Downloaded 22 times

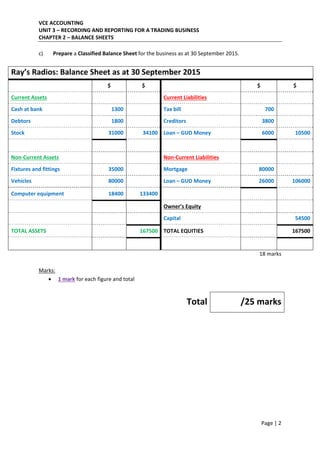

This document provides information about classifying items on a balance sheet for a trading business. It defines current assets as assets that will be turned into cash or used within 12 months, giving the example of cash at bank. It defines non-current liabilities as obligations due after 12 months, giving mortgages as an example. It explains that classifying items by current/non-current assists the business with decision making, such as prioritizing payment of liabilities. Finally, it provides a sample classified balance sheet for a business called Ray's Radios with current and non-current assets and liabilities, including cash, debtors, stock, fixtures, vehicles, computer equipment, tax bill, creditors, loans, mortgage,