Downloaded 13 times

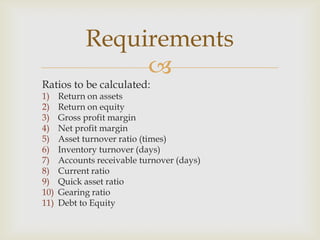

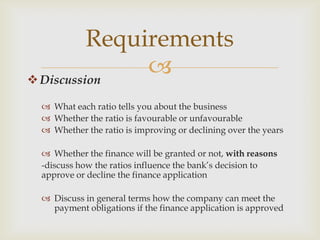

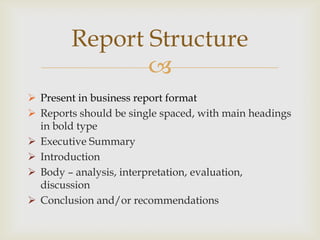

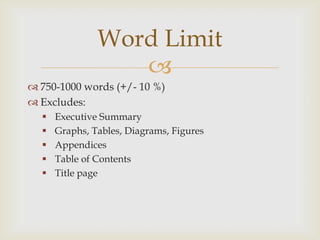

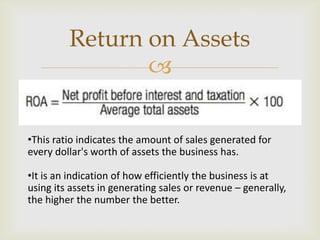

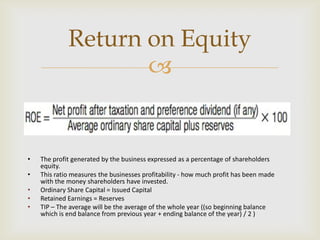

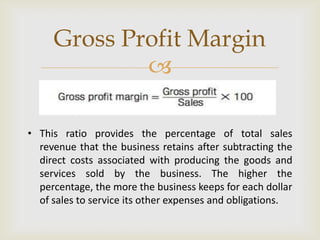

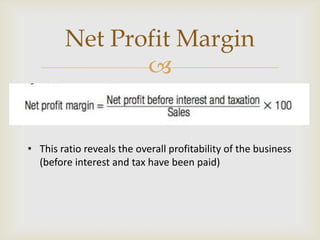

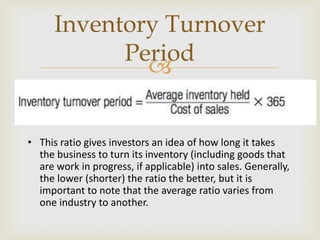

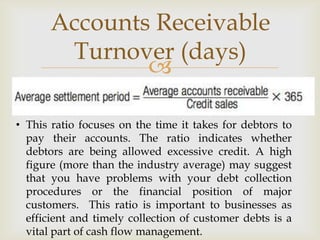

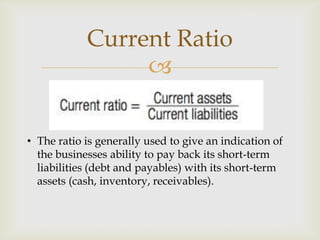

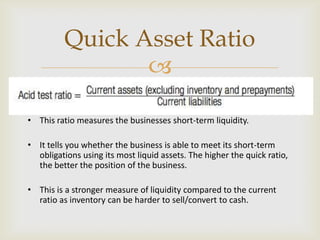

This document provides instructions for a ratio analysis assignment due on May 19, 2014. Students are required to calculate 11 financial ratios for the years 2010, 2012 and 2012 using the company's data. The ratios must be grouped under profitability, efficiency, liquidity and capital structure headings. Students must show the calculations and formulas in an appendix. In the main report, students must discuss the significance of each ratio, trends over time and how the ratios would influence a bank's decision to approve or decline a loan application for the company. The report must follow a specified structure and word limit. Detailed descriptions and examples of how to calculate and interpret each ratio are provided.