LEARNING GOALS

1. Marketefficiency

2. Basic stock valuation (zero,

constant, and variable growth)

3. Free cash flow valuation

4. Other Approaches to Common

Stock Valuation

3.

COMMON STOCK VALUATION

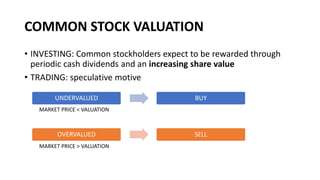

•INVESTING: Common stockholders expect to be rewarded through

periodic cash dividends and an increasing share value

• TRADING: speculative motive

UNDERVALUED BUY

OVERVALUED SELL

MARKET PRICE < VALUATION

MARKET PRICE > VALUATION

4.

MARKET EFFICIENCY

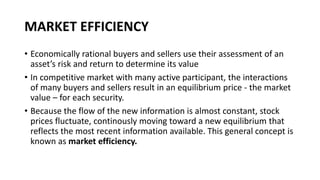

• Economicallyrational buyers and sellers use their assessment of an

asset’s risk and return to determine its value

• In competitive market with many active participant, the interactions

of many buyers and sellers result in an equilibrium price - the market

value – for each security.

• Because the flow of the new information is almost constant, stock

prices fluctuate, continously moving toward a new equilibrium that

reflects the most recent information available. This general concept is

known as market efficiency.

5.

MARKET EFFICIENCY

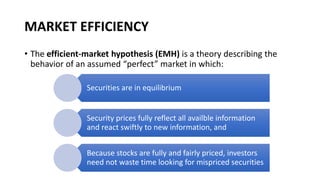

• Theefficient-market hypothesis (EMH) is a theory describing the

behavior of an assumed “perfect” market in which:

Securities are in equilibrium

Security prices fully reflect all availble information

and react swiftly to new information, and

Because stocks are fully and fairly priced, investors

need not waste time looking for mispriced securities

6.

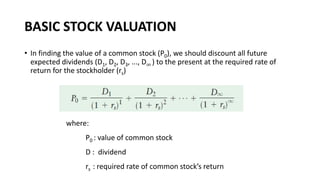

BASIC STOCK VALUATION

•In finding the value of a common stock (P0), we should discount all future

expected dividends (D1, D2, D3, ..., D∞ ) to the present at the required rate of

return for the stockholder (rs)

where:

P0 : value of common stock

D : dividend

rs : required rate of common stock’s return

7.

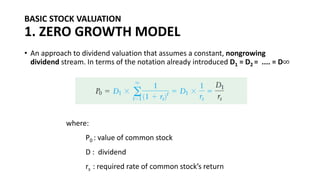

BASIC STOCK VALUATION

1.ZERO GROWTH MODEL

• An approach to dividend valuation that assumes a constant, nongrowing

dividend stream. In terms of the notation already introduced D1 = D2 = .... = D∞

where:

P0 : value of common stock

D : dividend

rs : required rate of common stock’s return

8.

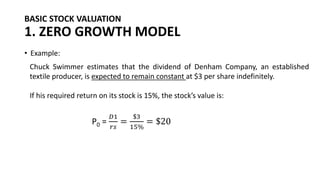

BASIC STOCK VALUATION

1.ZERO GROWTH MODEL

• Example:

Chuck Swimmer estimates that the dividend of Denham Company, an established

textile producer, is expected to remain constant at $3 per share indefinitely.

If his required return on its stock is 15%, the stock’s value is:

P0 =

𝐷1

𝑟𝑠

=

$3

15%

= $20

9.

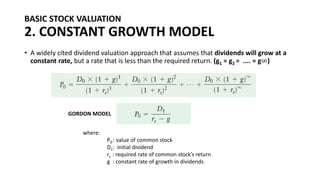

BASIC STOCK VALUATION

2.CONSTANT GROWTH MODEL

• A widely cited dividend valuation approach that assumes that dividends will grow at a

constant rate, but a rate that is less than the required return. (g1 = g2 = .... = g∞)

where:

P0 : value of common stock

D1: initial dividend

rs : required rate of common stock’s return

g : constant rate of growth in dividends

GORDON MODEL

10.

