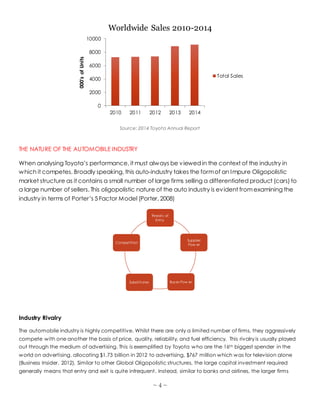

Toyota faced significant challenges during the global recession as vehicle sales declined sharply. However, Toyota has since recovered as the global economy improved. While Toyota remains the largest automaker, it faces challenges like maintaining brand reputation after recalls and managing rising input costs. Opportunities for Toyota include targeting emerging markets with growing demand and investing in fuel efficient technologies.