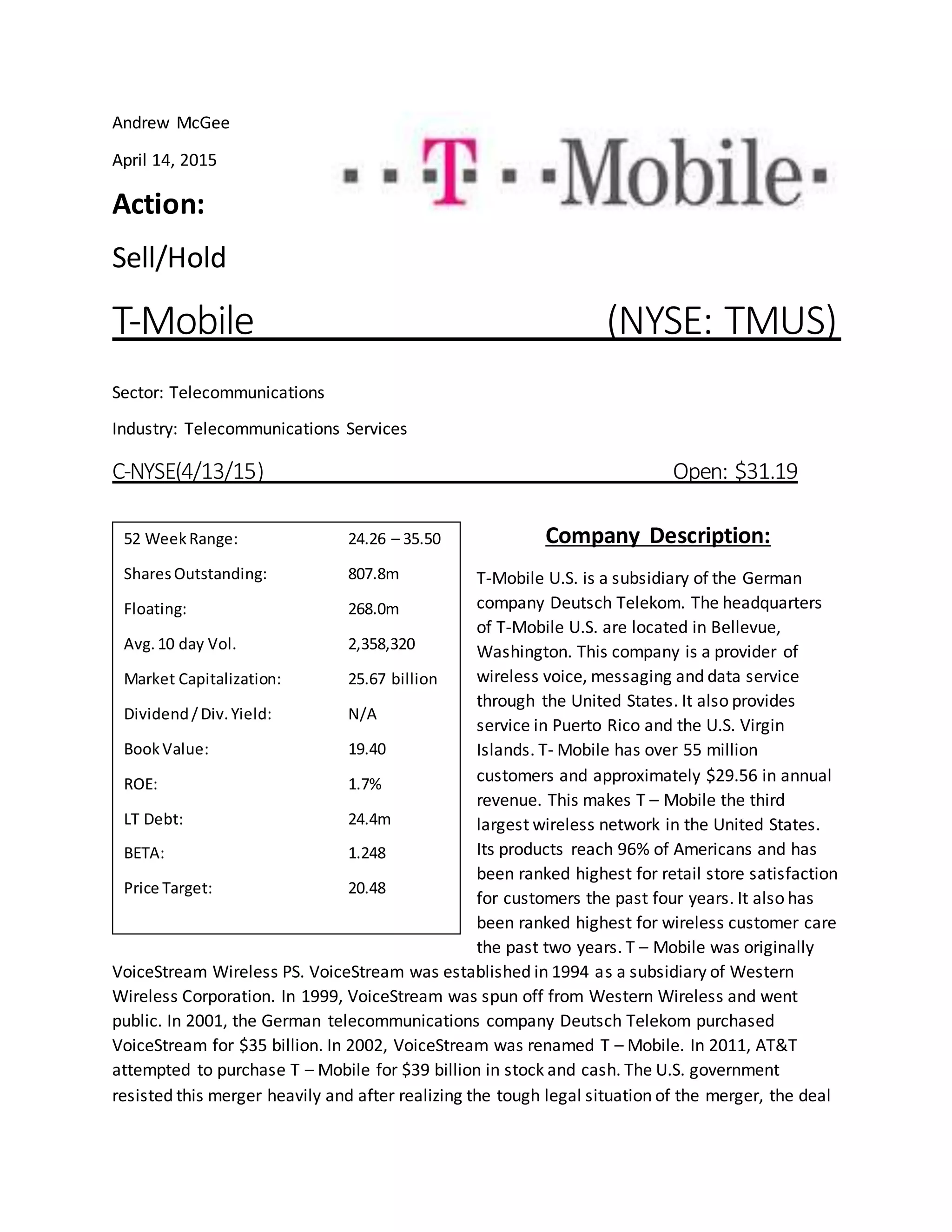

- The document analyzes T-Mobile US, Inc. as an investment opportunity and recommends selling the stock.

- Key points include T-Mobile's business overview as the 3rd largest US wireless carrier, its competitive strategies to attract customers from rivals, and financial analysis showing the stock is overvalued compared to the author's price target of $20.48 per share.

- The author cites concerns about T-Mobile's high debt levels, slowing revenue growth, and cyclical earnings patterns in recommending against establishing a position in the company.

![[2016 Outlook] Media Advertisement](https://cdn.slidesharecdn.com/ss_thumbnails/201512102016outlookmediaadvertisementoverweight1-151222013450-thumbnail.jpg?width=640&height=640&fit=bounds)