Download to read offline

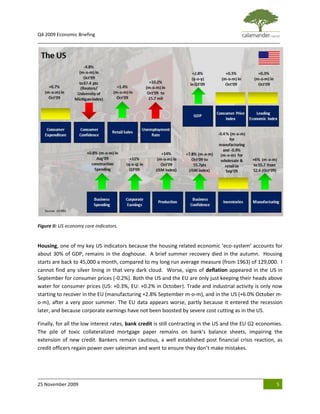

The document provides an economic briefing for Q4 2009. It summarizes that while major economic indicators show the US and EU economies have returned to growth, the recovery is slow and unemployment remains very high. Housing markets especially remain weak with signs of deflation. Trade and industrial activity are starting to recover but consumer spending and confidence remain subdued. While markets have rallied strongly, the underlying economic fundamentals still suggest a long, slow recovery.