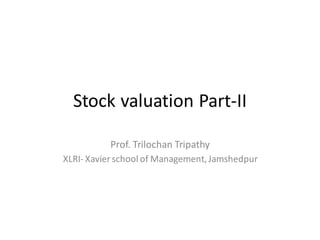

2. Cash Flow of Bond vs. Equity Investor

Firm

Equity

Debt

Net Income

Interest

(fixed income)

May Pay

Dividend

(variable residual

income)

Retained

Earnings

3. Cash Flow of Bond vs. Equity Investor

Bond Investorcash Flow

𝑃𝑉 =

𝐶1

1 + 𝑟 1 +

𝐶2

1 + 𝑟 2 + ⋯ +

100 + 𝐶𝑛

1 + 𝑟 𝑛

• Predictable Coupon Cash flow

• Predictable Terminal Value

Equity Investor cash flow

𝑉 =

𝐶1 =?

1 + 𝑟 =? 1 +

𝐶2 =?

1 + 𝑟 =? 2 + ⋯+

𝑇𝑉 =?+𝐶𝑛 =?

1 + 𝑟 =? 𝑛

• Cash flow to Owner is Unpredictable

• Difficult to Predict Terminal Value

4. Why Cash Flows are uncertain for

equity investor?

• Dividend and dividend growth

• Interestrate risk

• Reinvestmentrisk

• Credit/defaultrisk

• Inflationary risk

• Liquidity risk

• Exchange rate risk

• Politicalrisk

• Etc.

5. What Causes Stock Prices to Go Up

and Down?

Can you Guess??

Can we value the stock?

7. Equity Shares Characterization & Valuation

– Equity shares in general are characterized by:

• Ownership and management

• Entitlement to residual cash flows

• Limited liability

• Infinite life

• Substantiallydifferent risk profile

-Thus, equity shares valuation is not that easy like

bonds.

8. Efficient market Hypothesis

Efficient Market Hypothesis

-Security are in equilibrium, which means they are fairly priced

(expected returns= required returns)

-Security prices accurately reflect available information, and

respond rapidly to new information as soon as it becomes

available”

-Securities are fairly priced and there is no undervaluation or over

valuation

– Weak form efficiency:pricesincorporateinformation aboutpast

prices

– Semi-strongform: incorporateall publicly available information

– Strongform: all information,includinginsideinformation

Stock price move in Random: Random Walk Hypothesis

9. However, we try to predict the value of

a stock amidst wide arrays of

uncertainty !

10. Alternative Stock valuation Models

DCF

• Dividend Discounted Model

• FCFF and FCFE

Relative Valuation Model

• P/E

• P/S

• EV/EBITDA etc.

Asset Based Valuation

• BV

• LV

11. Common stock valuation: DDM-Three Special Cases

• Constant (Zero growth) dividend

– The firm will pay a constantdividend forever

– This is like preferred stock

– The price is computed using the perpetuity formula

𝑉0 = 𝑡=1

∞ 𝐷𝑡

(1+𝑟)𝑡= D / r

• Constant dividend growth

– The firm will increase the dividend by a constantpercentevery period

– The price is computed using the growing perpetuity model

𝑉0 = 𝑡=1

∞ 𝐷𝑡

(1+𝑟)𝑡 = 𝑡=1

∞ 𝐷0(1+𝑔)𝑡

(1+𝑟)𝑡 =

𝐷1

𝑟−𝑔

• Supernormal growth

– Dividend growth is not consistentinitially, but settles down to constantgrowth

eventually

– The price is computed using a multistagemodel ( example two stage)

𝑉0 =

𝑡=1

𝑛

𝐷0 1 + 𝑔𝑆

𝑡

(1 + 𝑟)𝑡 +

𝐷0 × 1 + 𝑔𝑆

𝑛

× (1 + 𝑔𝐿)

(𝑟 − 𝑔𝐿) × (1 + 𝑟)𝑛

12. Value of a stock in a two-stage growth DDM

Given g1 35%

g2 10%

r% 15%

D0 50

Year AnticipatedDiv

HGP LGP Sum of DCFs

1 58.69565217

2 68.90359168

3 80.88682502

4 94.95409893

5 111.4678553 414.9080231

6 …...infanite 1219.222936

2452.292816 1634.130959

Thus, the expectedstock price is Rs. 1634.13

Suppose a company is providinginitial amountof dividendof Rs. 50

The company CFO is anticipatingto pay year on year dividendgrowthby

35% up to five years

From 6yr onwards it isanticipatedby the CFO of the company that the

company can pay 10% incremental dividendgrowthyearafteryear till

the life of the company

if the requiredrate of return on thiskind of riskyasset is 15% ,

what shouldbe the expectedstockprice of the company today?

