Download as PDF, PPTX

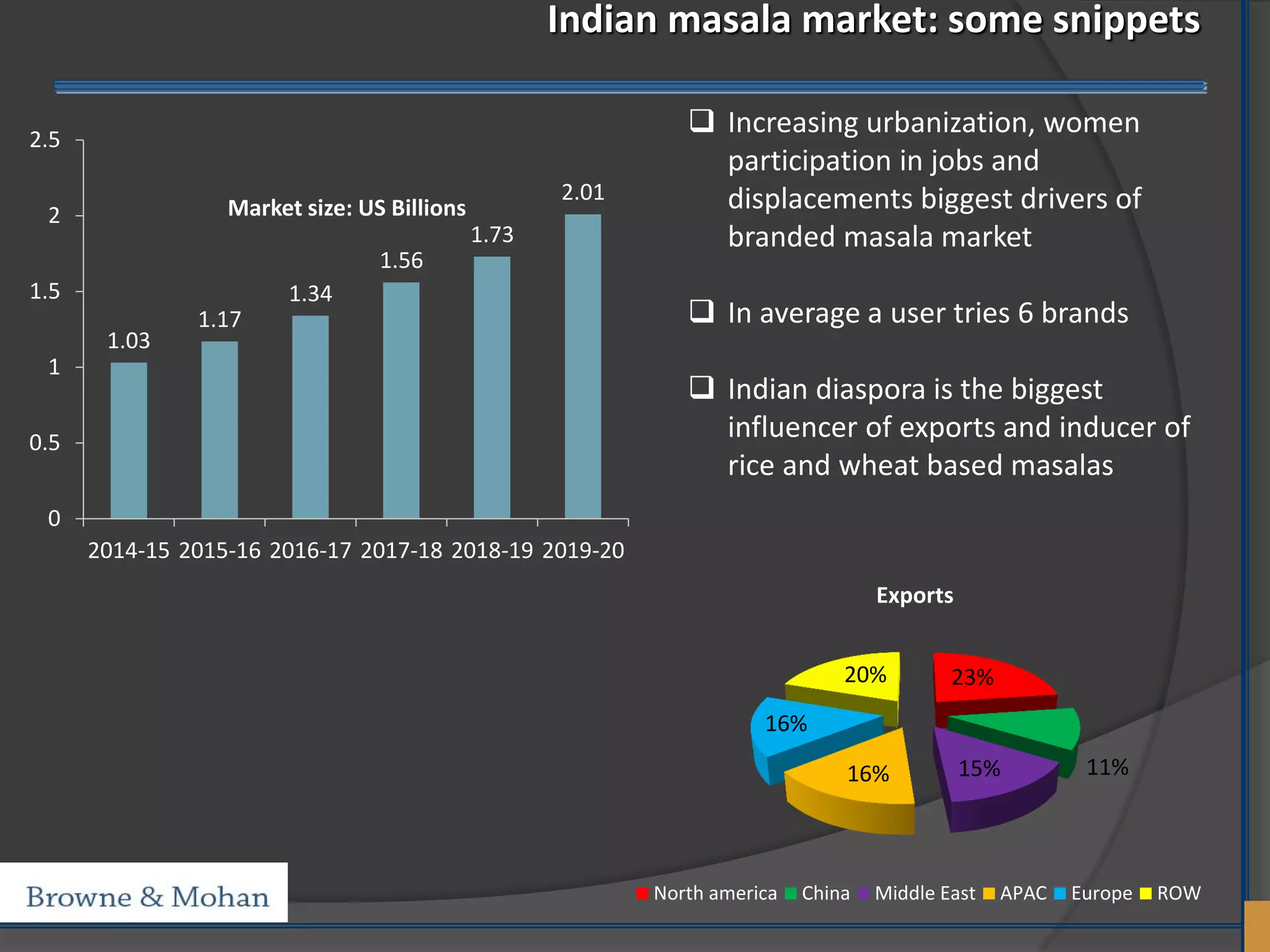

The Indian masala market is driven by urbanization and job participation, with 1,235 competing brands. Major players, primarily SMEs, have adopted growth strategies involving product diversification and expansion into contiguous markets. Key market challenges include managing growth, product optimization, and competition from foreign brands.