Download as PDF, PPTX

The document explains the concept of gearing ratio, which measures a business's reliance on debt versus equity for funding its assets. It discusses various definitions of debt used by lenders for calculating this ratio, their implications on risk assessment, and the importance of understanding the nature of the debt (long-term vs. short-term). Additionally, it highlights that the optimal gearing ratio varies by industry and provides guidance on interpreting these ratios and considering preference shares and shareholder loans in calculations.

Introduction to the concept of gearing ratio from Business Banking Coach.

Gearing, or leverage, describes a business's mix of debt and equity funding used to finance its assets.

Lenders are interested in the gearing ratio as it indicates a business's reliance on external funding.

Different lenders may define 'debt' differently, affecting the gearing ratio's calculation.

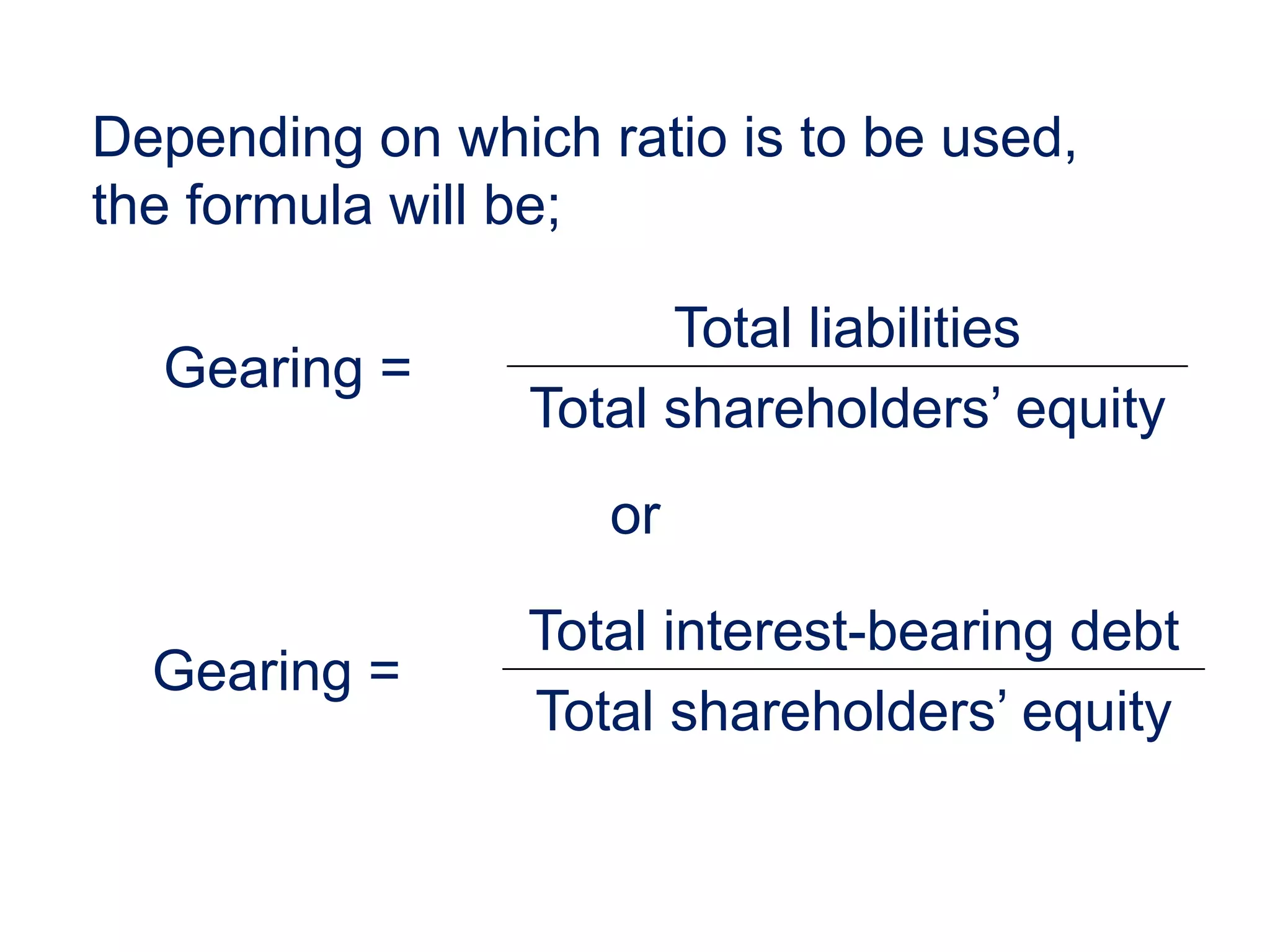

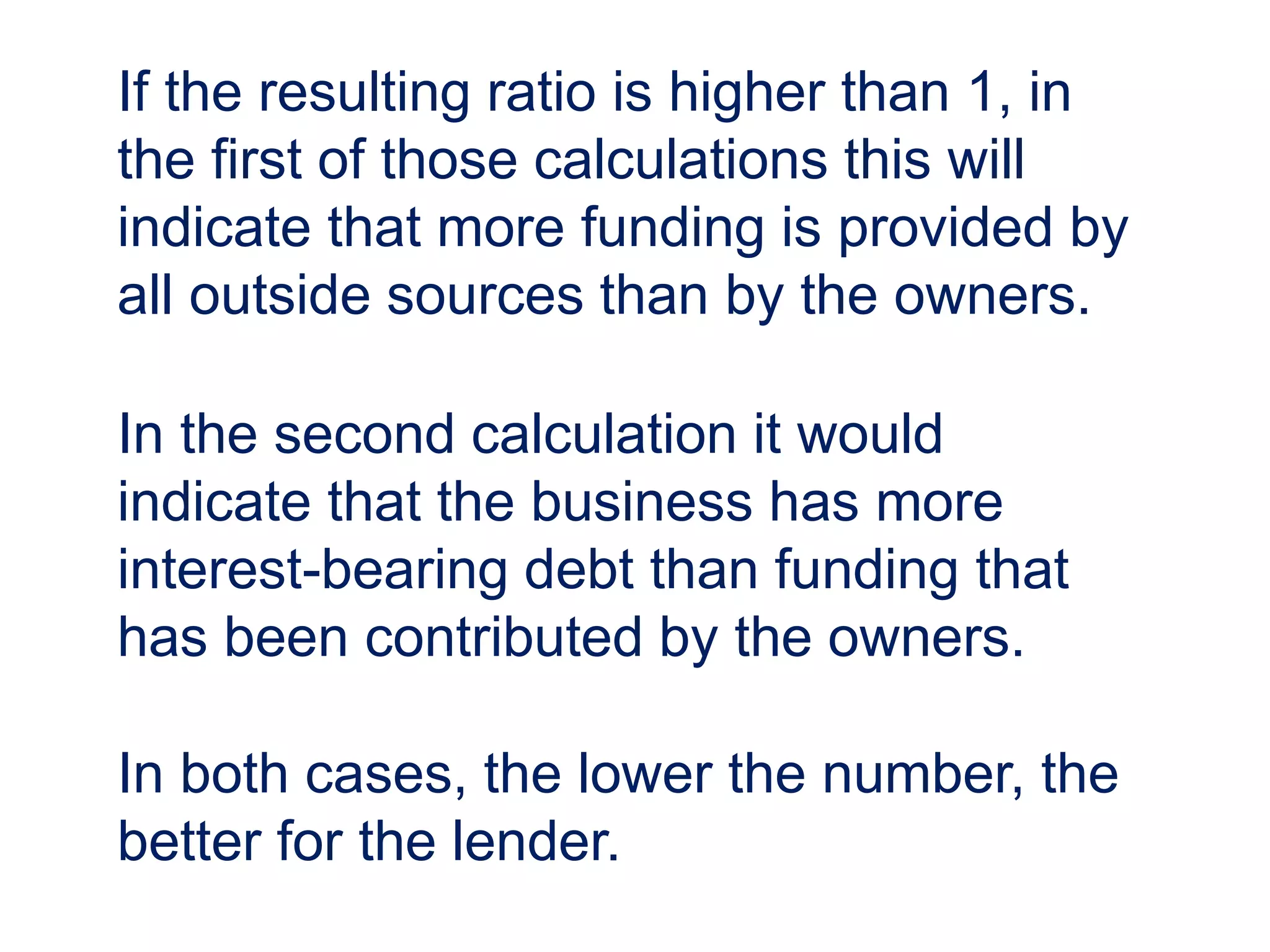

The formula for calculating gearing ratios depends on whether total liabilities or interest-bearing debt is used.