14. Why Free Cash flow Valuation?

Many firms pay no, or low, cash dividends

Dividends are paid at discretion of the board of

director; therefore, it may be poorly aligned with the

firm's long-run profitability

If a company is views as acquisition target, free cash

flow is more appropriate measure because the new

owners will have discretion over future dividend.

Free cash flow may more related to long-run

probability of the firm compared to dividend

15. Free Cash flow valuation model

• The free cash flow model is based on the same

premise as the dividend valuation models except that

we value the firm’s free cash flows rather than

dividends.

16. FCFE Growth Model

Constand Growth Model

V0=

𝐹𝐶𝐹𝐸1

𝑟−𝑔

=

𝐹𝐶𝐹𝐸0 ×(1+𝑔)

𝑟−𝑔

Two-Stage Free Cash Flow to Equity (FCFE) Discount Model

𝑉0 =

𝑡=1

𝑛

𝐹𝐶𝐹𝐸0 1 + 𝑔𝑆

𝑡

(1 + 𝑟)𝑡

+

𝐹𝐶𝐹𝐸0 × 1 + 𝑔𝑆

𝑛

× (1 + 𝑔𝐿)

(𝑟 − 𝑔𝐿) × (1 + 𝑟)𝑛

Equity Value = FCFE discounted at the required return on equity

Return on equity= Risk-free rate of return + beta × (Market

rate of return−Risk-free rate of return)

17. Free Cash flow valuation model

• The free cash flow valuation model estimates the value of the

entire company and uses the cost of capital as the discount

rate.

• As a result, the value of the firm’s debt and preferred stock

must be subtracted from the value of the company to

estimate the value of equity.

VE =VC - VD-VPS

• Equity Value = Firm Value – Market Value of Debt- Market

Value of Preferred stock

FCFF = EBIT 1− Tax rate + Dep – FC Investment –dWC Investment

Firm Value (VF) = FCFFdiscountedat WACC

18. How to calculate FCFF in a real-world

scenario ?

Formula 1 Formula 2 Formula 3 Formula 4

NI (+) EBIT*(1-t) (+) EBITDA*(1-t) CFO +

NCC (+) NCC (+) NCC*t (+)

dWC Inv (-) dWC Inv (-) dWC Inv (-)

Int(1-t) (+) Int (1-t) +

FC inv (-) FC inv (-) FC inv (-) FC inv (-)

FCFF FCFF FCFF FCFF

• 𝐹𝐶 𝐼𝑛𝑣 = 𝑒𝑛𝑑𝑖𝑛𝑔 𝑔𝑟𝑜𝑠𝑠 𝑃𝑃&𝐸 − 𝑏𝑒𝑔𝑖𝑛𝑛𝑖𝑛𝑔 𝑔𝑟𝑜𝑠𝑠 𝑃𝑃&𝐸

• 𝑊𝐶 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 = 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦𝑡 + 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠𝑡 − 𝑃𝑎𝑦𝑎𝑏𝑙𝑒𝑡 - (𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦𝑡−1 + 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠𝑡−1

19. Try with an example

Items (Rs. In billion)

Sales 100

Operatingcost 20

EBITDA 80

NCC(depreciation) 20

EBIT 60

Interest 30

EBT 30

Tax (@40%) 12

EAT 18

dWC Investment -10

FC Investment 0

Principal repayment 10

No. of Common share outstanding .3

in %

WACC 12%

re 9%

g 6%

20. Solution

Sign Fourmula 1 Values (bn) Sign Formula 2 Values (bn)

NI 18 EBIT*(1-t) 36

+ NCC 20+ NCC 20

- WC Inv -10- WC Inv -10

+ Int(1-t) 18+

- FC inv 0- FC inv 0

FCFF 46 FCFF 46

sign Formula 3 Values (bn) sign Formula 4 Values (bn)

EBITDA*(1-t) 48 CFO 28

+ NCC*t 8

- WC Inv -10

+ + Int (1-t) 18

- FC inv 0

FCFF 46 FCFE 46

21. Solution for FCFE

sign Formula 4 Values (bn)

CFO 28

+ Int (1-t) 18

FCFF 46

- Int (1-t) -18

- Principal repayment -10

FCFE 18

Suppose the concerned company’s FCFE is growing at the rate g=6%

here onwards 9 Just an approximation)

Total Future value of cash flows= CurrentYr. FCFE + Future FCFE=

18+ 18*((1+6%)/(9%-6%))= = 654 billoin

Value per share= 654 billion/3 billion share outstanding=Rs. 218

22. FCFF is a Financial performance

Indicator

• Free cash flow to the firm (FCFF) represents the cash

flow from operations available for distribution after

accounting for depreciation expenses, taxes, working

capital, and investments.

