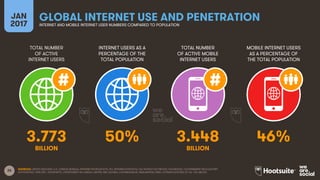

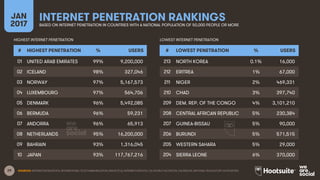

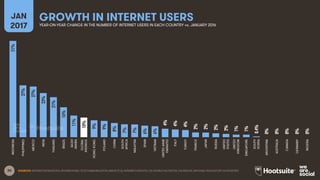

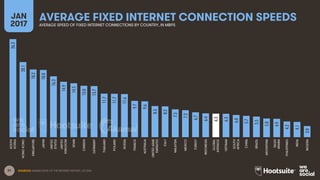

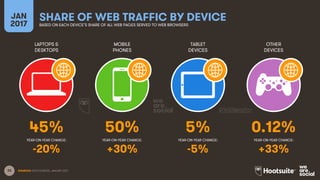

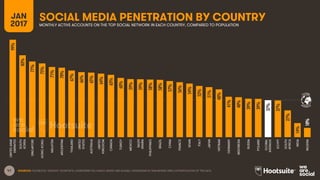

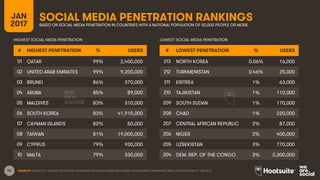

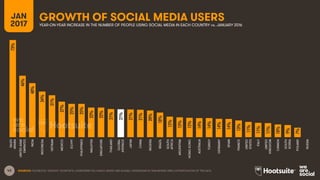

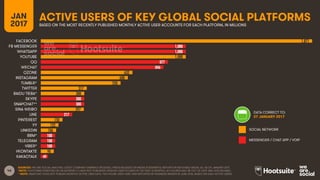

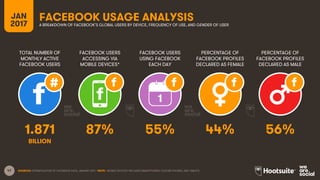

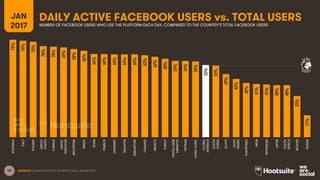

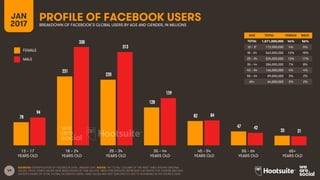

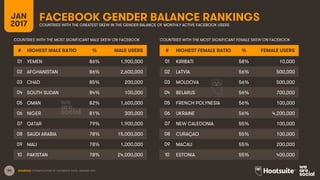

Downloaded 12 times

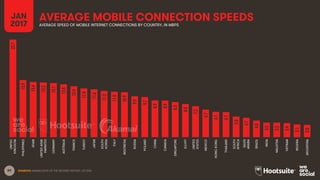

![32

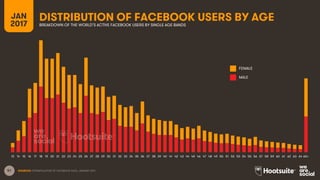

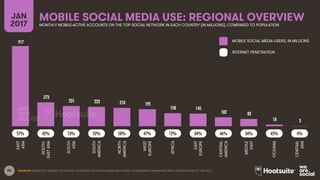

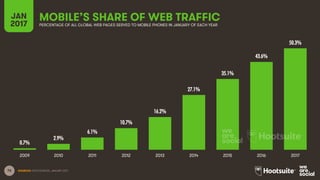

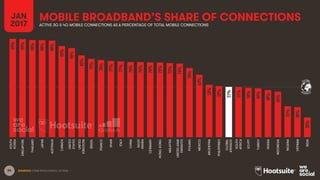

TIME SPENT ON THE INTERNETJAN

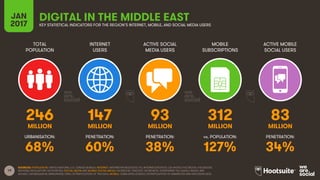

2017 AVERAGE NUMBER OF HOURS SPENT USING THE INTERNET PER DAY, SPLIT BY COMPUTER USE AND MOBILE PHONE USE [SURVEY BASED]

05:23

04:59

04:35

04:48

04:47

04:47

04:27

04:59

04:37

04:01

04:27

03:25

04:19

03:47

