Unit 4 Outcome 1B - Solutions v1a

•

0 likes•722 views

The document summarizes accounting concepts related to inventory valuation, balance day adjustments, and revenue recognition. It provides multiple examples and calculations to illustrate: (1) depreciation of non-current assets using reducing balance and straight-line methods, (2) treatment of prepaid and accrued revenues, and (3) accounting for asset disposals. The examples cover a range of scenarios for businesses including a delivery van, computer systems, and gym equipment.

Recommended

More Related Content

What's hot

What's hot (17)

Viewers also liked

Viewers also liked (20)

Similar to Unit 4 Outcome 1B - Solutions v1a

Similar to Unit 4 Outcome 1B - Solutions v1a (20)

More from VCE Accounting - Michael Allison

More from VCE Accounting - Michael Allison (20)

Recently uploaded

Recently uploaded (20)

Unit 4 Outcome 1B - Solutions v1a

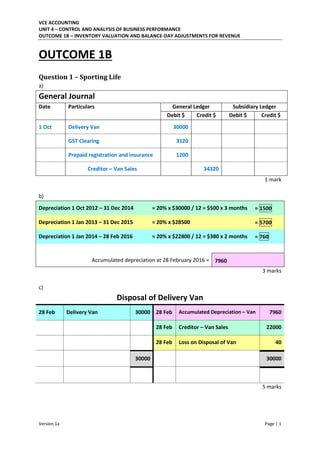

- 1. VCE ACCOUNTING UNIT 4 – CONTROL AND ANALYSIS OF BUSINESS PERFORMANCE OUTCOME 1B – INVENTORY VALUATION AND BALANCE-DAY ADJUSTMENTS FOR REVENUE Version 1a Page | 1 OUTCOME 1B Question 1 – Sporting Life a) General Journal Date Particulars General Ledger Subsidiary Ledger Debit $ Credit $ Debit $ Credit $ 1 Oct Delivery Van 30000 GST Clearing 3120 Prepaid registration and insurance 1200 Creditor – Van Sales 34320 1 mark b) Depreciation 1 Oct 2012 – 31 Dec 2014 = 20% x $30000 / 12 = $500 x 3 months = 1500 Depreciation 1 Jan 2013 – 31 Dec 2015 = 20% x $28500 = 5700 Depreciation 1 Jan 2014 – 28 Feb 2016 = 20% x $22800 / 12 = $380 x 2 months = 760 Accumulated depreciation at 28 February 2016 = 7960 3 marks c) Disposal of Delivery Van 28 Feb Delivery Van 30000 28 Feb Accumulated Depreciation – Van 7960 28 Feb Creditor – Van Sales 22000 28 Feb Loss on Disposal of Van 40 30000 30000 5 marks

- 2. VCE ACCOUNTING UNIT 4 – CONTROL AND ANALYSIS OF BUSINESS PERFORMANCE OUTCOME 1B – INVENTORY VALUATION AND BALANCE-DAY ADJUSTMENTS FOR REVENUE Version 1a Page | 2 Question 2 – Greenfinger Nursery a) Calculation Depreciation expense Accumulated depreciation 1 Jul – 31 Dec 2014 = 5000 x 30% = 1500 / 2 (6 months) = 750 = 750 1 Jan – 31 Dec 2015 = 5000 x 30% = 1500 = 750 + 1500 Accumulated Depreciation = $ 2250 2 marks b) Calculation Existing computers = 25000 x 30% = 7500 New computer on 1 Apr 16 = 4000 x 30% = 1200 / 12 = $100 per month x 9 months = 900 Depreciation Expense = $ 8400 2 marks c) Computer System 1 Jan Balance 30000 31 Jan Disposal of computer sys. 5000 30 Apr Bank/Sund Cred – B Comps 4000 31 Dec Balance 29000 34000 34000 1 Jan Balance 29000 Disposal of Computer System 31 Jan Computer system 5000 31 Jan A . dep’ – Computer sy 2250 31 Jan Bank 2000 31 Jan Loss on disposal of comp. 750 5000 5000 3 + 4 = 7 marks

- 3. VCE ACCOUNTING UNIT 4 – CONTROL AND ANALYSIS OF BUSINESS PERFORMANCE OUTCOME 1B – INVENTORY VALUATION AND BALANCE-DAY ADJUSTMENTS FOR REVENUE Version 1a Page | 3 Question 3 – Findlay Builders a) Calculation Deprecation = 30% x 45000 / 2 = 6750 Depreciation expense for year ended 30 June 2015 = $ 6750 Calculation Deprecation = 30% x 38250 Depreciation expense for year ended 30 June 2016 = $ 11475 1 + 1 = 2 marks b) i 1 mark = Net Profit would be $4,075 lower 1 mark = depreciation would be $11,475 under the reducing balance method 1 mark = depreciation would be $7,400 under the straight-line method ii 1 mark = Net Profit would be $194 lower 1 mark = depreciation would be $37,194 under the reducing balance method 1 mark = depreciation would be $37,000 under the straight-line method 3 + 3 = 6 marks Calculations: Reducing balance Straight-line Period Length Depreciation Period Length Depreciation 1 Jan 2012 to 30 June 2012 0.5 year $ 6,750.00 1 Jan 2012 to 30 June 2012 0.5 year $ 3,700.00 1 July 2013 to 30 June 2013 1 year $ 11,475.00 1 July 2013 to 30 June 2013 1 year $ 7,400.00 1 July 2014 to 30 June 2014 1 year $ 8,032.50 1 July 2014 to 30 June 2014 1 year $ 7,400.00 1 July 2015 to 30 June 2015 1 year $ 5,622.75 1 July 2015 to 30 June 2015 1 year $ 7,400.00 1 July 2016 to 30 June 2016 1 year $ 3,935.93 1 July 2016 to 30 June 2016 1 year $ 7,400.00 1 July 2017 to 31 Dec 2016 0.5 year $ 1,377.57 1 July 2017 to 31 Dec 2016 0.5 year $ 3,700.00 Total $ 37,193.75 Total $ 37,000.00

