Download as PDF, PPTX

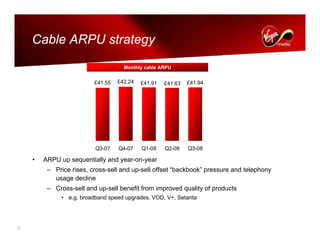

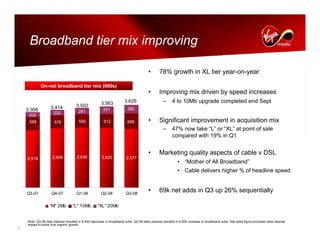

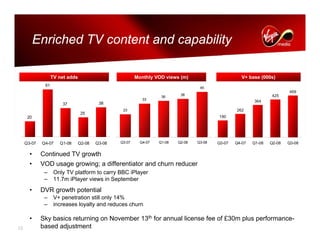

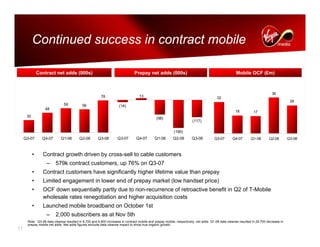

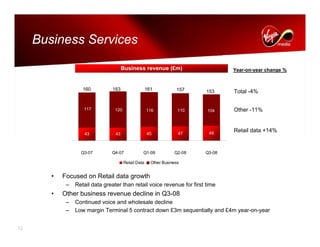

This document provides a summary of Virgin Media's financial results for the third quarter of 2008. It reports that Virgin Media continued to see growth in key metrics such as on-net customer additions, broadband and TV subscriber growth, and improving triple play penetration. ARPU increased through price increases, cross-selling, and upselling efforts. Mobile contract customer growth was strong through cross-selling to cable customers. Content revenues increased for VMtv but declined for Sit-Up. Overall revenue was flat, while operating cash flow and margins declined slightly compared to last year. Capital expenditures remained high to continue network upgrades and expand service offerings.