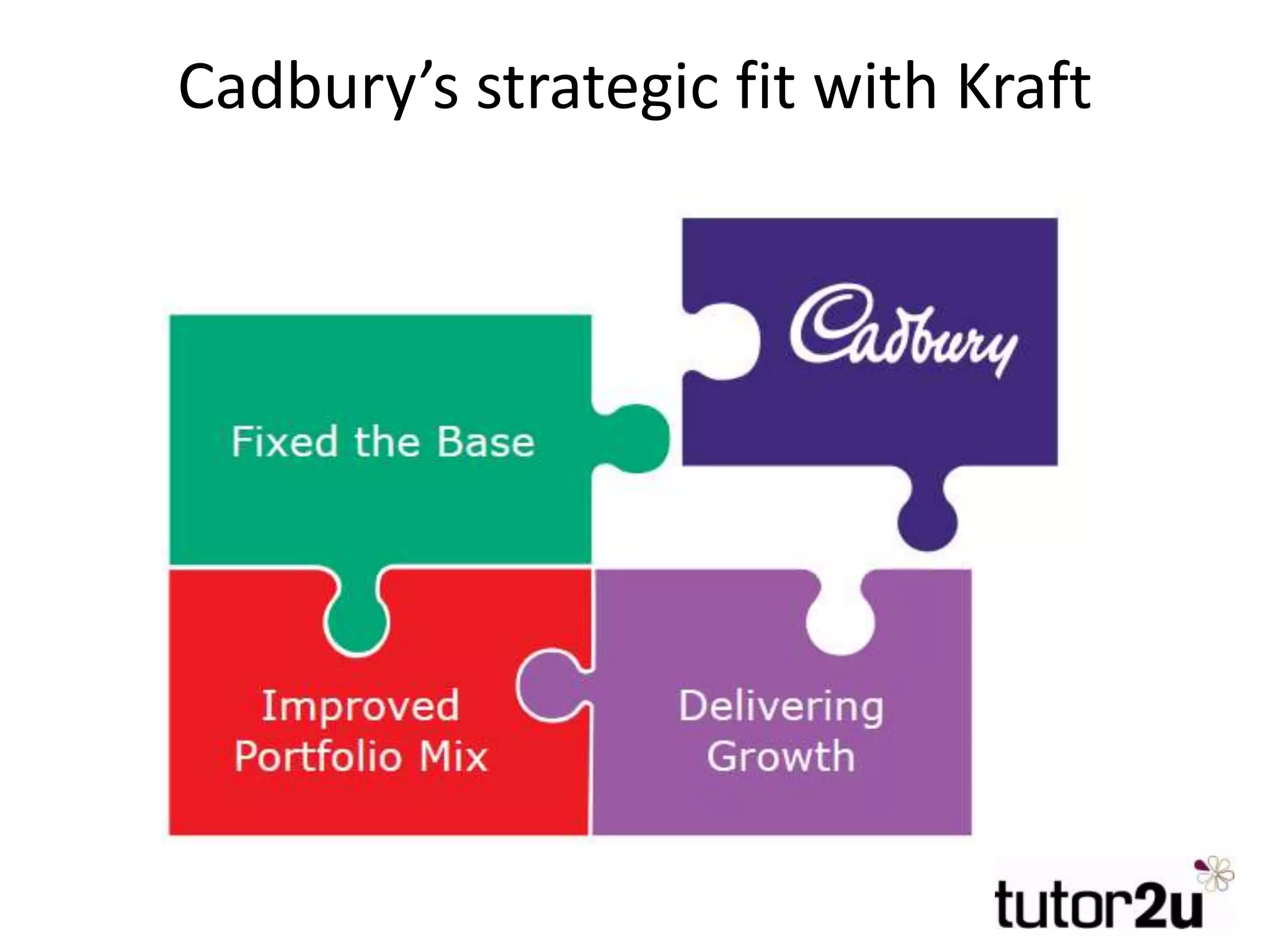

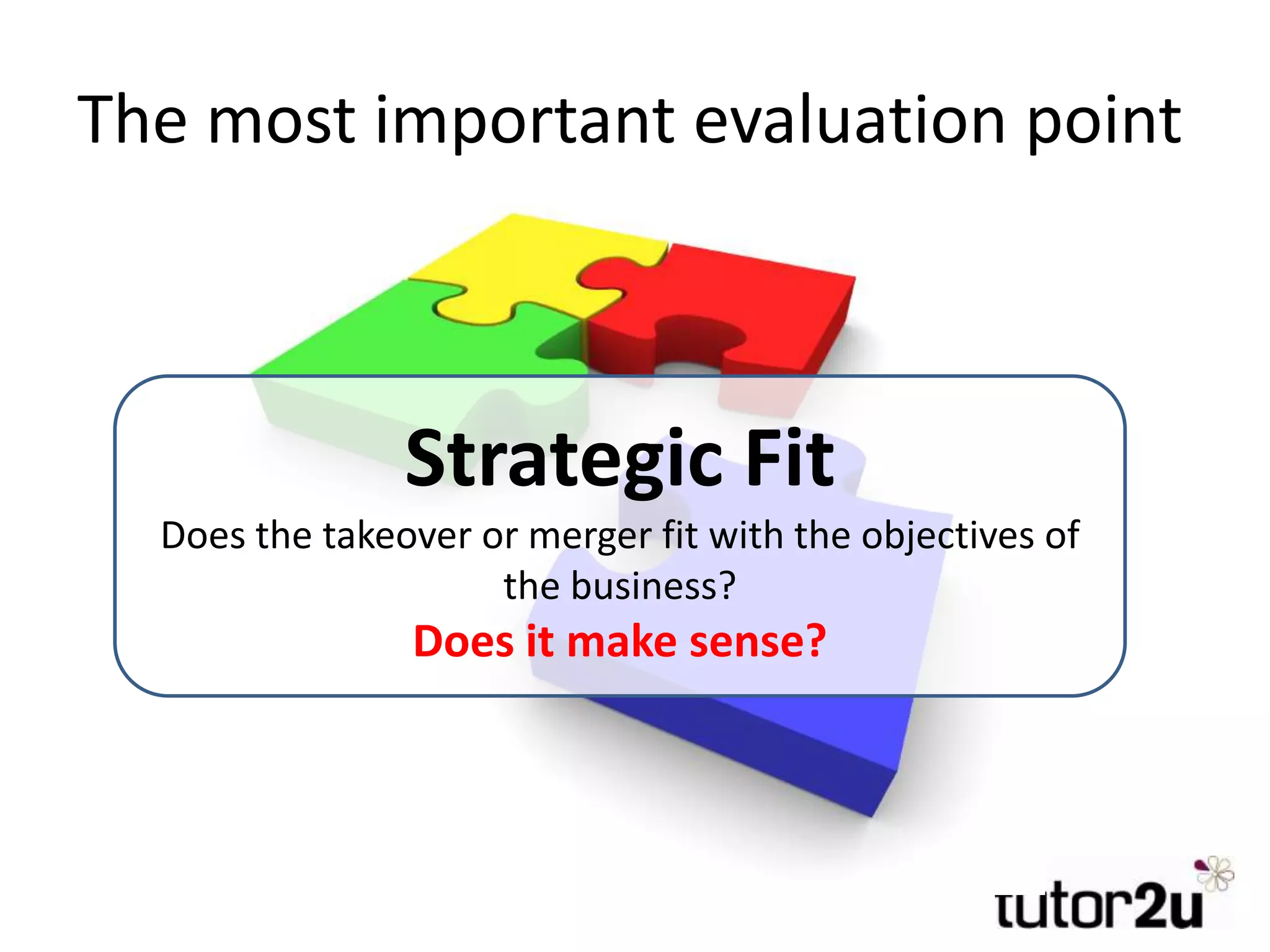

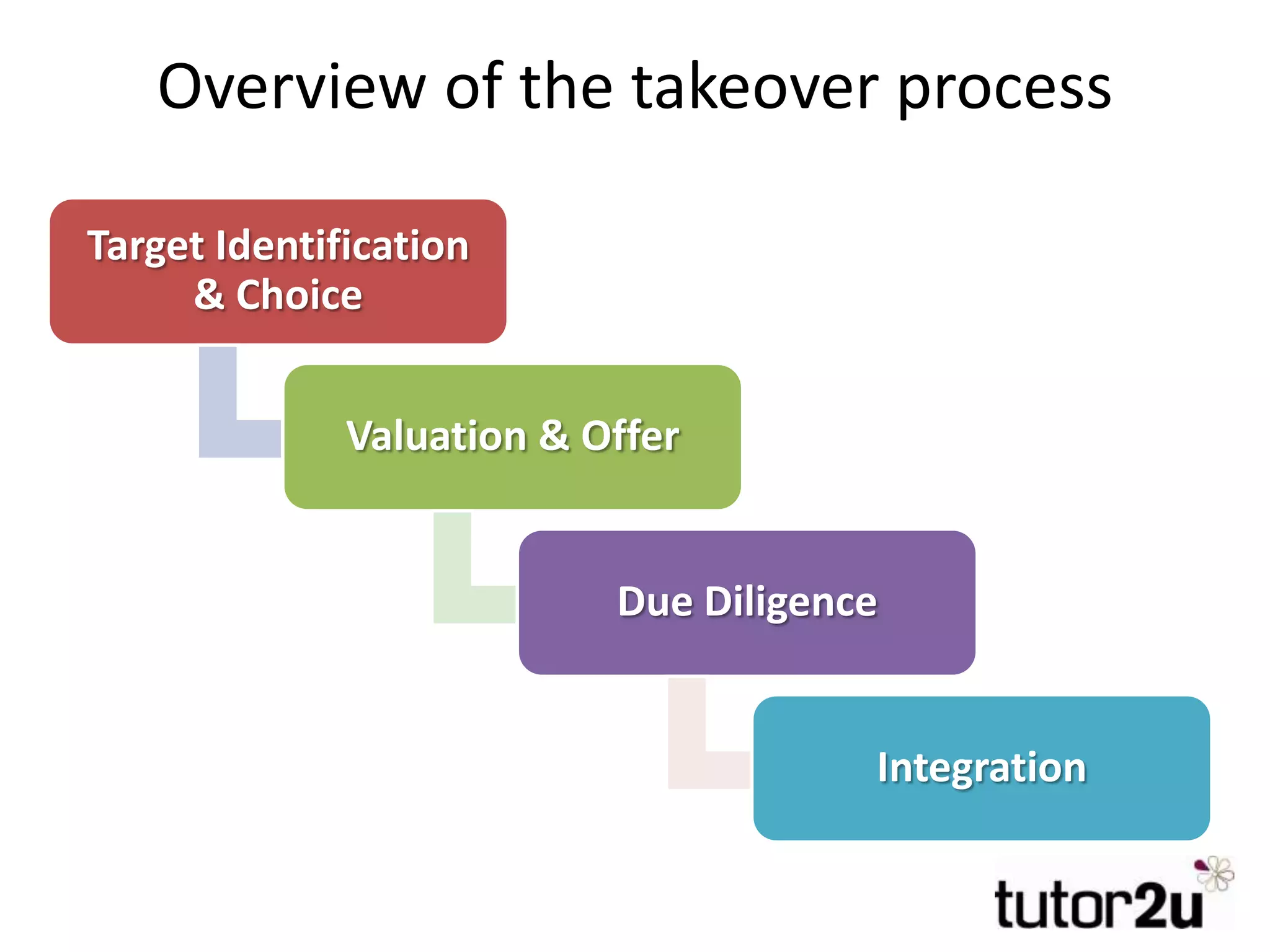

