Download to read offline

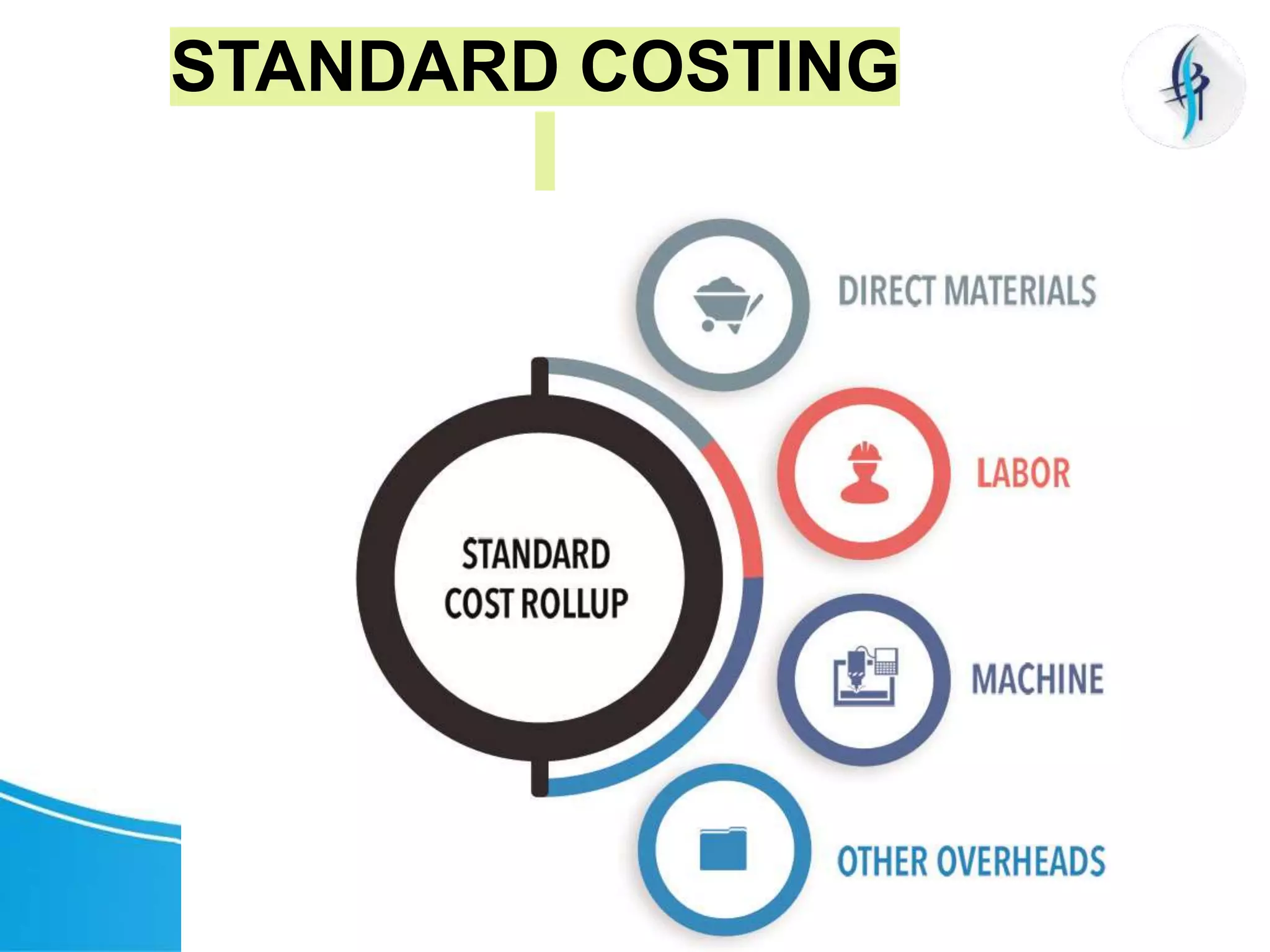

Standard costing is an accounting method that involves predetermined costs for materials, labor, and overhead, which are then compared to actual costs to measure variances. This system is applicable across various forms of accounting and helps in identifying the causes of cost variations. The results are presented to management for better cost control in production processes.

![Roland PPT[Prateek Mishra]](https://cdn.slidesharecdn.com/ss_thumbnails/8835b5ff-5ce1-43b8-b7e9-22600d4565ea-170109021210-thumbnail.jpg?width=640&height=640&fit=bounds)