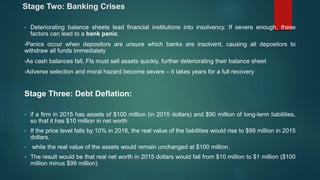

Financial crises can begin due to credit and asset price booms and busts or increases in uncertainty. This can lead to banking crises as balance sheets deteriorate and panics ensue as depositors withdraw funds. Debt deflation can then occur as the value of assets falls relative to liabilities. The 2007-2009 crisis was caused by financial innovation enabling subprime lending, agency problems in mortgage markets, and asymmetric information exacerbated by credit rating agencies. The effects included a collapse in the US housing market, deterioration of financial institution balance sheets, a run on the shadow banking system, turmoil in global financial markets, and the failure of major financial firms.