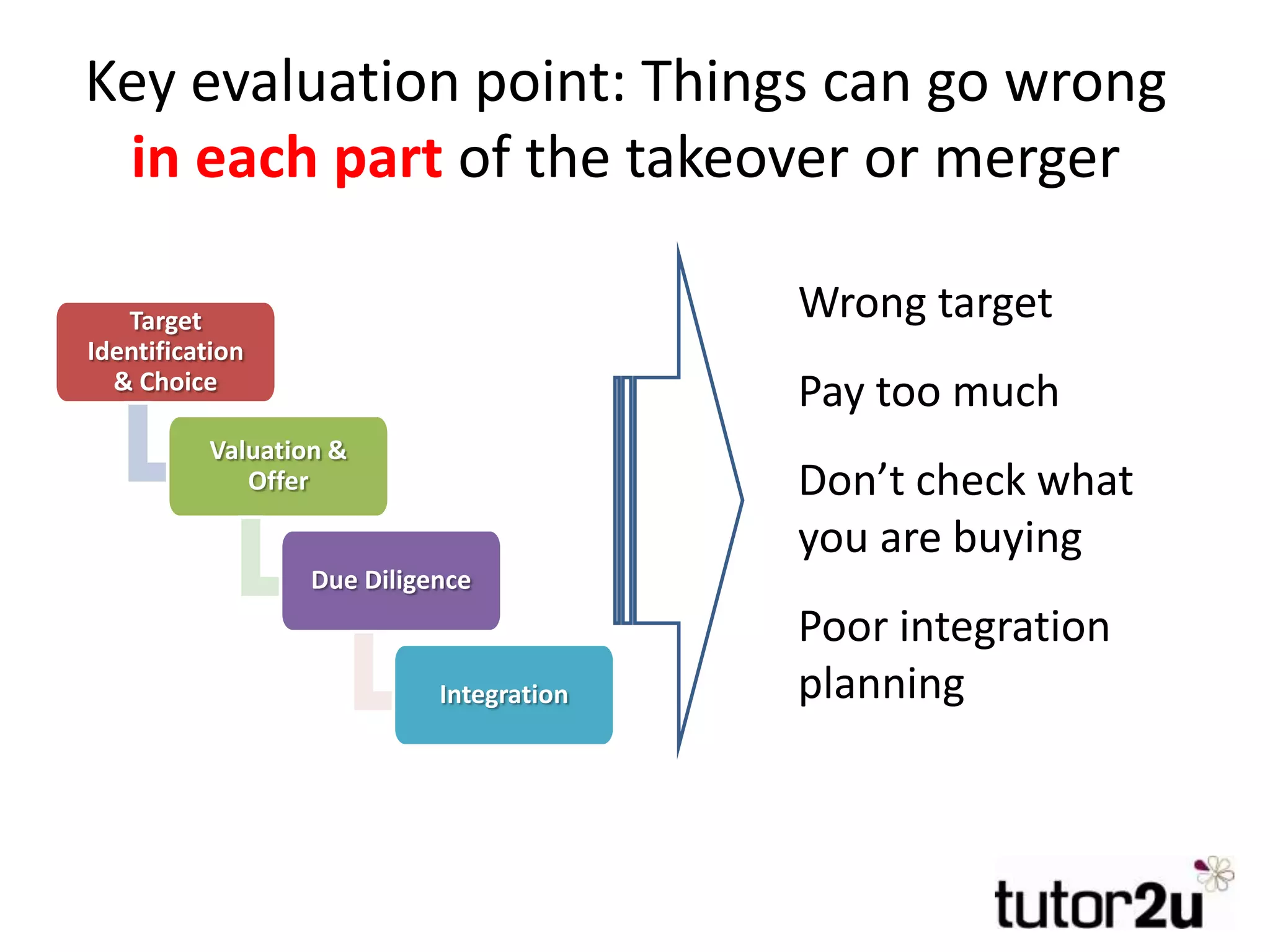

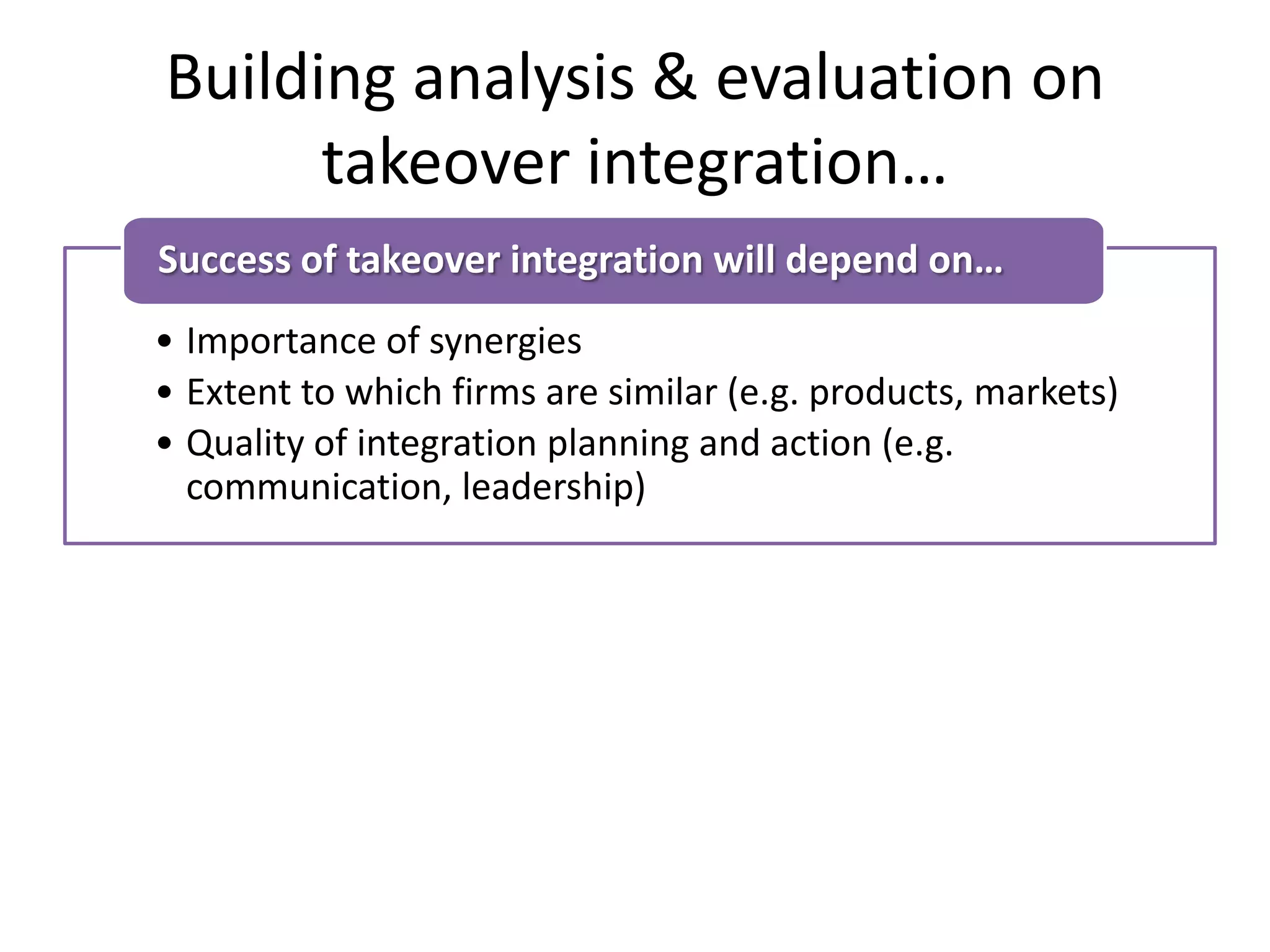

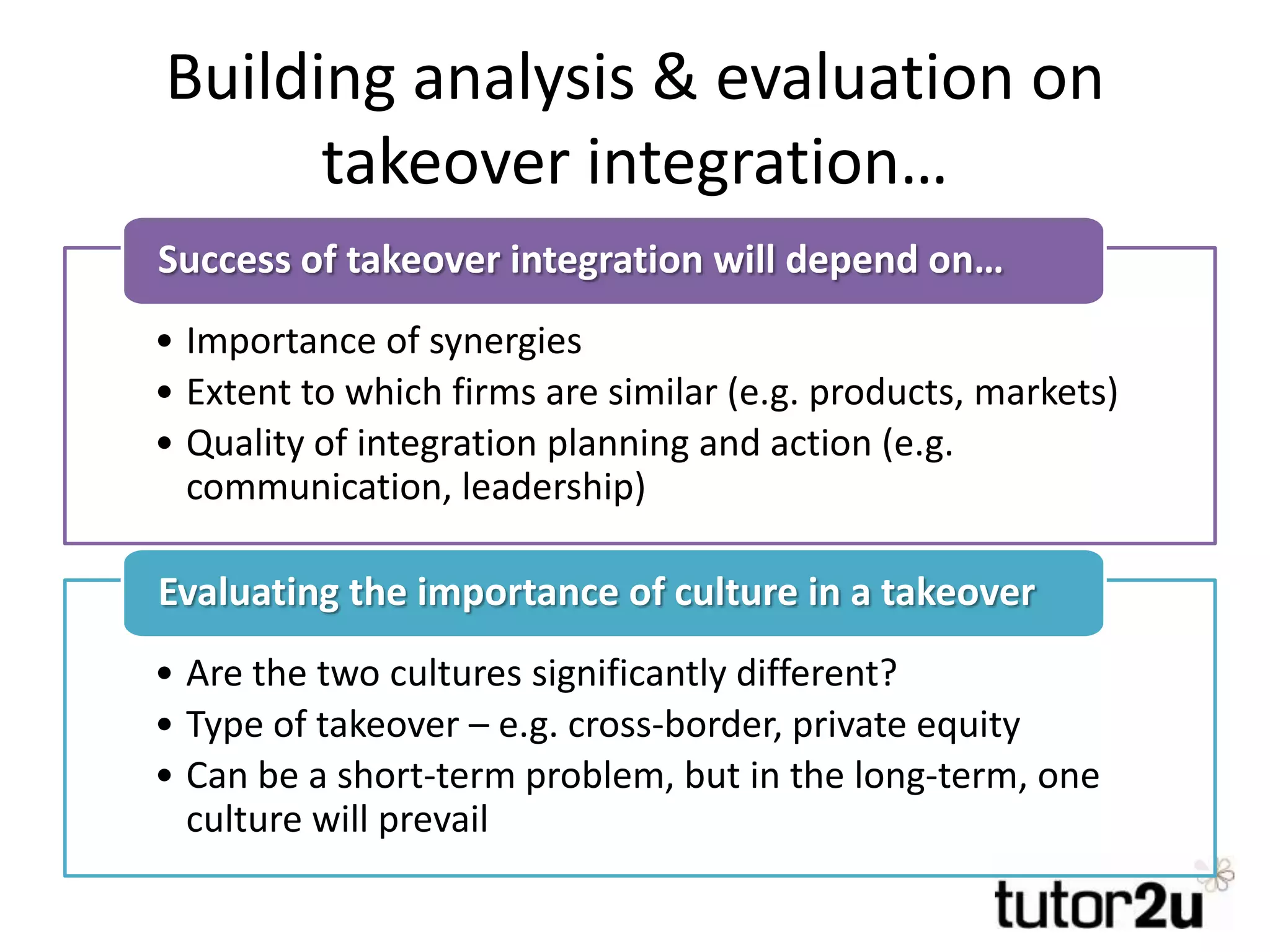

Evaluation points for mergers, Importance of strategic fit and synergy in assessing potential takeover success.

