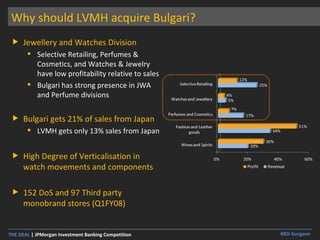

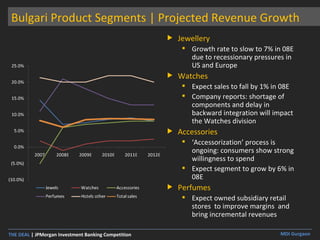

The document discusses the strategic rationale behind LVMH's acquisition of Bulgari, highlighting the luxury goods industry's growth potential and market dynamics. It analyzes Bulgari's valuation, product segments, and potential synergies within LVMH's existing operations, while outlining various financing options for the acquisition. Additionally, it examines market conditions and considers the timing and alternatives for the acquisition, culminating in a detailed financial assessment.