STOCK SNAPSHOT - De.mem Limited - Water treatment tech with growing recurring revenues

•

0 likes•100 views

De.mem (ASX: DEM) provides bespoke industrial water treatment solutions combining its (i) unique water membrane technology product suites and (iii) specialist engineering skills. DEM is improving revenue quality through growing recurring revenues and revenue diversification. Further valuation re-rating is possible as the company grows recurring revenues and drives to cash positive.

Recommended

Recommended

More Related Content

What's hot

What's hot (18)

Similar to STOCK SNAPSHOT - De.mem Limited - Water treatment tech with growing recurring revenues

Similar to STOCK SNAPSHOT - De.mem Limited - Water treatment tech with growing recurring revenues (20)

More from George Gabriel

More from George Gabriel (20)

Recently uploaded

Recently uploaded (20)

STOCK SNAPSHOT - De.mem Limited - Water treatment tech with growing recurring revenues

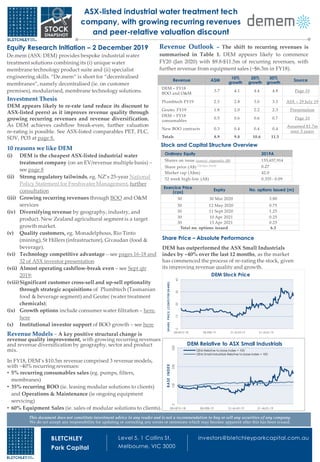

- 1. BLETCHLEY Park Capital Level 5, 1 Collins St, Melbourne, VIC 3000 investors@bletchleyparkcapital.com.au Share Price – Absolute Performance DEM has outperformed the ASX Small Industrials index by ~40% over the last 12 months, as the market has commenced the process of re-rating the stock, given its improving revenue quality and growth. This document does not constitute investment advice to any reader and is not a recommendation to buy or sell any securities of any company. We do not accept any responsibility for updating or correcting any errors or omissions which may become apparent after this has been issued. Equity Research Initiation – 2 December 2019 De.mem (ASX: DEM) provides bespoke industrial water treatment solutions combining its (i) unique water membrane technology product suite and (ii) specialist engineering skills. “De.mem” is short for “decentralised membranes”, namely decentralised (ie. on customer premises), modularised, membrane technology solutions. Stock and Capital Structure Overview Ordinary Equity 2019A Shares on issue (source: Appendix 3B) 155,657,914 Share price (A$) (28 Nov 2019) 0.27 Market cap (A$m) 42.0 52 week high-low (A$) 0.355 - 0.09 Exercice Price (cps) Expiry No. options issued (m) 30 30 Mar 2020 3.80 30 12 May 2020 0.75 30 11 Sept 2020 1.25 30 10 Apr 2021 0.25 30 13 Apr 2021 0.25 Total no. options issued 6.3 ASX-listed industrial water treatment tech company, with growing recurring revenues and peer-relative valuation discount Revenue Models – A key positive structural change is revenue quality improvement, with growing recurring revenues and revenue diversification by geography, sector and product mix. In FY18, DEM’s $10.5m revenue comprised 3 revenue models, with ~40% recurring revenues: • 5% recurring consumables sales (eg. pumps, filters, membranes) • 35% recurring BOO (ie. leasing modular solutions to clients) and Operations & Maintenance (ie ongoing equipment servicing) • 60% Equipment Sales (ie. sales of modular solutions to clients). Revenue Outlook – The shift to recurring revenues is summarised in Table 1. DEM appears likely to commence FY20 (Jan 2020) with $9.8-$11.5m of recurring revenues, with further revenue from equipment sales (~$6.3m in FY18). Investment Thesis DEM appears likely to re-rate (and reduce its discount to ASX-listed peers) as it improves revenue quality through growing recurring revenues and revenue diversification. As DEM achieves cashflow break-even, further valuation re-rating is possible. See ASX-listed comparables PET, FLC, SDV, PO3 at page 8. 10 reasons we like DEM (i) DEM is the cheapest ASX-listed industrial water treatment company (on an EV/revenue multiple basis) – see page 8 (ii) Strong regulatory tailwinds, eg. NZ’s 25-year National Policy Statement for Freshwater Management, further consultation (iii) Growing recurring revenues through BOO and O&M services (iv) Diversifying revenue by geography, industry, and product. New Zealand agricultural segment is a target growth market. (v) Quality customers, eg. Monadelphous, Rio Tinto (mining), St Hillers (infrastructure), Givaudan (food & beverage). (vi) Technology competitive advantage – see pages 16-18 and 32 of ASX investor presentation (vii) Almost operating cashflow-break even – see Sept qtr 2019; (viii)Significant customer cross-sell and up-sell optionality through strategic acquisitions of Plumbtech (Tasmanian food & beverage segment) and Geutec (water treatment chemicals); (ix) Growth options include consumer water filtration – here, here (x) Institutional investor support of BOO growth – see here Revenue A$M 10% growth 20% growth 30% growth Source DEM – FY18 BOO and O&M 3.7 4.1 4.4 4.8 Page 10 Plumbtech FY19 2.5 2.8 3.0 3.3 ASX – 29 July 19 Geutec FY19 1.8 2.0 2.2 2.3 Presentation DEM – FY18 consumables 0.5 0.6 0.6 0.7 Page 10 New BOO contracts 0.3 0.4 0.4 0.4 Assumed $1.7m over 5 years Totals 8.9 9.8 10.6 11.5 010203040 28-NOV-18 28-FEB-19 31-M AY-19 31-AUG-19 SHAREPRICE(CENTSPERSHARE) DEM Stock Price 0100200300 28-NOV-18 28-FEB-19 31-M AY-19 31-AUG-19 BASEINDEX DEM Relative to ASX Small Industrials DEM Relative to base index = 100 DEM Small Industrials Relative to base index = 100