04:20

04:19

03:17

04:13

04:01

03:33

04:06

04:00

04:09

03:36

03:42

02:49

03:40

03:26

03:09

03:36

03:56

04:14

03:55

03:43

03:35

03:44

03:03

03:22

03:54

03:20

03:51

02:33

02:59

02:21

02:02

03:04

01:58

02:08

02:26

01:42

01:47

01:33

01:53

01:36

02:04

01:08

01:16

00:57

PHILIPPINES

BRAZIL

THAILAND

INDONESIA

MALAYSIA

MEXICO

ARGENTINA

SOUTH

AFRICA

INDIA

UNITEDARAB

EMIRATES

EGYPT

SAUDI

ARABIA

VIETNAM

TURKEY

SINGAPORE

UNITED

STATES

CHINA

RUSSIA

ITALY

HONGKONG

CANADA

UNITED

KINGDOM

POLAND

SPAIN

AUSTRALIA

SOUTH

KOREA

FRANCE

GERMANY

JAPAN

SOURCES: GLOBALWEBINDEX, Q3 & Q4 2016. BASED ON A SURVEY OF INTERNET USERS AGED 16-64.

NOTE THAT TIMES CAN BE ADDED TOGETHER TO FIND TOTAL INTERNET TIME BY COUNTRY; RANKINGS ARE IN ORDER OF TOTAL TIME SPENT USING THE INTERNET EACH DAY

ACCESS THROUGH LAPTOP / DESKTOP

ACCESS THROUGH MOBILE DEVICE](https://image.slidesharecdn.com/08digitalin2017regionaloverviews-wearesocialandhootsuite-v001-170124010014-180304193246/85/we-are-social-SG-Report-2017-32-320.jpg)

