Downloaded 10 times

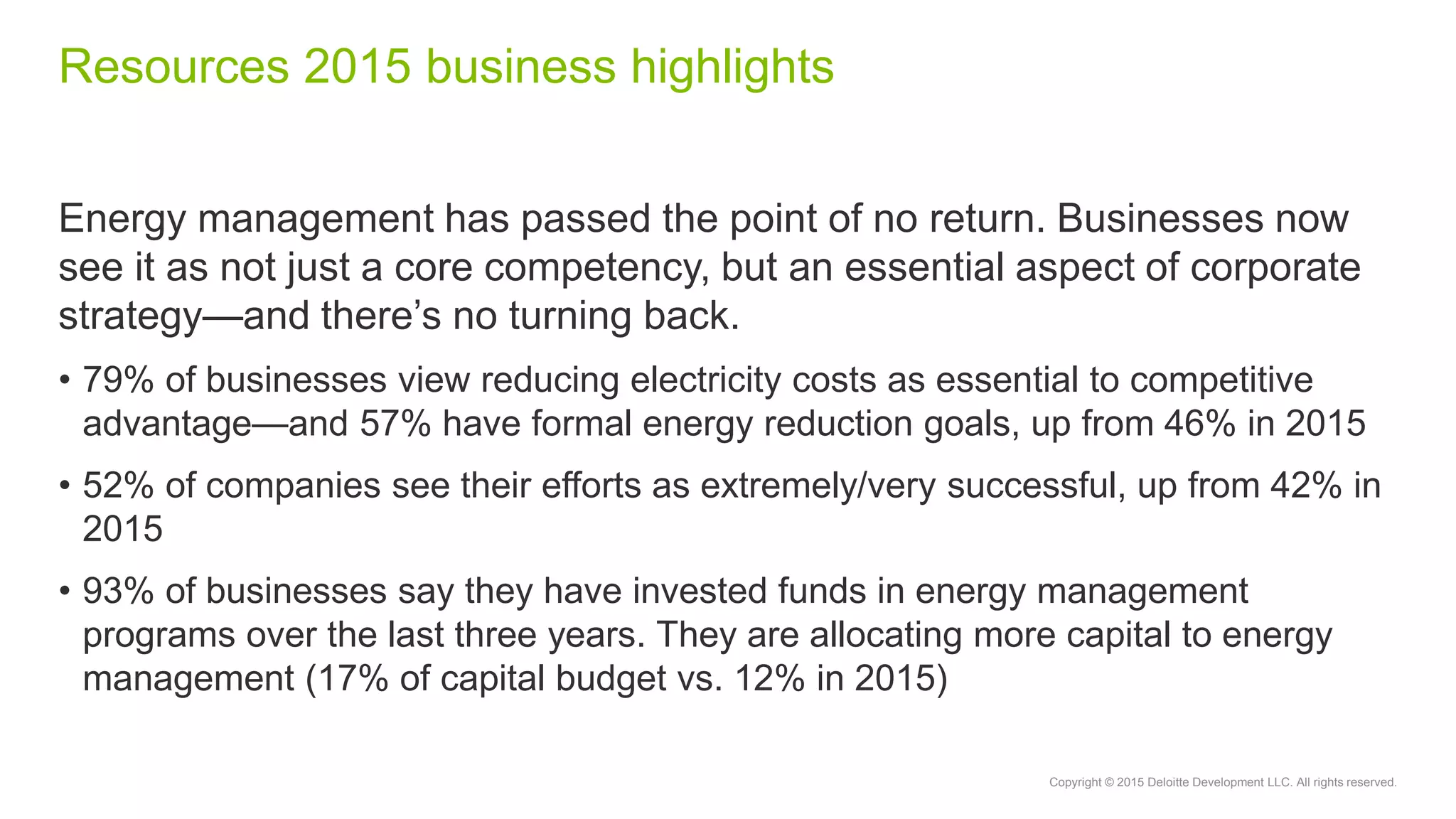

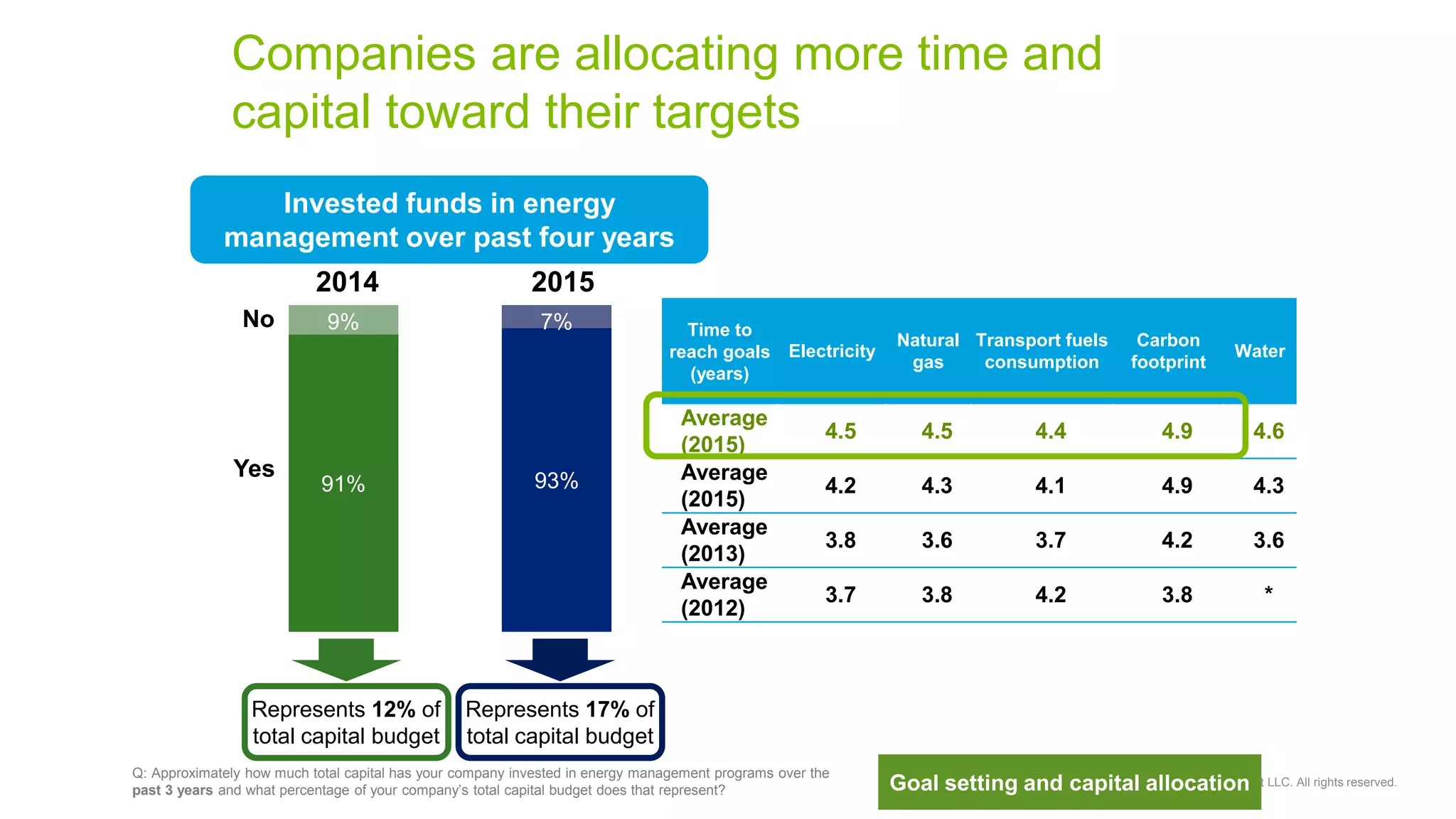

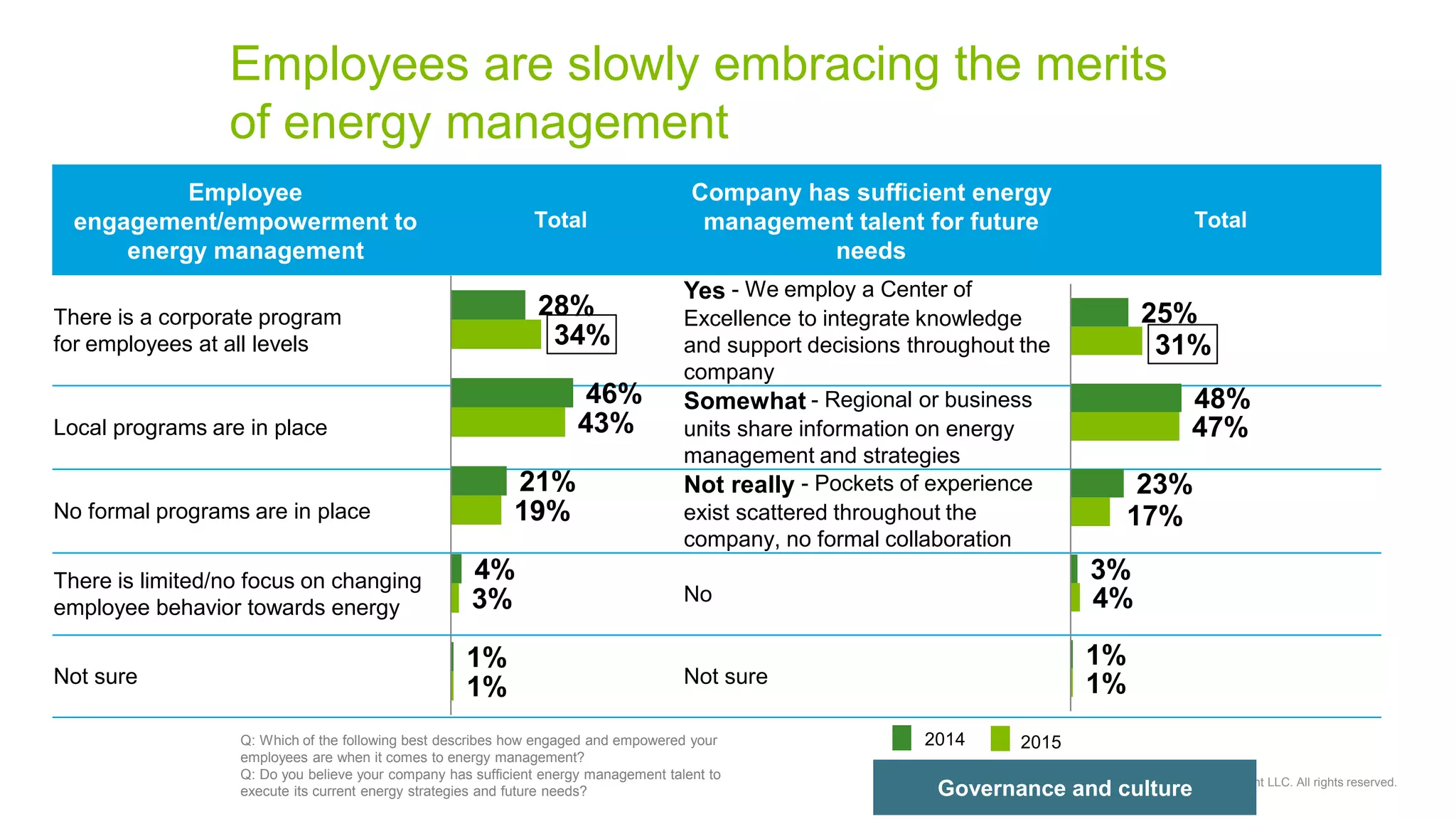

