Download to read offline

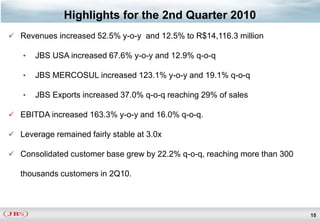

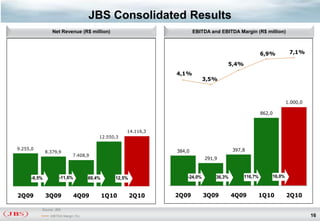

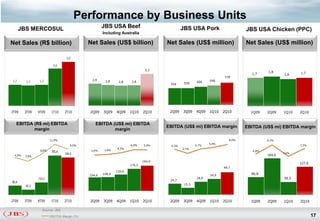

The company posted record EBITDA of R$1.0 billion in the second quarter of 2010. Forward-looking statements involve risks and uncertainties because they depend on future events and circumstances outside of the company's control. The presentation provides an overview of the company, its market position and strategy, highlights from the second quarter, and short-term outlook.