Downloaded 149 times

![2.3

Overview to the Sub-Orbital Sounding Rocket Industry

Sounding rockets take their name from the nautical term ‘to sound’, which means to take

measurements. Sounding rockets have been in use since the 1950s and the technology used

in their design is relatively simple and based primarily on military missile technology. They

are used as an experimental platform to test instruments on satellites / spacecraft and to

provide scientific information about the sun, stars, galaxies and the earth’s atmosphere. This

type of testing is unique because it is simple, cost-effective and time efficient, also the

payloads used for experimentation can be developed in a short period of time, eg six months.

Sounding rockets are ideal for deploying Micro Gravity based experiments, ie those scientific

experiments that need to be conducted in a near zero effect gravitational environment. It is

possible to conduct micro gravity based experiments in high drop towers or by using a plane

following a parabolic flight curve, (as used for astronaut training). However sounding rockets

provide the ideal means of deploying these payloads as they are able to reach a far greater

height and more importantly the experiments can be conducted for longer periods of time.

The various micro gravity launch methods are compared below in Fig. 1 [1]. It is possible to

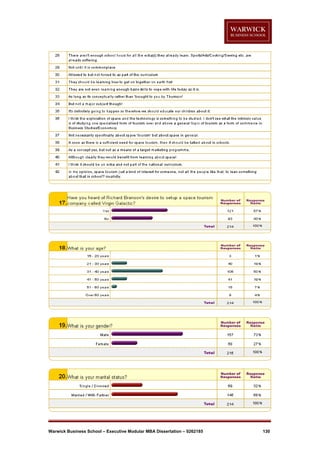

also conduct these experiments on either the Space Shuttle or ISS however the country

wishing to launch the payload would have to be a member of either the NASA or ESA space

programmes in order to gain access to these facilities.

Fig. 1

Comparison of Micro Gravity Launch Methods

Warwick Business School – Executive Modular MBA Dissertation – 0262185

13](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-13-320.jpg)

![Fig.2 [2] below shows a typical layout for a sounding rocket, the rocket is normally split into

two parts, the payload and the rocket motor. This is called a single stage rocket. For greater

height and hence longer experimentation times, multi stage rockets are used. The rockets

are modular in nature meaning that the rockets can be easily configured according to the

weight of payload being carried. In addition to the motor and payload, the rocket will contain

a simple guidance system, telemetry antenna (for transmitting results back to the ground) and

a radar tracking beacon so that the rocket can be tracked during flight.

Fig. 2 Typical Configuration for a Sounding Rocket

After the rocket is launched it follows a parabolic trajectory into space and as the rocket motor

uses its fuel, it separates from the payload and falls back to earth. Meanwhile, the payload

continues into space and when the payload reaches the top of the parabolic flight, ie at it’s

apogee, the experiments are conducted. In most cases, after the payload has re-entered the

atmosphere, it is brought gently down to earth by way of a parachute and is then retrieved. A

typical flight trajectory profile is shown below in Fig.3 [2].

Fig. 3 Typical Parabolic Flight Path for a Sounding Rocket

Warwick Business School – Executive Modular MBA Dissertation – 0262185

14](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-14-320.jpg)

![Scientific payloads are carried to altitudes of between 30 and 800 miles and although the

overall time spent in space is relatively short, (typically 5 to 20 minutes) the experiment is

perfectly positioned to conduct its mission successfully. As the scientific payload does not go

into orbit, sounding rocket missions do not need expensive booster rockets or extended

telemetry and tracking technology. Significant cost savings are realised as parts and rocket

motors are acquired in large quantities and they utilise tried and tested design configurations

for each launch.

In some cases, namely those missions conducting astronomy, planetary or micro gravity

experiments, the payloads are recoverable which means the costs of experiments and subsystems are spread over many missions. Scientists are able to accomplish their research at a

specific time and place because the sounding rockets can potentially be launched from

temporary sites all over the world. Due to the low cost and short lead time, sounding rocket

payload testing is invaluable for University students conducting graduate work in scientific

fields.

Sounding rockets offer one of the most robust, versatile and cost-effective launch systems

and in the case of NASA has provided nearly 40 years of critical scientific, technical and

educational contributions to the nation’s space programme. The reasons for their success

are as follows [3] :

Quick, low cost and fast access to high altitudes where optical observations of

astronomical, solar and planetary sources can be made of radiation at wavelengths

absorbed by the earth’s lower atmosphere

Direct access to the earth’s mesosphere and lower thermosphere (40-120km)

Ability to fly relatively large payloads (>500kg) masses on inexpensive vehicles

Provision of several minutes of ideal, “vibration free” microgravity

Ability to gather in-situ data in specific geophysical targets such as the aurora, the

equatorial electro jet and thunderstorms

Access to remote geophysical sites and southern hemisphere astronomical objects

Long dwell times at apogee

Ability to fly simultaneous rockets along different trajectories, eg with different

apogees, flight profiles etc

Ability to fly numerous free-flying sub-payloads from a single launch vehicle

Ability to recover and re-launch instruments

Warwick Business School – Executive Modular MBA Dissertation – 0262185

15](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-15-320.jpg)

![2.3.1

Review of the Primary Sounding Rocket Launch Providers

Today’s sounding rocket launch activities are mainly conducted in the US or Northern Europe.

Both NASA and ESA have active sounding rocket programmes and there are a number of

companies that build sounding rockets on behalf of these space agencies and for

independent research organisations.

These particular regions have been able to develop and sustain a reliable launch record and

for this reason other countries around the world tend to use these services rather than go to

the time and effort of developing their own sounding rocket launch capabilities.

Given that

the sounding rocket experiments are relatively expensive and sometimes irreplaceable, many

universities and research establishments prefer to launch their payloads with leading space

agencies such as NASA and ESA. The primary reason is to ensure that their payloads are

launched safely with good quality measurements being taken when the payload reaches

apogee. Commercial companies such as Orbital Sciences Inc. have been successful at

entering this market sector, primarily launching U.S Air Force related sounding rockets,

however their business model is changing to support small satellite related launches. The

following section identifies the key sounding rocket programmes.

2.3.1.1

European Based Sounding Rocket Programmes

Up until 2005, Europe had one of the oldest sounding rocket programmes, the British Skylark

sounding rocket service which was first launched in the 1950s. Skylark was initially flown

from the Woomera launch facility in Australia and was first operated on a commercial basis by

British Aerospace. This programme was then taken over by Matra Marconi Space and finally

Sounding Rocket Services (SRS) Ltd in 1999. Skylark [4] was flown for the last time in April

2005 from the Esrange range in Northern Sweden. Following the demise of the Skylark

programme, SRS now plan to become the European agent for the American built Oriole range

of rockets and a supplier of hardware to the German / Brazilian VSB-30 vehicle. ESA are

currently participating in four different sounding rocket programmes, namely the German

Texus and Mini-Texus programmes, the Swedish Maser programme and the joint German

and Swedish Maxus programmes [5]

The Texus and Mini Texus programmes were initiated in 1976 by the German Ministry for

Research as a preparatory programme to the 1983 Spacelab programme.