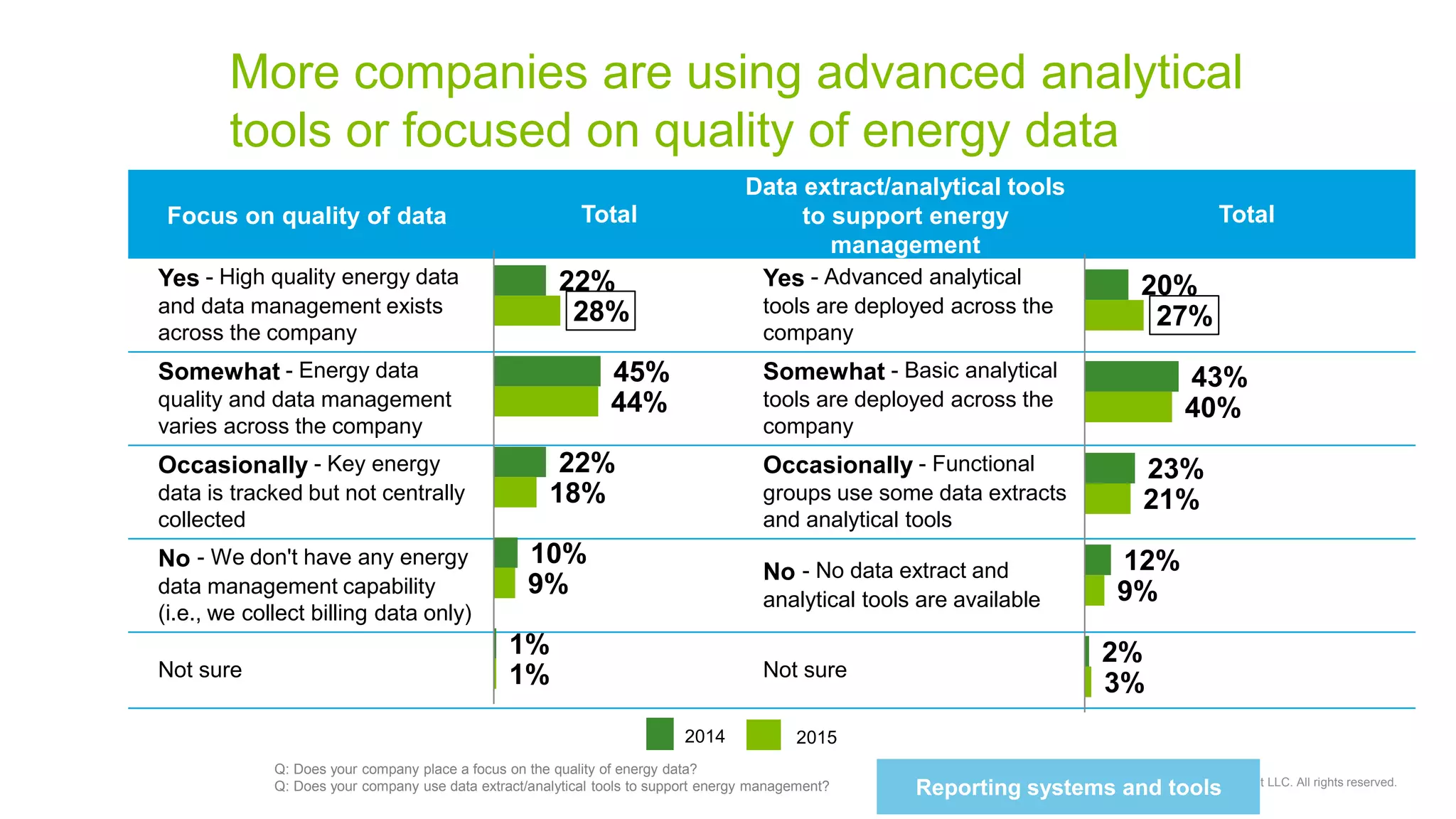

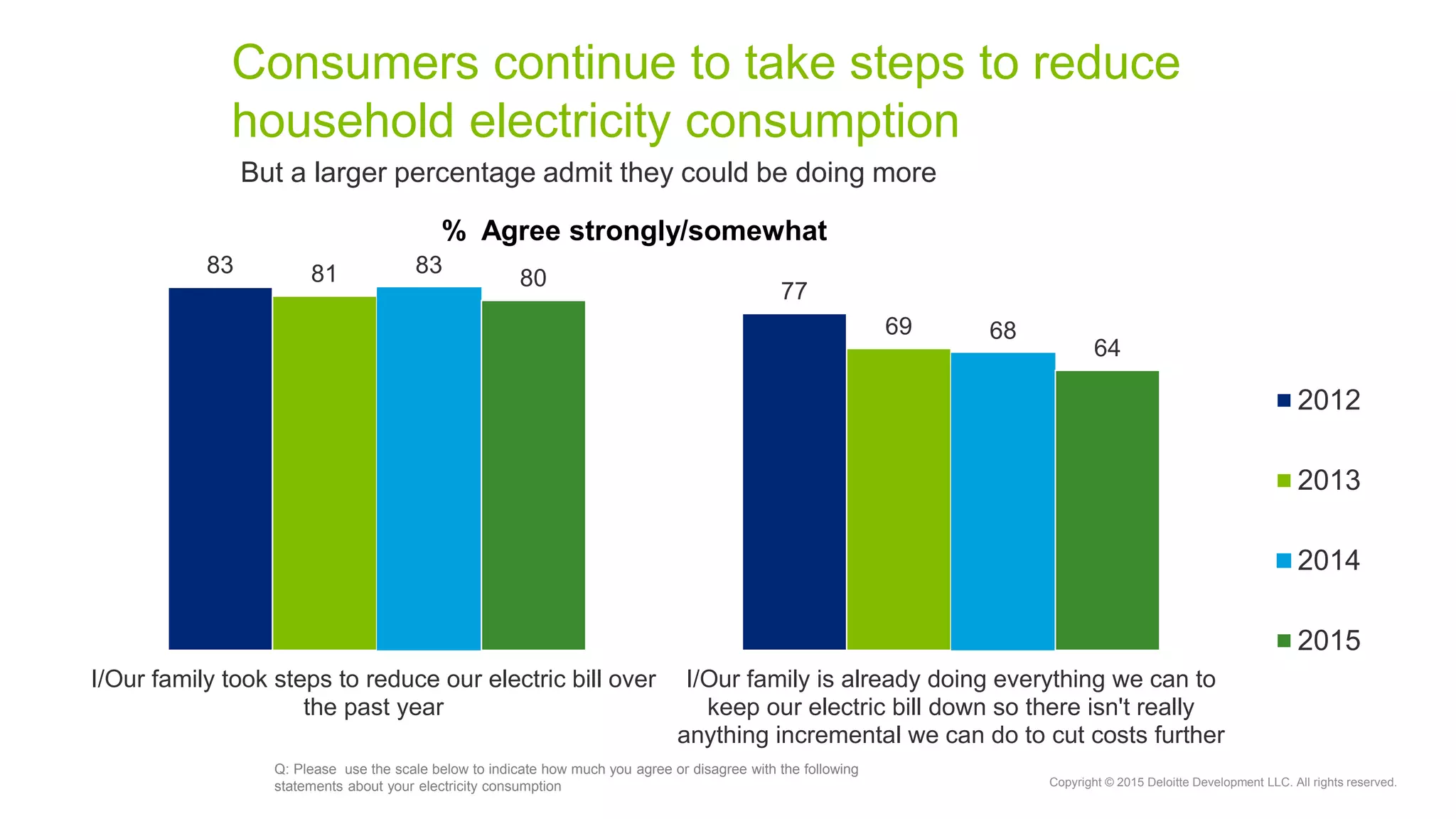

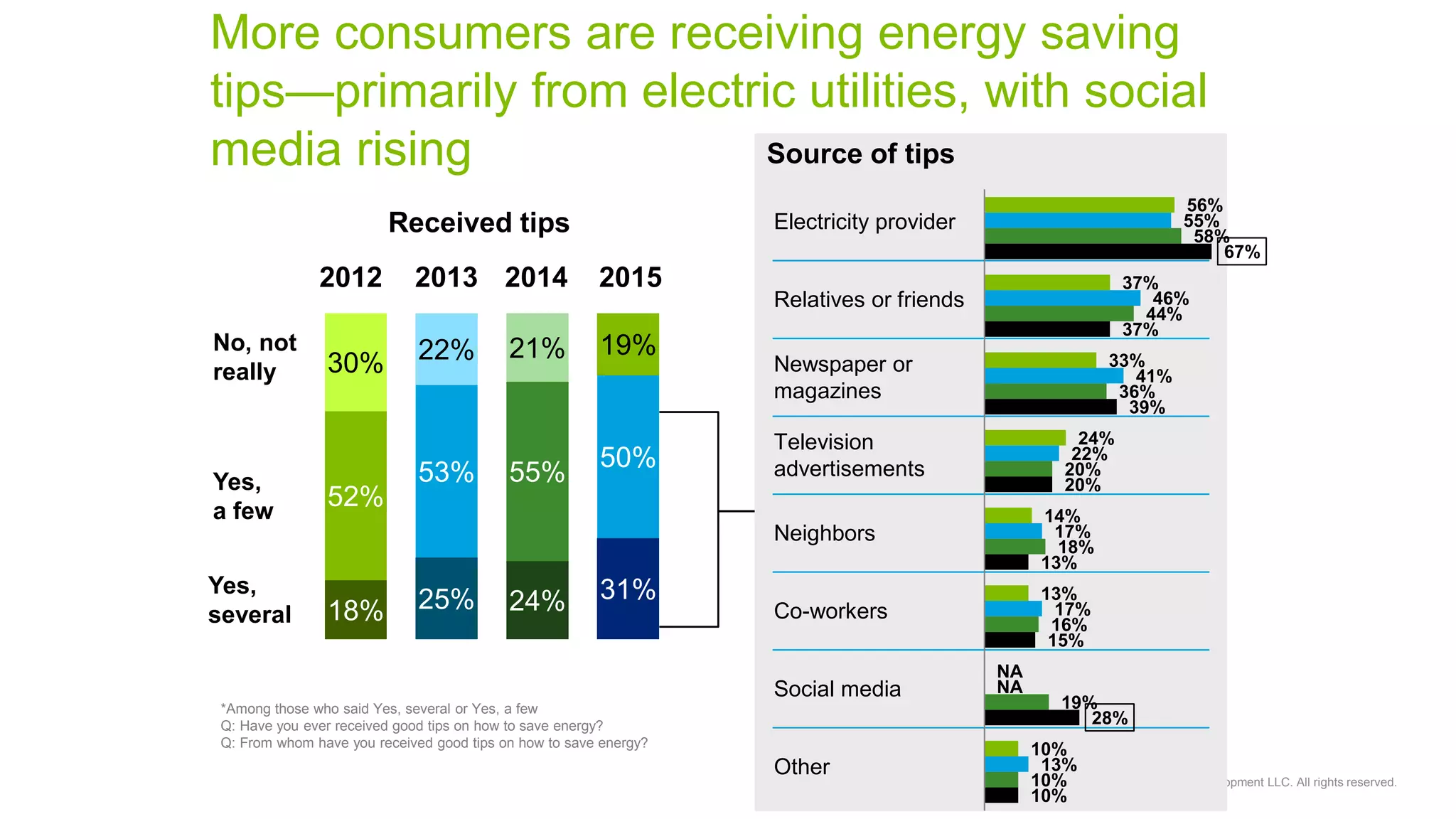

Energy management has become an essential part of corporate strategy for most businesses according to a Deloitte study. More companies now see reducing electricity costs as important to their competitive advantage, and have formal energy reduction goals. Most businesses have invested in energy management programs in the last three years, allocating a larger portion of their capital budgets to these efforts compared to previous years. Consumers continue taking steps to reduce energy usage but many feel they could do more, and more are receiving tips primarily from electric utilities but increasingly through social media.