Download to read offline

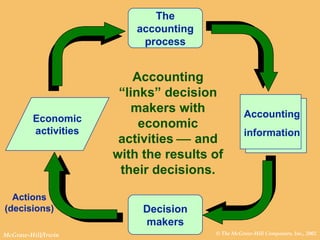

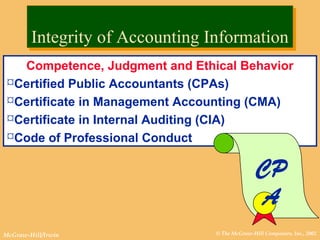

This document discusses accounting information and its uses. It describes how accounting links decision makers with economic activities and results. There are three main types of accounting: financial, managerial, and tax. Accounting information supports decision making and is used by various internal and external users. Financial reporting aims to provide information to investors and creditors about resources, claims on resources, and cash flows. Managerial reporting aims to provide information for assessing performance and directing future actions. Integrity of accounting information is supported by generally accepted accounting principles, oversight bodies, professional organizations, and competency requirements for accountants.