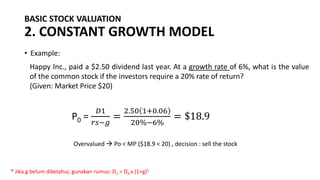

BASIC STOCK VALUATION

2.CONSTANT GROWTH MODEL

• Example:

Happy Inc., paid a $2.50 dividend last year. At a growth rate of 6%, what is the value

of the common stock if the investors require a 20% rate of return?

(Given: Market Price $20)

P0 =

𝐷1

𝑟𝑠−𝑔

=

2.50 1+0.06

20%−6%

= $18.9

Overvalued → Po < MP ($18.9 < 20) , decision : sell the stock

* Jika g belum diketahui, gunakan rumus: D1 = D0 x (1+g)1

11.

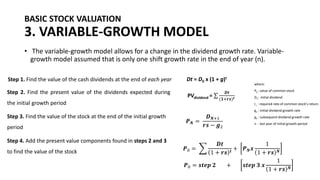

BASIC STOCK VALUATION

3.VARIABLE-GROWTH MODEL

• The variable-growth model allows for a change in the dividend growth rate. Variable-

growth model assumed that is only one shift growth rate in the end of year (n).

Step 1. Find the value of the cash dividends at the end of each year Dt = D0 x (1 + g)t

Step 2. Find the present value of the dividends expected during

the initial growth period

PVdividend = σ

𝑫𝒕

(𝟏+𝒓𝒔)𝒕

Step 3. Find the value of the stock at the end of the initial growth

period

𝑷𝑵 =

𝑫𝑵+1

𝒓𝒔 − 𝒈2

Step 4. Add the present value components found in steps 2 and 3

to find the value of the stock

𝑷0 =

𝑫𝒕

1 + 𝒓𝒔 𝒕

+ 𝑷𝑵𝒙

1

1 + 𝒓𝒔 𝑵

where:

P0 : value of common stock

D1: initial dividend

rs : required rate of common stock’s return

g1 : initial dividend growth rate

g2 : subsequent dividend growth rate

n : last year of initial growth period

𝑷0 = 𝒔𝒕𝒆𝒑 𝟐 + 𝒔𝒕𝒆𝒑 𝟑 𝒙

1

1 + 𝒓𝒔 𝑵

12.

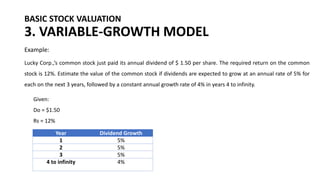

BASIC STOCK VALUATION

3.VARIABLE-GROWTH MODEL

Example:

Lucky Corp.,’s common stock just paid its annual dividend of $ 1.50 per share. The required return on the common

stock is 12%. Estimate the value of the common stock if dividends are expected to grow at an annual rate of 5% for

each on the next 3 years, followed by a constant annual growth rate of 4% in years 4 to infinity.

Given:

Do = $1.50

Rs = 12%

Year Dividend Growth

1 5%

2 5%

3 5%

4 to infinity 4%

13.

BASIC STOCK VALUATION

3.VARIABLE-GROWTH MODEL

Example:

Step 1: Find the value of the cash dividends at the year end of each year.

Dt = D0 x (1+g)t

D1 = D0 x (1+g)1 = 1.50 x (1+5%) = $ 1.575

D2 = D0 x (1+g)2 = 1.50 x (1+5%)2 = $ 1.65375

D3 = D0 x (1+g)3 = 1.50 x (1+5%)3 = $ 1.7364375

D4 = D3 x (1+g)1 = 1.7364375x (1+4%)1 = $ 1.805895

Year Dividend Growth

1 5%

2 5%

3 5%

4 to

infinity

4%

14.