The Texus

programme was commercialised and is today managed by EADS-ST, Bremen. The Texus

programme employed Skylark VII rocket motors as the basis of its programme. The most

recent Texus rocket, Texus-EML1, was flown on 1st December 2005 and provided 7 minutes

of micro-gravity experimentation time. This particular flight used the Brazilian VSB-30 rocket

engine, the successor to the Skylark rocket motor.

The Mini Texus programme was

established to fill the gap in the market for projects requiring microgravity for the range of 3-4

Warwick Business School – Executive Modular MBA Dissertation – 0262185

16](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-16-320.jpg)

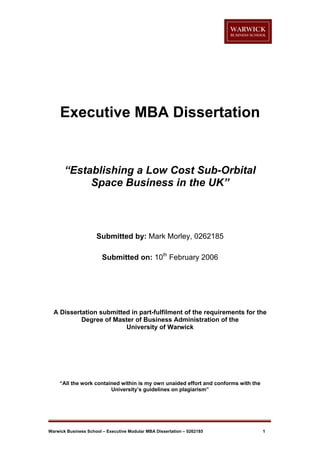

![NSRP customers are primarily from the university and government research groups however

some research activities involve the commercial sector. The programme has contributed

major scientific findings and research to the world of suborbital space science and has also

provided a valuable proving ground for space ship / station sub-components. There are

currently eleven operational support launch vehicles in the NSRP and all of these launch

vehicles utilise a solid propellant propulsion system. These rockets typically use surplus 2030 year old military rocket motors and all the rockets are unguided.

The NSRP uses three

main groups of rockets [6] and these are described overleaf and referenced in more detail in

Appendices 8-D & E [58]

Black Brant, produced by Bristol Aerospace Limited has been in service since 1962 and

provides the main ‘workhorse’ of the NASA sounding rocket fleet. Different versions of the

Black Brant can carry payloads ranging between 70 & 850 kilograms to altitudes from 150 to

1500 kilometres and can provide up to 20 minutes of microgravity time during flight. The

smallest Black Brant rocket is the Black Brant 5 single stage rocket and is used as the basis

of larger multi stage rockets from the Black Brant family. The most powerful rocket the Black

Brant 12 is a four stage vehicle that can launch a 113 kg payload to 1400 kilometres or a 454

kilogram payload to an altitude of at least 400 kilometers.

Oriole, produced by DTI Associates, was developed in the late 1990s to provide launch

services for commercial and scientific payloads.

Oriole is significant as it was the first

privately funded sounding rocket in the U.S and the first new sounding rocket for 25 years.

The Oriole, when combined with a Terrier rocket motor can reach an altitude of 385

kilometres providing between 6 to 9 minutes of microgravity time.

Terrier – Orion, produced by DTI Associates, is a two stage spin stabilized sounding rocket.

The Terrier-Orion can launch a payload weighing up to 290kg to an altitude of 190 kilometers.

2.3.2

Review of Sounding Rocket Launch Sites

Most of today’s global sounding rocket launch sites, have been developed from existing

missile test ranges and others have been established due to the restrictions with getting

access to some government owned launch sites.

One of the first sounding rocket test

facilities was established in Woomera, Australia and since then numerous sub-orbital launch

facilities have been established to cater for the sounding rocket market sector. The main

sounding rocket launch sites around the world are listed in Appendix 8-F.

From a U.S perspective there are two main launch sites, White Sands Missile Range, New

Mexico & Wallops Island, Virginia. All launches at these facilities are overseen by NASA and

hence it can be difficult to obtain a launch slot outside of the allotted launch programme. The

Warwick Business School – Executive Modular MBA Dissertation – 0262185

18](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-18-320.jpg)

![locations of these sites and other proposed non-federal launch sites are shown below in

Fig.5. [6] White Sands Missile Range is the Department of Defense’s largest overland

national range and is located in southern New Mexico approximately 35 miles northeast of

Las Cruces. The climate is semi arid with usually unlimited visibility, warm to hot temperatures

and a low humidity. The range covers an area of 8100 square miles making it ideal for the

launch and recovery of high altitude sounding rockets. The facility is operated by the U.S

Army and is also used for missile flight testing, rocket engine development and for conducting

experimental space craft flights.

Fig. 5 U.S Federal, Non-Federal and Proposed New Spaceports

Wallops Island is the location from which the majority of U.S sounding rockets are launched.

The facility was established in 1945 and since then there have been over 14,000 small rocket

launches from this facility. The facility is maintained by NASA and caters for both orbital and

sub-orbital launches. On average there are about 20 sub-orbital sounding rocket launches

per year. Moving forwards, the facility intends to become a centre of excellence for suborbital launches and the facility has been upgraded to include launch facilities for commercial

organisations.

From a European perspective there are two key sounding rocket launch facilities. They are

located in Northern Europe, the Esrange facility in Sweden and the Andoya range in Norway.

The Esrange facility is the operational centre for the Swedish Space Corporation (SSC) and

its location 200km north of the Arctic circle offers several unique advantages, namely

Warwick Business School – Executive Modular MBA Dissertation – 0262185

19](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-19-320.jpg)

![payloads from sounding rockets have a landing zone of 120 x 75 km in size. This makes it

ideal for easy payload recovery operations (this is the only place in Europe where payloads

can be recovered on land). The location is outstanding for the observation of the boreal

phenomena such as the northern lights and a good launch infrastructure is in place to support

space agencies from across the World. Nearly all of ESA’s sounding rockets are launched

from this facility due to its proximity to the Arctic Circle.

The Andoya range in Norway is unique as it stretches North West from Norway over the

Arctic and provides the most northern location in the World for a permanent rocket launch

facility. The facility was built in 1962 and is owned and operated by the Norwegian Space

Centre. Andoya range has conducted more than 650 rocket launches and has hosted nearly

70 universities and research institutes from around the World.

Its location provides

favourable conditions for studying various atmosphere and ionosphere phenomena and as

the launches are conducted over the arctic the airspace is relatively clear and there are hardly

any major shipping lanes to worry about. The facility has a large impact area, permitting a

variety of launch directions and rocket configurations without the need for guidance systems.

2.4

Overview to the Emerging Sub-Orbital Space Tourism Industry

The world’s first commercial orbital space tourism flight took place on April 28th 2001 when a

wealthy Californian investor Dennis Tito boarded a Russian Soyuz rocket to the International

Space Station at a price of $20million [7]. This made him the first individual to personally pay

for a ticket into space. This had two knock on effects for the Russian space industry. Firstly

they could see that there would be huge financial reward to their own space industry if they

supported these space tourism flights. Secondly the Russian space craft was considered to

be a fairly reliable space craft, despite its age, and it helped to improve its public image,

something the Americans were struggling to achieve with its ill-fated Shuttle programme.

Since Tito’s flight in 2001 two other space tourists have taken off on Russian space craft, in

April 2002 Mark Shuttleworth [8] became the second commercial space tourist as a member

of another mission to the ISS. More recently in September 2005 Greg Olsen [9], a U.S

scientist & entrepreneur, became the third space tourist. Both Mark and Greg were thought to

have also paid the Russian Space Agency $20million for the privilege of travelling to the ISS.