• Free cash flow is arguably the most important financial

indicator of a company's stock value.

• A positive FCFF value indicates that the firm has cash

remaining after expenses.

• A negative value indicates that the firm has not

generated enough revenue to cover its costs and

investment activities.

23. Some Relative Valuation methods

• This method estimates the value of the firm’s stock

as a multiple of some measure of firm ’ s

performance, such as the firm’s earnings per share,

book value per share, sales per share, cash flow per

share, where the multiple is determined by the

multiples observed from comparable companies.

• The most common metrics are:

– Earnings Per Share and

– Book value per Share

– Liquidation value per share

24. Common Stock valuation by PE Ratio

• P/E ratio is a relative value model because it

tells the investor how many dollars investors

are willing to pay for each dollar of the

company’s earnings.

𝑇𝑟𝑎𝑖𝑙𝑖𝑛𝑔 𝑃/𝐸 =

𝑀𝑎𝑟𝑘𝑒𝑡 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒

𝐸𝑃𝑆 𝑜𝑣𝑒𝑟 𝑝𝑟𝑒𝑣𝑖𝑜𝑢𝑠 12 𝑚𝑜𝑛𝑡ℎ𝑠

𝐹𝑜𝑟𝑤𝑎𝑟𝑑 𝑃/𝐸 =

𝑀𝑎𝑟𝑘𝑒𝑡 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒

𝐸𝑃𝑆 𝑜𝑣𝑒𝑟 𝑛𝑒𝑥𝑡 12 𝑚𝑜𝑛𝑡ℎ𝑠

26. Common Stock valuation by PE Ratio

• Suppose XYZ company’ had last year earnings of $1.65 per

share for the 12-month period ended in March, 2016. XYZ’s

CFO estimates that company earnings for 2017 will be $1.83 a

share. The current P/E ratios for three comparable firms are

26.85, 18.79 & 22.18 and thus the comparable average PE

ratio is 22.61. Based on above information, estimate the value

of the common stock?

– Ans: $41.38

27. Common Stock valuation: BV per Share

Value of Common Stock (Vc)=

𝑇𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡−𝑇𝑜𝑡𝑎𝑙 𝐿𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑦

𝑁𝑜.𝑜𝑓 𝐶𝑆 𝑆ℎ𝑎𝑟𝑒𝑠 𝑜𝑢𝑡𝑠𝑡𝑎𝑛𝑑𝑖𝑛𝑔

Example: At year end XYZ company balance sheet

shows total asset of Rs. 600,0000 , total liability of Rs.

450,0000 and 100,000 of share of common share

outstanding. Find the value of the common stock?

Ans: Rs.15 per share

28. Common Stock Valuation: LV per Share

Value of Common Stock =

𝑇𝑜𝑡𝑎𝑙 𝑙𝑖𝑞𝑢𝑖𝑑𝑎𝑡𝑒𝑑 𝑎𝑠𝑠𝑒𝑡−𝑇𝑜𝑡𝑎𝑙 𝐿𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑦

𝑁𝑜.𝑜𝑓 𝐶𝑆 𝑆ℎ𝑎𝑟𝑒𝑠 𝑜𝑢𝑡𝑠𝑡𝑎𝑛𝑑𝑖𝑛𝑔

• Example: XYZ company is on verge of liquidation and an

investment bank estimated that upon liquidation the

total asset of the company is Rs. 525,0000 total liability

of Rs. 450,0000 and 100000 of share of common share

outstanding. Find the liquidation value of the common

stock?

Ans: Rs. 7.5

29. Preferred Stock

• Claims on Assets and Income

– In the event of bankruptcy, preferred stockholders have

priority over common stock. However, they have lower

priority than the firm’s debt holders.

– Firm must pay dividends on preferred stock prior to paying

dividend on common stock.

– Most preferred stock carry a cumulative feature.

Cumulative feature requires that all past unpaid dividends

to be paid before any common stock dividends can be

declared.