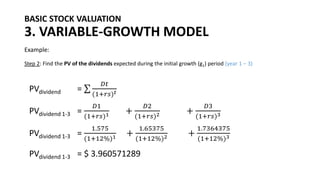

BASIC STOCK VALUATION

3.VARIABLE-GROWTH MODEL

Example:

Step 2: Find the PV of the dividends expected during the initial growth (g1) period (year 1 – 3)

PVdividend = σ

𝐷𝑡

(1+𝑟𝑠)𝑡

PVdividend 1-3 =

𝐷1

(1+𝑟𝑠)1 +

𝐷2

(1+𝑟𝑠)2 +

𝐷3

(1+𝑟𝑠)3

PVdividend 1-3 =

1.575

(1+12%)1 +

1.65375

(1+12%)2 +

1.7364375

(1+12%)3

PVdividend 1-3 = $ 3.960571289

15.

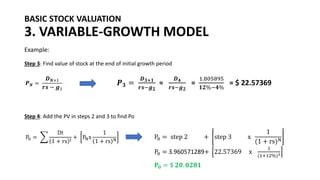

BASIC STOCK VALUATION

3.VARIABLE-GROWTH MODEL

Example:

Step 3: Find value of stock at the end of initial growth period

𝑷𝑵 =

𝑫𝑵+1

𝒓𝒔 − 𝒈2

𝑷𝟑 =

𝑫𝟑+𝟏

𝒓𝒔−𝒈𝟐

=

𝑫𝟒

𝒓𝒔−𝒈𝟐

=

1.805895

𝟏𝟐%−𝟒%

= $ 22.57369

Step 4: Add the PV in steps 2 and 3 to find Po

P0 =

Dt

1 + rs t

+ PNx

1

1 + rs N

P0 = step 2 + step 3 x

1

(1 + rs)N

P0 = 3.960571289+ 22.57369 x

1

(1+12%)3

𝐏𝟎 = $ 𝟐𝟎. 𝟎𝟐𝟖𝟏

16.

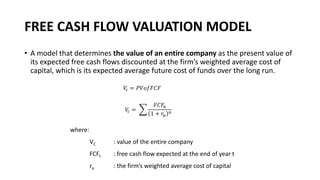

FREE CASH FLOWVALUATION MODEL

• A model that determines the value of an entire company as the present value of

its expected free cash flows discounted at the firm’s weighted average cost of

capital, which is its expected average future cost of funds over the long run.

where:

VC : value of the entire company

FCFt : free cash flow expected at the end of year t

ra : the firm’s weighted average cost of capital

𝑉

𝑐 = 𝑃𝑉𝑜𝑓𝐹𝐶𝐹

𝑉

𝑐 =

𝐹𝐶𝐹𝑛

1 + 𝑟𝑎

𝑛

17.

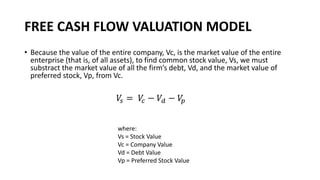

FREE CASH FLOWVALUATION MODEL

• Because the value of the entire company, Vc, is the market value of the entire

enterprise (that is, of all assets), to find common stock value, Vs, we must

substract the market value of all the firm’s debt, Vd, and the market value of

preferred stock, Vp, from Vc.

where:

Vs = Stock Value

Vc = Company Value

Vd = Debt Value

Vp = Preferred Stock Value

𝑉

𝑠 = 𝑉

𝑐 − 𝑉𝑑 − 𝑉

𝑝

18.