The Soyuz space craft is currently the only vehicle which can provide supplies to the ISS and

with there being three seats onboard and only two cosmonauts required to fly the Soyuz craft,

for the moment at least, this spare seat provides the only means for private individuals to

achieve orbital flight. Clearly the $20million cost per ticket of flying into space will have to be

brought down considerably if the orbital space tourism industry is to attract many more private

Warwick Business School – Executive Modular MBA Dissertation – 0262185

20](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-20-320.jpg)

![space travellers. These three privately funded space flights have demonstrated to the public

that space tourism is not only possible but will become more popular in the not too distant

future. According to the Futron Corporation, who conducted a Space Tourism Market Study in

2002 [10], there is a potential sub-orbital market for 15,000 passengers and $700 million in

revenues per year by 2021. The orbital space tourism industry is estimated to have 60

passengers who will help to bring in $300 million per year by 2021. This makes the industry

potentially worth $1 billion by 2021.

In terms of potential market growth, sub-orbital flight, simply due to its cost benefits, would

appear to be the main sector that will drive the space tourism industry. The main problem with

kick starting the sub-orbital space tourism industry is the availability of suitable space craft.

Up until now, nearly all space craft and launch services have been provided by the

government backed agencies such as NASA and ESA. These facilities were developed for

manned exploration, launching payloads into space and constructing the ISS. In order for this

industry to establish itself, a new breed of cheaper, more affordable, space craft and launch

facilities need to be developed. As with any new industry, companies will not invest time and

money in developing these space craft without a suitable incentive.

For this reason and to help kick start the space tourism industry a global competition was

established, and a significant financial prize offered, to the first non-government organisation /

company who could develop a reusable sub-orbital space craft. This competition was known

as the Ansari XPRIZE.

2.4.1

The Ansari XPRIZE Competition

The Ansari XPRIZE [11] is widely regarded as the catalyst for the emerging sub-orbital space

tourism industry and is based on a competition run in the 1920s, won by Charles Lindberg in

his Spirit of St.Louis aircraft, for the first aircraft to successfully cross the Atlantic. Once it was

shown that it was possible to cross the Atlantic by plane, other companies emerged and

started to develop aircraft which would one day help the birth of Atlantic passenger travel. The

Spirit of St.Louis proved that the principal barrier to commercial air travel was not a

technological barrier but more of a psychological one.

It was this competition that gave Peter Diamandis the idea of establishing the XPRIZE

Foundation. The aim of the XPRIZE Foundation was to create a future in which the general

public would personally participate in space travel and its benefits. The Ansari XPRIZE was

the first competition initiated by the XPRIZE Foundation and it offered a $10million prize to

establish the space tourism industry through competition amongst the most talented

entrepreneurs and rocket experts in the world.

Warwick Business School – Executive Modular MBA Dissertation – 0262185

21](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-21-320.jpg)

![The prize would be awarded to the first team that could :

Privately finance, build and launch a spaceship, able to carry three people to 100

kilometers , (the official start of space)

Return safely to Earth

Repeat the launch with the same spaceship within 2 weeks

The aim of repeating the launch was to prove that the spaceship could be reused rather than

having to rebuild a new spaceship from scratch each time. Since its inception in May 1996,

(up until the XPRIZE was won in October 2004), 27 teams from seven countries competed in

the prize. The aim of the prize was to :

Create a new generation of aviation heroes in the mould of Lindberg

Provide inspiration and education opportunities for students

Focus public attention and investment capital on this new business opportunity

To challenge explorers and rocket scientists from around the world

From its inception in 1996, many different designs of space craft were entered into the

competition. These ranged from conventional plane style craft which took off on a runway,

traditional multi-stage rockets complete with a three person space capsule, through to

vehicles that were towed or carried aloft to a high altitude before being released to travel to

their final apogee. Further information about the original XPRIZE contenders can be found in

Appendix 8-G. The XPRIZE was won in October 2004 by Scaled Composites and their

SpaceShipOne vehicle [12]. This was carried aloft by a high altitude plane called White

Knight. Once the White Knight had reached a specific altitude the SpaceShipOne rocket

powered plane would be released, its engines would be ignited and it would then continue up

to an altitude of 112 kilometers. It would remain on the edge of space for 5 minutes before

starting its descent.

SpaceShipOne then glided back to its original takeoff location.

SpaceShipOne is shown below in Fig.6 underneath its launch carrier, White Knight.

Fig. 6 SpaceShipOne Space Craft & White Knight Launcher

Warwick Business School – Executive Modular MBA Dissertation – 0262185

22](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-22-320.jpg)

![SpaceShipOne technology is currently owned by the co-founder of Microsoft, Paul Allen and

his company called Mojave Aerospace Ventures (MAV). He bankrolled the $20Million project

and even though the prize was only $10 million, the prestige of winning the XPRIZE combined

with the downstream commercial opportunities that would come along, made the investment

worth while.

2.4.2

Current Developments in Low Cost Space Craft Design

The original Ansari XPRIZE had 27 entrants competing for the $10 million prize. Today, only

7 of the original contenders remain in business and a number of new companies have

entered the low cost space launch industry.

Many of the original entrants to the competition

were designing craft which could be used after the XPRIZE, however a few companies

including Starchaser were designing their craft with one goal in mind, to win the XPRIZE.

Starchaser felt that using a single stage rocket would be the simplest and most cost effective

way of winning the XPRIZE. Starchaser were the second favourite entrant to win the XPRIZE

as they were the only other entrant to have actually launched an XPRIZE development rocket

prior to SpaceShipOne winning the prize.

The following table lists the original XPRIZE

contenders who are still developing space craft for the space tourism sector. Further

information about these companies can be found in Appendix 8-H [13].

Fig. 7 Post XPRIZE Contenders Currently in Business, (See Appendix 8-H)

The XPRIZE contenders, in most parts, were funded privately from numerous sponsoring

companies and organisations. They were able to develop significant space technology on a

minimal budget and in the case of Starchaser were able to develop a fully working rocket.

Their rocket ‘Nova’ was successfully launched in November 2001 and was subsequently used

to promote the XPRIZE initiative until the prize was claimed by Paul Allen’s company.

Compared to the government space agencies, the XPRIZE contenders were developing their

craft on relatively small budgets. Private enterprise will make or break the future space

tourism industry and during the latter stages of the XPRIZE competition a number of the

World’s most high profile billionaires decided that they wanted to get involved with the

privately funded commercial space industry. Fig.8 overleaf shows the new entrants to the

sub-orbital spacecraft market sector.

Warwick Business School – Executive Modular MBA Dissertation – 0262185

23](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-23-320.jpg)

![Fig. 8 New Entrants to the Privately Funded Space Industry

Further information about these companies can be found in Appendix 8-I. Virgin Galactic are

currently leading the way in terms of introducing economically viable technology but it won’t

be too long before other companies such as Starchaser develop their own technology to

compete in this market sector.

2.4.3

Emergence of Commercial Spaceports

As of today there are five non federal spaceports licensed in the U.S however due to the

expected growth in the private space sector, eight other locations in the U.S have applied for

a license to operate a space port. For private space companies such as Starchaser this is

important as it will provide them with a gateway into space without fear of imposing on any

government backed space programmes.