- 4. VCE ACCOUNTING UNIT 4 – CONTROL AND ANALYSIS OF BUSINESS PERFORMANCE OUTCOME 1B – INVENTORY VALUATION AND BALANCE-DAY ADJUSTMENTS FOR REVENUE Version 1a Page | 4 c) Discussion 2 marks The depreciation method should ’t e ha ged based on the Consistency Principle because: The firm must continue using the same accounting methods and the straight-line method was used in previous years. This will the fir ’s Depreciation Expense and Net Profit are comparable over time. 2 marks However, the depreciation method should be changed based on the Reporting Period Principle. The depreciation method should be chosen which best matches the Revenue Earned with Expenses Incurred of the asset. As a computer gets less efficient and earns less Revenue as it gets older, the reducing-balance should be used as it will match less Depreciation Expenses. 4 marks

- 5. VCE ACCOUNTING UNIT 4 – CONTROL AND ANALYSIS OF BUSINESS PERFORMANCE OUTCOME 1B – INVENTORY VALUATION AND BALANCE-DAY ADJUSTMENTS FOR REVENUE Version 1a Page | 5 Question 4 – Denise’s Quilts a) Depreciation method 1 mark = Reducing balance depreciation Accounting principle 1 mark = Reporting period principle Justification 1 mark At the end of each period, the firm must calculate profit by matching revenues earned and expenses incurred. 1 mark 3Reducing balance is more effective at at hi g the deli er a ’s e pe se depre iatio against its revenue as: o More depreciation is charged in earlier periods when the van earns more revenue o Less depreciation is charged in later periods when the van earns less revenue 1 + 1 + 2 = 4 marks b) Calculation Depreciation = 20% x (50,000 – 10,000 – 8,000 – 6,400) = 20% x 25,600 Depreciation expense for year ended 31 December 2013 = $ 5,120 2 marks c) Calculation Depreciation = (Cost – Residual) / Life 5,000 = (40,000 – 10,000) / Life 6 = Life Estimated useful life of asset = 6 years 2 marks

- 6. VCE ACCOUNTING UNIT 4 – CONTROL AND ANALYSIS OF BUSINESS PERFORMANCE OUTCOME 1B – INVENTORY VALUATION AND BALANCE-DAY ADJUSTMENTS FOR REVENUE Version 1a Page | 6 Question 5 – Gym World a) Explanation The deposit should be treated as a liability because: 1 mark = the firm has a present obligation to provide the treadmills to the customer. 1 mark = the obligation arises because of a past event when the firm received a $15,000 deposit. 1 mark = there will be a future outflow of economic benefits (in the form of treadmills) 3 marks b) Cash Receipts Journal Date Details Receipt Number Bank $ Debtors Control $ Cost of Sales $ Sales $ Sundries $ GST $ 5 Jun Prepaid sales revenue 48 15000 15000 1 mark c) Sales Journal Date Debtor Invoice Number Cost of Sales $ Sales $ GST $ Debtors Control $ 16 Jun Golden Gyms 45 12500 35000 5000 40000 General Journal Date Particulars General Ledger Subsidiary Ledger Debit $ Credit $ Debit $ Credit $ 16 Jun Prepaid sales revenue 15000 Sales revenue 15000 3 + 1 = 4 marks

- 7. VCE ACCOUNTING UNIT 4 – CONTROL AND ANALYSIS OF BUSINESS PERFORMANCE OUTCOME 1B – INVENTORY VALUATION AND BALANCE-DAY ADJUSTMENTS FOR REVENUE Version 1a Page | 7 d) Prepaid Sales Revenue 30 Jun Sales revenue 15000 30 Jun Bank 15000 15000 15000 3 marks e) General Journal Date Particulars General Ledger Subsidiary Ledger Debit $ Credit $ Debit $ Credit $ 30 Jun Accrued interest revenue 450 Interest revenue 450 Cash Receipts Journal Date Details Receipt Number Bank $ Debtors Control $ Cost of Sales $ Sales $ Sundries $ GST $ 30 Sep Accrued interest revenue 15 900 450 Interest revenue 450 31 Mar Term deposit 107 20900 20000 Interest revenue 900 2 + 2 + 2 = 6 marks f) Explanation If the adjustment for $450 of Accrued Revenue was NOT made then: 1 mark Assets would be understated by $450 – in this case, the Accrued Interest Revenue asset would be too low. 1 mark Liabilities would not be effected. 1 mark O er’s Equity would understated by $450 – i this case, the fir ’s Interest Revenue would be too low. 3 marks