– Thus, preferred stocks are less risky than common stocks

but more risky than bonds.

30. Preferred Stock

• Preferred Stock as a Hybrid Security

– Like common stocks, preferred stocks do not have

a fixed maturity date. Also, like common stocks,

nonpayment of dividends does not lead to

bankruptcy of the firm.

– Like debt, preferred stocks have a fixed dividend.

Also, most preferred stocks are periodically retired

even though there is no stated maturity date.

31. Preferred Stock

• Dividend:

– Unlike common stockholders, preferred stockholders

receive the same fixed dividend regardless of how well the

firm does.

– In general, size of preferred stock dividend is fixed, and it is

either stated as a dollar amount or as a percentage of the

preferred stock’s par value.

– Multiple Classes: If a company chooses, it can issue more

than one class of preferred stock, and each class can have

different characteristics.(Cumulative, Participating, Convertible,

Callable and Adjustable-rate: try yourself no time)

32. Valuing Preferred Stock

Since preferred stockholders generally receive a fixed

dividend and the stocks are perpetuities (non-

maturing), it can be valued using the present value of

perpetuity equation.

33. Example

• Consider XYZ company’s preferred stock issue, which

pays an annual dividend of $5.00 per share, does not

have a maturity date, and on which the market’s

required yield or promised rate of return (rps) for

similar shares of preferred stock is 6.02%. What is

the value of the XYZ’s preferred stock?

34. Try Yourself

• What is the present value of a preferred stock that

pays a dividend of $12 per such stock if the market’s

yield on similar issues of preferred stock is 8%?

Ans: $150

35. Example

• What will be the yield on XYZ’s preferred

stock if the company has promised annual

dividend of $1.20 per share and each share is

currently selling for $32.50?

37. Practice problems

• RETURN ON INVESTMENT

• Q1. Diksha bought a share at a price of Rs.100.

The price of the stock moved to Rs.200 a year

later. During the period, Ramesh received a

dividend of Rs.8 per share.

– What is the % return Diksha received a year later?

– If she has paid 40% of the investment amount as margin

money to her broker while the rest amount is funded by

an overdraft borrowed at 15%, what is the return for her a

year later?

38. Solution

Return for Ramesh for a period of 1 year

Purchaseprice =Rs.100.00

Selling priceafter one year=Rs.200.00

Profit = Rs.100.00

Dividend duringthe period = Rs.8

% Return may be computed usingthe following formula:

Return (%) = [(P1-P0+Do)/P0]× 100= =108%

(b) Own fundsinvested(%) =40%

Own investment(Equity)= Rs.40

Profit and dividend earned=Rs.108

less: Interestpaid =15% on Rs.60 = Rs.9

Return on equity = Rs.99

Return on equity % =Return/Owninvestmentx 100 = (99/40)×100 =

248%

39. Practice problems ( Try Yourself)

• A share of the firm is trading at Rs. 350 currently. The market

that the price next year is going to be Rs.420.

(a) What is the growth in price of the share?

(b) If the currentdividend isRs.20 per share,what is the dividend

expected fromthe firm in the coming year?(c) What is the

expectation of return by the investors?Would it be the same as

growth in the priceof the share?Why and why not?

(d) If investordecidesto sell the share prior to the anticipated

dividend at what price would he sell his share?

(e) Would therebe any differencein return if investor sellsbefore

or after the dividends? Why and why not?

Note: Do you need any other information to solvethe problem.If so

you may assume such an info and solve the problem]

40. Practice problems

Q. Suppose the market value of the firm rs.416.94

million, firm has Rs. 40 million total debt and preferred

stock and has 10 million of common share outstanding.

Find the value per share?

Solution:

• MV Equity= MV of the firm – MV debt and preferred

stock

• MV of equity =Rs.(416.94-40)million =Rs.376.94 million

• Value per share= MV of equity/No. of shares=

Rs.376.94 million/10 million= Rs37.69

42. What Causes Stock Prices to Go Up and Down?

– The most recent dividend (D0): The more, the higher ….

– Expected rate of growth in future dividends (g): The higher,

the higher…..

– Investor’s required rate of return (rcs ): The higher, the

lower…..

– Since most recent dividend (D0) has already been paid, it

cannot be changed. Thus, variations in the other two

variables, rcs and g, can lead to changes in stockprices.

– Interest rate risk, Reinvestment risk, Credit risk, Inflation,

Liquidity risk, Currency risk, price risk, Political risk etc.