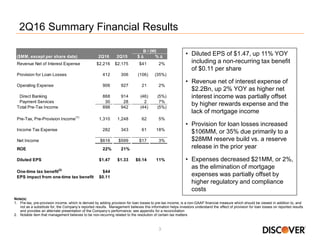

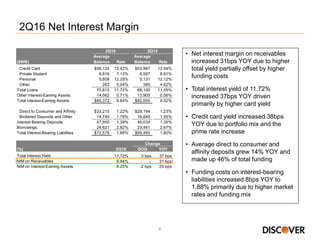

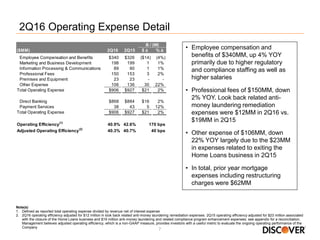

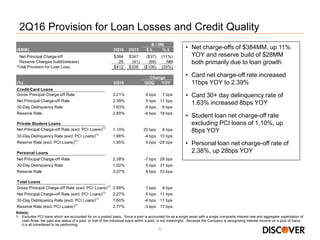

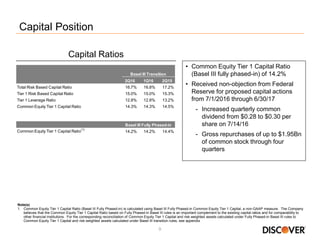

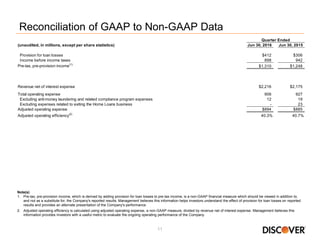

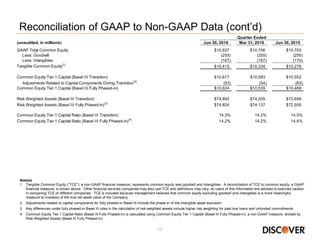

- Discover Financial reported diluted EPS of $1.47 for 2Q16, up 11% YOY, including a one-time $0.11 tax benefit. Revenue was $2.2 billion, up 2% YOY, as higher net interest income was offset by higher rewards expenses and lack of mortgage income. Provision for loan losses increased 35% to $412 million due to loan growth and a $28 million reserve build.