Introduction

What doyou understand by the following

terms?

Cost?

Price?

Expense?

A Cost Object?

4.

Introduction Cont…

Cancost data compiled for a particular

purpose be appropriate for other use? e.g.

Profit measurement?

Decision making

Since the word cost can mean different things

for different purposes – for cost information

to be at all useful it needs first to be classified

so that managers are able to understand it.

5.

Cost Classification

Fourmost common and useful categorisations

for management accounting purposes

Function – e.g. production, marketing, administration

etc.

Behaviour – e.g. fixed, variable

Nature – e.g. direct, indirect

Element – e.g. material, labour

6.

Classification by “Nature”

A cost that can be easily and accurately

traced/identified with a particular cost

unit/object (e.g. department) is called “Direct

cost”, e.g. timber in furniture.

The cost that is not directly traceable to a

particular cost unit is referred to as an

“Indirect cost” of that unit. Think of the GM

of ABC co. is an indirect cost of each of the

company’s production departments.

7.

Classification by “Element”of Production

Integral elements of production includes: direct

materials, direct labour, direct expenses and

overheads.

Direct materials consist of all those materials that

can be identified with a specific product.

They represent a major cost of producing that

product.

They are principal substances used in production of

finished goods by the addition of labour and

overheads.

8.

Classification by “Element”of production

Cont…

Labour is the physical/mental efforts

expended in the production of a

product/service.

So “direct labour” involves the cost of

salaries, wages, etc, that can directly be traced

to or identified with a particular product.

They represent major labour costs!!

9.

Classification by “Element”of production

Cont…

“Direct expenses” these represents costs that

are directly attributable to the production

process e.g.

hire of special machine tools for one-off jobs,

royalties for patents etc

10.

Overheads

All othercosts – other than direct materials,

labour and expenses – of producing a product.

For instances materials which does not become

an integral part of a finished product and the

cost of personnel who do not work directly on

the product, but whose services are necessary

for the production process are classified as

indirect material and labour respectively.

11.

Total Costs Structuredby Nature and by

Element

Direct material + Indirect materials = Total material cost

Direct Labour + Indirect labour = Total labour cost

Direct expense + Indirect expense = Total expenses

Prime Cost + Overheads = Total cost

In short all direct costs are prime costs of

production; together with overhead they make up the

total cost of a product cost unit

12.

Classification by “Behaviour”

When classifying costs by behaviour the major focus

rests on variable and fixed costs. Though other

‘hybrid’ pattern called step and semi-variable costs

exists.

Cost that is sensitive, and varies in proportion, to

corresponding changes in the activity level is known

as variable cost.

Cost that is insensitive to activity level fluctuations

but is determined by the influence of time (and its

passing) is called fixed cost.

13.

Variable Cost Behaviour

Variable cost comprises of the following:

Variable overheads + direct (prime) costs =

variable costs

Illustration

Assume a firm employs Wamachinga selling “Yebo-

yebo” for commission – only earnings door to door.

Wamachinga are paid a commission of 10% for each

product sold. Yebo-yebos are priced at Tshs. 400.

Required: Provide a graphical and algebraic expressions

of this variable cost pattern. (Linear, non-linear,

curvilinear)

14.

Fixed Cost Behaviour

Fixed (a.k.a period) - cost is said to be fixed

with respect to two factors:

Short-run time periods, i.e. up to and including a full year

Volume (although under very extreme circumstances, such

as complete shutdown where the volume is sustained at zero,

even fixed costs may change or be avoided entirely

All fixed costs are overhead and they are often

alternatively given the full title “fixed overhead costs”

The algebraic expression is Y = a; where ‘Y’ is cost and ‘a’

is a constant.

Fixed overheads are constant/fixed in total!!!

15.

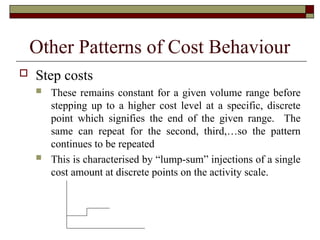

Other Patterns ofCost Behaviour

Step costs

These remains constant for a given volume range before

stepping up to a higher cost level at a specific, discrete

point which signifies the end of the given range. The

same can repeat for the second, third,…so the pattern

continues to be repeated

This is characterised by “lump-sum” injections of a single

cost amount at discrete points on the activity scale.

16.

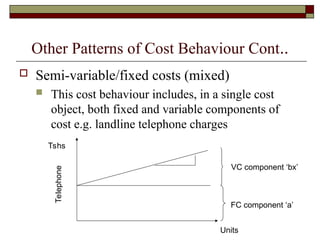

Other Patterns ofCost Behaviour Cont..

Semi-variable/fixed costs (mixed)

This cost behaviour includes, in a single cost

object, both fixed and variable components of

cost e.g. landline telephone charges

Units

FC component ‘a’

VC component ‘bx’

Tshs

Telephone

17.

Cost as Assetsand Expenses

The issue of timing i.e. when should the cost

of acquiring an asset be recognized as an

expense.

Expense - the cost incurred when an asset is used up or

sold for the purpose of generating revenue (when benefits

are received, the cost becomes an expense)

The timing with which various expenses are recognised is

described by the following terms:

Product costs

Period costs

18.

Product Costs

Productcost = a cost of goods purchased or

manufactured for resale (assets).

Are inventoriable costs for reporting on B/S and

P&L

Are used to decide which product to produce and

to determine selling prices

Once the goods are sold, product costs

becomes expenses – called cost of goods sold.

19.

Period Costs

Allcost that are not product costs are

called period costs.

Costs which are not necessary for

production (not inventoriable)

They are written of as expenses (in the

P&L) in the period in which these are

incurred – e.g. rent, salary of executives,

travel expenses etc.

20.

Unit costs andTotal costs

!

!

!

run!

-

short

in the

volume

of

effect

the

Why?

unit.

per

cost

variable

from

hed

distinguis

be

should

unit

per

cost

Fixed

Note!

produced

units

Total

costs

mfg

Accum.

(average)

cost

Unit

Editor's Notes

#3 Cost can also be defined as a benefit/sacrifice given up to acquire goods/services

A cost object is any activity for which a separate measurement of costs is desired i.e. the cost of something

#4 Cost can also be defined as a benefit/sacrifice given up to acquire goods/services

Different costs for different Purposes

Manufacturing organizations assign costs to products for two purposes:

First:

For internal profit measurement and external financial reporting requirements in order to allocate the mfg costs incurred during a period btn cost of goods sold and inventories.

Secondly:

To provide useful information for managerial decision-making requirements.

Different levels of accuracy , and different cost information is required for different purposes. For decision making purposes, more accurate product costs are required so that we can distinguish between profitable and unprofitable products. For external reporting it may not be necessary to accurately trace costs to individual products.

Again not all costs are relevant for decision making e.g. depreciation of machinery will not be affected by a decision to discontinue a product.

#6 A cost can be treated as direct for one cost object but indirect in respect of another. If the cost object is the product then the salary of the storekeeper or warehouse rent is indirect BUT IF the cost object is distribution channels – the salary of the storekeeper is regarded as direct cost for each distribution channel.

#13 Variable (linear segmental) cost behaviour – 25% for sales above 200 units; 40%(400)

The non-linear/curvilinear pattern of variable cost behaviour concurs with the economists’ approach to cost analysis

![7_C's_OF_COMMUNIOCATION[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7csofcommuniocation1-230801063320-9af405b3-thumbnail.jpg?width=640&height=640&fit=bounds)