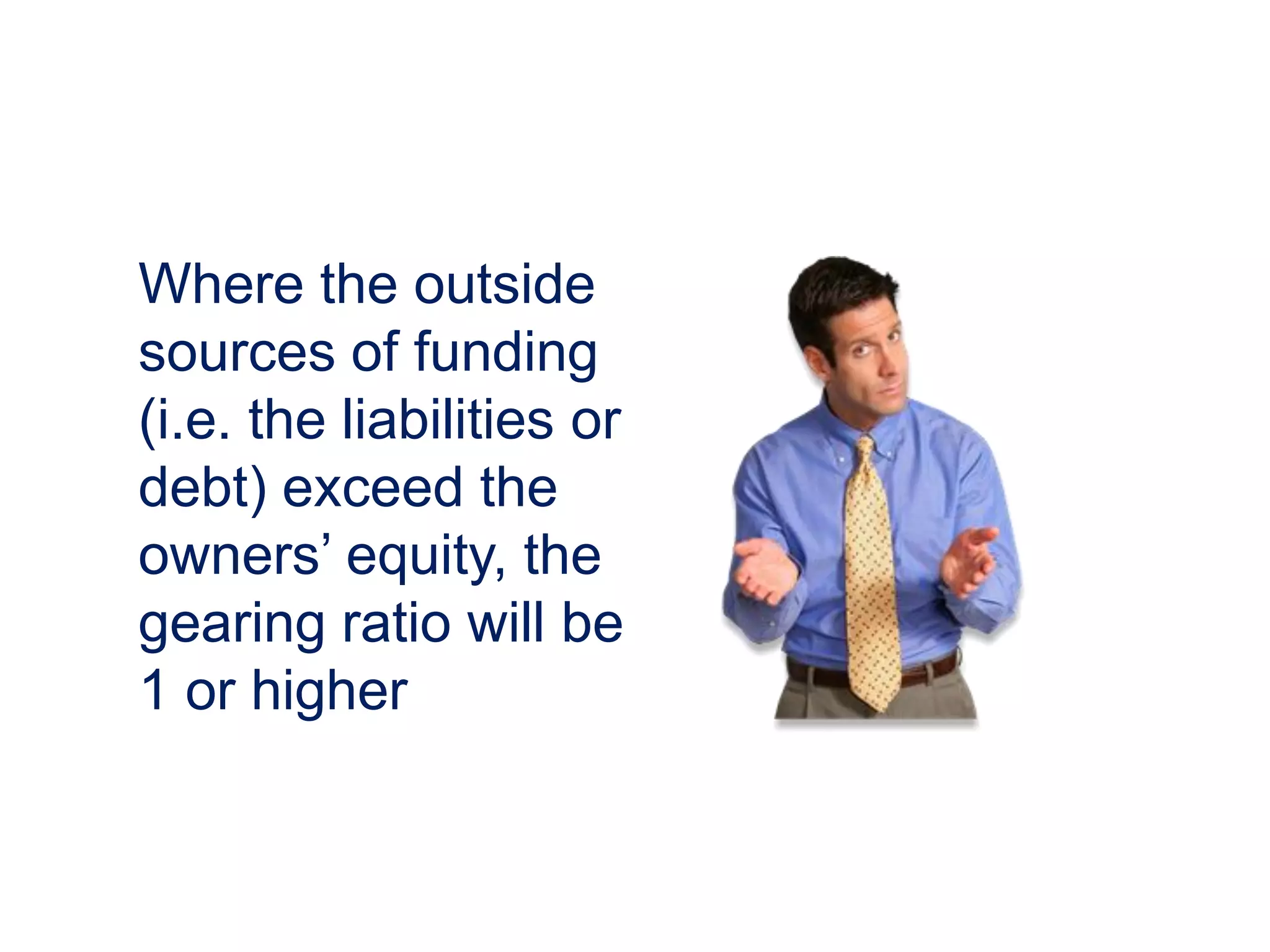

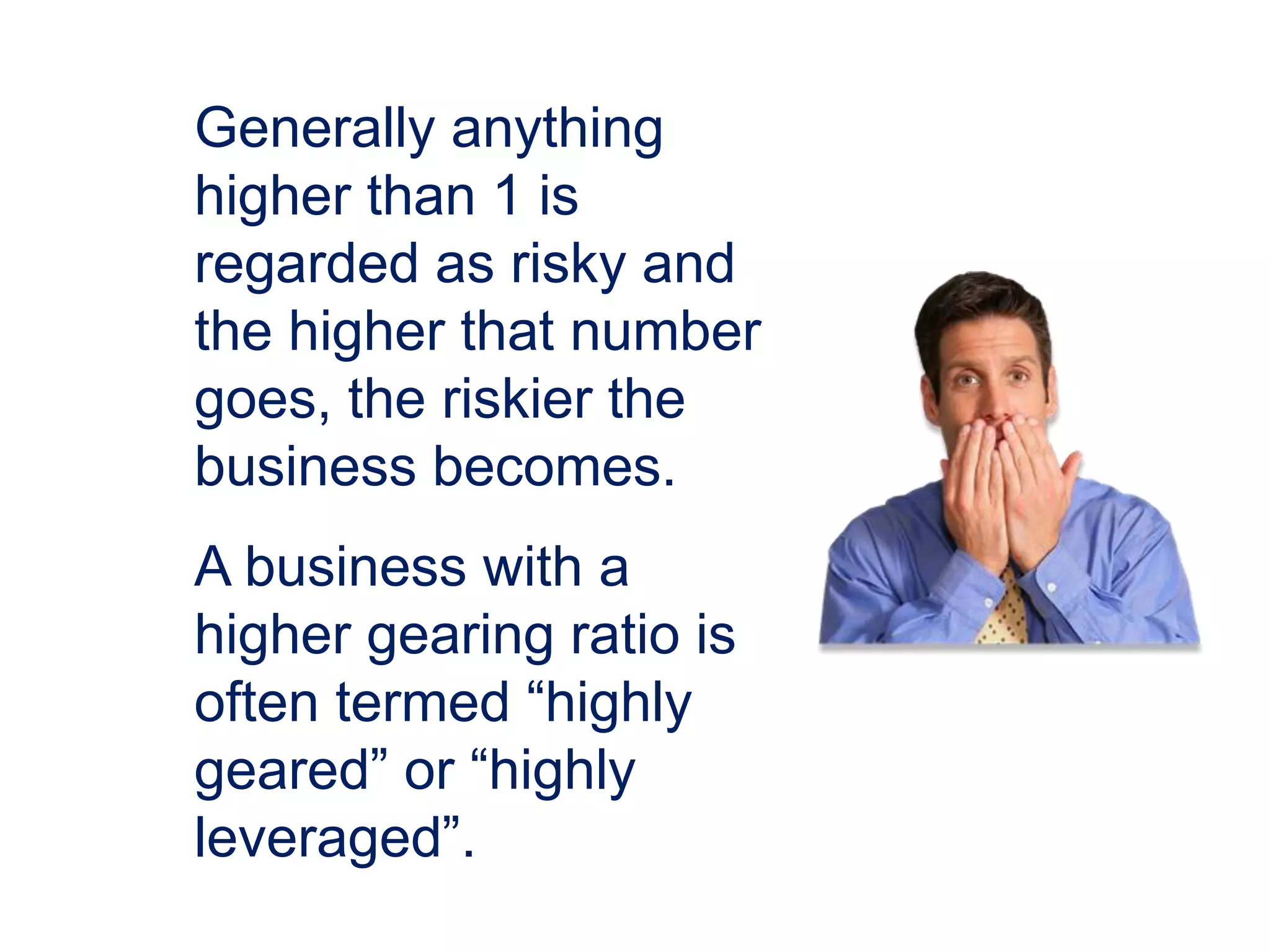

A gearing ratio greater than 1 indicates more outside funding than equity, which is risky for lenders.

Ratios higher than 1 are considered risky, signaling high leverage or gearing.

Intangible assets may be deducted from equity when calculating gearing ratios to assess liquidation value.

There is no universal optimal gearing ratio; it varies based on business type and capital needs.

Businesses needing significant capital typically have higher gearing ratios, while service businesses tend to have lower.

Judging risk based on debt level and consideration of debt duration—shorter debt is riskier than long-term.

Preference shares may be viewed as either equity or debt by lenders, usually treated as interest-bearing debt.

Shareholders' loans are generally considered debt despite appearing as equity on the balance sheet.

Thank you note and links for more business banking resources.