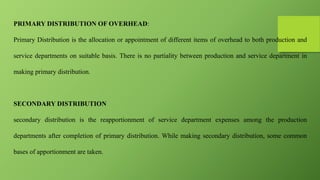

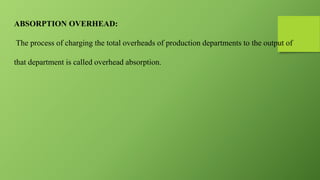

Overheads are business costs that cannot be traced to a specific activity and instead support overall revenue generation. There are various ways to classify overheads, including by function (e.g. manufacturing, selling), behavior (e.g. fixed, variable), element (e.g. materials, labor), controllability, and normality. Overheads are departmentalized by allocating expenses to cost centers like manufacturing or service departments. Primary distribution allocates overhead to departments, while secondary distribution reapportions service department expenses among production departments. Total overhead costs are then absorbed into the output of each production department.