Download as PDF, PPTX

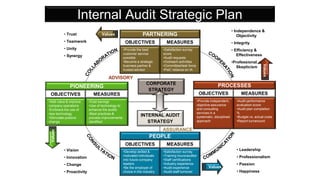

The document outlines strategies for transforming the internal audit function into a data analytics hub within organizations, emphasizing the importance of customer service, integration of new technologies, and proactive evaluations. It details tactical approaches such as market visibility, timing, and collaboration with other data analytic groups while maintaining independence. Ultimately, the goal is to enhance the credibility and effectiveness of internal audits to add value and improve organizational operations.

![2019 07 Bizbok with Archimate 3 v3 [UPDATED !]](https://cdn.slidesharecdn.com/ss_thumbnails/201907bizbokwitharchimate3v3-190722110214-thumbnail.jpg?width=640&height=640&fit=bounds)

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)