1) The doctrine of utmost good faith, or uberrimae fidei, requires that parties entering an insurance contract disclose all material facts honestly and not mislead each other.

2) Violations of this duty can lead to the contract being voidable if there are intentional misrepresentations or fraudulent concealment of material facts.

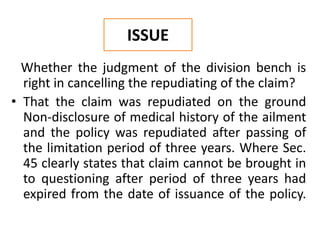

3) Under the Marine Insurance Act of 1963, marine insurance contracts specifically must be made in "utmost good faith" or either party can cancel the contract.