One of the first new spaceports has been

established in New Mexico with the help of the local government. They realised that the

private space industry could bring significant financial and employment benefits to its region

and with an abundance of wide open space it decided to apply to the Federal Aviation

Authority (FAA) for an official license to operate a non-federal spaceport. The Southwest

Regional Spaceport is located at Las Cruces, New Mexico and as part of its marketing

campaign recently hosted the global XPRIZE Cup, a competition for privately funded space

companies to demonstrate their capabilities.

The primary reasons that Las Cruces was granted an FAA operational license were [14]:

Its relatively high altitude, where the air is thinner, allowing rockets to be launched

much more easily

Approximately 350 days of sunshine annually, providing near perfect launch and

recovery operations

The availability of large, open, unpopulated land for establishing launch facilities with

unrestricted airspace

The availability of significant infrastructure along with access to a large population of

engineers and scientists that have previously been involved with a distinguished

history in space related research

Warwick Business School – Executive Modular MBA Dissertation – 0262185

24](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-24-320.jpg)

![The New Mexico Government commissioned Futron Corporation to estimate the potential

space tourism market size [14].

Using a number of quantitative and qualitative survey

methods they were able to estimate the potential total market size (in terms of number of

flights) shown in the first row of Fig.9. The New Mexico market share is shown in the second

row.

Fig. 9 Global Space Tourism Market Opportunity

It is expected that other spaceports will be developed overtime which explains the drop from

75% to 50% market share, however with New Mexico developing the first Spaceport they will

have a significant first mover advantage. Starchaser were the first space tourism company to

establish a base at the spaceport and now with Virgin Galactic wishing to establish a

significant presence in the region, New Mexico has the opportunity to position itself as the

primary destination for those interested in space tourism. Taking into account the space

tourism providers, visitors and spectators to the proposed rocket racing league developed by

XCOR, Futron expect the economic benefits to the region to be very significant, these are

highlighted below in Fig.10.

Fig. 10 Economic Value to New Mexico State

Over time, the Spaceport will expand considerably and will become home to a number of

space tourism operators, service companies and manufacturing operations. These activities

are summarised overleaf in Fig.11 [14].

The combination of Virgin Galactic, Starchaser and New Mexico State has for the first time

shown that space tourism for the masses is not only a reality but will be possible within 2

years. The technology has been demonstrated and proven, Virgin and Starchaser have the

vision that space tourism is economically achievable and the New Mexico State authorities

have the belief that they can lay the foundations for an entirely new industry which will bring

significant economic benefits to it’s region.

Warwick Business School – Executive Modular MBA Dissertation – 0262185

25](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-25-320.jpg)

![Fig. 11 New Mexico Spaceport Business Opportunities

2.5

Review of the UK’s Space Strategy

Today’s UK space strategy, prepared by the British National Space Committee (BNSC)

focuses on three core areas and is currently supported by the British Government with nearly

£200Million of funding. This is relatively small when compared to France which contributes

nearly £2Billion to its space efforts, making the UK a relatively small partner in the European

space industry. The UK’s space strategy maps out clear scientific and commercial objectives

rather than to develop space technology as an end to itself.

For this reason, the UK’s Vision is [15]:-

“To be the most developed user of space-based systems in Europe for science, enterprise

and the environment. UK citizens will provide and exploit the advanced space-based systems

and services which will stimulate innovation in the knowledge driven society”.

To achieve this vision the government has therefore decided to focus on the following :

To expand knowledge in astronomy, planetary and environmental sciences

To create opportunities for commercial exploitation of satellite systems

To advance key public services

Warwick Business School – Executive Modular MBA Dissertation – 0262185

26](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-26-320.jpg)

![2.5.4

Size and Health of the UK Space Industry

The commercial sector of the British space industry primarily supports the satellite industry.

This particular industry is split into two sectors, those companies providing space technology

for the satellites, the ‘upstream’ industry and those companies that actually exploit the satellite

services, namely the ‘downstream’ industry. In 2004 the BNSC conducted a survey of all UK

companies involved with space related business, 222 organisations were represented in the

findings [16].

The space related turnover of these companies varies over a wide range with only five

companies having a space turnover of £100Million and some 68% of the companies having a

space related turnover of less than £1Million. The total space related turnover of the UK

space industry is estimated to be £4Billion.

Compared to the upstream sector the

downstream turnover represents 87%of the total industry turnover. The breakdown of the

upstream and downstream sectors are shown below in Fig.13.

Fig. 13 The Upstream and Downstream Sectors of the UK Space Industry

The application of these activities is dominated by the telecommunications and broadcasting

industry, this application alone represents nearly 80% of all UK space industry turnover. This

investment has paid off as the UK is one of the World leaders in the adoption of digital

television services. Fig.14 below shows the turnover by space application. It is significant that

the space transportation sector represents only 1% of the total turnover.

Fig. 14 2003 Turnover by Application, Excluding the Consumer Market

Warwick Business School – Executive Modular MBA Dissertation – 0262185

28](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-28-320.jpg)

![2.5.5

UK Involvement with the ESA Programme

The UK is one of the founding members of the ESA programme which is divided into two

categories, optional and mandatory programmes. The UK chooses to take part in most of the

optional programmes, and membership of the mandatory programmes is subscription based

and rates are worked out as a percentage of each European country’s GNP. Fig.15 below

shows the various ESA programmes in 2001 and how the UK subscribes to programmes

which it feels best supports the UK space strategy, namely Navigation, Earth Observation and

Science [1]. Today, the UK contributions to ESA are roughly the same, this is despite the UK

being the second richest country, (behind Germany), in Europe.

Fig. 15 UK Financial Contributions to ESA Programmes

2.5.6

UK Micro-Gravity Activities

The main issue faced by the UK is that it does not have access to a dedicated micro gravity

environment. The UK decided not to be a member of the ISS when it was being discussed in

the 1980s. Similarly the UK has refused to become involved with micro gravity programmes

run by ESA.

The UK has decided to not participate in the European Life and Physical

Sciences (ELIPS) research programme and as such will not be able to get access to the

research and data derived from this programme. In 2002 , 102 UK researchers from 33

universities, 5 research institutions and 13 industrial companies were identified as potential

users of the ELIPS programme [1].

These researchers also formed part of the survey

population for this dissertation and the results will be discussed in Chapter 4.

Some UK universities have used sounding rockets for conducting micro gravity experiments

but with the demise of the Skylark programme the UK currently does not have a dedicated

launch facility for these experiments. As mentioned earlier, Sounding Rocket Services Ltd

are looking to re-introduce a new sounding rocket service in the near future.

Warwick Business School – Executive Modular MBA Dissertation – 0262185

29](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-29-320.jpg)

![Fig. 19 PEST Analysis of the UK Sounding Rocket Industry

Over the years the sounding rocket industry has seen many new entrants into a market which

was once dominated by the larger space agencies such as NASA.

Over time, smaller

companies began to emerge who subsequently took over from where the major agencies left

off. Today, NASA sub-contracts out the manufacture of the rockets for its sounding rocket

programme and numerous other companies have emerged, primarily in the U.S and Europe,

to compete in this specialised industry. The PEST analysis in Fig.19 provided a high level

overview to the industry as a whole and the companies competing within this industry are

analysed by way of Porter’s Five Forces [17], illustrated in Fig.20 below.