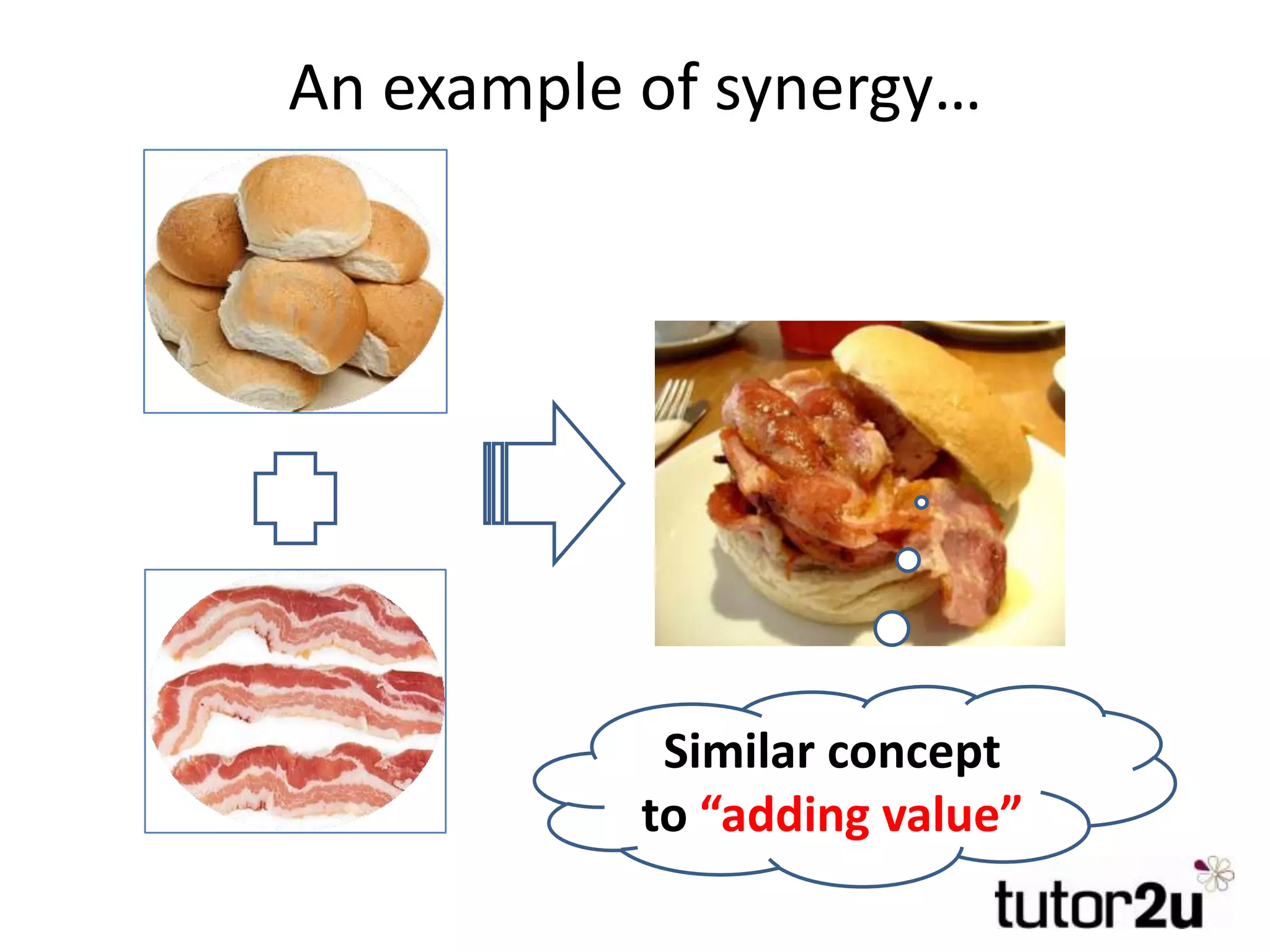

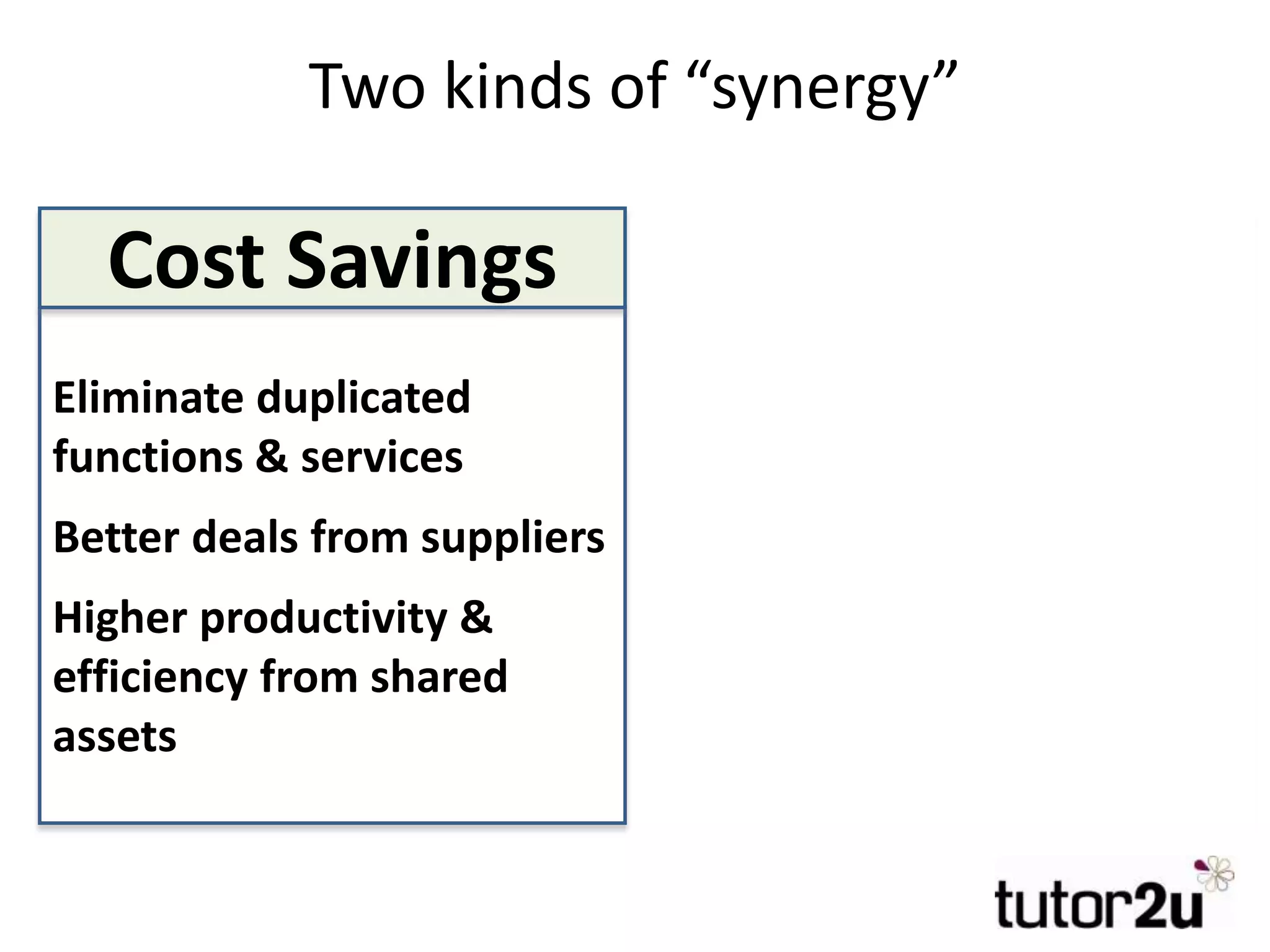

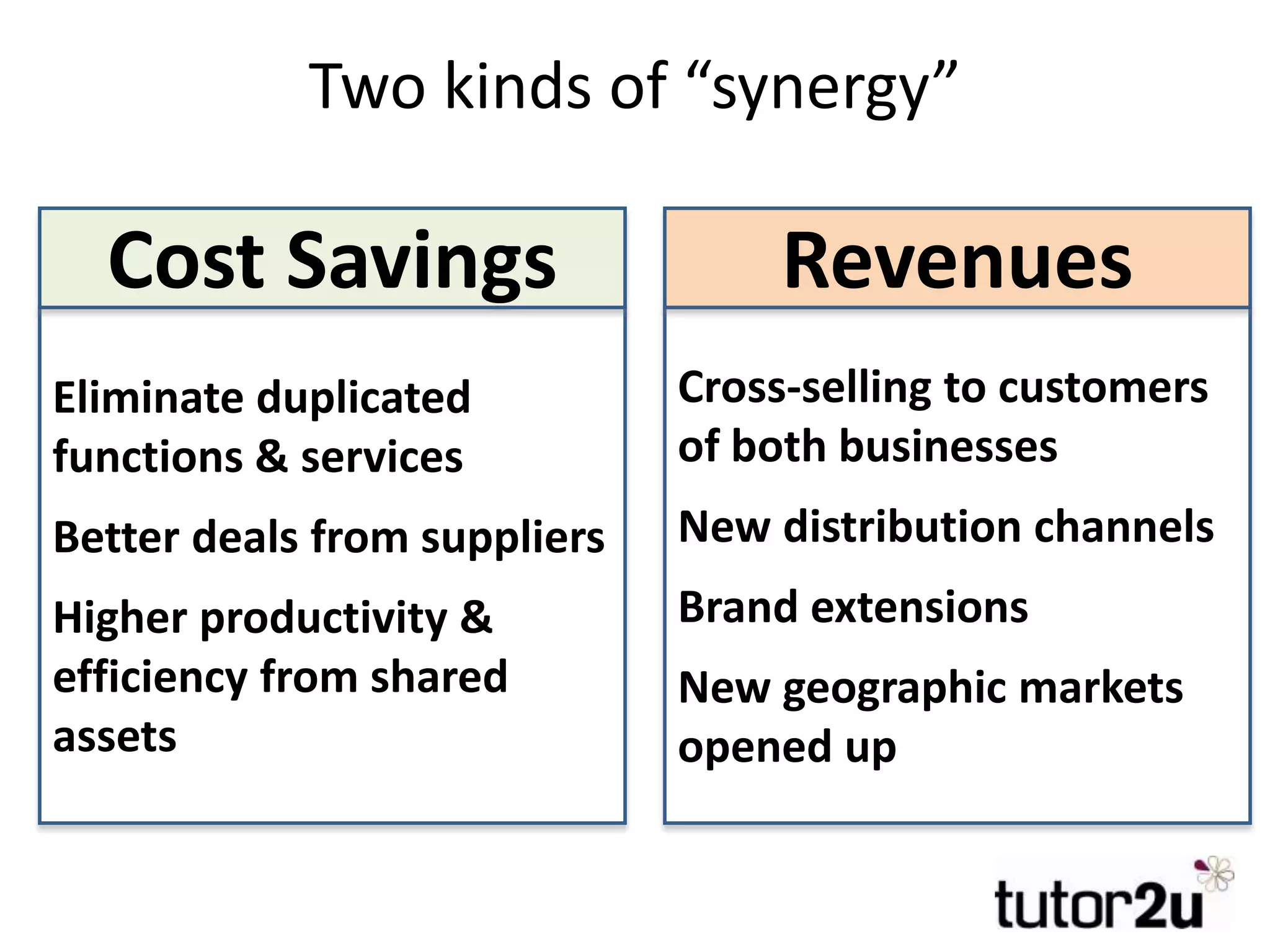

Definition of synergy and its two types; focuses on eliminating duplicated services and achieving higher efficiency and revenue.