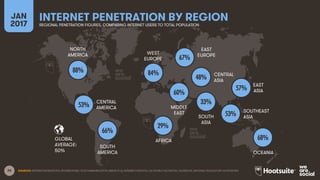

![45

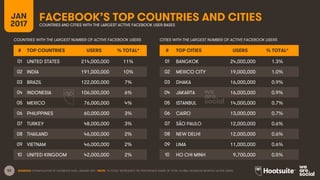

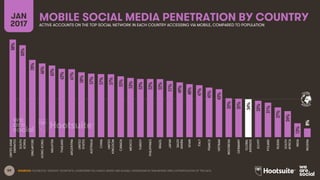

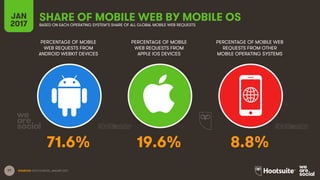

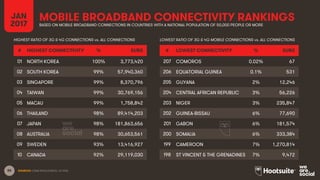

TIME SPENT ON SOCIAL MEDIAJAN

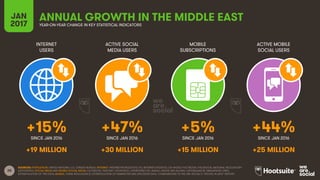

2017 AVERAGE NUMBER OF HOURS THAT SOCIAL MEDIA USERS SPEND USING SOCIAL MEDIA EACH DAY [SURVEY BASED]

04:17

03:43

03:32

03:32

03:24

03:19

03:16

03:10

03:01

02:55

02:54

02:48

02:39

02:36

02:19

02:07

02:06

02:00

01:50

01:48

01:47

01:45

01:41

01:41

01:39

01:23

01:11

01:09

00:40

PHILIPPINES

BRAZIL

ARGENTINA

MEXICO

UNITEDARAB

EMIRATES

MALAYSIA

INDONESIA

EGYPT

TURKEY

SAUDI

ARABIA

SOUTH

AFRICA

THAILAND

VIETNAM

INDIA

RUSSIA

SINGAPORE

UNITED

STATES

ITALY

CHINA

UNITED

KINGDOM

CANADA

POLAND

HONGKONG

SPAIN

AUSTRALIA

FRANCE

SOUTH

KOREA

GERMANY

JAPAN

SOURCES: GLOBALWEBINDEX, Q3 & Q4 2016. BASED ON A SURVEY OF INTERNET USERS AGED 16-64.](https://image.slidesharecdn.com/08digitalin2017regionaloverviews-wearesocialandhootsuite-v001-170124010014-180304193246/85/we-are-social-SG-Report-2017-45-320.jpg)

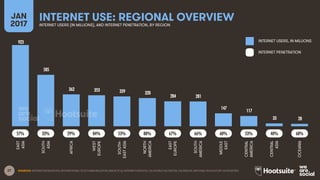

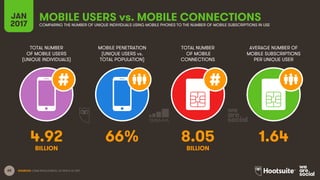

![88

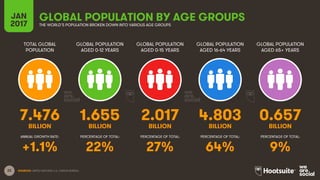

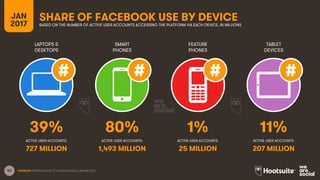

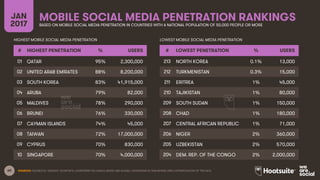

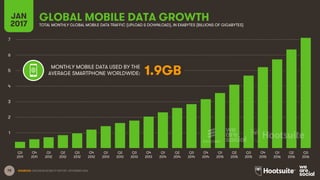

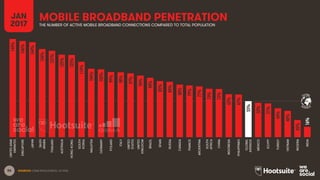

TIME SPENT USING MOBILE INTERNET

SOURCES: GLOBALWEBINDEX, Q3 & Q4 2016. BASED ON A SURVEY OF INTERNET USERS AGED 16-64.

JAN

2017 AVERAGE NUMBER OF HOURS THAT INTERNET USERS SPEND ACCESSING THE INTERNET VIA A MOBILE PHONE EACH DAY [SURVEY BASED]

04:14

03:56

03:55

03:54

03:51

03:44

03:43

03:36

03:35

03:22

03:20

03:04

03:03

02:59

02:33

02:26

02:21

02:08

02:04

02:02

01:58

01:53

01:47

01:42

01:36

01:33

01:16

01:08

00:57

THAILAND

BRAZIL

INDONESIA

UNITEDARAB

EMIRATES

SAUDI

ARABIA

ARGENTINA

MALAYSIA

PHILIPPINES

MEXICO

INDIA

EGYPT

CHINA

SOUTH

AFRICA

TURKEY

VIETNAM

HONGKONG

SINGAPORE

ITALY

SOUTH

KOREA

UNITED

STATES

RUSSIA

SPAIN

UNITED

KINGDOM

CANADA

AUSTRALIA

POLAND

GERMANY

FRANCE

JAPAN](https://image.slidesharecdn.com/08digitalin2017regionaloverviews-wearesocialandhootsuite-v001-170124010014-180304193246/85/we-are-social-SG-Report-2017-88-320.jpg)