Fig. 20 Porter’s Five Forces Analysis

New Entrants – The space industry has always been perceived as a technically

challenging and high cost industry to enter. For this reason there are relatively few

companies involved in this industry. Government red tape, flight safety and

operational licenses from the respective aviation industry bodies all add to keeping

Warwick Business School – Executive Modular MBA Dissertation – 0262185

35](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-35-320.jpg)

![The Rutherford / BNSC report [1] noted that from a historical perspective, the life and physical

sciences research areas, (that exploit microgravity conditions), have never been a high

priority in comparison with other UK space related activities. One of the initial academic

research studies, the Pippard Report [18] , was conducted in 1989 by Professor Sir Brian

Pippard on behalf of SERC and it concluded that there was no strong case at that point for

the UK to join the ESA microgravity programme. Whilst many European countries signed up

with the construction of the ISS, the UK declined becoming involved with this project. This

negative attitude to any involvement with microgravity and the ISS continues to this very day,

with the government’s current space policy centred on “putting space to work”, ie needing to

identify clear scientific or commercial benefits from space activities before participating.

The microgravity review panel concluded [19] that there were a number of scientific

opportunities for microgravity based research and these were divided into six disciplines,

namely fundamental physics, fluid and combustion physics, materials science, biology,

physiology and astro/exobiology and planetary exploration. (The leading academics involved

with these areas of research were contacted as part of the research for this dissertation and

the results of the survey are discussed in Chapter 4).

In May 2000, ESA commissioned a strategic marketing study on the potential industrial

opportunities for microgravity based work. This was conducted by Batelle ITM, Cranfield

School of Management and Access-Matrix.

The common overall conclusion from these

independently conducted studies was that the tangible commercial returns in the field of

microgravity were far from being mature. They forecasted that the need over the next 5-10

years is for state sponsored basic research to establish a background from which a

partnership between industry and government can proceed to demonstrate potential, and

then for a similar further period before genuine commercially sponsored R&D would be

attainable.

The falling number of students choosing to study science and technology subjects at

university is a matter of widespread and growing concern in UK industry. Subjects which

involve space research are effective at generating interest in young people. One advantage

of having a UK microgravity research programme would be the opportunity to generate more

interest in science and technology amongst the young generation in particular.

At the time of the microgravity review panel research, the UK had a number of options with

respect to establishing a microgravity research programme, namely [19] :-

Warwick Business School – Executive Modular MBA Dissertation – 0262185

37](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-37-320.jpg)

![

Join ESA Programme (ELIPS), which would provide access for UK researchers to

European collaborations and facilities and provide significant commercial space

contracts to UK companies

Collaborate with NASA, this would only be possible if the UK were to become a

member of ELIPS

Collaborate with other U.S Agencies, this would allow UK institutions to make their

own arrangements but they would have to source their own funding rather than

depend on a central funding system

Use facilities of a commercial basis, Individual research groups would be free to

make use of ISS facilities either through ISS partners of one of the commercial

agents. Similarly most other microgravity facilities could be hired commercially from

the operators

Do nothing – Naturally the lowest cost option but there would be no involvement in

research or industrial collaborations, no access to results and more importantly a

poor political impression of the UK as a world-class player

Upon reviewing the available options, the review panel recommended to the UK government

that they should join the ELIPS programme at the minimum membership level. They believed

that while there was no single scientific area where such an investment would lead to a real

breakthrough there were a number of areas where access to this complimentary tool would

be of value. In May 2003 the UK government reviewed the panel’s report and based on the

findings decided not to sign up with the ELIPS programme due to limited budget availability

and lack of demonstrable commercial benefits to be gained [20].

The government also

highlighted the problems with the ISS and the issues associated with getting suitable launch

vehicles, such as the Space Shuttle, up to the ISS. The potential issues faced with

establishing a microgravity industry in the UK can be summarised by way of the Porter’s

Diamond [21] shown below in Fig.21

Fig. 21 Porter’s Diamond Summary of Potential UK Based Microgravity Industry

Warwick Business School – Executive Modular MBA Dissertation – 0262185

38](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-38-320.jpg)

![Starchaser’s sounding rocket programme has been designed to provide significant

advantages over its competitors, namely:

Skybolt will be the industry’s first reusable sounding rocket.

Many of today’s

sounding rockets are expendable meaning that new sounding rockets currently have

to be built for each launch.

This is both very expensive and a drain on a limited

supply of rocket engines. The other issue associated with today’s sounding rockets is

that they are being designed to carry more than one scientific payload.

So for

example the latest MASER rocket carried six different payloads. In order for the

MASER rocket to be economically viable it must carry its full payload capacity

otherwise it will be launched at a significant loss. Having to wait for six payloads to

be ready for launch puts a significant time delay on the launch of the MASER rocket

and hence makes it very inflexible from a launch timing point of view. The reusable

nature of Skybolt will hopefully alleviate this problem and allow payloads to be

launched on a more frequent basis.

Skybolt will also represent one of the lowest cost sounding rocket services.

Starchaser have had to manage for years on a minimal development budget but they

have proven that they are capable of developing high altitude rockets. The lack of

budget has actually worked in Starchaser’s favour as they have been able to design

and build rockets using cheaper materials and manufacturing processes, more

importantly without compromising on safety or performance grounds.

Starchaser’s current strategic position is therefore summarised by way of Fig.23 below [17]

Fig. 23 Strategic Focus of Starchaser’s Sounding Rocket Programme

Warwick Business School – Executive Modular MBA Dissertation – 0262185

41](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-41-320.jpg)

![In the context of the whole space industry, Starchaser’s Skybolt programme is targeting a

narrow market segment, namely the sounding rocket market sector. Starchaser’s current

strategy is to adopt a significant product differential over its competitors (ie the reusable

nature of Skybolt) which in turn will help to drive down overall launch costs. In terms of

improving a company’s competitive advantage there are three recognised approaches,

adopting either a specific product focus, product differentiation or product cost leadership.

The reusable nature of Skybolt and its uniqueness in the sounding rocket market means that

Starchaser should be following a differentiation strategy which has the characteristics shown

below in Fig.24 [22]. Other more general company related strategies and issues will be

discussed in section 3.4

Fig. 24 Competitive Advantage through Product Differentiation

3.3

Review of the Space Tourism Market Sector

As highlighted in the previous chapter, space tourism potentially represents a lucrative

$1Billion a year industry by 2020. Initially the main area of development will be the sub-orbital

market sector and then as technology is developed and the investment community start to

take an interest then orbital space tourism will develop very quickly. Prior to the winning of

the XPRIZE in late 2004 it has been the orbital space tourism sector which has received most

interest from the academic community. For example predicting what it would be like to orbit

the earth as a space tourist, what business opportunities could evolve, eg orbital space hotels

and space sports centres.

Warwick Business School – Executive Modular MBA Dissertation – 0262185

42](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-42-320.jpg)

![Fig.25 below tries to predict what the orbital space tourism market and associated

opportunities, could be like by 2030 [23]. Clearly, significant investment and technological

advances will have to be realised before this vision can become a reality and the recent

interest in sub-orbital space tourism ignited by the XPRIZE competition has led the academic

community to re-focus their research into the short term business opportunities rather than

the long term. Orbital space tourism will happen one day and U.S billionaire Robert Bigelow

has established a new $50 million competition [24], similar to the XPRIZE, for the first

company to design a reusable orbital spacecraft which can be used to service his proposed

network of orbital space hotels. It is forward thinking entrepreneurs such as Bigelow and

Branson that will help to kick start the future orbital space tourism industry.