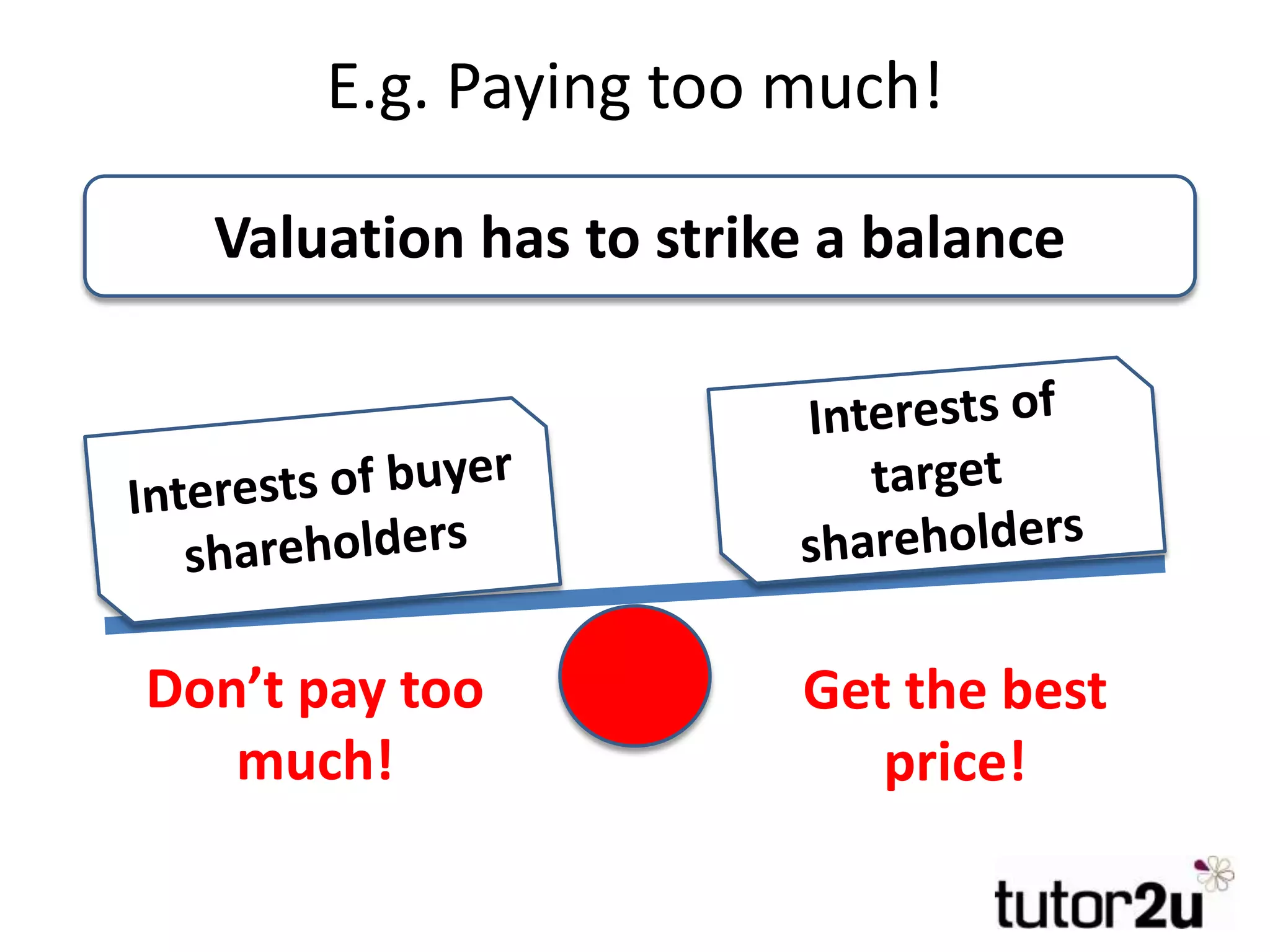

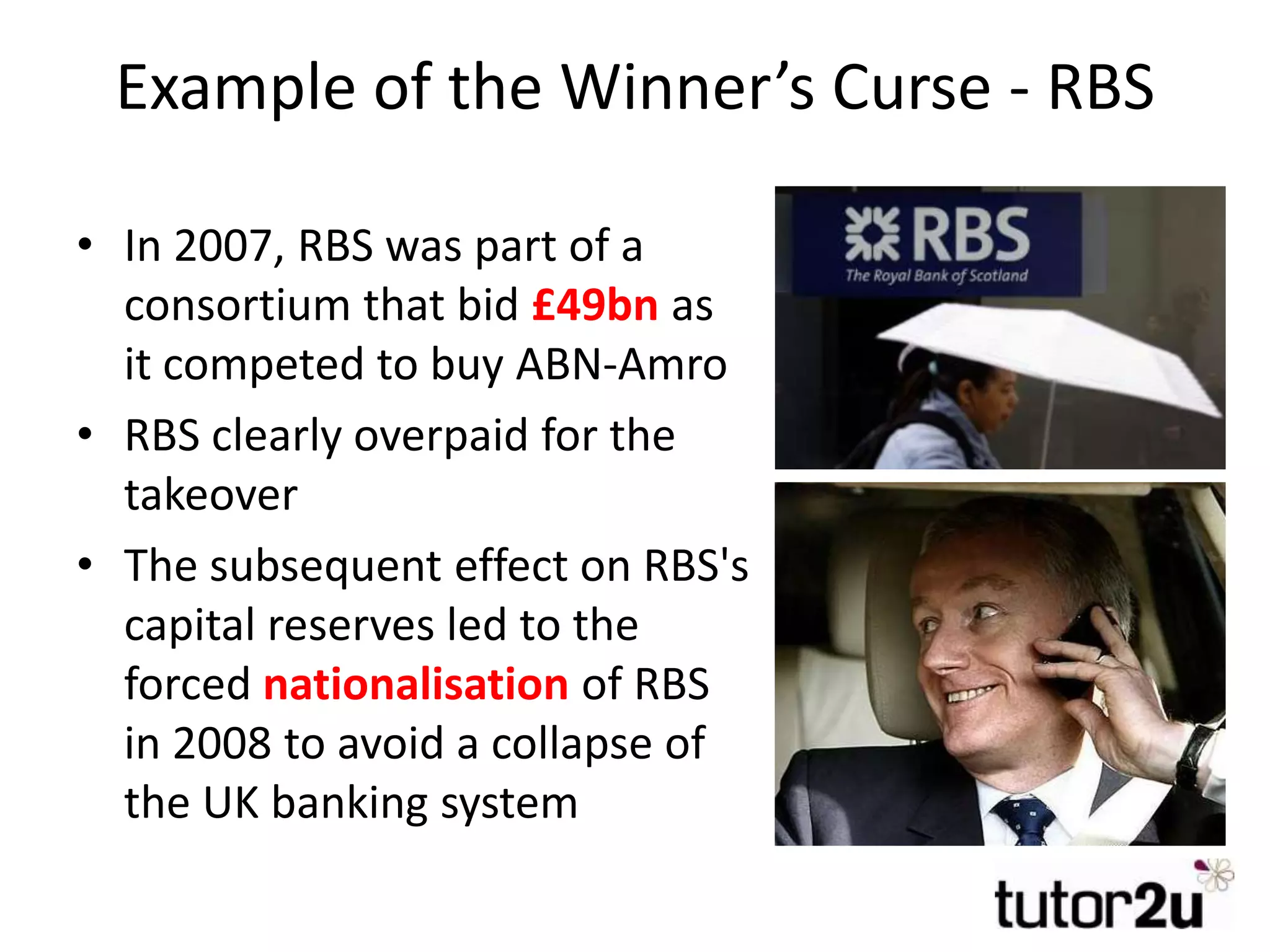

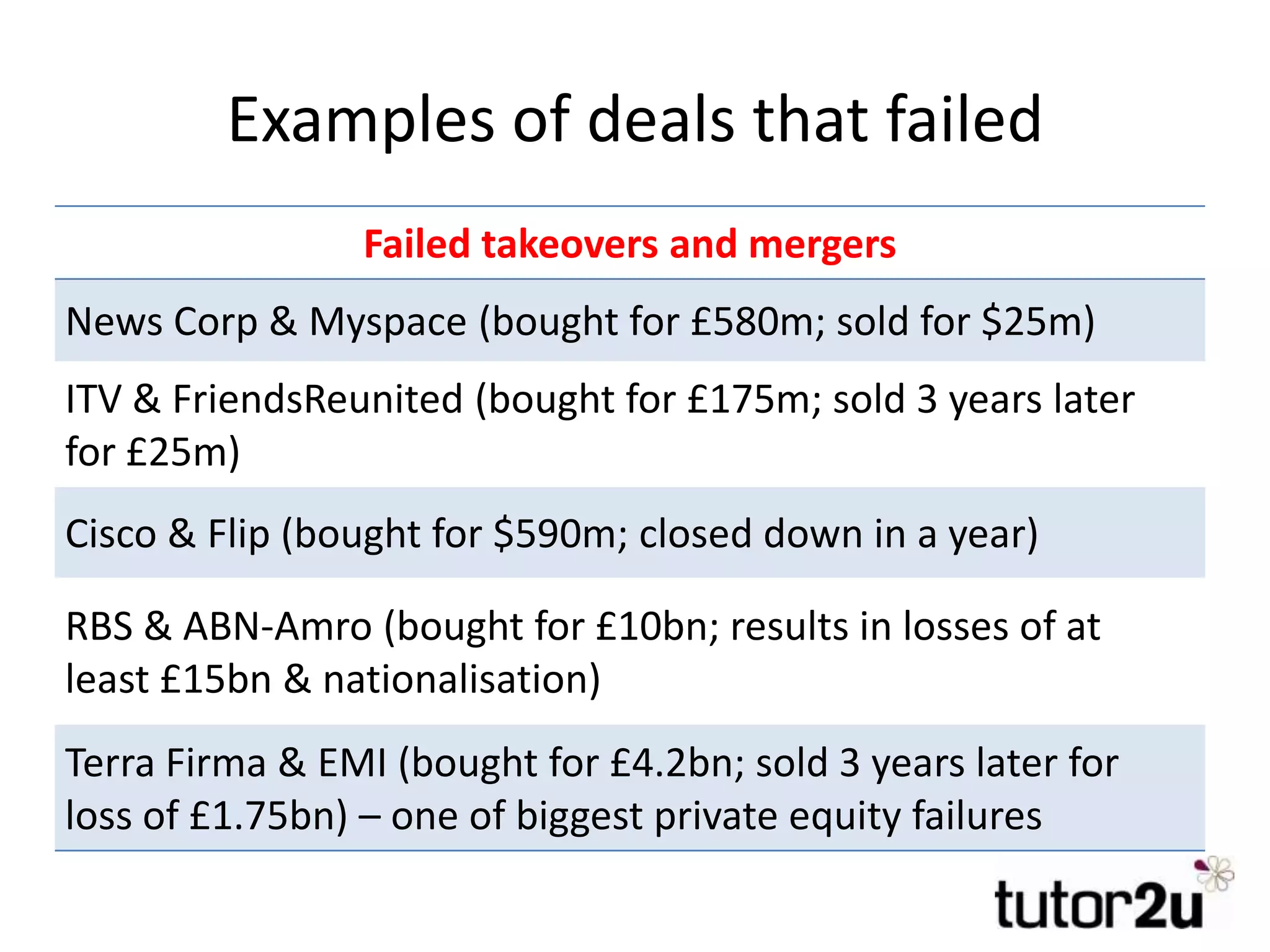

Risks in M&As include wrong target selection, overvaluation, and high-profile failures like RBS's acquisition of ABN-Amro.

