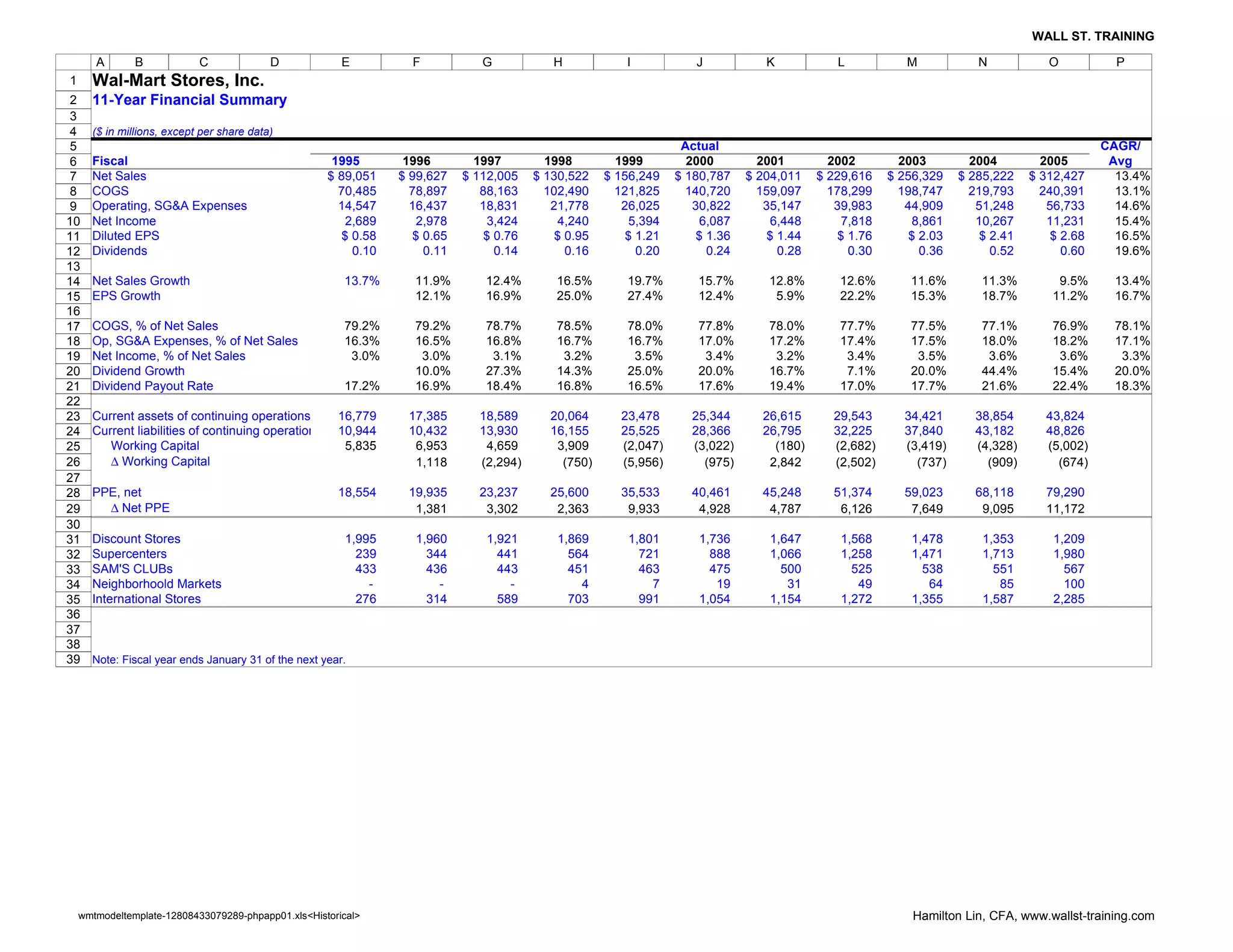

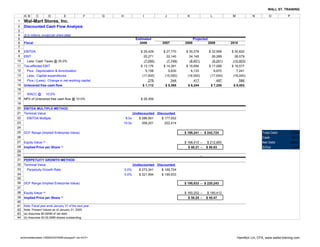

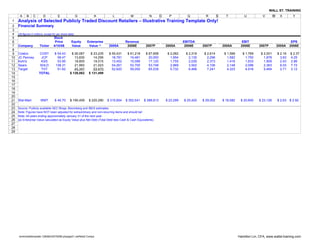

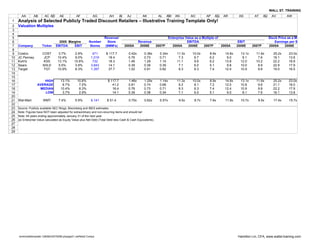

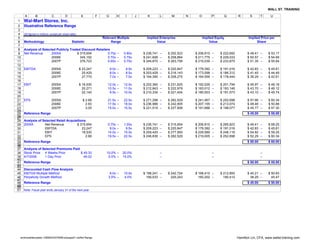

The document provides an 11-year financial summary of Wal-Mart Stores, Inc. from 1995 to 2005, showing key metrics such as net sales, operating expenses, net income, and earnings per share grew at a compound annual growth rate of around 15%. It also includes projections for financial statements such as the income statement and balance sheet from 2006 to 2010, with assumptions around revenue, expense, and capital expenditure growth rates.