Download as PDF, PPTX

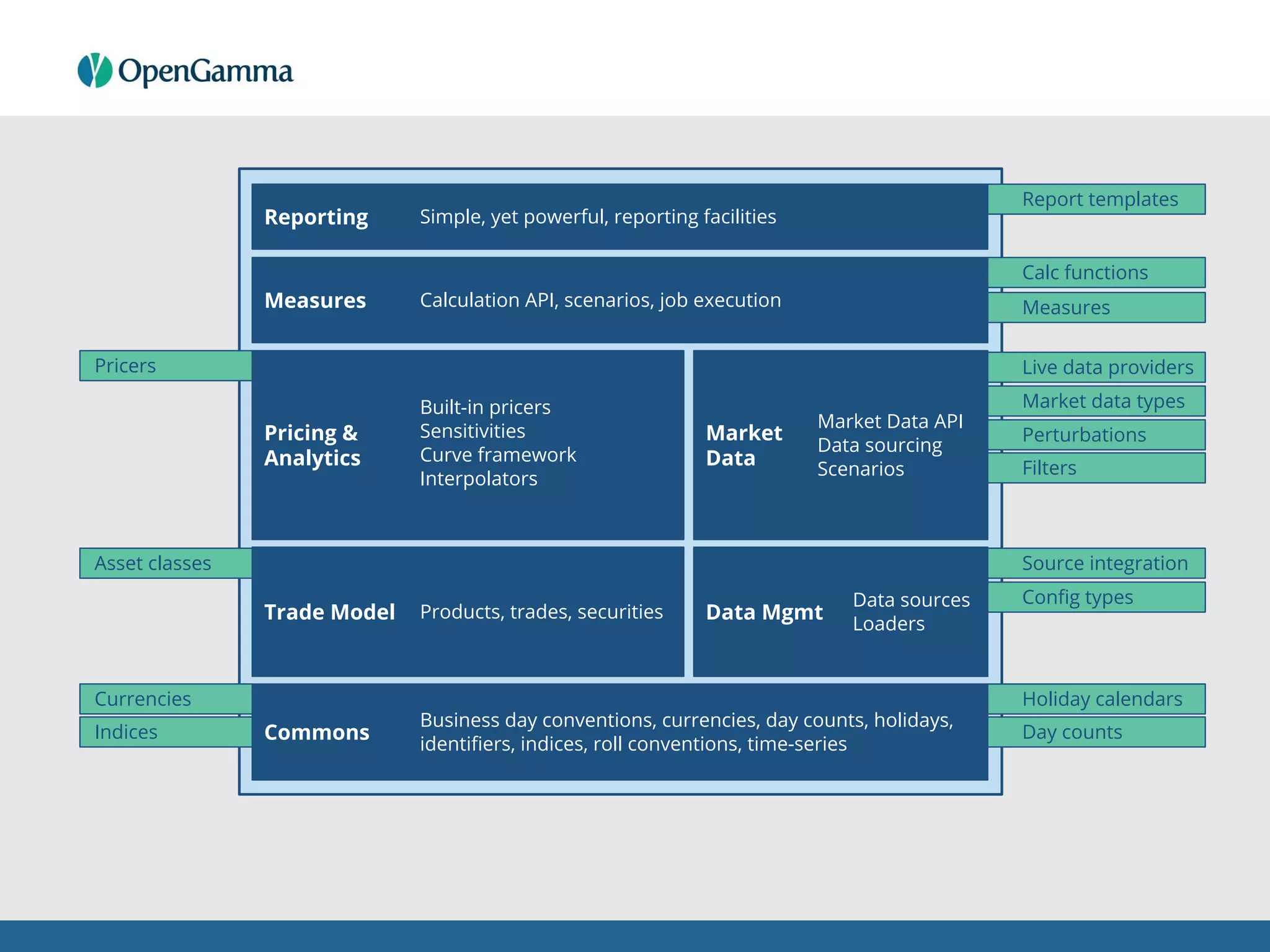

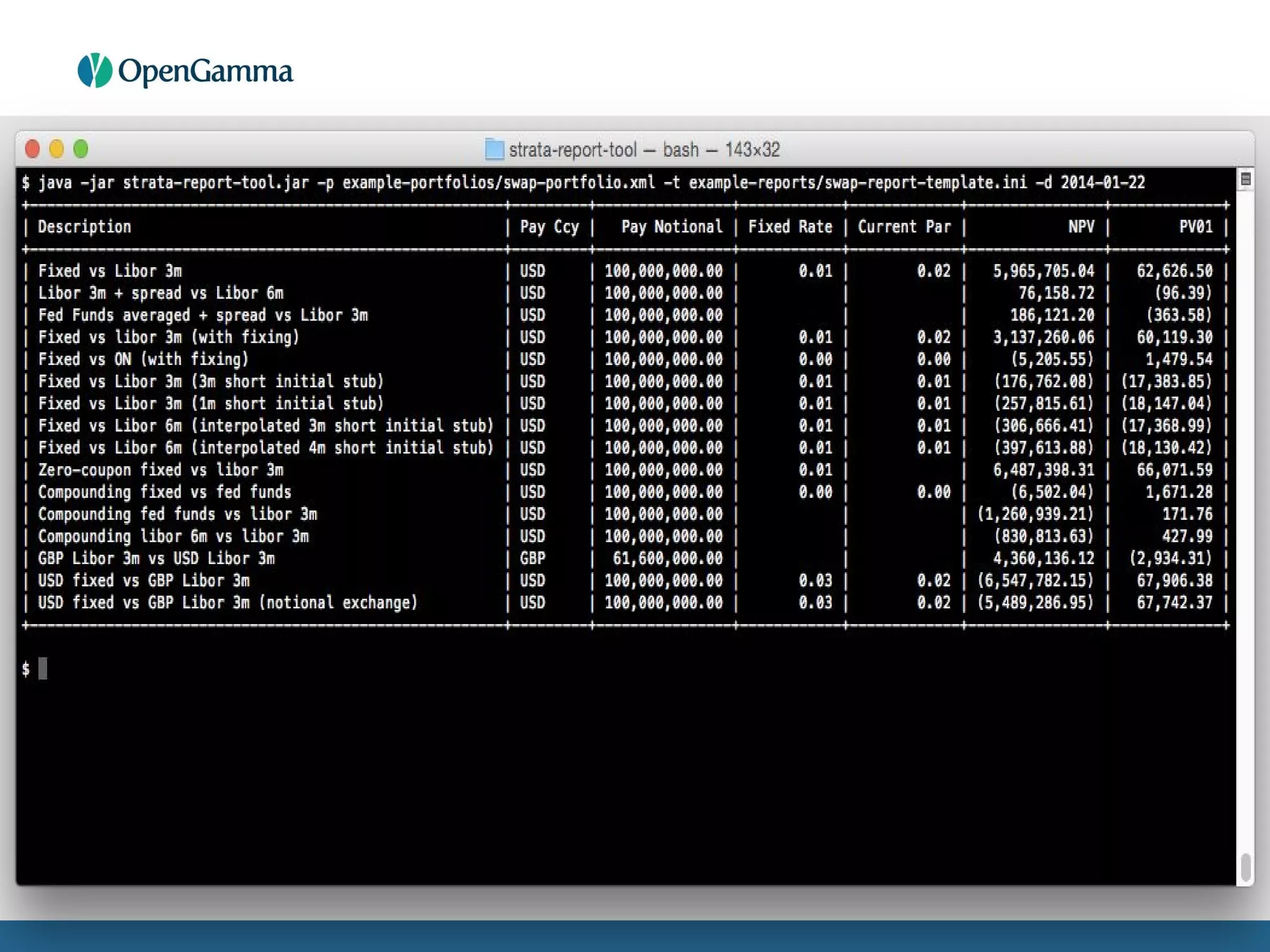

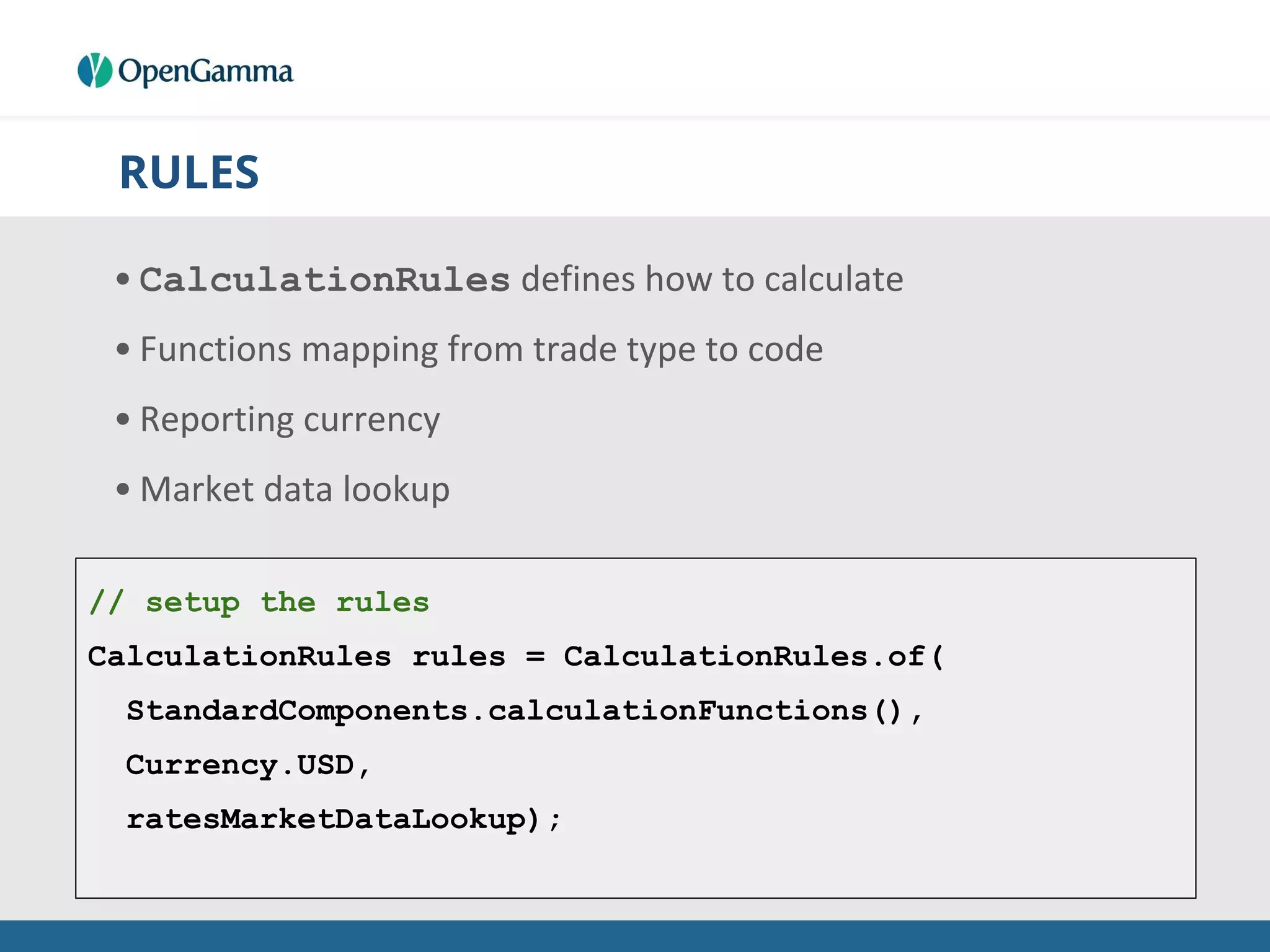

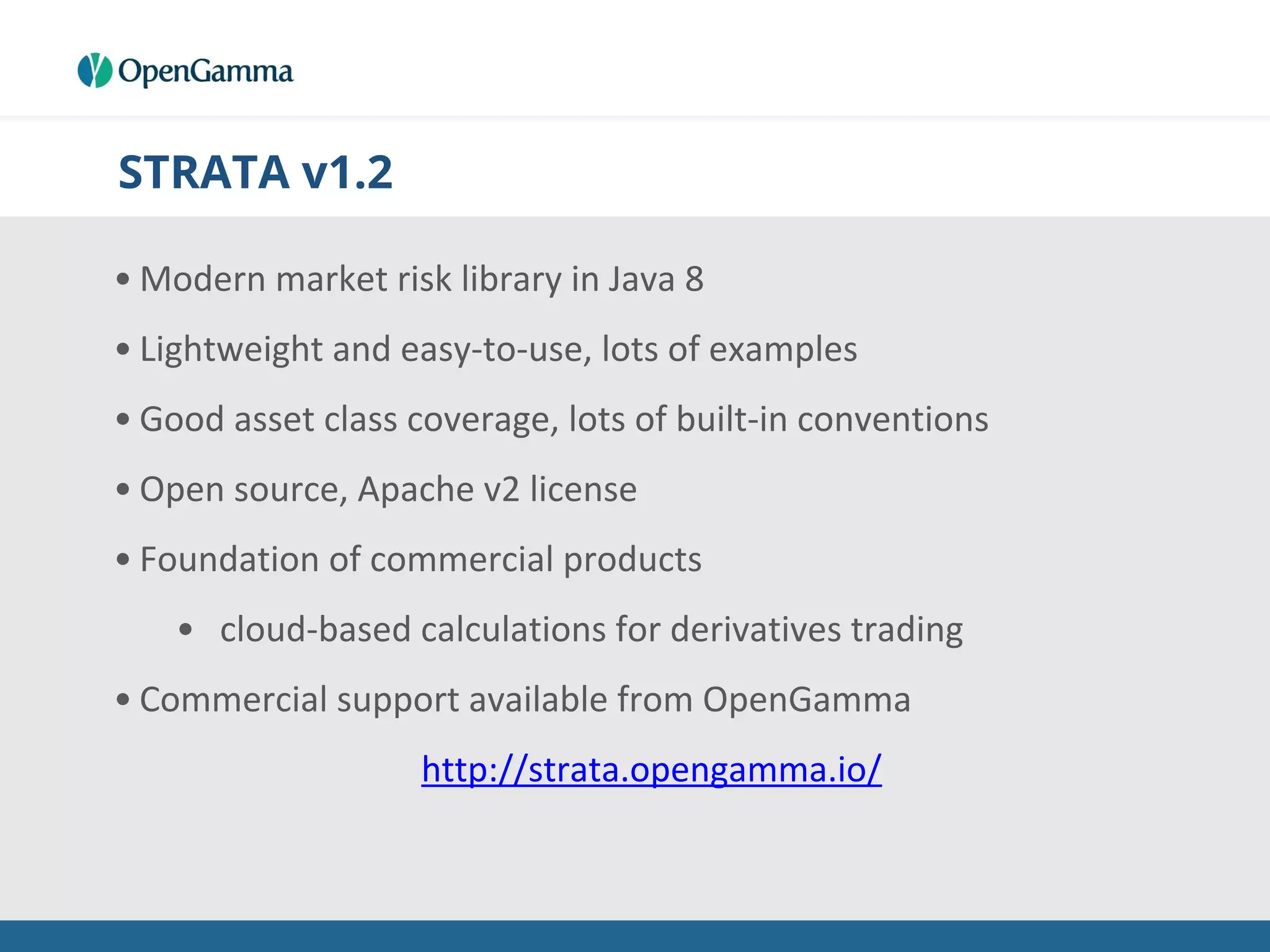

Strata is an open-source market risk library designed for use in the finance industry, emphasizing market risk analytics, derivatives, and trading. It offers a lightweight Java library under the Apache v2 license and features a robust API for pricing and risk calculations, supports various asset classes, and provides built-in conventions. Developed by OpenGamma, Strata aims to bring open-source values to finance and includes features for cloud-based calculations and commercial support options.