Emphasizes the importance of planning for cultural integration and synergy post-merger to ensure success.

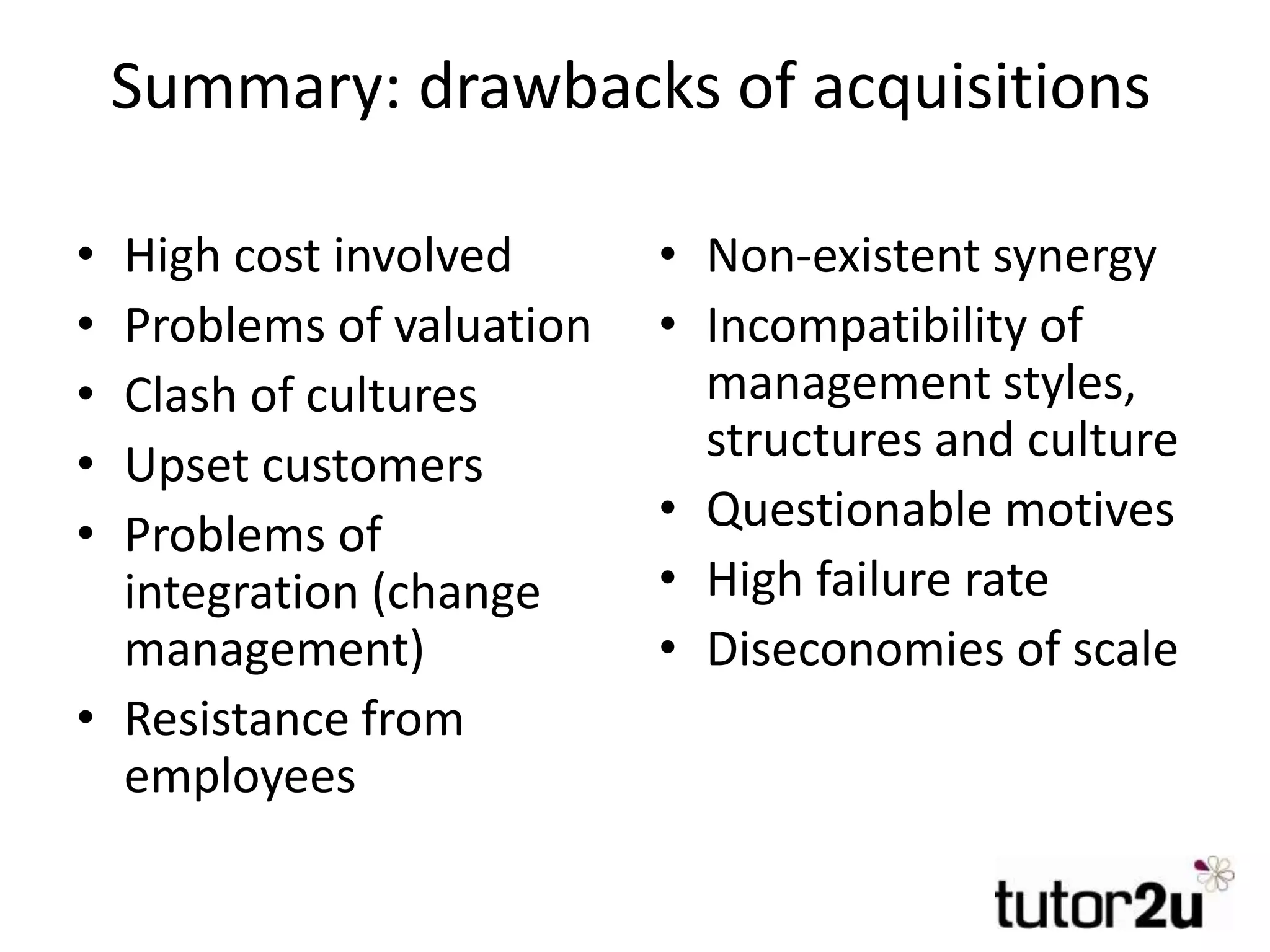

Details common issues related to M&As including high costs, cultural clashes, integration challenges, and high failure rates.