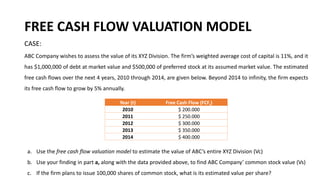

FREE CASH FLOWVALUATION MODEL

CASE:

ABC Company wishes to assess the value of its XYZ Division. The firm’s weighted average cost of capital is 11%, and it

has $1,000,000 of debt at market value and $500,000 of preferred stock at its assumed market value. The estimated

free cash flows over the next 4 years, 2010 through 2014, are given below. Beyond 2014 to infinity, the firm expects

its free cash flow to grow by 5% annually.

Year (t) Free Cash Flow (FCFt)

2010 $ 200.000

2011 $ 250.000

2012 $ 300.000

2013 $ 350.000

2014 $ 400.000

a. Use the free cash flow valuation model to estimate the value of ABC’s entire XYZ Division (Vc)

b. Use your finding in part a, along with the data provided above, to find ABC Company’ common stock value (Vs)

c. If the firm plans to issue 100,000 shares of common stock, what is its estimated value per share?

19.

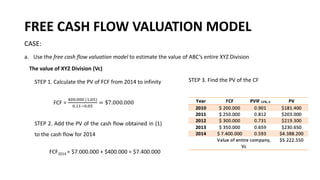

FREE CASH FLOWVALUATION MODEL

CASE:

a. Use the free cash flow valuation model to estimate the value of ABC’s entire XYZ Division

The value of XYZ Division (Vc)

STEP 1. Calculate the PV of FCF from 2014 to infinity

FCF =

400.000 (1,05)

0.11−0.05

= $7.000.000

STEP 2. Add the PV of the cash flow obtained in (1)

to the cash flow for 2014

FCF2014 = $7.000.000 + $400.000 = $7.400.000

STEP 3. Find the PV of the CF

20.

FREE CASH FLOWVALUATION MODEL

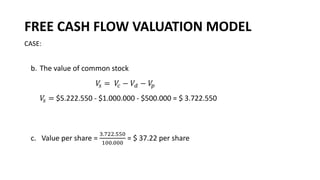

CASE:

b. The value of common stock

𝑉

𝑠 = 𝑉

𝑐 − 𝑉𝑑 − 𝑉

𝑝

𝑉

𝑠 = $5.222.550 - $1.000.000 - $500.000 = $ 3.722.550

c. Value per share =

3.722.550

100.000

= $ 37.22 per share

21.

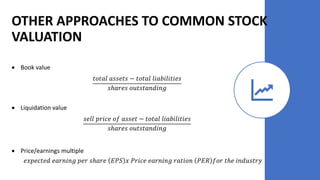

• Book value

𝑡𝑜𝑡𝑎𝑙𝑎𝑠𝑠𝑒𝑡𝑠 − 𝑡𝑜𝑡𝑎𝑙 𝑙𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑖𝑒𝑠

𝑠ℎ𝑎𝑟𝑒𝑠 𝑜𝑢𝑡𝑠𝑡𝑎𝑛𝑑𝑖𝑛𝑔

• Liquidation value

𝑠𝑒𝑙𝑙 𝑝𝑟𝑖𝑐𝑒 𝑜𝑓 𝑎𝑠𝑠𝑒𝑡 − 𝑡𝑜𝑡𝑎𝑙 𝑙𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑖𝑒𝑠

𝑠ℎ𝑎𝑟𝑒𝑠 𝑜𝑢𝑡𝑠𝑡𝑎𝑛𝑑𝑖𝑛𝑔

• Price/earnings multiple

𝑒𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑒𝑎𝑟𝑛𝑖𝑛𝑔 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒 𝐸𝑃𝑆 𝑥 𝑃𝑟𝑖𝑐𝑒 𝑒𝑎𝑟𝑛𝑖𝑛𝑔 𝑟𝑎𝑡𝑖𝑜𝑛 𝑃𝐸𝑅 𝑓𝑜𝑟 𝑡ℎ𝑒 𝑖𝑛𝑑𝑢𝑠𝑡𝑟𝑦

OTHER APPROACHES TO COMMON STOCK

VALUATION