Downloaded 12 times

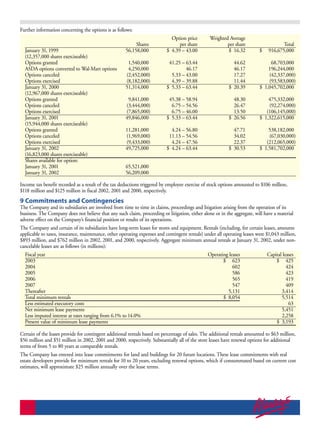

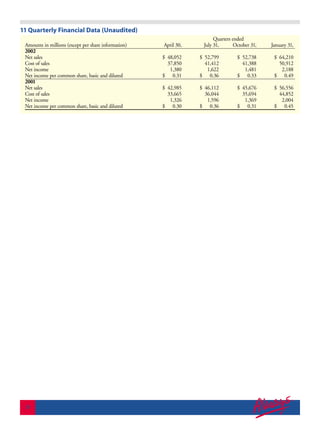

This document provides an 11-year financial summary for Walmart from 1992-2002. Some key details include: - Net sales increased 14% in 2002 to $217.8 billion, with a 6% increase in domestic store sales. Operating expenses rose slightly as a percentage of sales. - Earnings per share were $1.49 in 2002, up from $1.41 in 2001. Return on assets was 8.5% and return on equity was 20.1%. - The number of U.S. stores grew to include over 1,000 Supercenters and 500 SAM'S Clubs, with international units totaling over 1,170.