- 2. BLETCHLEY Park Capital Level 5, 1 Collins St, Melbourne, VIC 3000 investors@bletchleyparkcapital.com.au This document does not constitute investment advice to any reader and is not a recommendation to buy or sell any securities of any company. We do not accept any responsibility for updating or correcting any errors or omissions which may become apparent after this has been issued. Technology Competitive Advantage DEM tech offering has a collaboration with Nanyang Technologica University (NTU), Singapore for research and development of its technologies. NTU is ranked #2 in the world for membrane research, by Lux Research. High Quality Customers diversified across sectors Customers include Rio Tinto, Monadelphous (mining), St Hilliers (infrastructure), food & beverage (Givaudan). See page 12. Financial Analysis As at 30 Sept 2019, DEM reported $2.8m cash balance, with an additional $2.95m received in October 2019 (total ~$5.75m). There is no financial debt, convertible notes, or other structured financial instruments on balance sheet. DEM is approaching operating cash break-even, with operating cash outflow of only -$30k and the highest ever quarterly cash receipts from customer of $3.4m. Visible equity upside potential At 27cps and assuming ~$14m of FY19F revenues, DEM trades at EV/revenue multiple of 3x, a ~75% discount to its ASX-listed peers. See page 8. As revenue quality improves, DEM’s valuation could re-rate. Assuming FY20F revenues of (say) $20m results at 3x implies a market capitalisation of $60m. If DEM re-rates to 4-6x, this implies a market cap of $80m - $120m is possible (2-3x upside on current market cap of $42m). Large addressable market, with regulatory tailwinds The global water and waste water solutions market has an estimated annual capital expenditure of $240 billion.(2) The global market for packaged / decentralised water treatment systems was valued at US$12 billion in 2015 and is expected to grow at a CAGR of 10.4% to reach US$21.8 billion by 2021.(3) Low-cost, strategic acquisitions provide cross-sell growth options The combined acquisitions of Pumptech and Geutec were no significant in financial cost (<5% of total DEM marke capitalisation), but provide significant cross-sell growth options int food & beverage segment (Pumptech) and chemicals (Geutec). Key Recent News Date Event 11 Nov 19 First revenues from new 5-stage domestic water filter 23 Sep 19 Geutec acquisition 27 Sep 19 Placement with leading investors 12 Sep 19 Launches new in-house developed microfiltration membrane 28 Aug 19 First orders in diversified markets 29 Jul 19 Pumptech acquisition (Tasmania) 27 Jun 19 Welcomes leading institutional investors to register 18 Jun 19 First revenues from new Forward Osmosis Membrane 26 Feb 19 First Commercial Order – Domestic Water Filters (Singapore) 22 Nov 18 Release of first self-developed membrane for commercial use 18 dJuly 18 Launched a new product line for ‘point of use’ domestic water filtration Outlook and Key Catalysts • Retention and expansion of existing customer contracts • New customer contracts • Regional and international expansion, with a focus on Europa and Asia Pacific • Strategic partnerships and mergers & acquisitions • Expansion of current technological portfolio Equity Analyst Coverage – no recent analyst coverage. Further Research Resources 1. http://demembranes.com/ 2. https://www.linkedin.com/company/de.mem-limited/ 3. Markets and Markets 4. Frost and Sullivan Revenue Diversification DEM is diversifying by geography, customer segment and product mix. • In FY18, ~90% revenues were generated from Queensland in the mining, municipal and infrastructure segments. • The Pumptech acquisition expanded the revenues into Tasmania, Australia and diversified the product range into the food & beverage segment. • Expanded operations with new regional offices established in Melbourne and Adelaide • The Geutec acquisition provides a European base (primarily Germany) and complements the water membrane technology with specialist industrial water chemicals products. • New Zealand is a target market, with DEM welcoming strategic NZ investors as a pathway to NZ customers, particularly in the agricultural sector. Key Investment Considerations ASX-listed industrial water treatment tech company, with growing recurring revenues and peer-relative valuation discount