Fig. 25 Space Tourism Market Opportunities by 2030

Today’s academic sub-orbital market research research focusses on :

Trying to establish the potential market demand for what is a completely new and

unknown industry and then trying to predict the likely ticket price per trip into space

Estimating potential economic benefits, eg the Futron study conducted on behalf of

the New Mexico State government

Establishing which of the current sub-orbital space tourism companies are likely to

succeed based on their proposed spacecraft designs, individual business models,

marketing capabilities and proposed methods of financial investment

Trying to work out how to market and position a space tourism company, within an

entirely new industry sector, to a general public that knows little about the industry

The likely human ‘endurance’ implications for passengers wishing to take such flights

The technological barriers which have to be overcome to develop a cost effective

space craft design

Warwick Business School – Executive Modular MBA Dissertation – 0262185

43](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-43-320.jpg)

![3.3.1

Sub-Orbital Space Tourism Industry Analysis

One of the World’s leading authorities on space tourism is Professor Geoffrey Crouch from La

Trobe University in Australia.

Professor Crouch has written a number of space tourism

research papers which address some of the afore-mentioned key areas of the space tourism

market sector. Some of these will be discussed later in this section but first, the following

PEST analysis shown in Fig.26 below, (adapted from one prepared by Professor Crouch,[25])

attempts to highlight the current issues facing the sub-orbital space tourism industry.

Fig. 26 Sub-Orbital Space Tourism Industry PEST Analysis

The future direction of the space industry lies in part with what the major space agencies such

as NASA and ESA will do. They have already started to sub contract work out to companies

such as Orbital Sciences but they will need to do more to help small private firms enter what

is currently a very lucrative market. NASA suffers from two externally controlled forces,

uncertainty concerning its funding because the granting agency, the US congress, changes

elected membership every two years and in addition, members of congress have repeatedly

changed the content of NASA programmes to benefit the private space contractors within

their constituency [25]. This situation has called for privatisation of the space industry [26]

which will open up more commercial opportunities for entrepreneurs to establish new

commercial space companies. The recent success of projects such as the XPRIZE has

helped to highlight what small companies are able to achieve on relatively small budgets.

Warwick Business School – Executive Modular MBA Dissertation – 0262185

44](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-44-320.jpg)

![A viable commercial space tourism industry will require a clear legal framework to facilitate

and encourage developments in space tourism [24], rather than the existing legal regime

which originated during the cold war era. Legal issues that need addressing include the need

for co-ordination of potentially high frequency space launches (availability and desirability of

insurance for spacecraft / owners / operators / passengers and even the drafting of new

criminal laws to apply in a space context, (eg anti terrorism / hijacking etc). If the space

tourism industry is to flourish then these issues need to be addressed at an international level

rather than have different laws for each country.

Although governments may play an

important regulatory role, and the use of government assets may be a part of a space tourism

industry for some time, the real driving force behind space tourism, apart from customer

demand will be the financial returns that arise from new competition and enterprise. (Grouch,

2004)

3.3.2

Competitive Analysis of the Space Tourism Market

The space tourism market today is very much in it’s infancy with some of the original entrants

to the XPRIZE competition trying to transition their projects into commercial sub-orbital space

tourism businesses. As Virgin Galactic [27], in partnership with Burt Rutan, won the XPRIZE

they are perceived for the moment to be the market leaders (in terms of proven technology)

but the true measure of success of the venture will depend upon how quickly they can bring

their SpaceShipTwo craft into service. At the moment this is scheduled for 2008. Since the

XPRIZE competition, Virgin Galactic have used the marketing muscle of the Virgin Group to

help promote and position the company as the world’s only ‘viable’ space tourism company.

Virgin Galactic certainly has the technology and marketing skills in place to help build their

business but there are other companies aiming to take on Virgin Galactic in the future.

The nearest competitor is Starchaser, primarily as they were perceived as the only serious

competitor, other than Virgin Galactic to win the XPRIZE. From an XPRIZE point of view the

‘competition factor’ was measured by how much ‘working & demonstrable’ technology was in

place. Starchaser had completed a number of launches in the past and another 12 months

work could have seen them winning the XPRIZE ahead of Virgin Galactic.

There are many other companies continuing to develop sub-orbital technologies, most of the

XPRIZE teams had conducted engine tests but had never flown a full size version of their

craft. Other companies such as XCOR have developed a rocket plane to be used in the

Rocket Racing League competition, a further development of this craft, called Xerus, will

allow XCOR to enter the sub-orbital tourism market. One other competitor to watch out for

over the next few years will be Blue Origin [28], funded by the Amazon CEO Jeff Bezos, they

currently do not have any demonstrable technology to speak of but they are determined to

Warwick Business School – Executive Modular MBA Dissertation – 0262185

45](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-45-320.jpg)

![Virgin Galactic and Starchaser represent two completely different companies, one is well

funded with a global reputation for marketing expertise and risk taking whereas the other is

very much smaller, with minimal budget but a significant industry and knowledge base to offer

the potential of one day being a large and success full space tourism company. Richard

Branson and Steven Bennett share a desire to be successful at everything they do and if

necessary take risks to achieve their respective goals. They are both entrepreneurial in

nature and are sometimes referred to today as tomorrow’s ‘Astropreneurs’ [29].

3.3.3

Estimating Market Demand for Space Tourism Services

One of the key factors to the success of the space tourism industry will be the ability to

accurately predict the market demand levels for sub-orbital flights. A number of surveys have

been conducted to gauge the general public’s thoughts on space tourism. (This dissertation

undertook a similar survey and the results to which are discussed in Chapter 4). The one

common question asked by all surveys was “how much would you be willing to pay for a

space flight”. Market demand or in this case ‘interest’ [30] in terms of number of people willing

to take a trip into space was thus mainly determined by the price of the flight. Numerous

space tourism surveys have been conducted over the years and each one has provided

interesting feedback on the likely demand for space tourism services in the future. The overall

market elasticity was calculated by Ivan Bekey [31], this summarises the various price /

demand estimations and is shown by way of the graph in Fig.29 below.

Fig. 29 Estimating the Elasticity of the Space Tourism Industry

Warwick Business School – Executive Modular MBA Dissertation – 0262185

48](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-48-320.jpg)

![Once all the demand curves had been placed on the graph it became clear that the overall

demand trend highlighted that space flight ticket prices would become within the grasps of the

average person once ticket prices were between $5k and $10k. The survey conducted for

this dissertation showed that a significant number of respondents would be willing to pay up to

3 months average salary to take a sub-orbital space flight, (this ties in with the estimation

provided above). It will only be possible for the prices to come down once the technology is

‘in service’ and there are enough operators to encourage competition.

It has been argued that most of these surveys will have been very simplistic, measuring

‘interest’ instead of true ‘demand’ for space tourism [25]. One also has to consider that the

wide variety of possible space tourism products and experiences that might develop, will

affect potential demand tremendously as a function of the attributes of the various alternatives

which might emerge, [25].