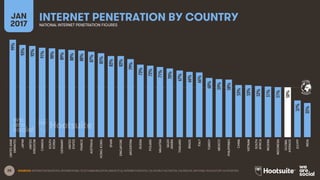

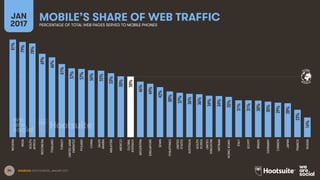

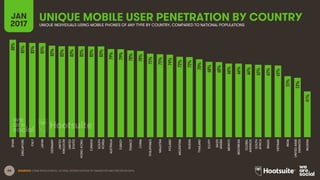

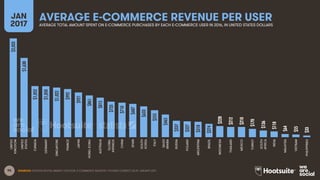

![92

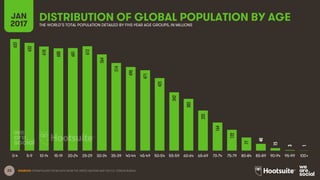

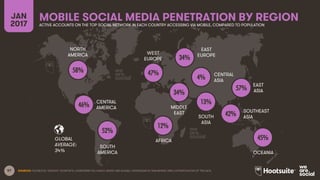

ACTIVE E-COMMERCE PENETRATIONJAN

2017 PERCENTAGE OF THE NATIONAL POPULATION WHO BOUGHT SOMETHING ONLINE IN THE PAST MONTH [SURVEY-BASED]

76%

72%

72%

68%

67%

62%

62%

60%

60%

60%

59%

58%

55%

52%

51%

48%

46%

46%

45%

45%

43%

41%

39%

39%

38%

37%

28%

28%

16%

UNITED

KINGDOM

SOUTH

KOREA

GERMANY

JAPAN

UNITED

STATES

UNITEDARAB

EMIRATES

FRANCE

CANADA

SINGAPORE

AUSTRALIA

HONGKONG

SPAIN

POLAND

MALAYSIA

THAILAND

ARGENTINA

ITALY

RUSSIA

CHINA

BRAZIL

TURKEY

INDONESIA

SAUDI

ARABIA

VIETNAM

PHILIPPINES

MEXICO

INDIA

SOUTH

AFRICA

EGYPT

SOURCES: GLOBALWEBINDEX, Q3 & Q4 2016. BASED ON A SURVEY OF INTERNET USERS AGED 16-64. NOTE: DATA HAS BEEN REBASED TO SHOW

TOTAL NATIONAL PENETRATION. PENETRATION FIGURES BASED ON POPULATION DATA FROM THE UNITED NATIONS AND THE U.S. CENSUS BUREAU.](https://image.slidesharecdn.com/08digitalin2017regionaloverviews-wearesocialandhootsuite-v001-170124010014-180304193246/85/we-are-social-SG-Report-2017-92-320.jpg)