- 3. BLETCHLEY Park Capital Level 5, 1 Collins St, Melbourne, VIC 3000 investors@bletchleyparkcapital.com.au Board Strong Industrial Background. Executive Highly qualified and experienced Management Team. Cosimo Trimigliozzi | CHAIRMAN • COO, Wild Flavors International • Managing Director, Givaudan Asia • MBA, University of Basel (Switzerland) Andreas Kroell | CEO AND DIRECTOR • Director, New Asia Investments • Corporate Finance, Deutsche Bank • Audit and Advisory, Deloitte • MBA, University of Frankfurt (Germany) Bernd Dautel | NON-EXECUTIVE DIRECTOR • Director, New Asia Investments • Managing Director, Wieland Metals Asia Pacific • Master of Chemical Engineering, Karlsruhe University of Technology (Germany) Shane Ayre | MANAGING DIRECTOR, AKWA-WORX • Founder of Akwa-Worx • 20 years industry experience Kian Lip Teo | COO • Lien Aid • Bachelor/Master, Nanyang Technological University (Singapore) David Chua | DIRECTOR, MEMBRANE MANUFACTURING • 10+ years experience in membrane production • Mann +Hummel • Hyflux • Bachelor/Master, Nanyang Technological University (Singapore) Nicanor Suarin | CHIEF ENGINEER • 30+ years experience in process and system design • Hyflux • Doosan Hydro • Bachelor of Engineering, MBA (Phillipines) LEGAL DISCLAIMER 1. This document does not constitute investment advice for any reader. 2. While this document is based on information sources which are considered reliable, we have not verified independently the information contained in the document and our directors, employees and consultants do not represent, warrant or guarantee, expressly or impliedly, that the information contained herein is complete or accurate. Nor do we accept any responsibility for updating any advice, views or opinions, contained in this document or for correcting any error or omission which may become apparent after the document has been issued. 3. We do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this document or any other person. 4. BPC may receive a commercial retainer by the Company to produce this document and may take or sell positions in the Company’s securities at any time. Stuart Carmichael | NON-EXECUTIVE DIRECTOR • Partner and Director, Ventnor Capital • Executive Vice President, UGL Limited • KPMG Corporate Finance • Chartered Accountant, Bachelor in Commerce Michael Edwards | NON-EXECUTIVE DIRECTOR • Partner and Director, Norwood Systems and Dawine Limited • Bachelor in Business (Economics/Finance), BSc (Geology) Key Risks and Mitigants • Revenue growth rate – mitigated by range of revenue growth options • BOO contract renewals – mitigated by long- standing customer relationships • Acquisition integration – mitigated by low value of acquisitions relative to total market capitalisation (both Geutec and Plumbtec total value is less than 5% of DEM market capitalisation) ASX-listed industrial water treatment tech company, with growing recurring revenues and peer-relative valuation discount