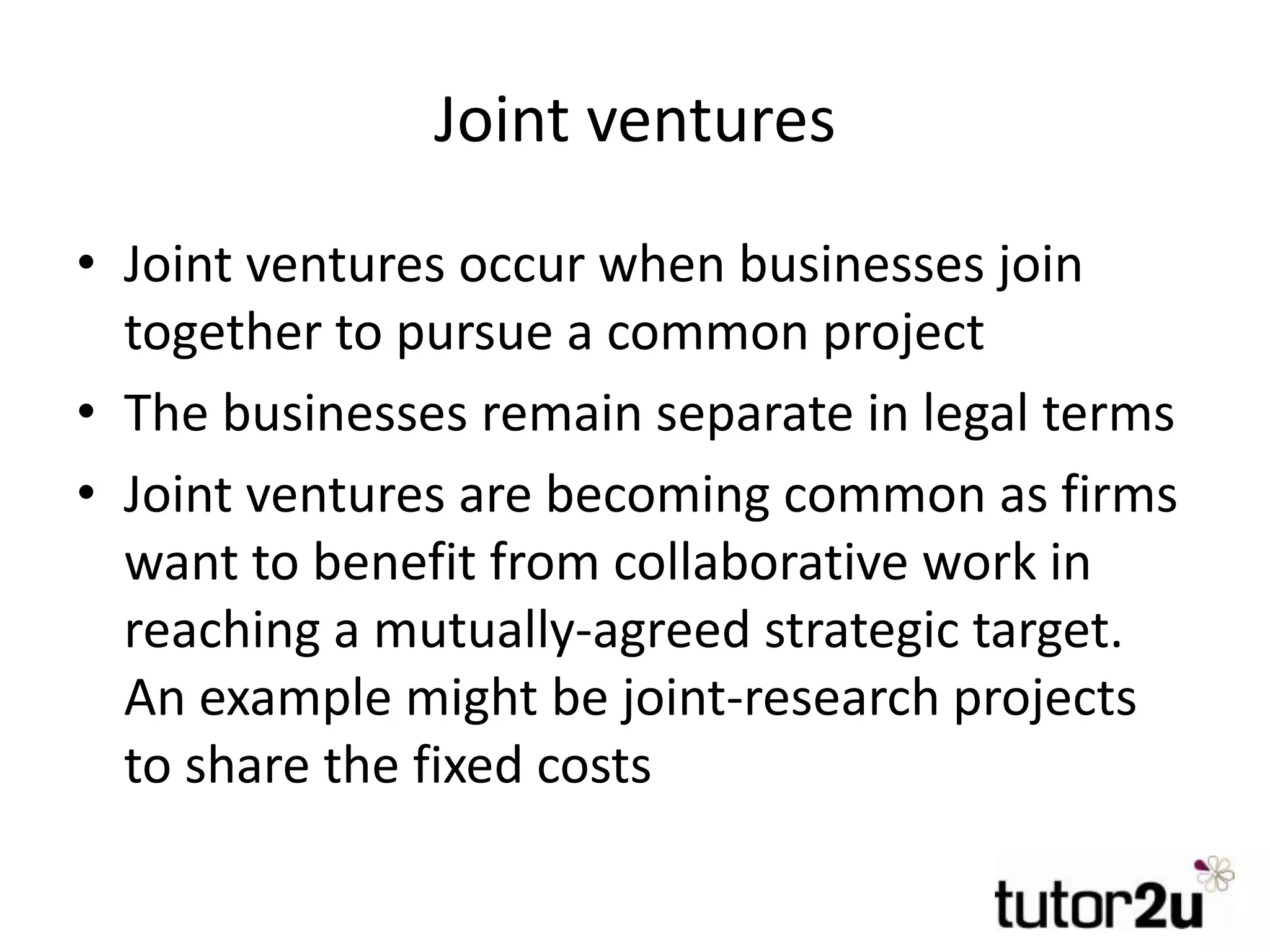

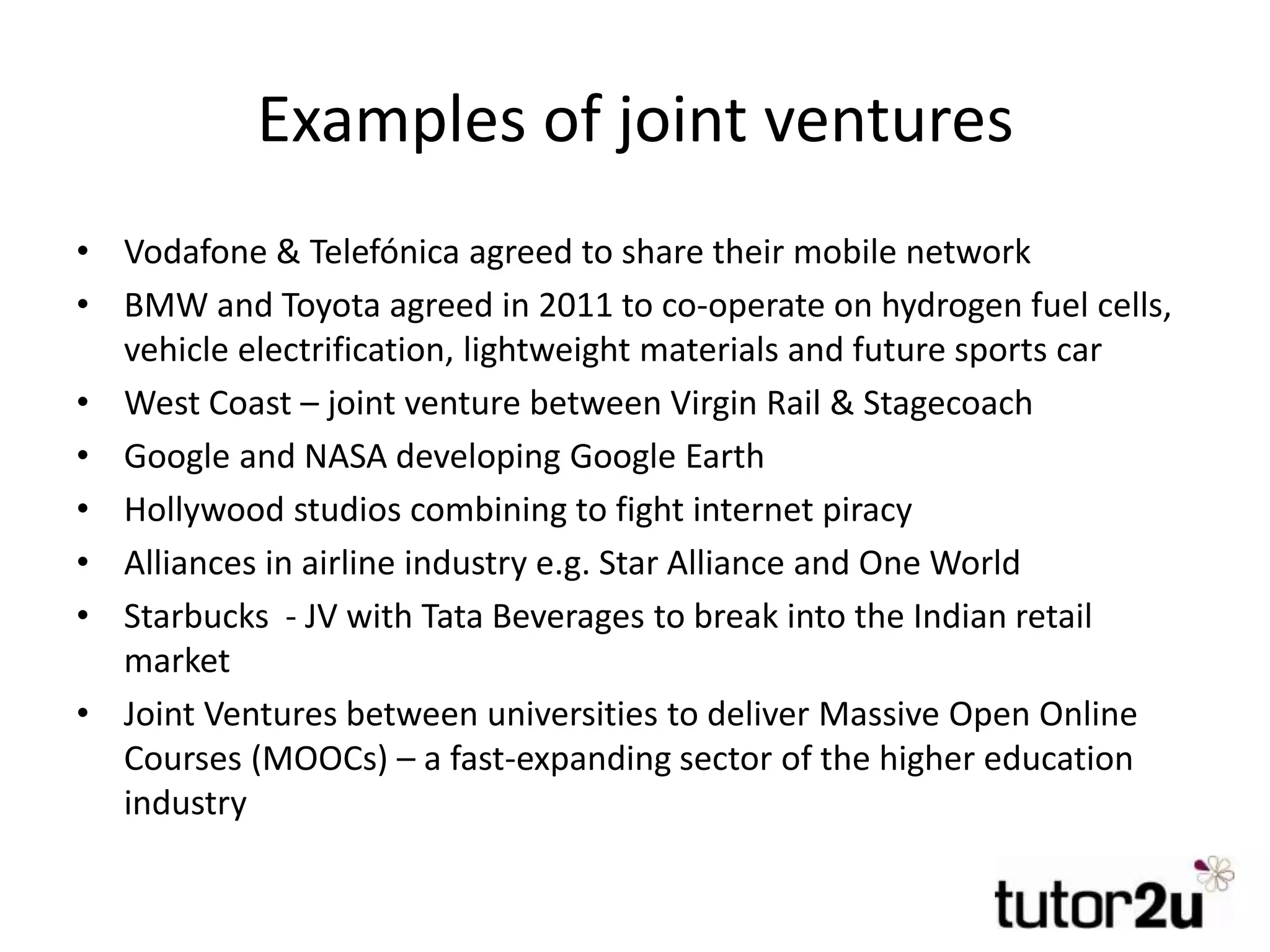

Overview of joint ventures, their purpose, and examples of firms using collaborative projects for shared benefits.

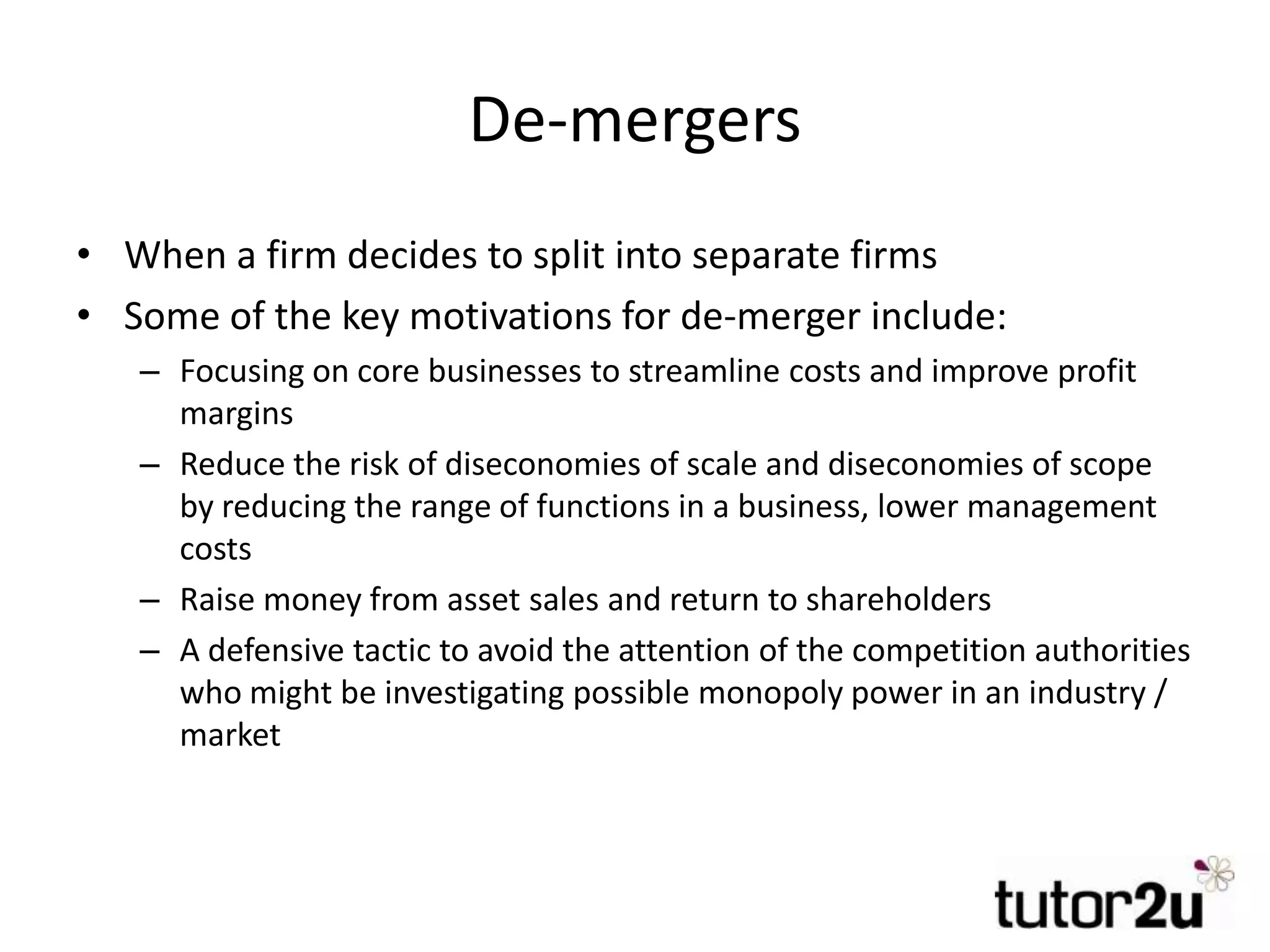

Definition of demergers and motivations including focus on core businesses, reducing costs, and asset sales.