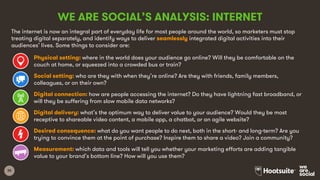

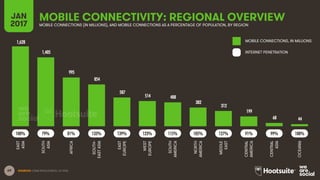

![93

ACTIVE M-COMMERCE PENETRATIONJAN

2017 PERCENTAGE OF THE POPULATION WHO BOUGHT SOMETHING ONLINE VIA A PHONE IN THE PAST MONTH [SURVEY-BASED]

55%

47%

41%

40%

40%

38%

37%

36%

33%

33%

33%

31%

30%

28%

27%

26%

26%

26%

25%

25%

23%

23%

23%

23%

21%

21%

19%

15%

11%

SOUTH

KOREA

UNITEDARAB

EMIRATES

THAILAND

CHINA

SINGAPORE

MALAYSIA

UNITED

KINGDOM

HONGKONG

INDONESIA

SAUDI

ARABIA

UNITED

STATES

TURKEY

SPAIN

VIETNAM

AUSTRALIA

BRAZIL

PHILIPPINES

GERMANY

CANADA

JAPAN

ITALY

ARGENTINA

POLAND

INDIA

RUSSIA

MEXICO

FRANCE

SOUTH

AFRICA

EGYPT

SOURCES: GLOBALWEBINDEX, Q3 & Q4 2016. BASED ON A SURVEY OF INTERNET USERS AGED 16-64. NOTE: DATA HAS BEEN REBASED TO SHOW

TOTAL NATIONAL PENETRATION. PENETRATION FIGURES BASED ON POPULATION DATA FROM THE UNITED NATIONS AND THE U.S. CENSUS BUREAU.](https://image.slidesharecdn.com/08digitalin2017regionaloverviews-wearesocialandhootsuite-v001-170124010014-180304193246/85/we-are-social-SG-Report-2017-93-320.jpg)

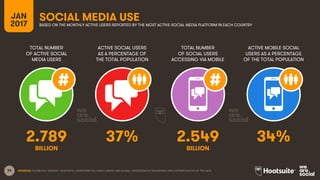

![94

GROWTH OF M-COMMERCE SHOPPERSJAN

2017 YEAR-ON-YEAR GROWTH IN THE NUMBER OF PEOPLE PURCHASING ONLINE VIA A PHONE [SURVEY-BASED]

SOURCES: GLOBALWEBINDEX, Q4 2015, AND Q3 & Q4 2016. BASED ON A SURVEY OF INTERNET USERS AGED 16-64.

PENETRATION FIGURES BASED ON POPULATION DATA FROM THE UNITED NATIONS AND THE U.S. CENSUS BUREAU.

155%

101%

85%

68%

64%

60%

57%

45%

45%

42%

40%

39%

36%

36%

32%

31%

31%

29%

28%

28%

26%

26%

25%

25%

25%

15%

6%

-1%

INDONESIA

JAPAN

PHILIPPINES

INDIA

MEXICO

THAILAND

SAUDI

ARABIA

RUSSIA

CANADA

BRAZIL

AUSTRALIA

UNITED

KINGDOM

VIETNAM

SINGAPORE

TURKEY

MALAYSIA

SOUTH

AFRICA

HONG

KONG

SOUTH

KOREA

POLAND

GERMANY

UNITED

STATES

FRANCE

CHINA

UNITEDARAB

EMIRATES

SPAIN

ITALY

ARGENTINA](https://image.slidesharecdn.com/08digitalin2017regionaloverviews-wearesocialandhootsuite-v001-170124010014-180304193246/85/we-are-social-SG-Report-2017-94-320.jpg)

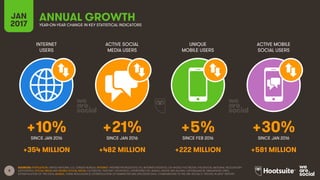

The document provides an overview of global digital trends in 2017. Some key findings include: - More than half the world's population now uses the internet, with over 3.75 billion online. - Mobile internet and social media usage grew substantially over the past year, with over 2.5 billion active mobile social media users. - Internet and smartphone penetration continues to increase globally, with 55% of mobile connections now coming from smartphones. - The report contains detailed statistics on internet, social media, and mobile usage broken down by region.