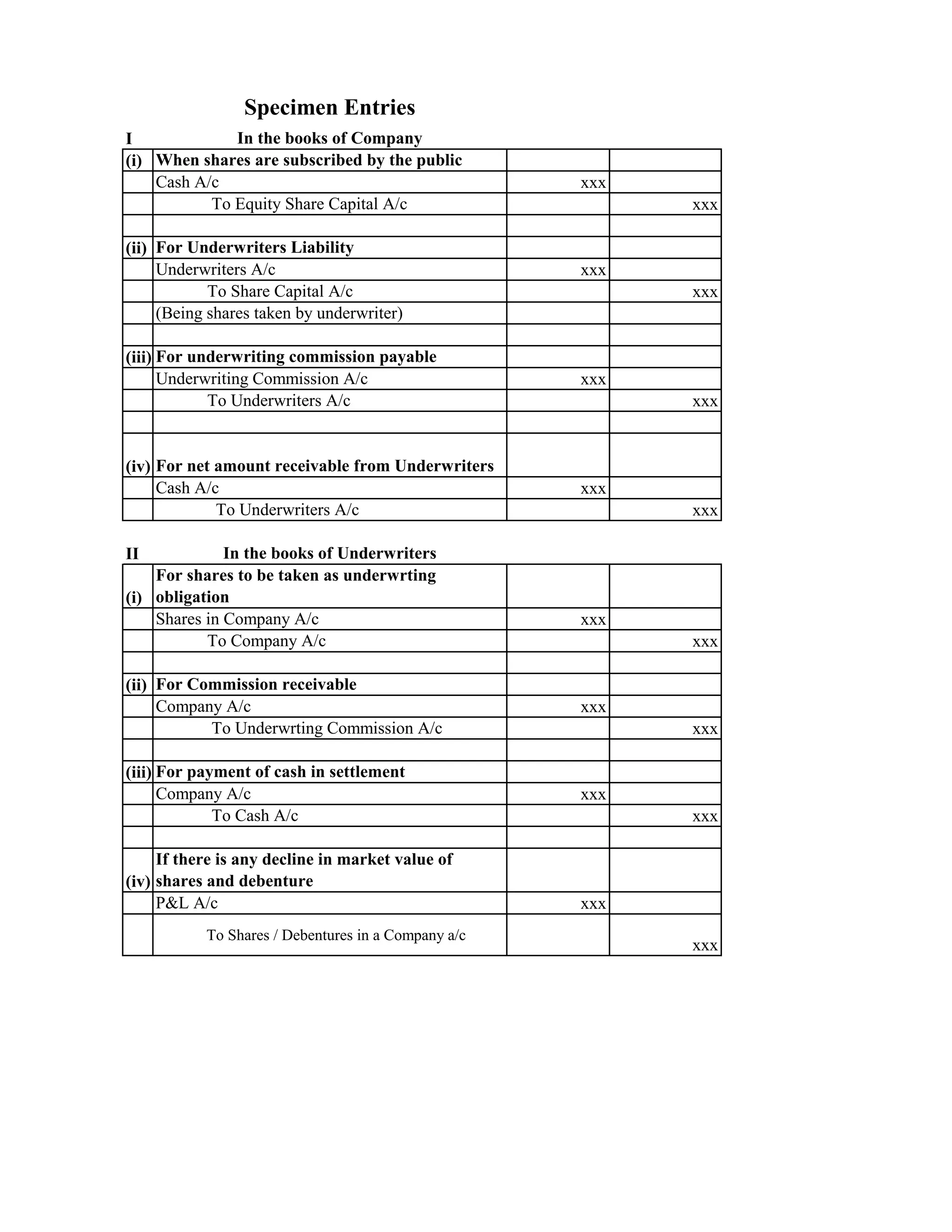

The document outlines specimen journal entries for recording underwriting transactions in the books of the company being underwritten and the underwriter. For the company, entries are shown for cash received from public share subscriptions, shares received from the underwriter, underwriting commission payable, and cash receivable from the underwriter. For the underwriter, entries record the obligation to take shares, commission receivable, cash paid to settle with the company, and any loss from a decline in the market value of shares underwritten.