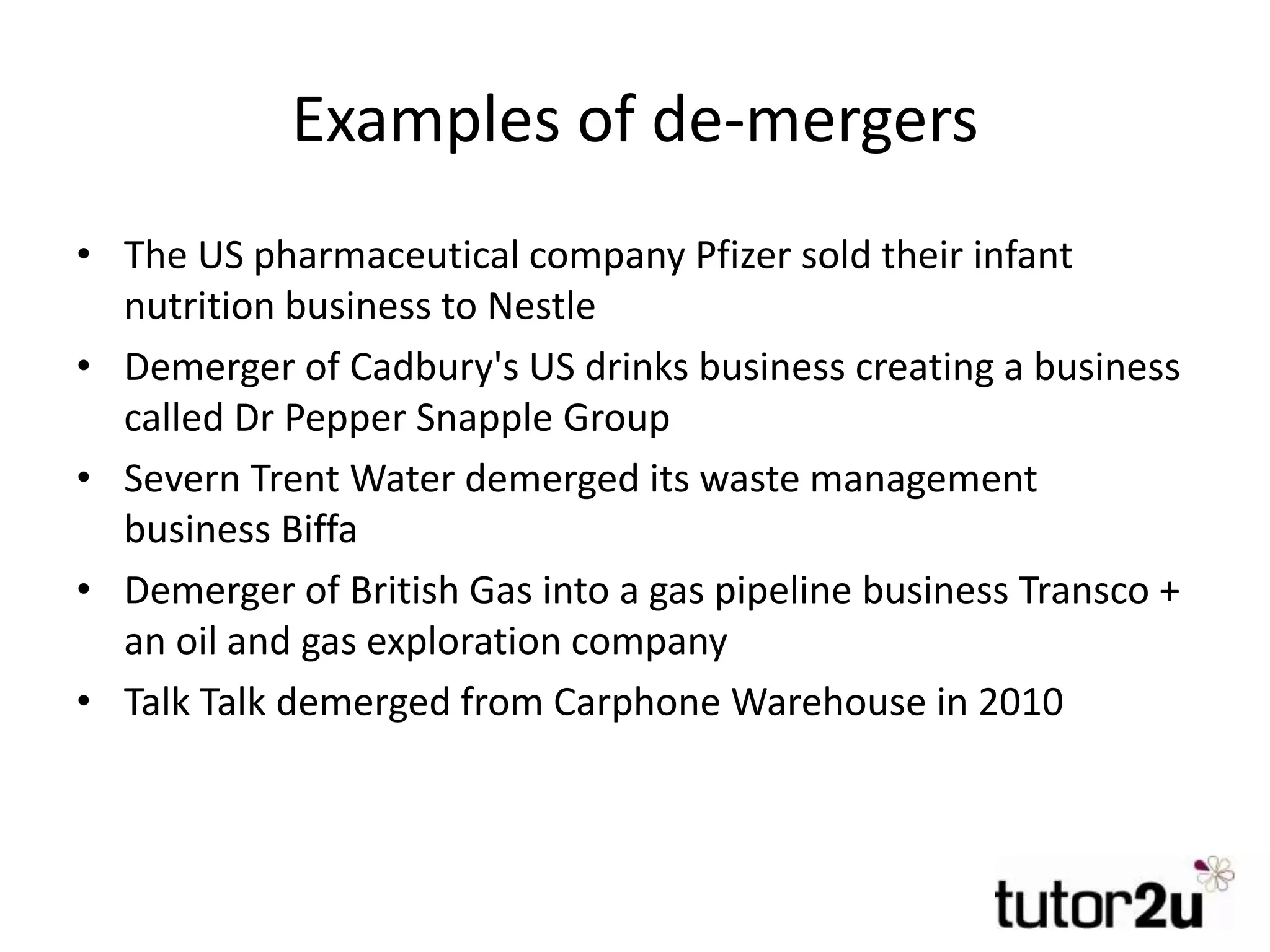

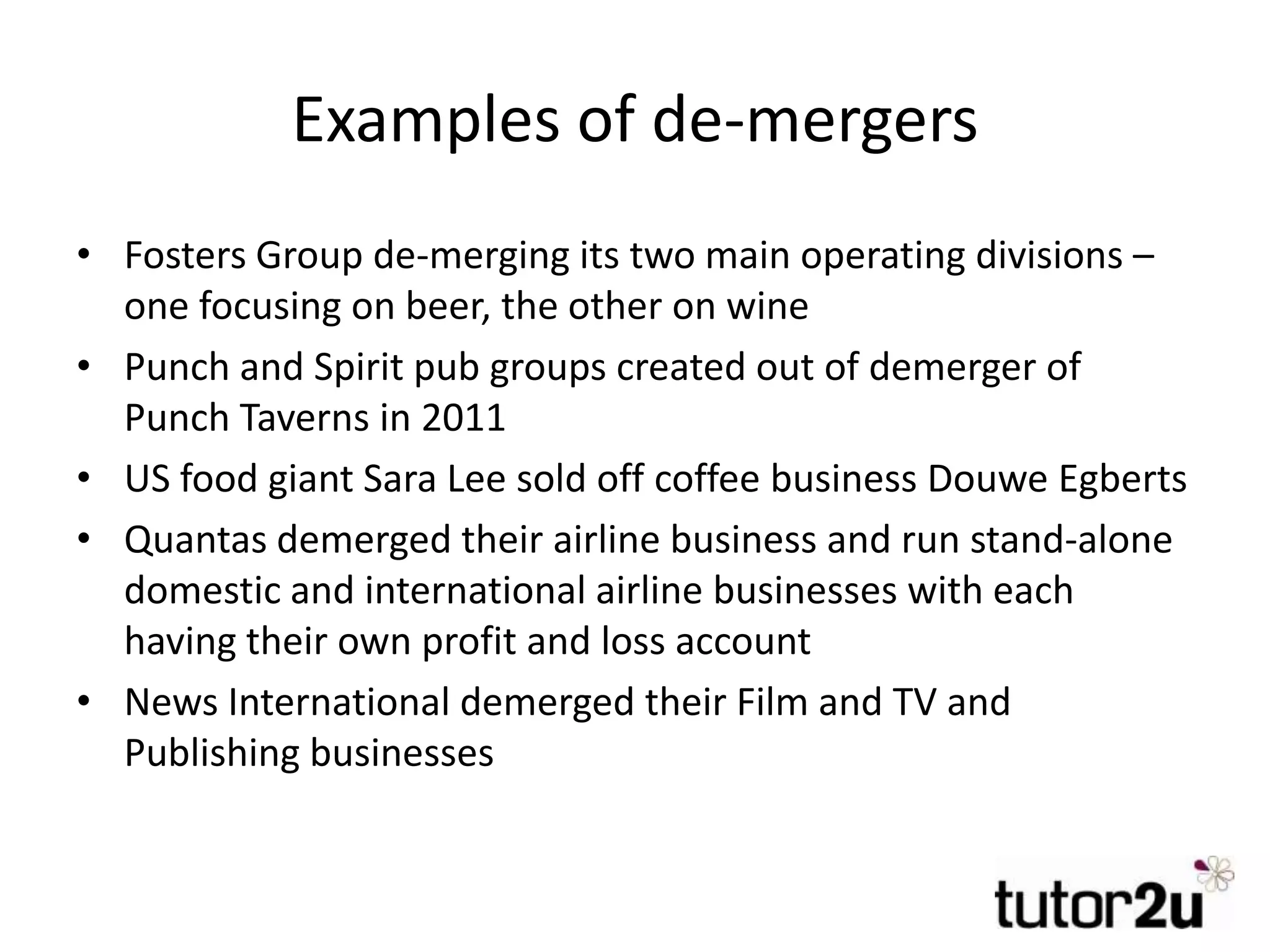

Examples of significant demergers and their implications on firms, focusing on streamlining operations and enhancing market power.

![Pcf (2) 4_mergers_and_acquisitions[2] ms](https://cdn.slidesharecdn.com/ss_thumbnails/pcf24mergersandacquisitions2ms-120403071025-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)