Download as PDF, PPTX

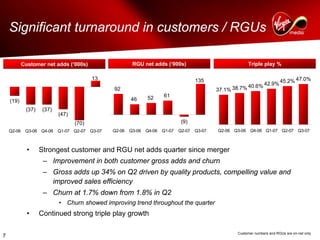

This document provides a summary of Virgin Media's financial results for the third quarter of 2007. It discusses improvements in customer and revenue growth metrics compared to previous quarters. Specifically, it notes record quarterly gross additions and reduced churn. It also summarizes growth in the company's broadband, TV, telephony, mobile, and business services segments. The document concludes with discussions of operating cash flow, revenue, and net debt levels.