In addition to ticket price, Crouch [30] highlights a number of other market factors which may

influence demand, eg how will the design of the spacecraft affects ticket reservations, ie plane

style or conventional rocket style. Each method of travel affects other factors such as cost,

risk, flight duration, comfort, training requirements, viewing configurations, launch and return

locations. Every passenger will subliminally assess all these variables before choosing which

operator to fly with. Therefore, with so many variables being measured within a new market

sector and with no previous comparable market demand data to work from, how can the

demand be estimated ?

There are a number of behavioural theories and research methodologies which can

potentially address these challenges. Discrete Choice Modelling, DCM, [32] using Random

Utility Theory (RUT), [33], combined with Information Acceleration (IA) [34], provides a

rigorous and reliable means for making progress in answering problems of this nature.

Gathering the data required to enable the DCM of consumer choice in space tourism would

therefore entail the design and execution of consumer choice experiments [30]. An example

of the attributes making up a consumer choice experiment related to space tourism is shown

in Appendix 8-M, [30]

In addition to the consumer choice experiment above which relies on probability to help

determine the ‘estimated’ market demand a much more simpler way would be to try and use

data that exists at the moment to form the basis of an estimation. In order to secure funding

from the investment community, they prefer to see hard facts relating to market demand

rather than the estimates derived from an extrapolated graph. Two leading experts from the

financial community, [35], proposed that a more accurate picture could be established by

using suitable figures from the World Wealth Report [36]. An overall market potential of over

Warwick Business School – Executive Modular MBA Dissertation – 0262185

49](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-49-320.jpg)

![40,000 people was calculated and conservatively estimating that 0.56% of high income

people would actually buy a ticket. The maximum ticket price was assumed to be $100k. The

demand figure was suitably high and gives a high enough safety margin. There is even room

for competitors hence the data shown below in Fig.30 presents a strong business case.

Fig. 30 Estimated Ticket Demand Based on World Wealth Report

3.3.4

Financial Investment Issues Associated With Space Tourism

Securing financial investment for space related technology development is one of the biggest

hurdles with developing a space tourism business. The XPRIZE was won by a company

funded by one of the richest men in the World, namely Paul Allen co-founder of Microsoft. If

he had not provided the $20 million investment into his Mojave Aerospace Ventures to

develop SpaceShipOne then there is a chance that organisations would still be competing for

the XPRIZE today.

A number of billionaires have now entered the space tourism industry, Jeff Bezos (Amazon

CEO), Richard Branson (Virgin Group) and of course Paul Allen (Microsoft) to name but a

few. These men are regarded as risk takers and are willing to put up money for a venture

which has a potential for a good return.

Venture capital companies are also renowned for investing in risky businesses however the

space tourism industry is an unknown quantity and many venture capital firms shy away from

providing funding with the following reasons being highlighted by Dr Livingston and venture

capital company Colony Fund LLC [37]

Warwick Business School – Executive Modular MBA Dissertation – 0262185

50](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-50-320.jpg)

![In addition to a very strong business and marketing plan, a venture capital company will

require the following characteristics when looking to invest in a project :

Exceptional management teams

Clear value propositions

High growth markets

Strong competitive position

Focused and differentiated technologies

Substantial gross margins

The apparent ‘signal to noise’ ratio [37] of today’s space enterprises is significantly high, with

some of the ex-XPRIZE contenders being the main examples of companies promoting nonviable business plans involving unrealistic concepts that deters VC’s from placing funds into

the industry.

The problem is that these companies are actually putting up a barrier for

companies such as Starchaser who have actually got their hands dirty with the technology

and who now need guidance as how to take their business to the next stage of evolution.

Some typical questions asked about the robustness of a space tourism startup are ;

Can the company raise what it needs under the projected market conditions ?

Can the company carry the cost of capital even if there is a slip in schedule ?

How high are the safety margins in the cash flow plan ?

If a space entrepreneur has to present a financial proposal to the investment community then

the following aspects should be researched in detail [35],

Parameter

Drivers

Cost of Capital

Debt / Equity Ratio

R & D Cost

Technology Maturity Level

Time to Market

Project Management / Regulatory Env.

Revenue Expectations

Overall Demand Competition

Fig. 31 Key Information Sought by the Investment Community

Warwick Business School – Executive Modular MBA Dissertation – 0262185

52](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-52-320.jpg)

![3.4

Review of Starchaser’s Current Business Strategy

Starchaser have matured immensely over the last ten years, starting out as a group of people

developing small rockets on a part time basis to now having ambitious plans to establish a

presence in the sounding rocket & emerging sub-orbital space tourism industries. This shows

that they have the entrepreneurial spirit and determination to grow their business. Unlike most

of the XPRIZE entrants, Starchaser have been able to keep their business afloat by securing

additional outside investment from private individuals and by developing a range of other

revenue generating initiatives. These activities have allowed Starchaser to continue to

develop their technology and to get the business to a position where it can begin to structure

itself so as to make itself attractive to the investment community.

3.4.1

Company Strategy

It is recognised that there are four stages to the effective development of an organisation,

Mission & Objectives describe what an organisation is looking to do and Strategy & Tactics

are the methods of how they will be achieved. This has simply become know as the M.O.S.T

method [38] of applying a systematic approach to business development which will increase

its long term stability and effectiveness. This model allows organisations to focus its

resources and provides a foundation on which to evaluate its performance. In terms of

identifying if Starchaser are undertaking the correct initiatives to help grow their business the

M.O.S.T analysis was used to examine their current business strategy.

Fig. 32 M.O.S.T Method of Analysing Business Growth

Using this method of analysing Starchaser’s current business strategy, their primary Mission

is to:

Provide a safe , reliable and affordable access to space for all

To become the market leader in non government space access

To be recognised as ‘the’ British Space Programme

Warwick Business School – Executive Modular MBA Dissertation – 0262185

53](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-53-320.jpg)

![Fig.35 attempts to show how each service will mature and we can see for example that the

sounding rocket service will be brought into service relatively quickly as the technology being

used is fairly mature and Starchaser already have significant experience in this area. It is

hoped that the sounding rocket service will become Starchaser’s initial source of income to

allow the continued development of the next stage of their programme. Their sub-orbital

service will require a longer period for R&D due to the additional requirement of carrying

passengers, but once again some of this work has already been conducted as part of the

XPRIZE competition. Overtime it is hoped that the lessons learnt developing sub-orbital space

technology will be applied to the orbital programmes that Starchaser would like to develop in

the future. Interplanetary travel is seen as a very long term goal and will require significant

financial investment.

Before Starchaser can devise a comprehensive business plan to take to the investment

community, they will need to undertake a number of assessments as to whether the company

is ‘ready’ to enter these new markets. According to Dr John Mullins [39], they will need three

crucial elements, a market, an industry and a core team of people to be able to successfully

execute the strategy. To assess whether Starchaser can reach each stage of their proposed

growth pyramid, Mullins recommends analysing each stage using the seven domains of

attractive opportunities.

The seven domains are shown overleaf in Fig.35 and each is

explained in more detail in Appendix 8-N.

Fig. 35 Seven Domains of Market Attractiveness

Warwick Business School – Executive Modular MBA Dissertation – 0262185

56](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-56-320.jpg)

![On first glance this model appears to highlight the normal issues when assessing a business

opportunity but there are three additional observations which are often missed, according to

Mullins, by entrepreneurs and some investors :

Markets and industries are not the same thing

Macro and micro level considerations are necessary, also markets and industries

must be reviewed at both levels

The keys to assessing entrepreneurs and their teams aren’t simply found on their

resumes or in assessment of their entrepreneurial character.

The PEST analysis of the proposed new market sectors was highlighted earlier along with a

SWOT analysis of Starchaser and their ability to enter these sectors. The critical factor now

is whether Starchaser has the correct internal resources to be able to drive the proposed

business strategy. The questions highlighted in Appendix 8-N [39] will help Starchaser to

effectively ‘road test’ their business ideas and identify what their internal needs will be in order

to develop an appropriate business plan to execute their proposed strategy.

In terms of assessing where Starchaser are now with respect to the growth of their company

we can use Greiner’s model of the five stages of growth [40] of a company to identify the

position of Starchaser according to its size and age. This is illustrated below in Fig.36.

Fig. 36 Position of Starchaser with Respect to its own Growth

Warwick Business School – Executive Modular MBA Dissertation – 0262185

57](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-57-320.jpg)

![At the moment Starchaser would be considered to be positioned near the beginning of phase

3 of the growth through delegation phase. Phases 1 & 2 saw Starchaser develop its early

rocket programmes before moving onto developing a rocket to compete in the XPRIZE

competition. The company is now growing strategically by choosing two projects, Skybolt &

Thunderstar and developing a business plan to bring these projects to market in order to bring

further investment into the company.

To explain this further and understand how a company grows from a people perspective, it is

important to understand the individuals that actually work for the company. According to

Sykes [41], you need the correct mix of people to be able to initially grow the organisation.

Sykes proposes that there are three types of people to be found in a company, namely

Envisioners, Enablers and Enactors and at company startup phase they should all be aligned

around a unifying vision or shared mission. The envisioner has the ability amongst an

individual or group to conceptualise.

Entrepreneurs are categorised as envisioners as they are responsible for generating the initial

business idea but then it is up to the enabler to take the envisioner’s idea and put it into

production. Finally the enabler gets the enactors to actually undertake the work in hand.

Fig. 37 Metamorphosis of a Company

Warwick Business School – Executive Modular MBA Dissertation – 0262185

58](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-58-320.jpg)

![Fig.37 on the previous page shows how the organisational structure changes over time,

initially you have the three Es at the start up of ‘Egg’ phase, as time moves on, rapid growth is

seen, the external environment changes and more resources are required. At point A on the

graph a period of ‘second thinking’ [41] is required to re-evaluate the organisation of the

company and if required bring in more people to delegate responsibility to. This process

repeats itself and the organisation grows organically into a ‘butterfly’ until a point is reached

where the product or service is brought to market. The important thing to note is that the

whole organisational structure is designed around the vision for the company and its

products.

From Starchaser’s point of view they are transitioning into the enlargement phase, shown by

the yellow star and expanding their business around the two strategies defined earlier. This is

backed up with the recent news that Starchaser has opened up a U.S office in New Mexico

and the CEO has delegated responsibilities to two new employees over there.

Up until

recently the CEO was undertaking both the envisioning and enabling role, ie minimal

delegation.

Moving forwards, the CEO needs to appoint an Operations Manager or

equivalent to undertake the day to day management tasks of running the business whilst he

focuses his time on developing the new business plan and securing new funding from

investors.

3.4.2

Marketing Strategy

In order to try and assess Starchaser’s marketing activities, the framework [42] shown in

Fig.38 overleaf was applied to examine their marketing mix, strategy and macro environment

that they currently operate in. Starchaser’s perceived marketing strengths / awareness are

shown by way of the yellow highlighted text.

From a marketing environment point of view Starchaser have a very good understanding of

the target markets they wish to enter. Starchaser have been around for many years and

during this time they have established a very good understanding of the macro environmental

issues which could affect their business.

They have a strong link with the XPRIZE

Foundation, the organisation that will help to develop the new space tourism industry and they

have a new relationship with the Governor of New Mexico State, the location of the

Spaceport. The PEST and SWOT analysis conducted earlier in this dissertation will help to

re-enforce Starchaser’s understanding of the environment that they will be operating in.

Warwick Business School – Executive Modular MBA Dissertation – 0262185

59](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-59-320.jpg)

![Fig. 38 Review of Starchaser’s Marketing Activities

From a strategy point of view, as highlighted earlier, they are currently focused on a

differential advantage strategy both in terms of a reusable sounding rocket and a traditional

rocket for space tourism. The next stage is for Starchaser to derive the marketing strategy for

each new sector and to start thinking about how they wish to position their products in the

market space. The next major issue faced by Starchaser is to work out how to position their

brand as the provider of low cost sub-orbital sounding rocket and space tourism services.

Ideally, when people think of space tourism they will immediately think of the name

Starchaser. According to Dibb& Simkin [43], a brand can have five groups of key attributes.

The attributes shown in Fig.39 represent the current perception, by the author, of the

Starchaser brand name.

Fig. 39 Starchaser Brand Characteristics

Warwick Business School – Executive Modular MBA Dissertation – 0262185

60](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-60-320.jpg)

![Starchaser are in a position where they have a very strong company name, unique and at the

same time relevant to the industry that they serve, but they now need to develop the brand

still further in order to try and compete with one of the strongest brands in the World, Virgin.

Dibb&Simkin [43] suggest that a successful brand should have six key characteristics and

these are shown in Fig.40 below.

Fig. 40 The Characteristics of a Successful Brand

Starchaser’s brand currently meets three of these criteria. The company name and identity

are unique in the market, they have a long term growth plan to develop their business and

enter new markets and they have a differential strategy for competing with other companies.

To develop the brand further they need to focus on developing the other three characteristics

shown in red.

One of the issues that needs addressing is related to the area of integrated marketing

communications. In order to further develop their brand strength they need to ensure that

there is a consistent ‘brand image’ across the whole company. Moving forwards Starchaser

need to develop a Branding Guide which will allow the management of all logos, colour

schemes and fonts to be used in all electronic and printed materials. In addition, Starchaser

need to start registering all logo designs and trademarks to prevent brand identity theft. The

brand, in terms of company name, is one of their biggest assets, which needs protecting.

Ever since Starchaser was formed they had a very strong logo and text font which was

immediately identifiable with the Starchaser brand.

Starchaser recently employed the

services of a marketing communications company who decided to give the company a fresh

look by re-designing their logo.

Warwick Business School – Executive Modular MBA Dissertation – 0262185

61](https://image.slidesharecdn.com/spacetourismmbadissertation-mmorley-140308063526-phpapp02/85/Space-Tourism-MBA-Dissertation-61-320.jpg)

![8

Appendices

Appendix 8 - A Review of Today’s Global Orbital Space Industry

Over the last thirty years there have been two main competitors dominating the space

industry, namely the United States and Russia. During the cold war of the 1970s and 1980s

most space launches were related to government funded defence programmes. This period

saw an extensive network of global spy and reconnaissance satellites being placed into orbit,